Valuations

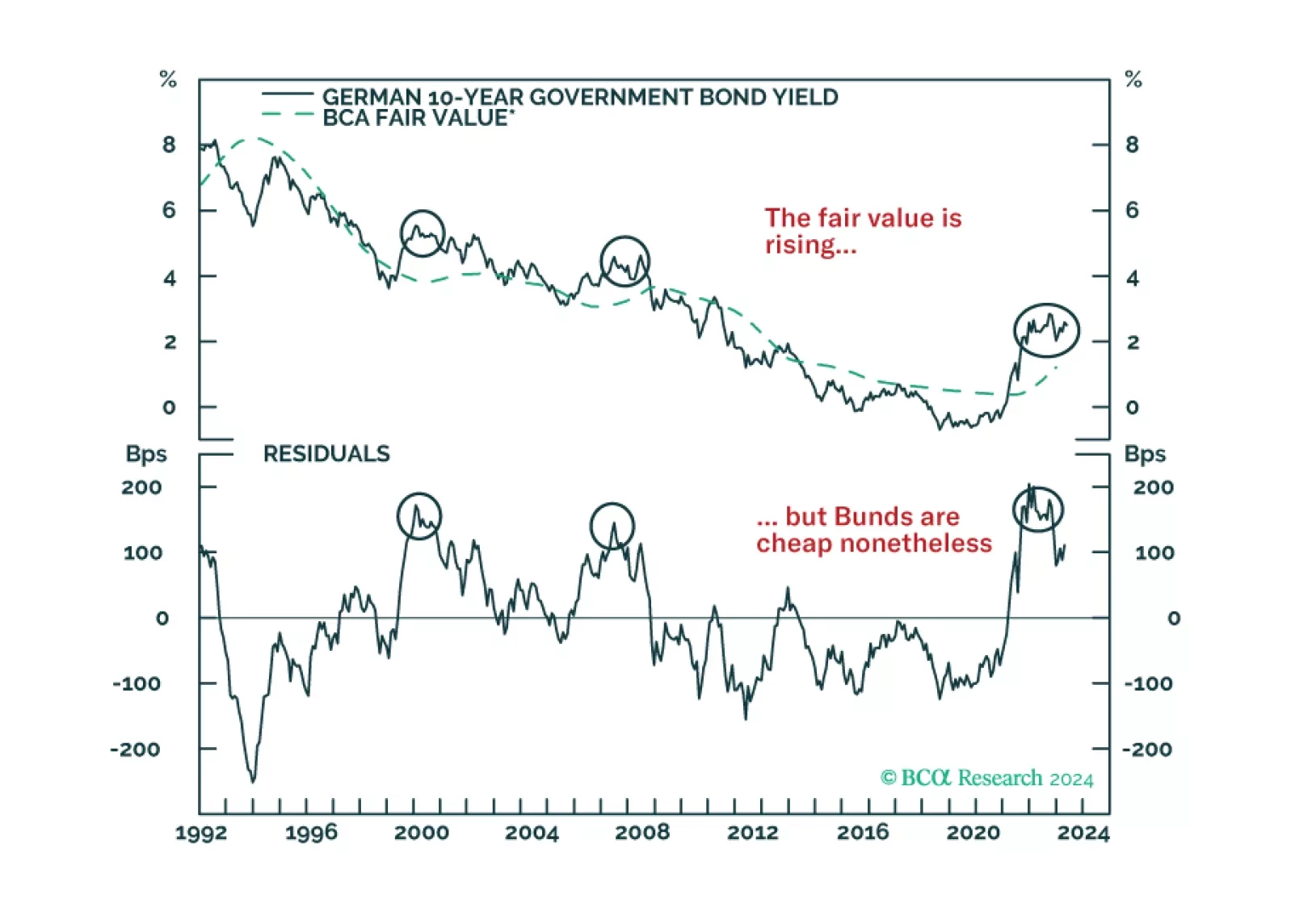

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

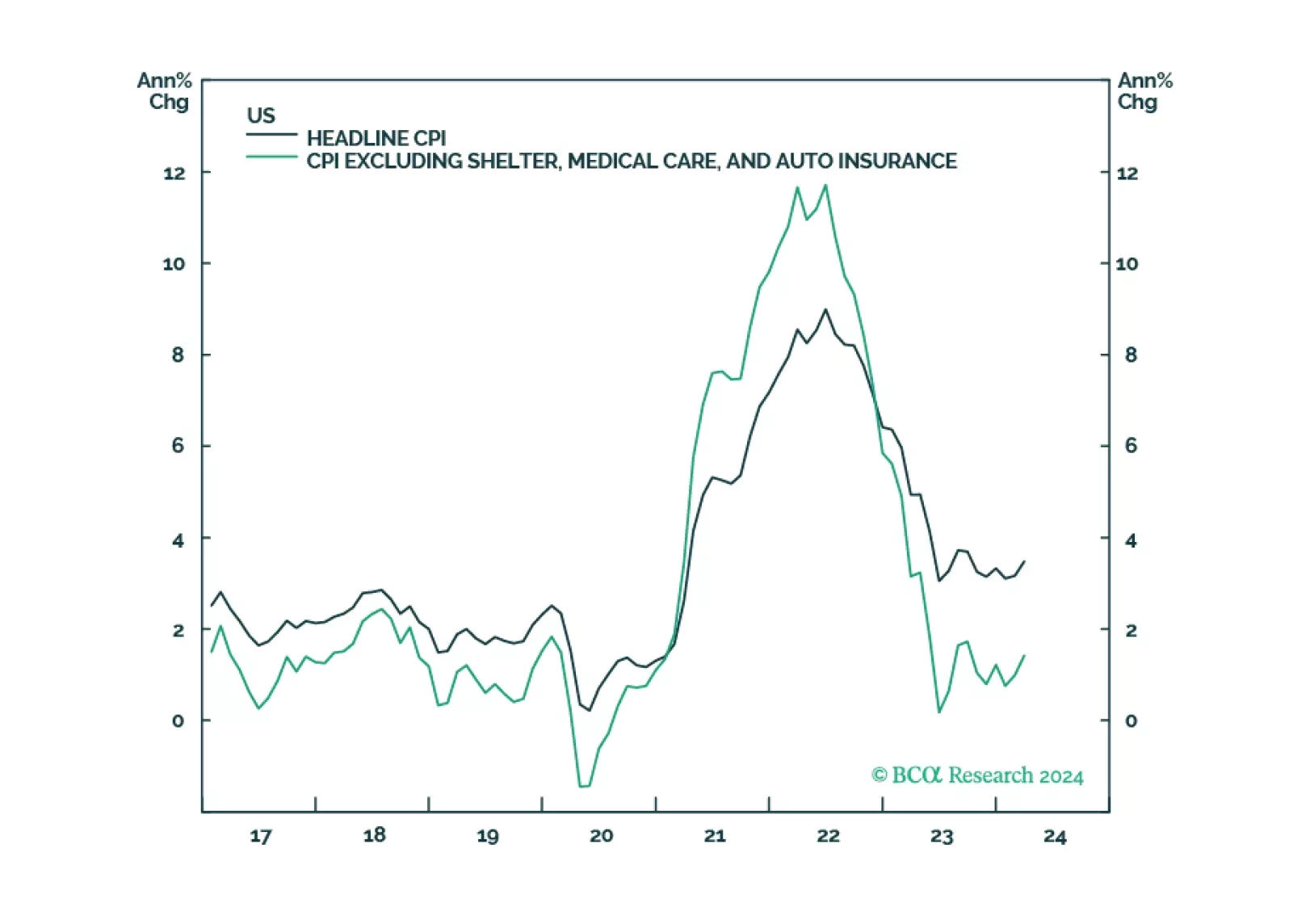

In this week’s report, we defend four out-of-consensus claims. Claim #1: Underlying inflation in the US is not reaccelerating. Claim #2: The US labor market is set to weaken abruptly. Claim #3: The S&P 500 will drop to 3700 in 2025. Claim #4: Japan is not in danger of a currency crisis.

The broad market took a significant step backward in April, as market jitters gripped investors, stoking fears of higher for longer monetary policy. However, our roundtable investor poll has demonstrated that the majority remain constructive on equities, and have plenty of cash ready to be invested, which could prolong the rally. Economic data is deteriorating while inflation is stubborn. However, so far, bad news is good news as many believe that a “Fed put” is still on.

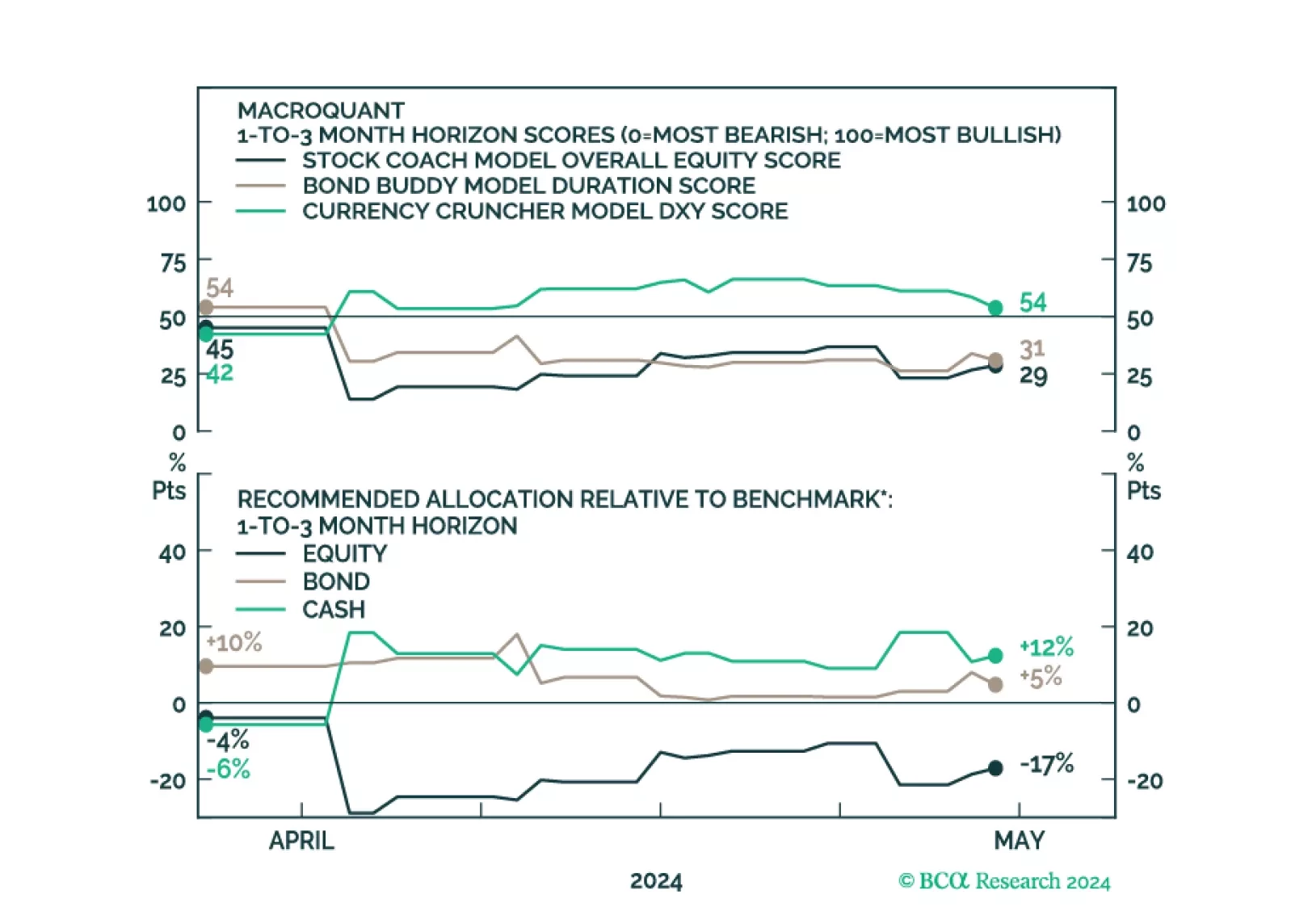

MacroQuant downgraded equities from neutral to underweight on a 1-to-3 month horizon. The model suggests increasing exposure to cash.

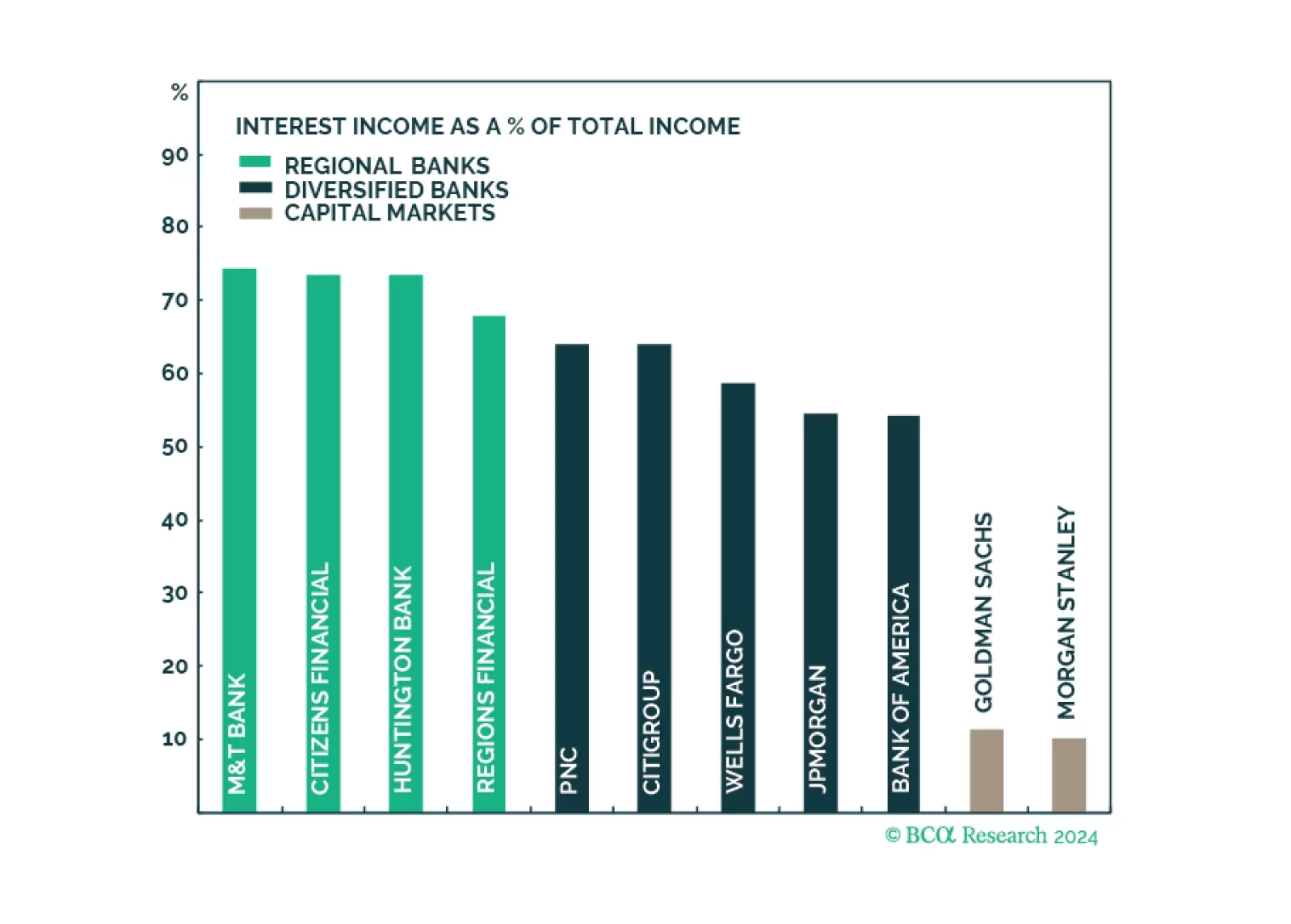

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.

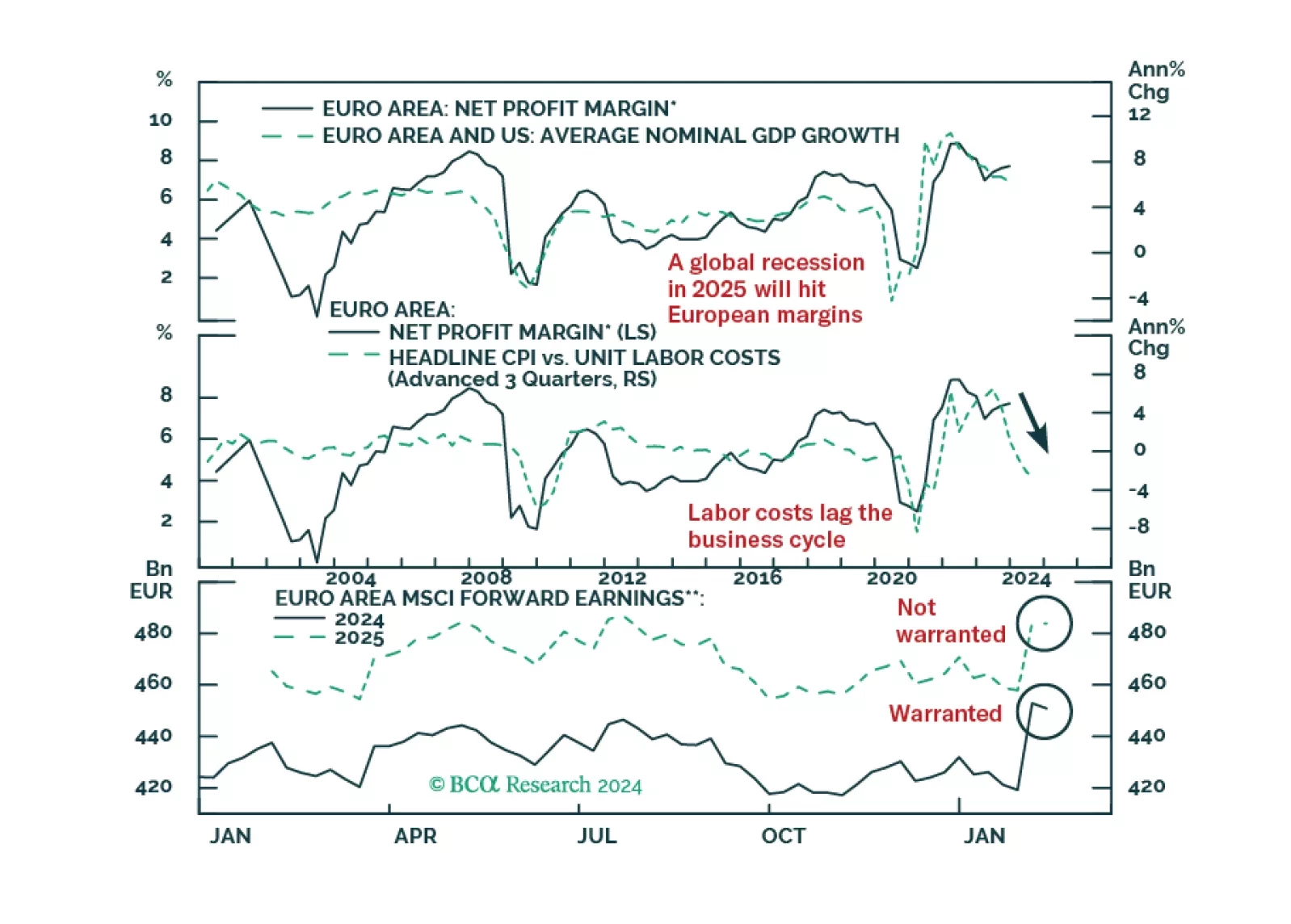

European profits margins are elevated. Will a mild recession be enough to bring them down?

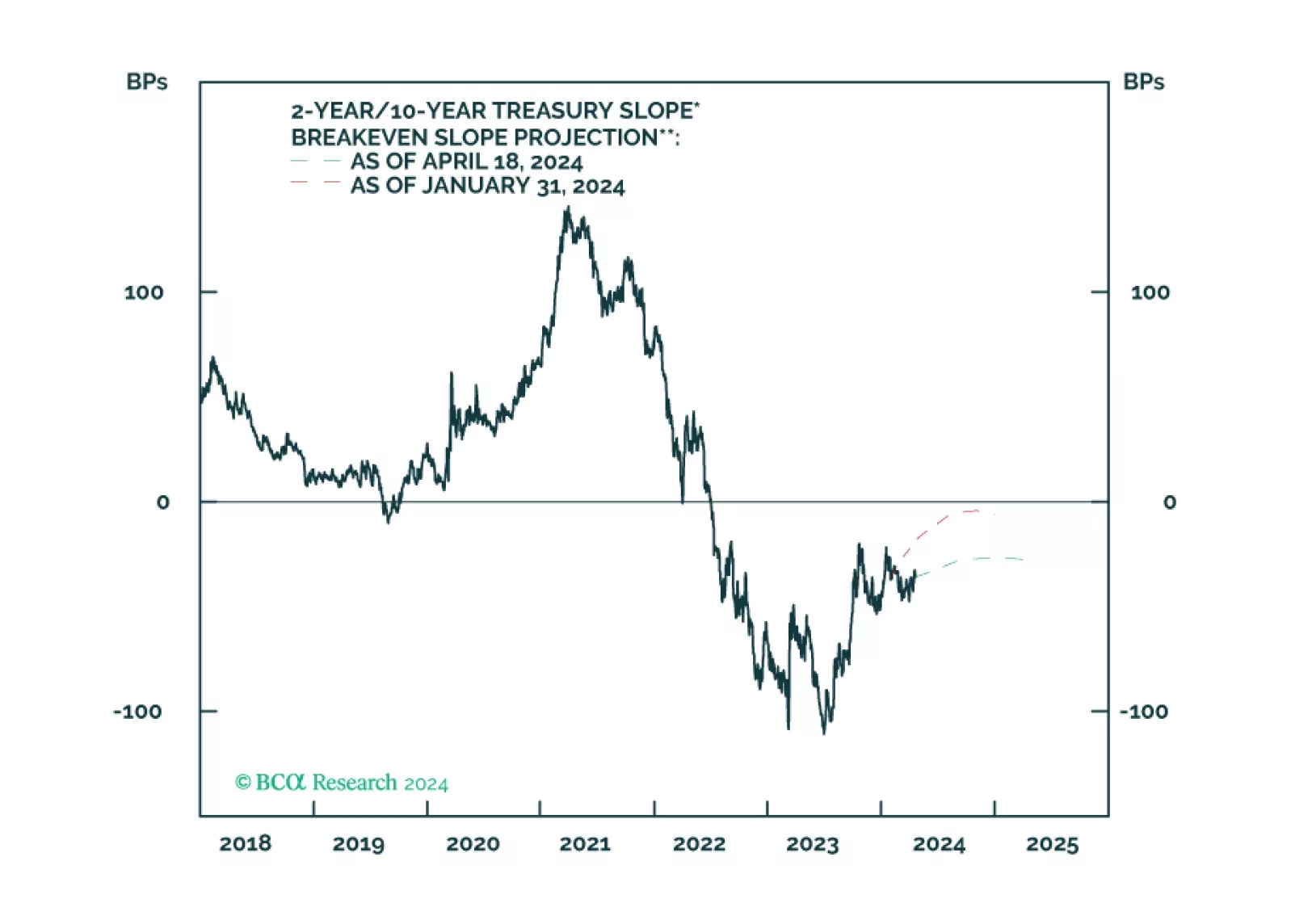

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

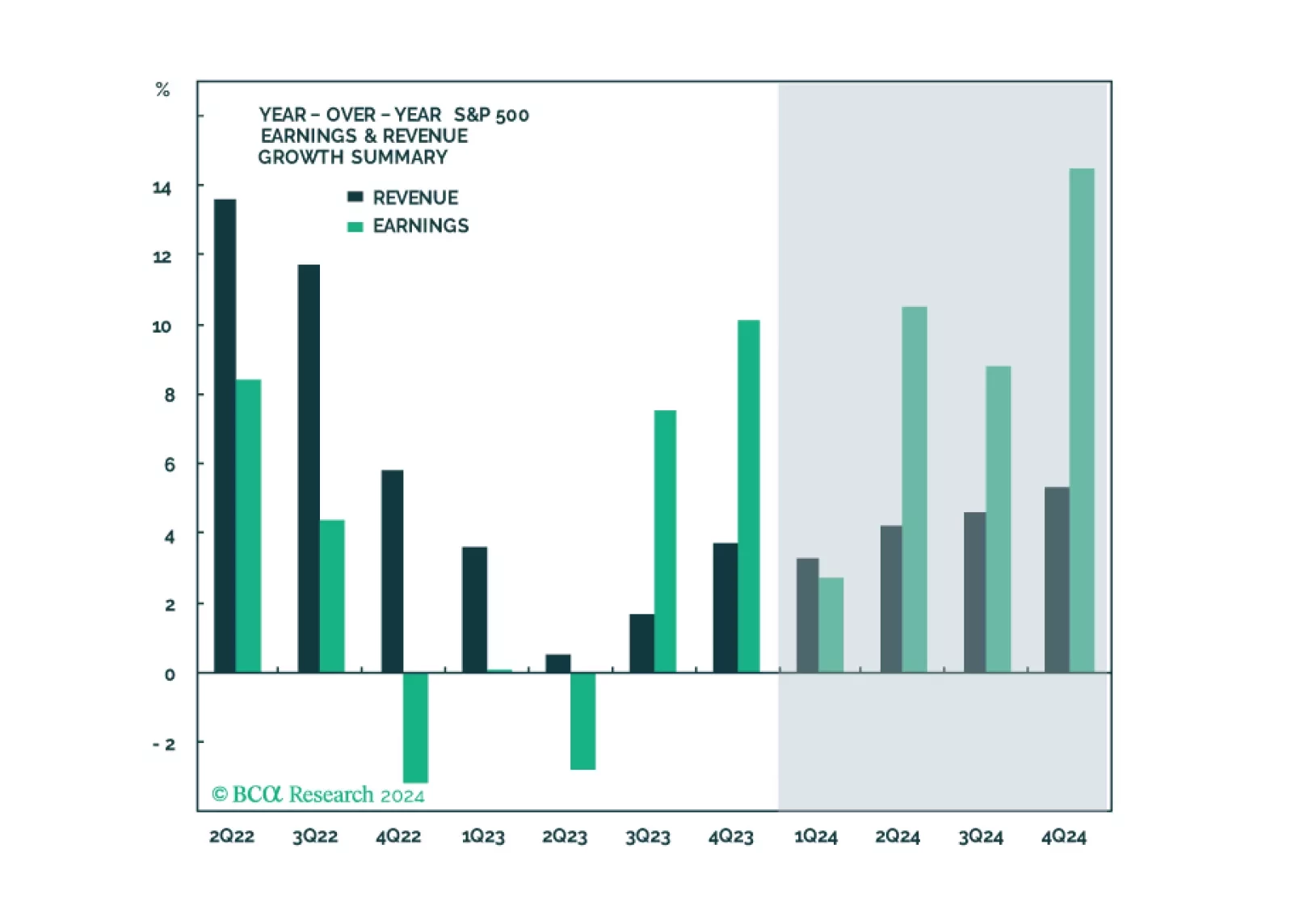

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.

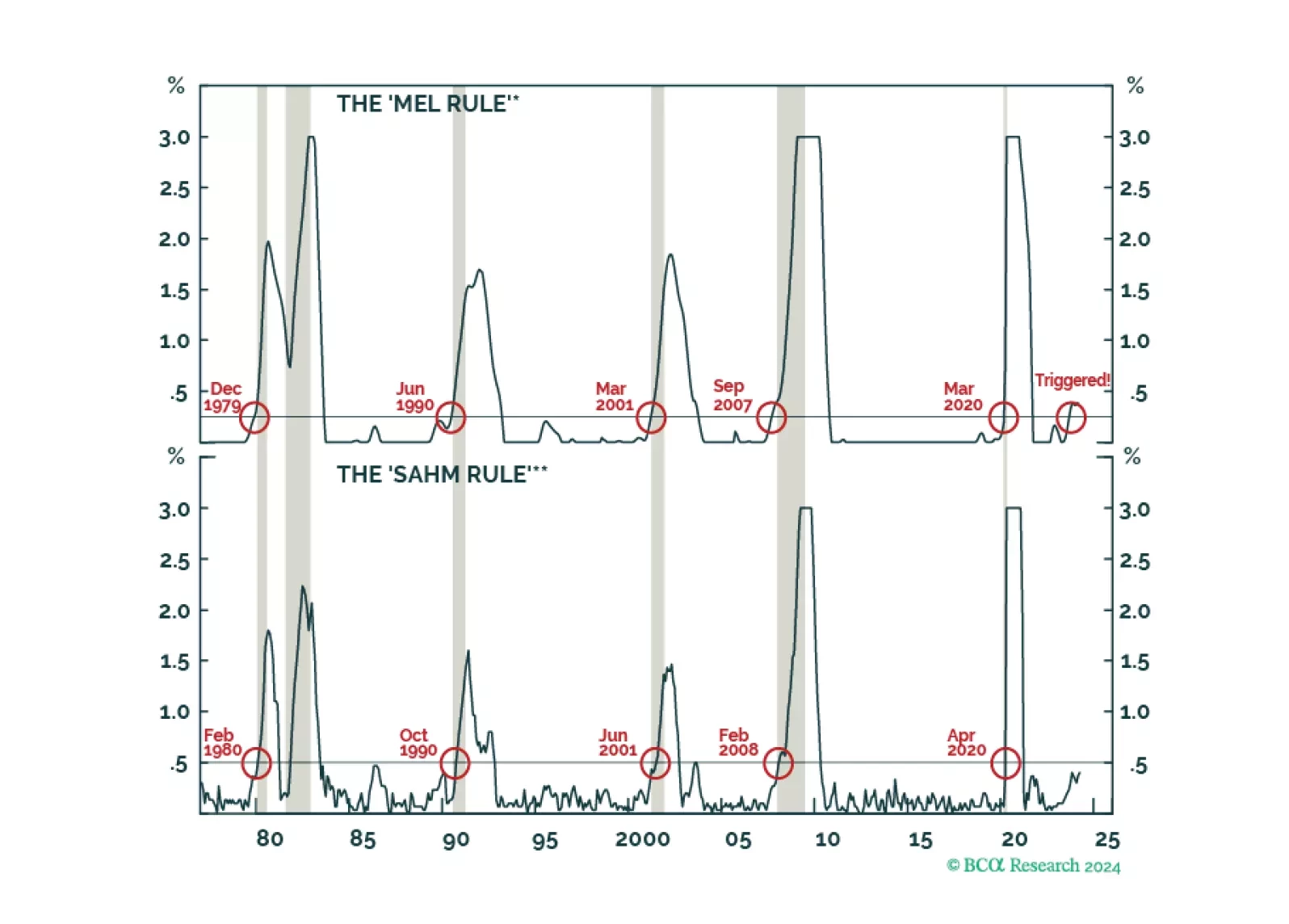

Contrary to conventional wisdom, most leading indicators suggest that the US labor market is weakening, including our very own “Mel rule.” After being overweight stocks last year, we moved to neutral at the start of 2024, and are now putting equities on downgrade watch with the expectation of shifting them to underweight later this year.