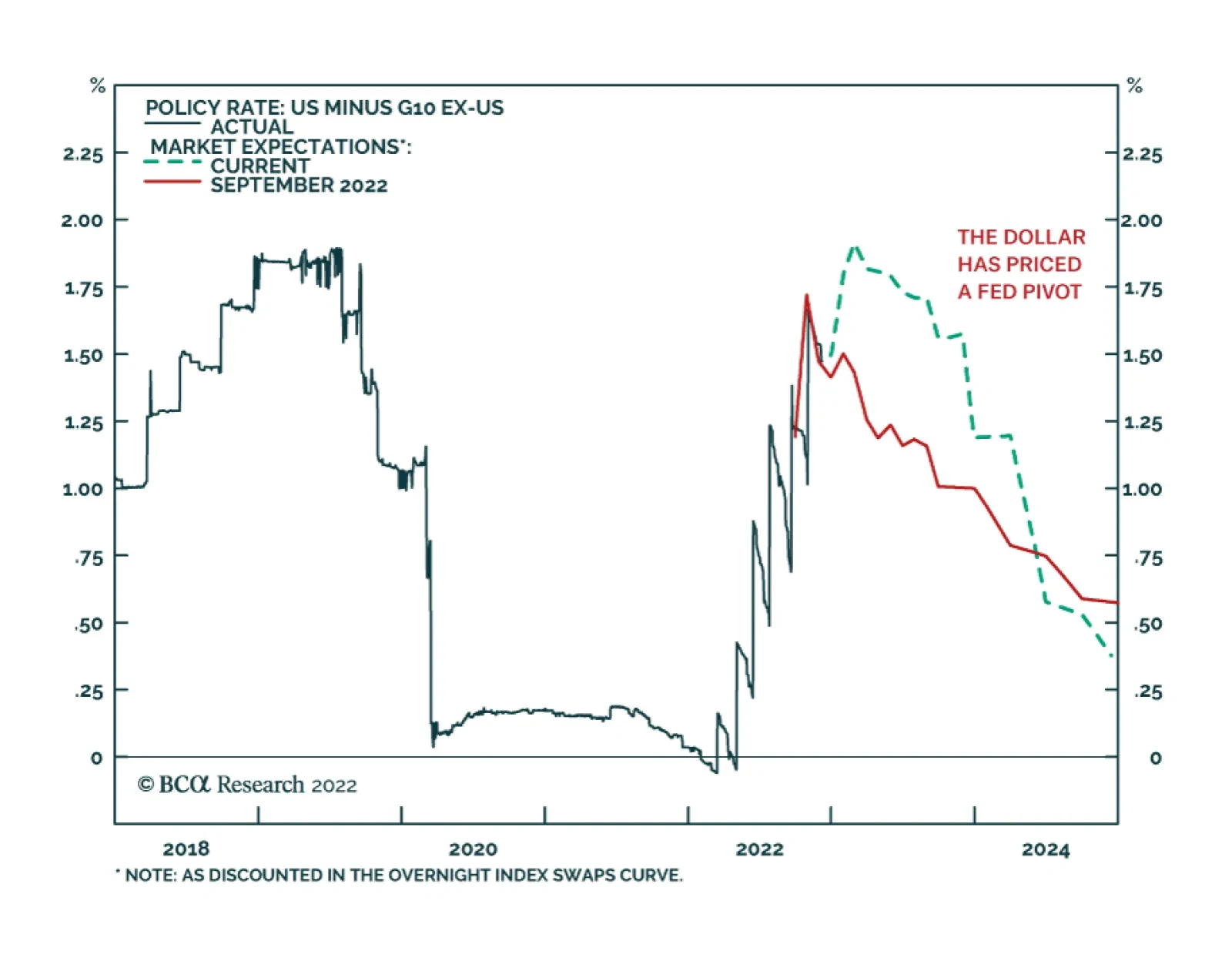

US Dollar

While the housing downturn will be fairly mild in the US, it will be more severe abroad. Continue to favor bonds of countries whose housing fundamentals will limit rate hikes.

The crucial question for 2023 is: will the US and UK Beveridge Curves shift back inwards to their pre-pandemic versions, ushering in a soft landing? Or, will we slide down the new post-pandemic Beveridge Curves into recession? Plus: we reveal the most important chart for Europe and the most important chart for China in early 2023.

Relative to beaten-down expectations, global growth will surprise on the upside in 2023. Investors should overweight equities for now but look to turn more defensive in the second half of the year.

This week, we look at the latest data releases in the G10, along with implications for all the major currencies.

Both the US and China have structural imbalances that need correcting. The former has a structurally imbalanced labour market in which demand far outstrips supply. The latter has a massively overvalued housing market. The concurrent correction of these two structural imbalances in the world’s two largest economies will necessitate a sharp slowdown in global growth, and leads to several investment conclusions.

In this report, we argue that the dollar will enter a volatile trading range, before a bear market begins in earnest. That said, fundamental forces are aligning for US dollar downside.

In this <i>Strategy Outlook</i>, we present the major investment themes and views we see playing out next year and beyond.

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

Web 3.0 plays will boom in the coming decade. Play this through a diversified exposure to today’s main blockchain tokens. But the Web 2.0 oligopolies, like Amazon and Meta, are in big trouble.