United Arab Emirates

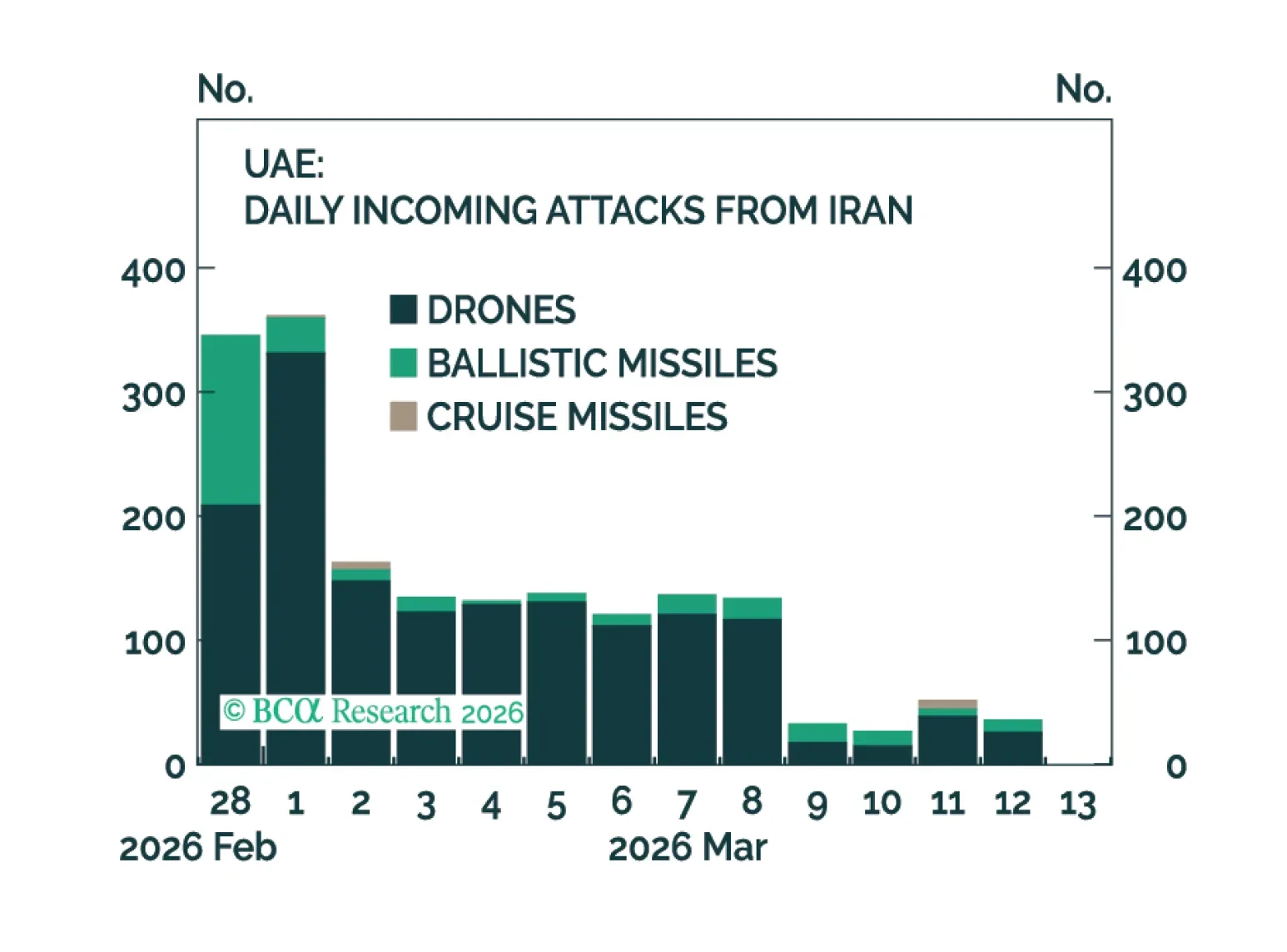

The conflict in the Middle East persists as the US and Israel keep striking at Iranian military and internal security sites, and Iran has responded with its own missiles and drones against the Gulf States. Although the pace of Iranian retaliation has declined, it appears to have stabilized, as evidenced by attacks against the UAE.

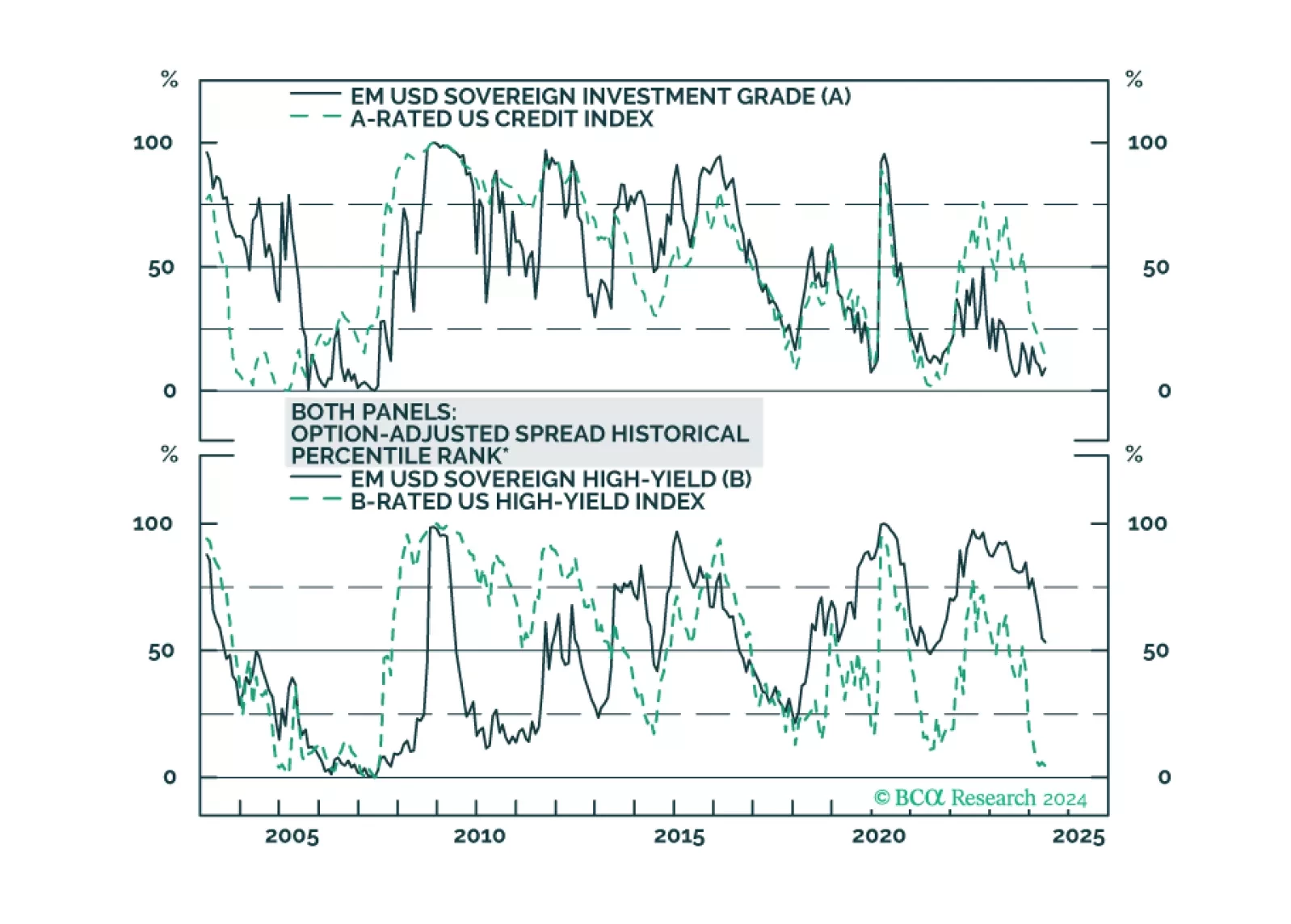

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

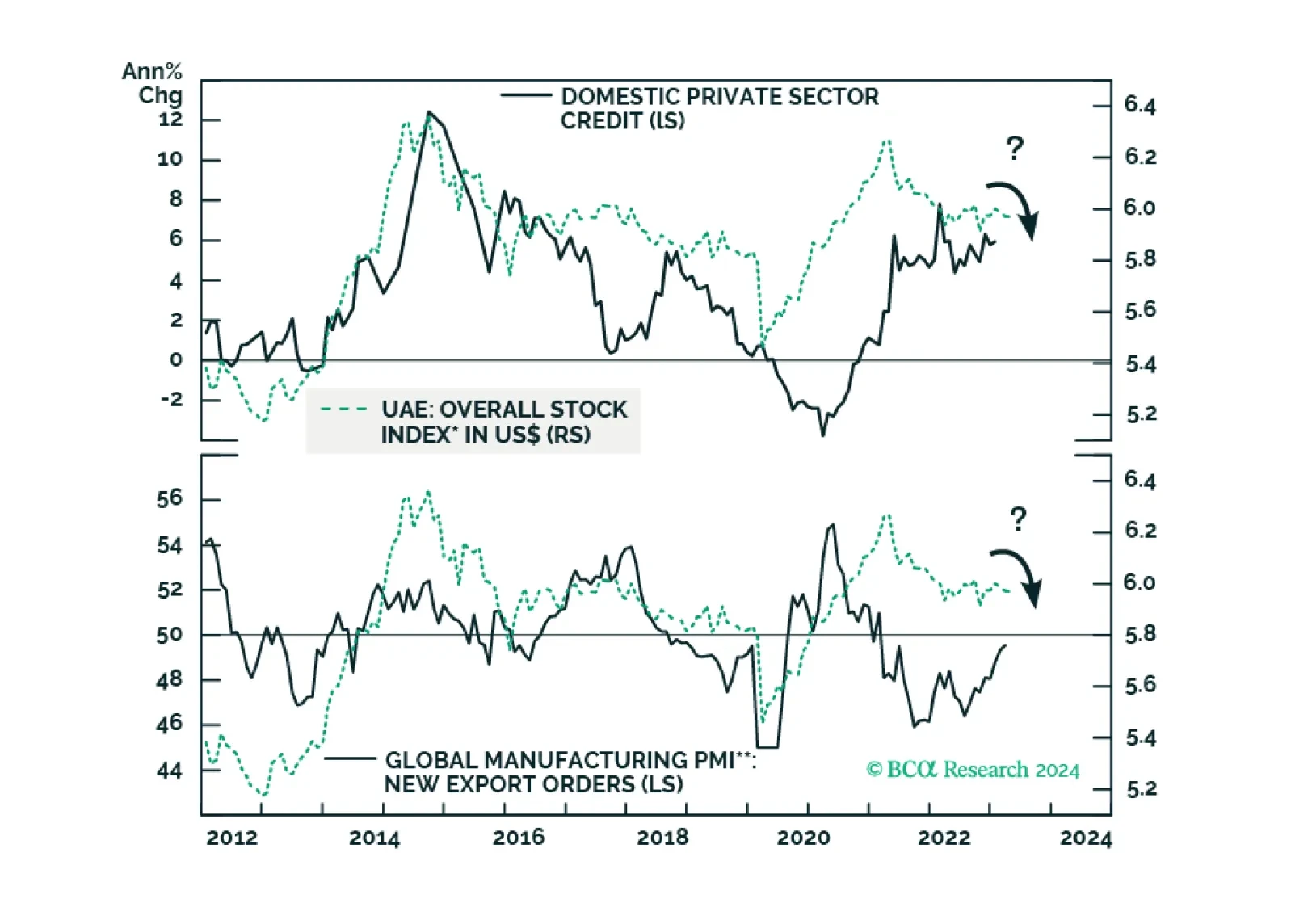

Subdued credit growth and weak global trade will remain headwinds for Emirati stocks. Surging property prices, which have led to a boom in real estate stocks, will also peak soon. Stay neutral on this bourse. Sovereign credit investors, however, should stay overweight UAE in EM credit portfolios.

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

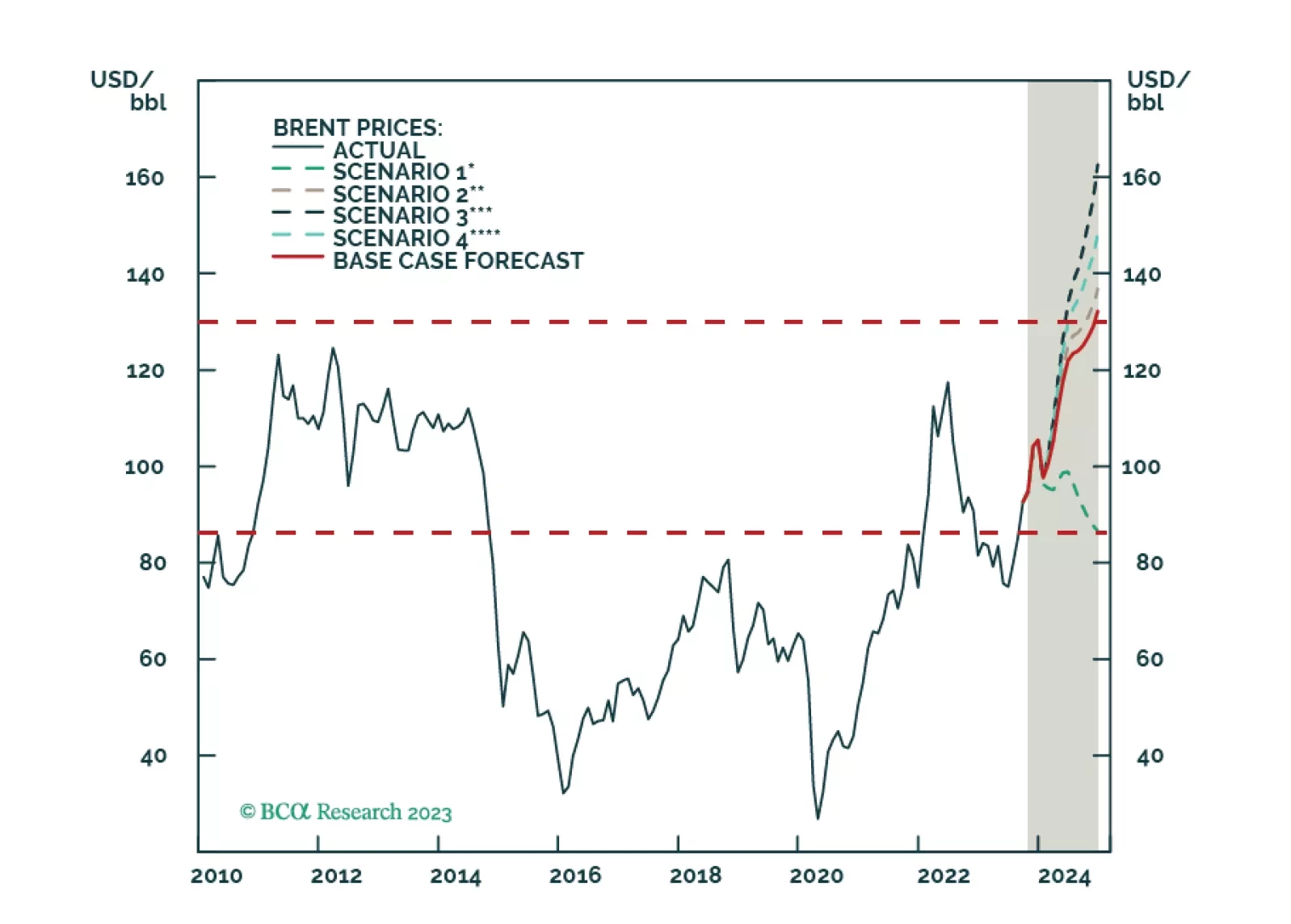

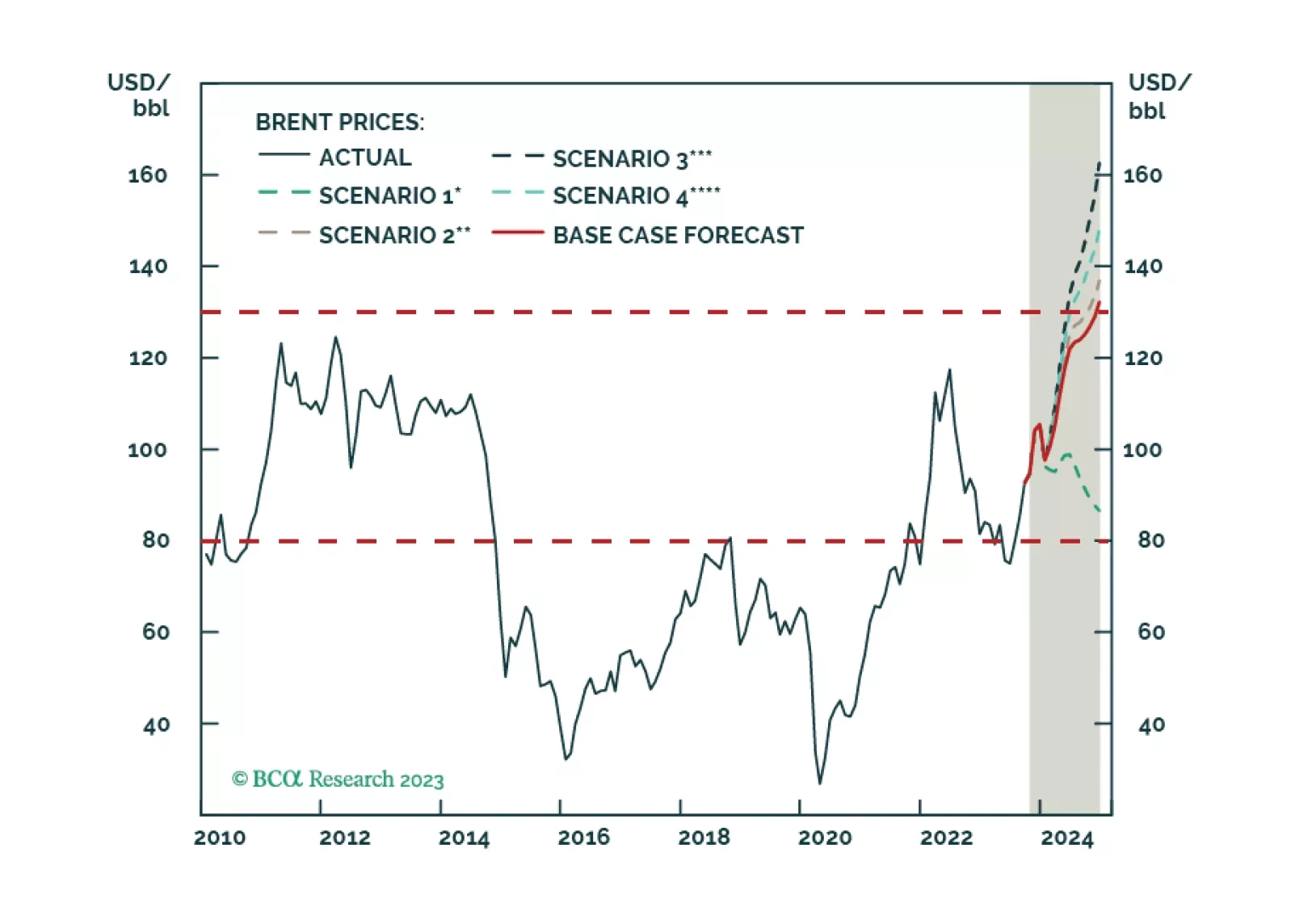

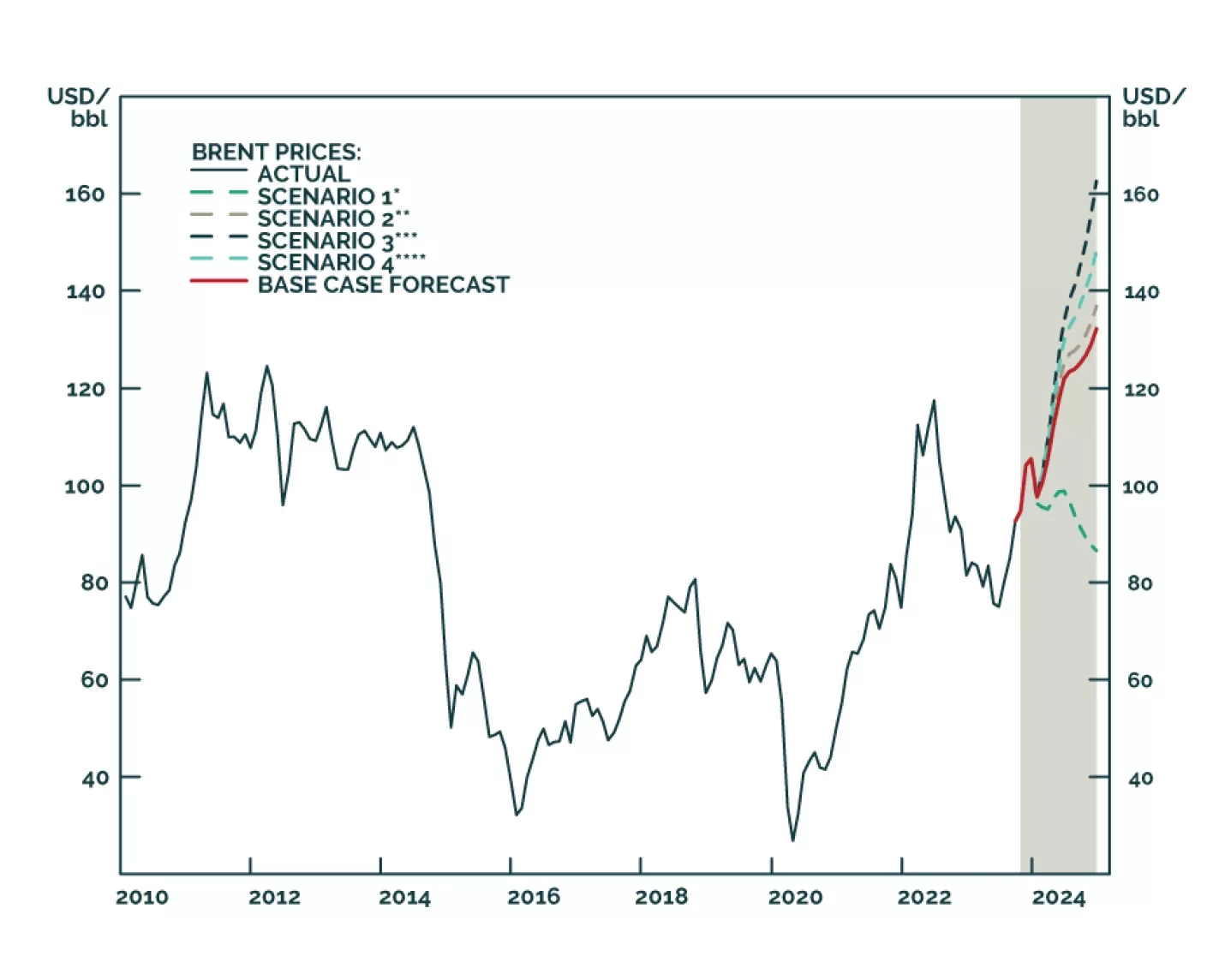

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

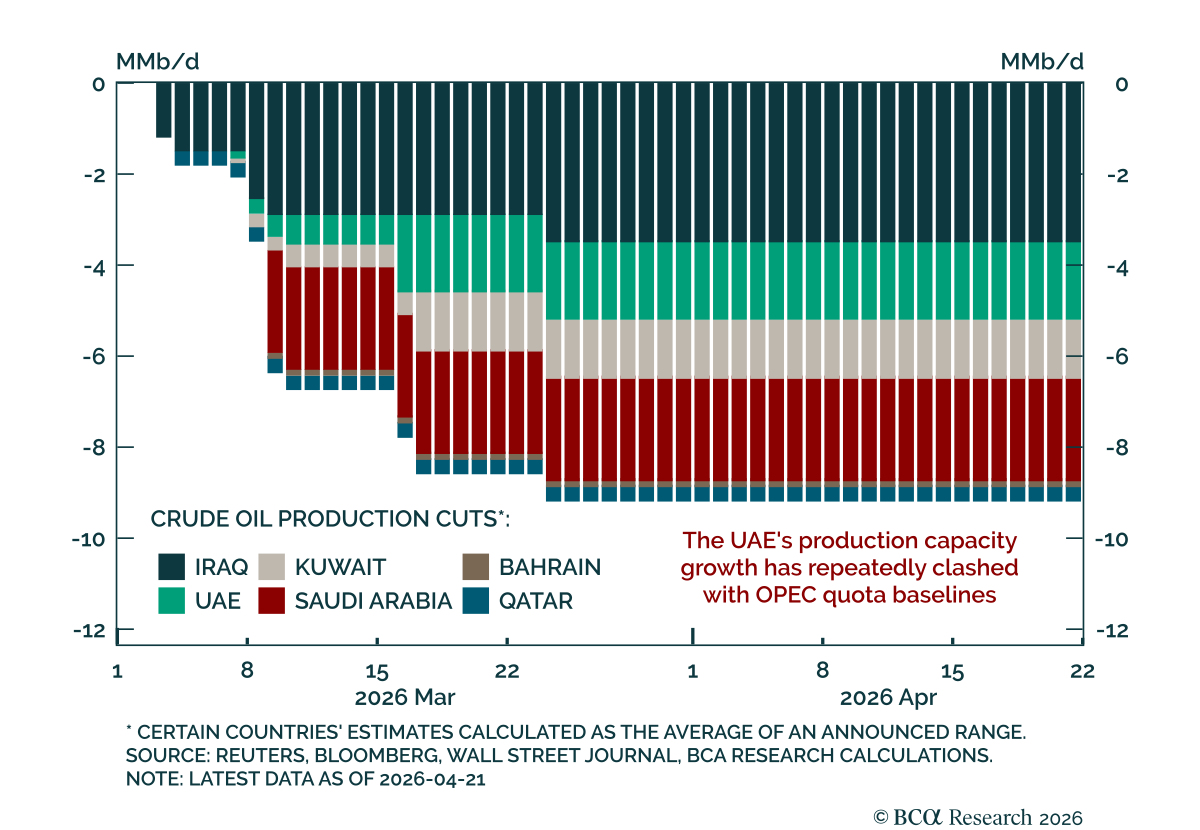

Following this weekend’s OPEC 2.0 meeting, KSA announced a 1mm b/d crude output cut, slated for this July or August, as it attempts to support weak oil prices. The new output quotas, reduced to reflect members’ weak crude oil production will continue until end-2024. UAE’s quota was the only one raised in acknowledgement of its higher production capacity. On the back of this announcement, we continue to expect brent prices will average $90/bbl this year.