Vietnam

We remain bullish on the alpha-generating potential of Vietnamese stocks over the medium and long term. But our negative outlook on global/EM beta makes us bearish on this bourse in absolute terms over the medium term.

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

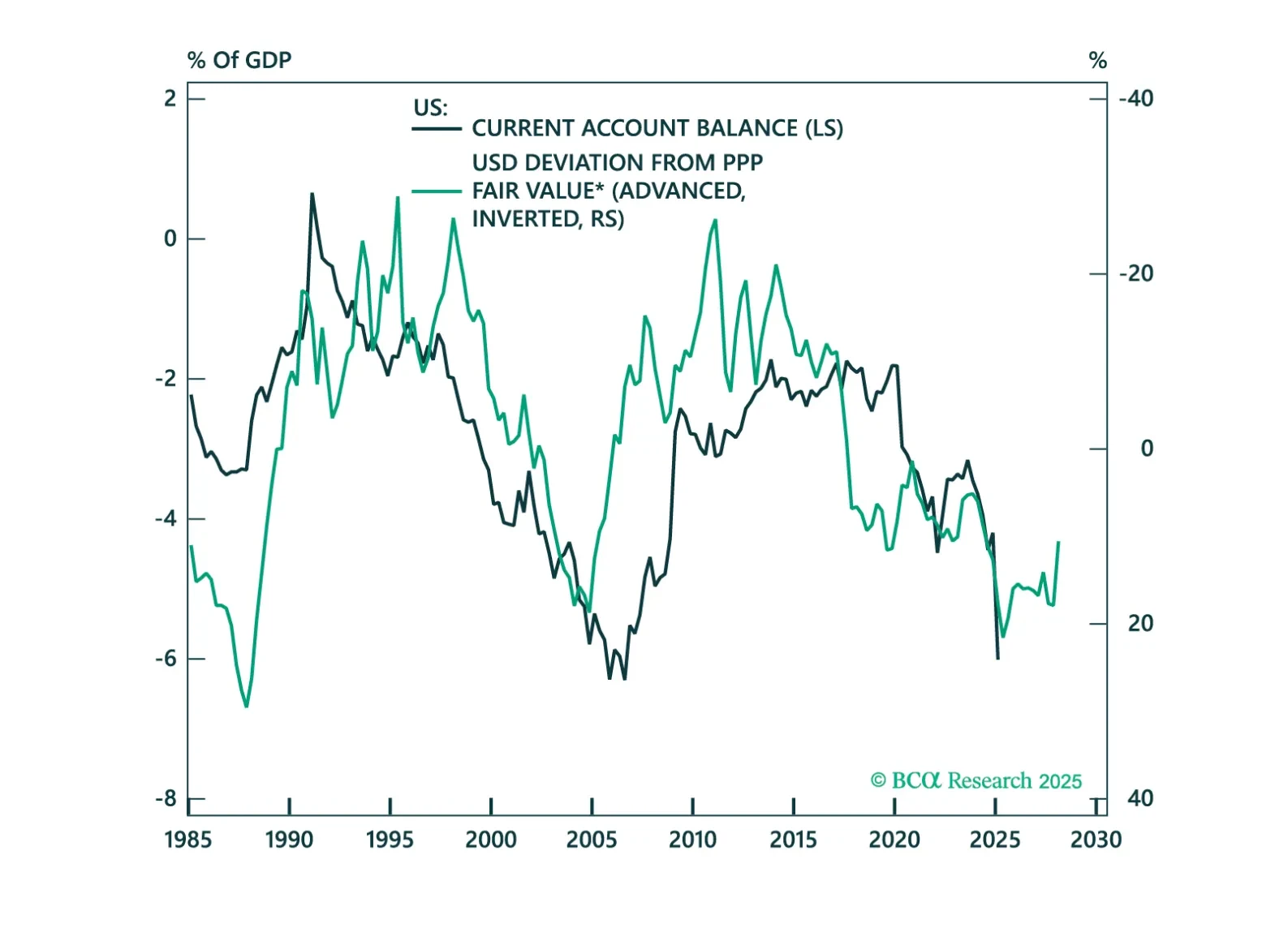

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

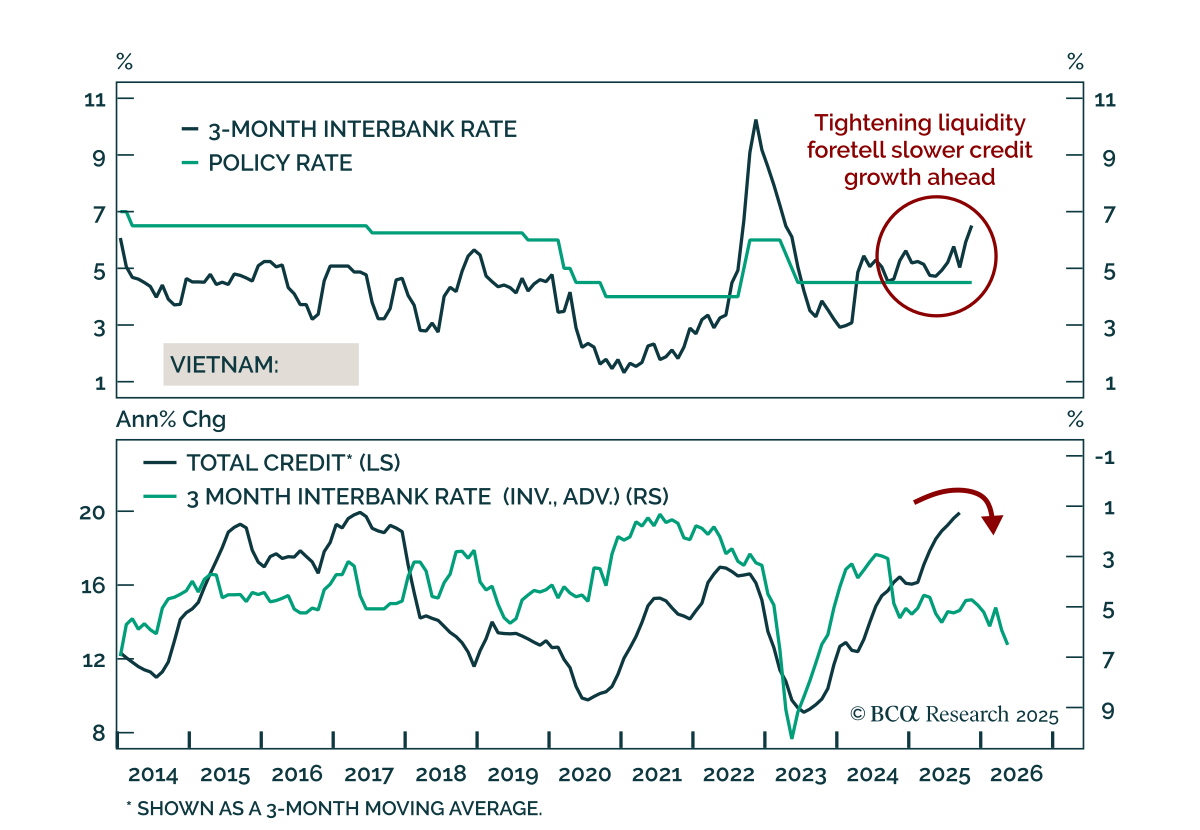

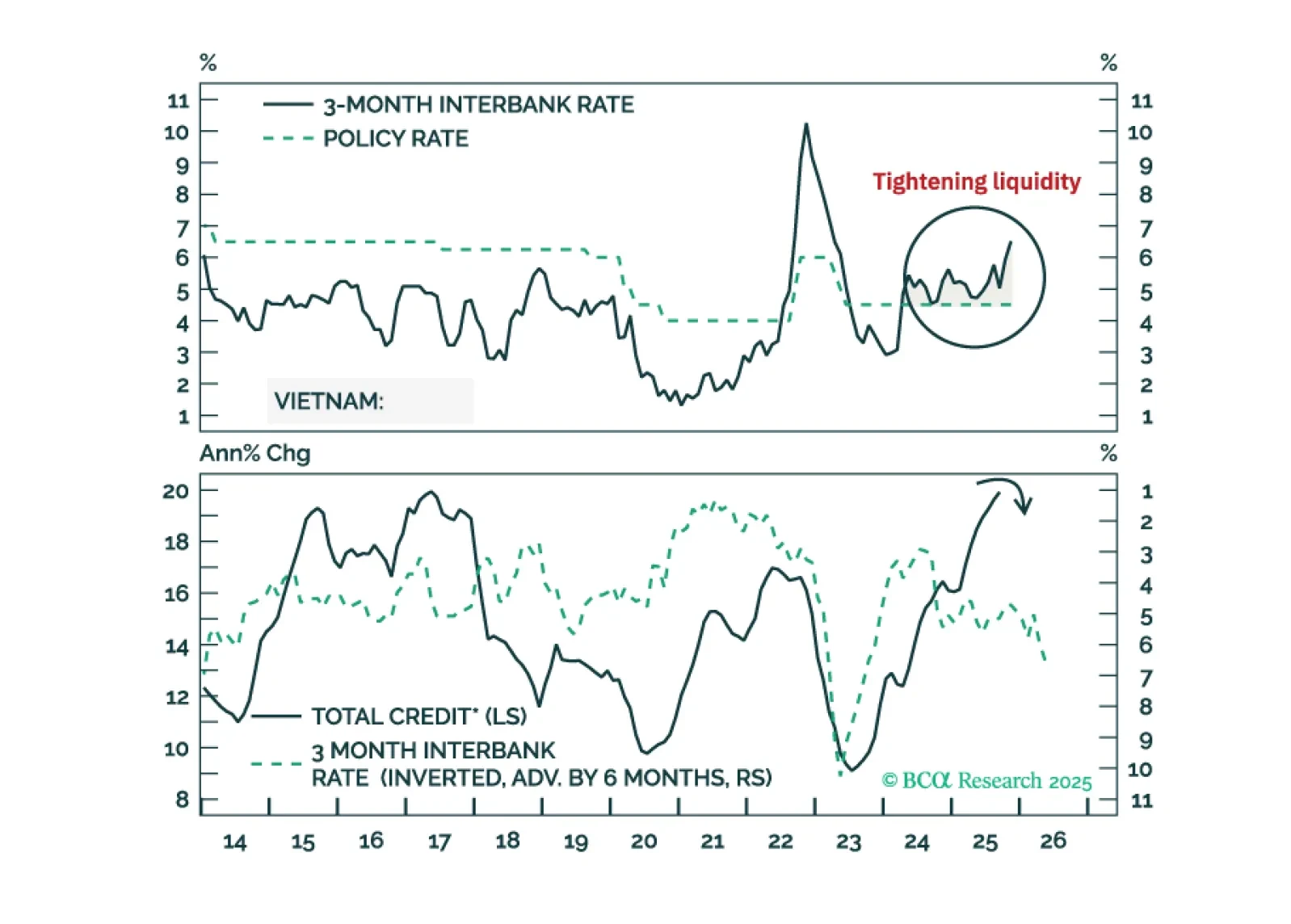

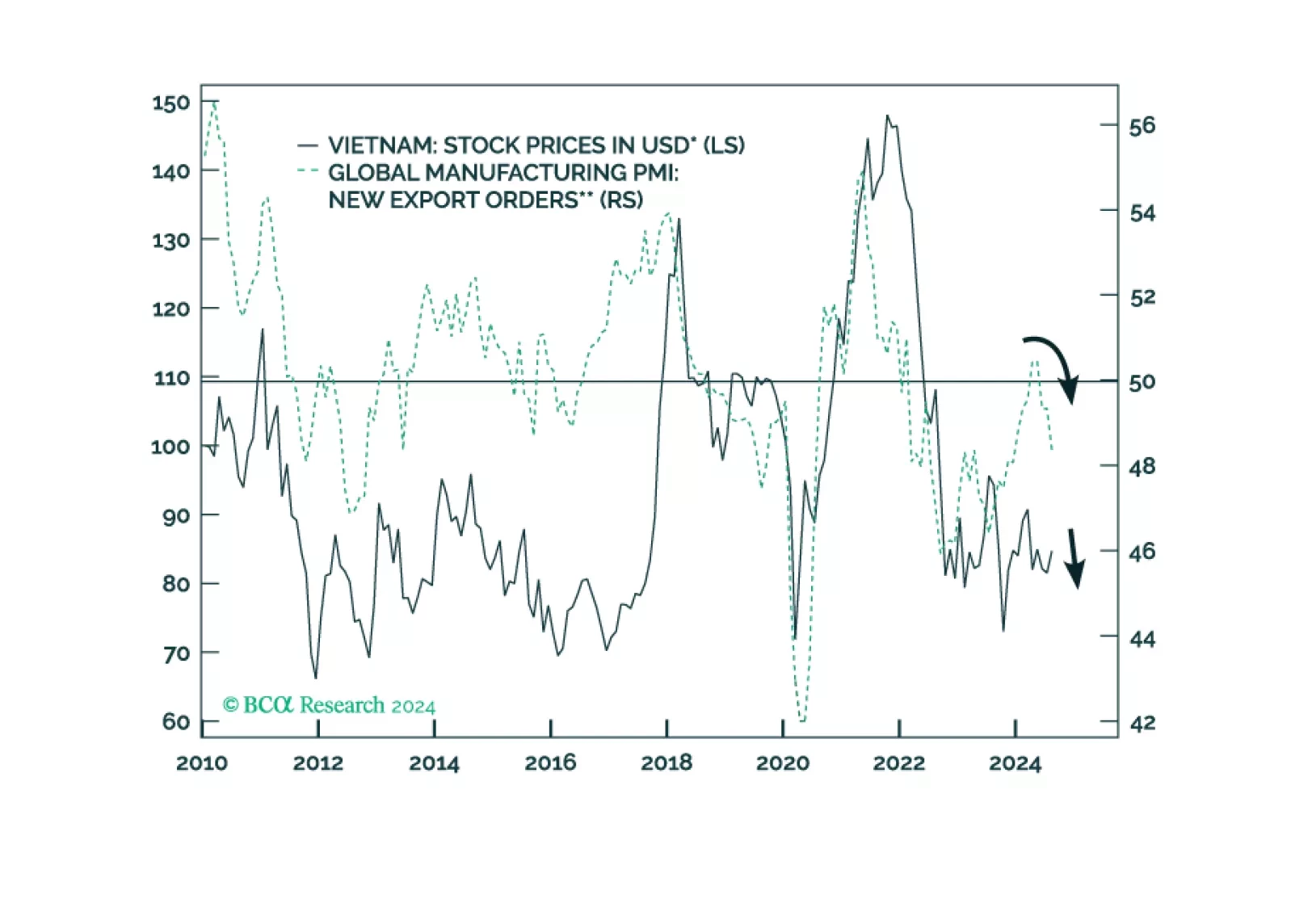

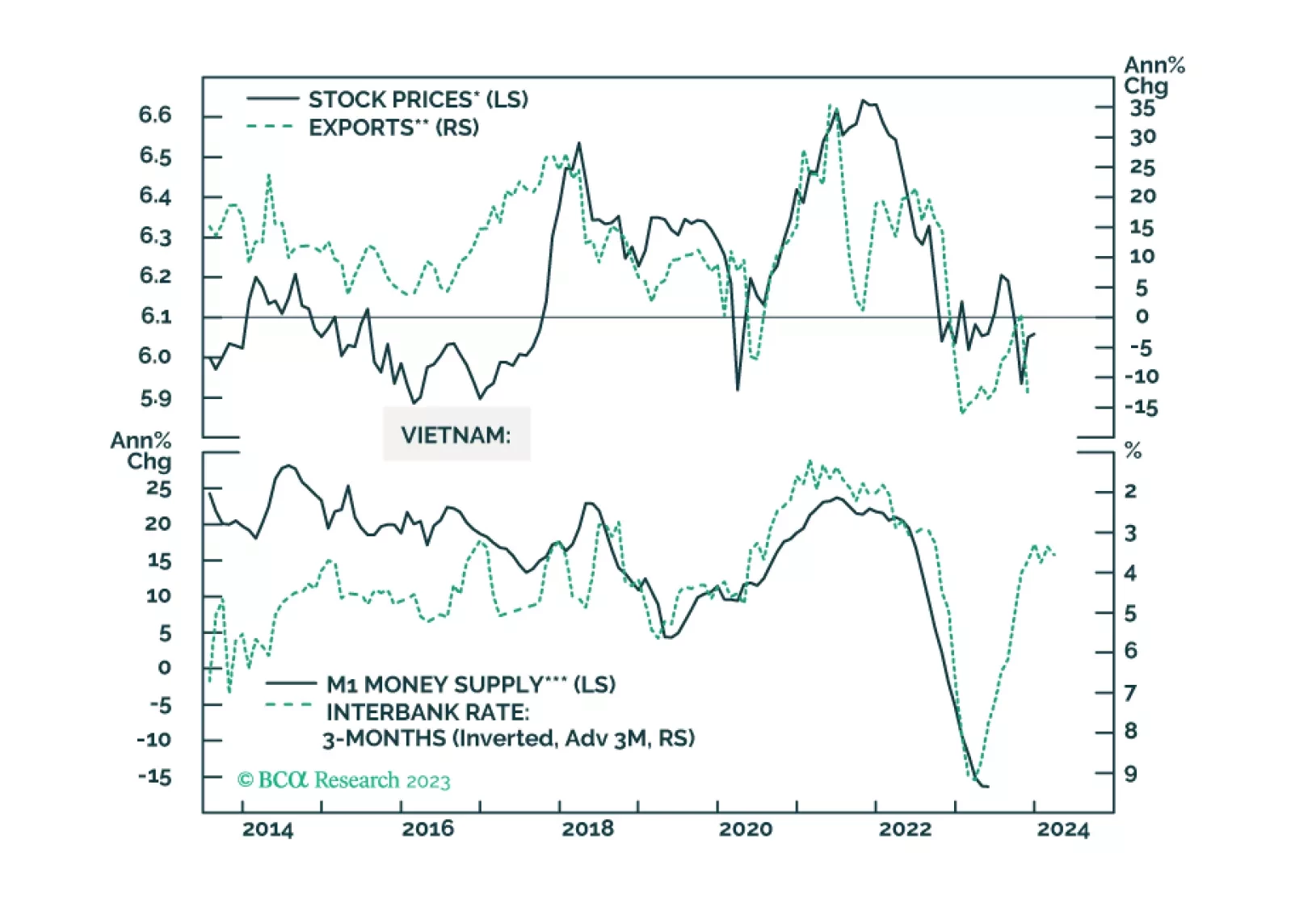

The Vietnamese economy is growing at a strong 7%. Why, then, are Vietnamese stocks struggling? Should investors expect a revival soon?

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

Great Power Rivalry is taking another leg up as Russia and China further align their geopolitical interests. Investors should stay long USD-CNY, favor defensives over cyclicals, and markets like North America and DM Europe that have less exposure to geopolitical risk.