United States

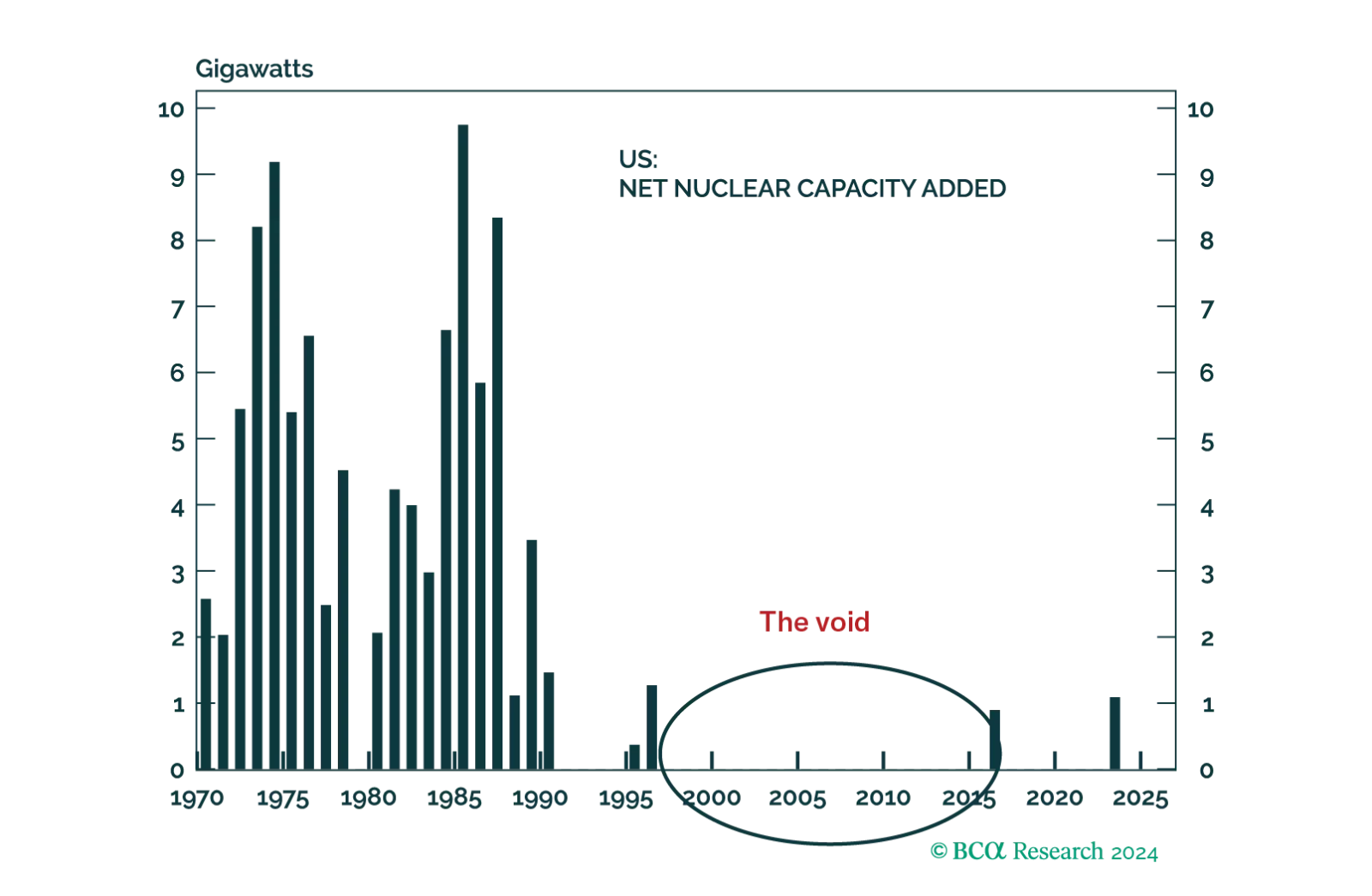

US nuclear energy is in a state of decay. The industry lacks standardization, making it expensive and timely to deploy new nuclear energy projects. Policy support is also lacking compared to other energy sources. Public opinion on nuclear energy is warming but will do little for commercial uptake – investors still face massively high startup costs. Meanwhile, competition is heating up. China is fast approaching the global top spot with its grand nuclear energy strategy. For once, the US may not be the best investment case we have all come to know.

We consider the possibility that lower interest rates could lead to an increase in household borrowing, prolonging the economic recovery.

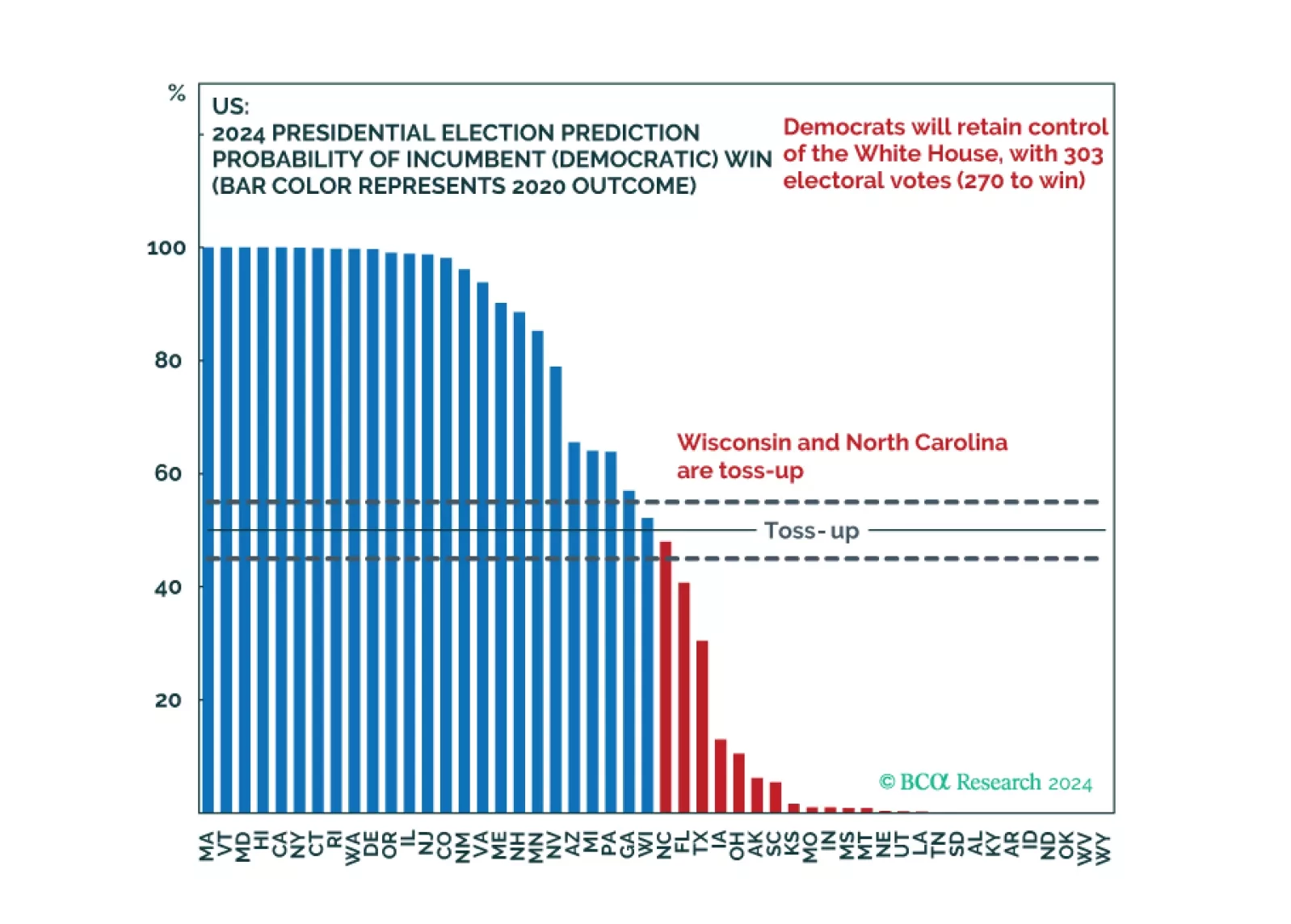

Our quant model shows Democrats winning the election at a 56% probability, with 303 electoral college votes. But swing state economies are slowing and Democrats’ odds in Michigan fell. Trump can win with Georgia, Michigan, plus one other state. Neither the Fed nor China’s stimulus should reduce one’s odds of a Republican upset.

Markets are rallying on Fed rate cuts and China stimulus but there will also be October surprises ahead of the US election, which Trump could still win. Russia’s conflict with the West is escalating and the Middle East is destabilizing further. Investors should favor US bonds but they should add some risk in emerging markets in response to China’s policy turn.