Trump's Policies

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

President Trump is only the second president to have won, lost, and won again in US history, so today’s inaugural address was unlike any other since Grover Cleveland in 1893.

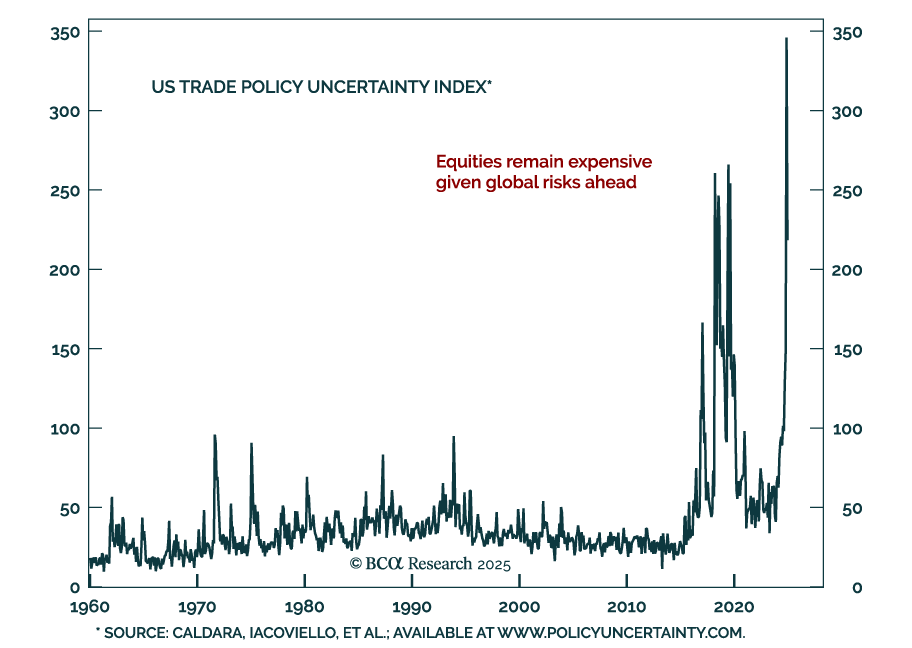

Inauguration Day or shortly thereafter will see either a global tariff of 10% or targeted but substantial tariffs on China, Mexico, and Canada. Treasury yields will rise on tax cuts, the dollar will stay strong, yet oil will also continue to rally, causing equity volatility in the near term.

In this Special Report, BCA’s Chief Geopolitical/US Political Strategist Matt Gertken discusses the top five “Black Swan” risks for 2025, from Trump to China.

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

In our Alpha report, we reiterate that we expect President Trump to curb his most enthusiastic plans for tax cuts due to the pressure from the bond market. That will be good for equities in the long run – as it will assuage the pressure on yields. However, it should be negative for the USD as investors grapple with far less fiscal support for the US economy over the next four years than expected. We also give our readers a blueprint for following the news flow when it comes to trade policy. Stick to a framework and ignore tweets.

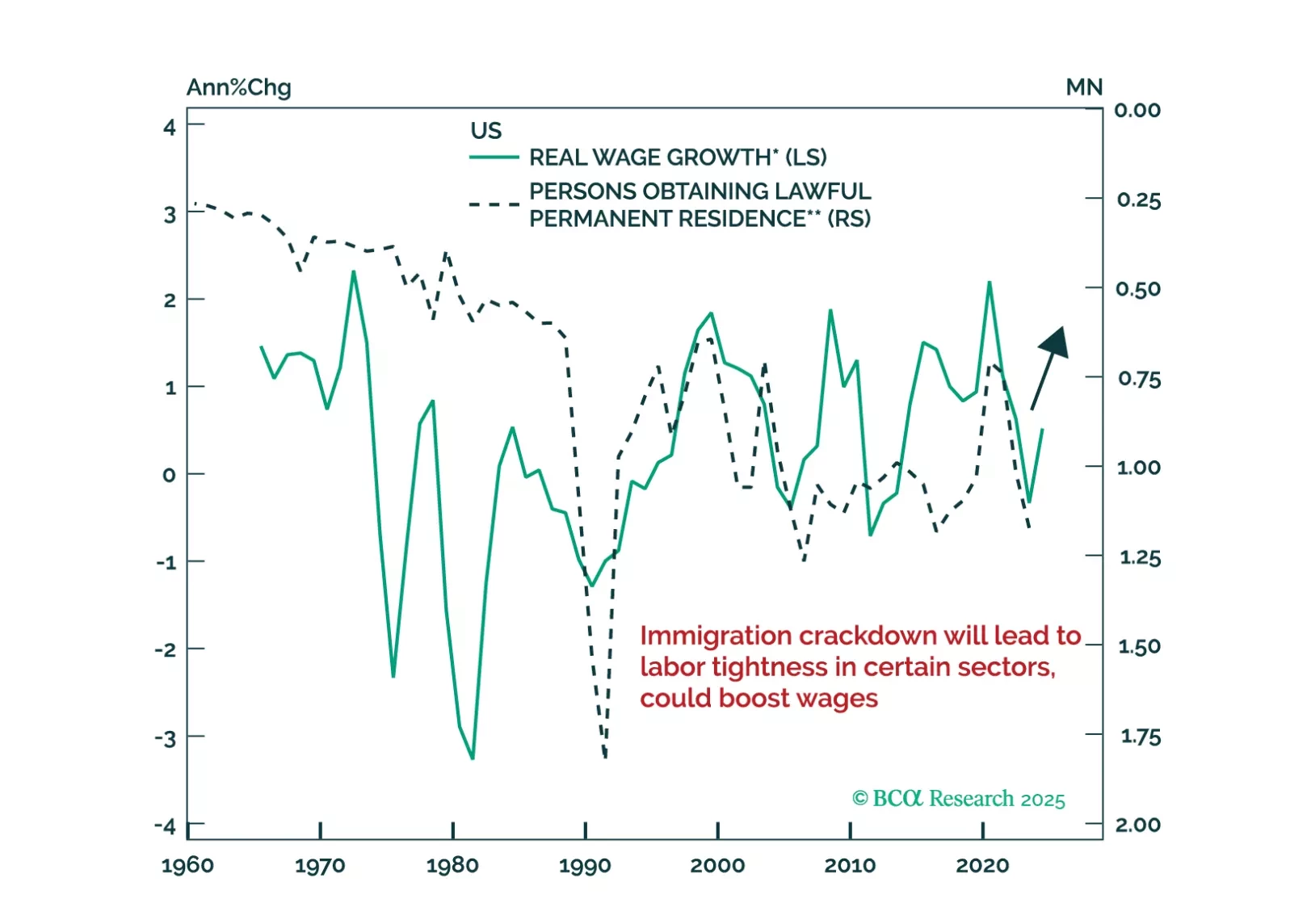

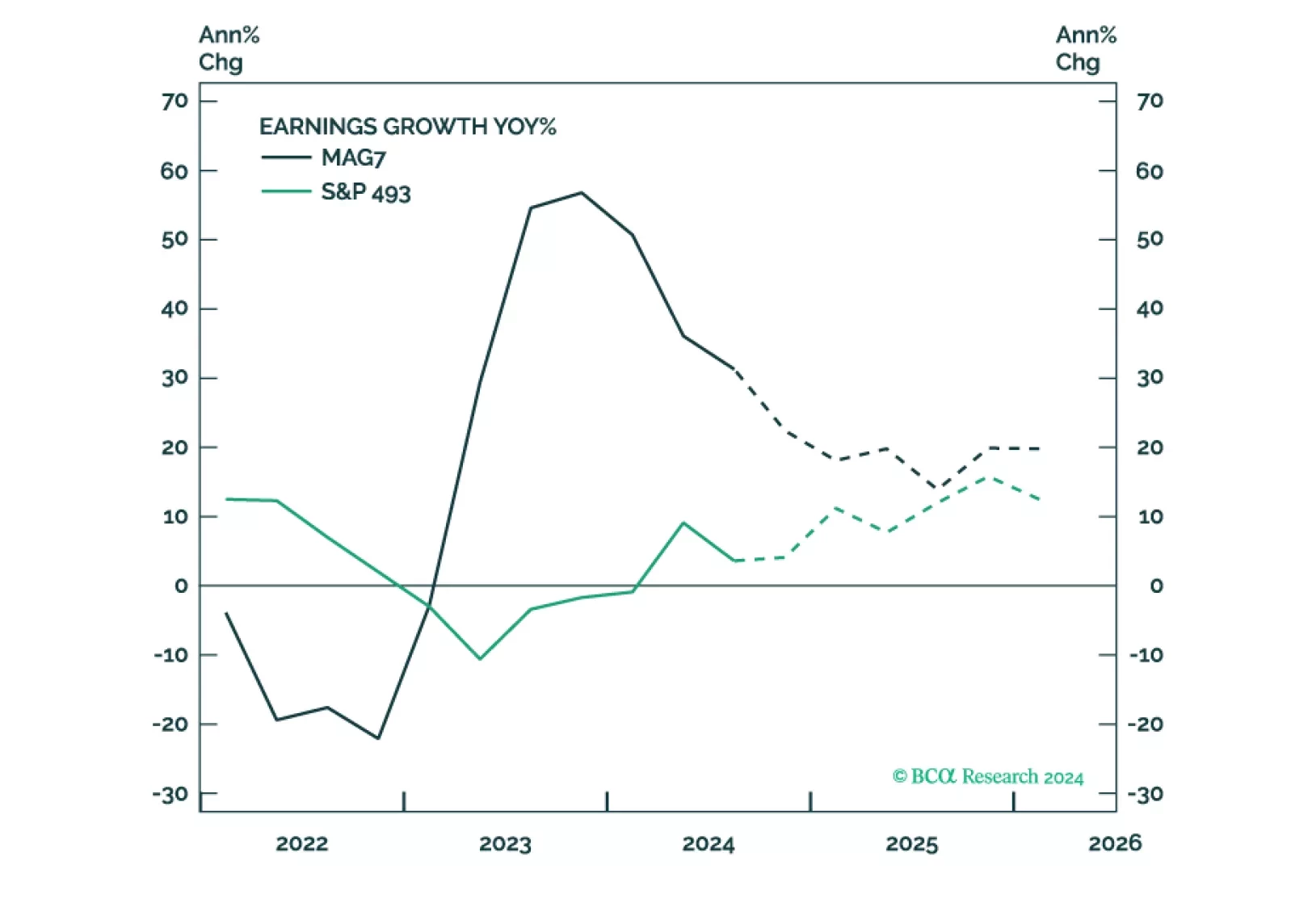

Trump's policies aim to support domestic producers and will be pro-growth and inflationary, at least initially. This environment is supportive of equities. Earnings will likely be strong, but elevated valuations make equities prone to a correction. Earnings growth broadening will translate into performance broadening – the S&P 493, Cyclicals, Value, Small and Mid are likely to outperform.

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

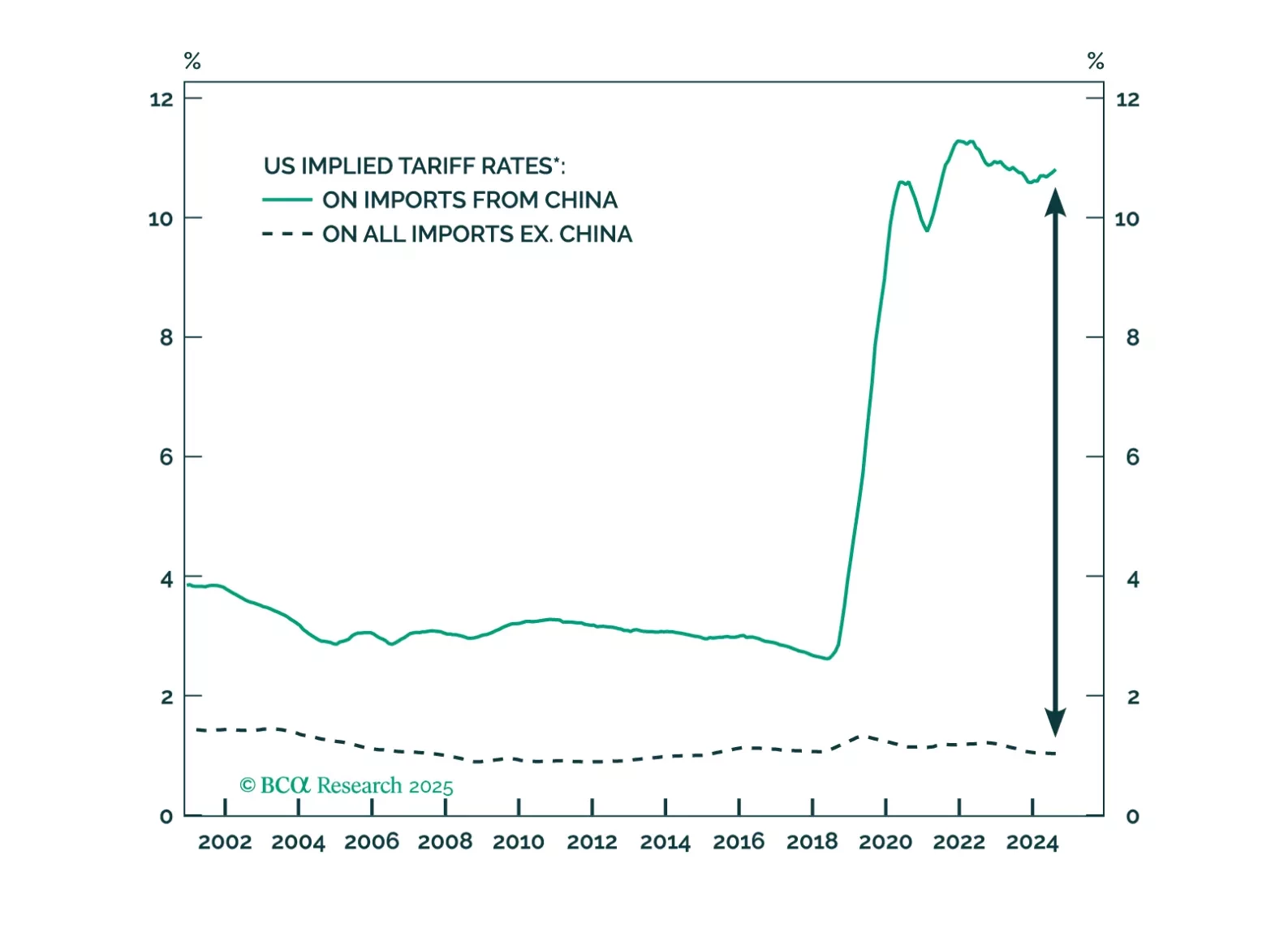

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

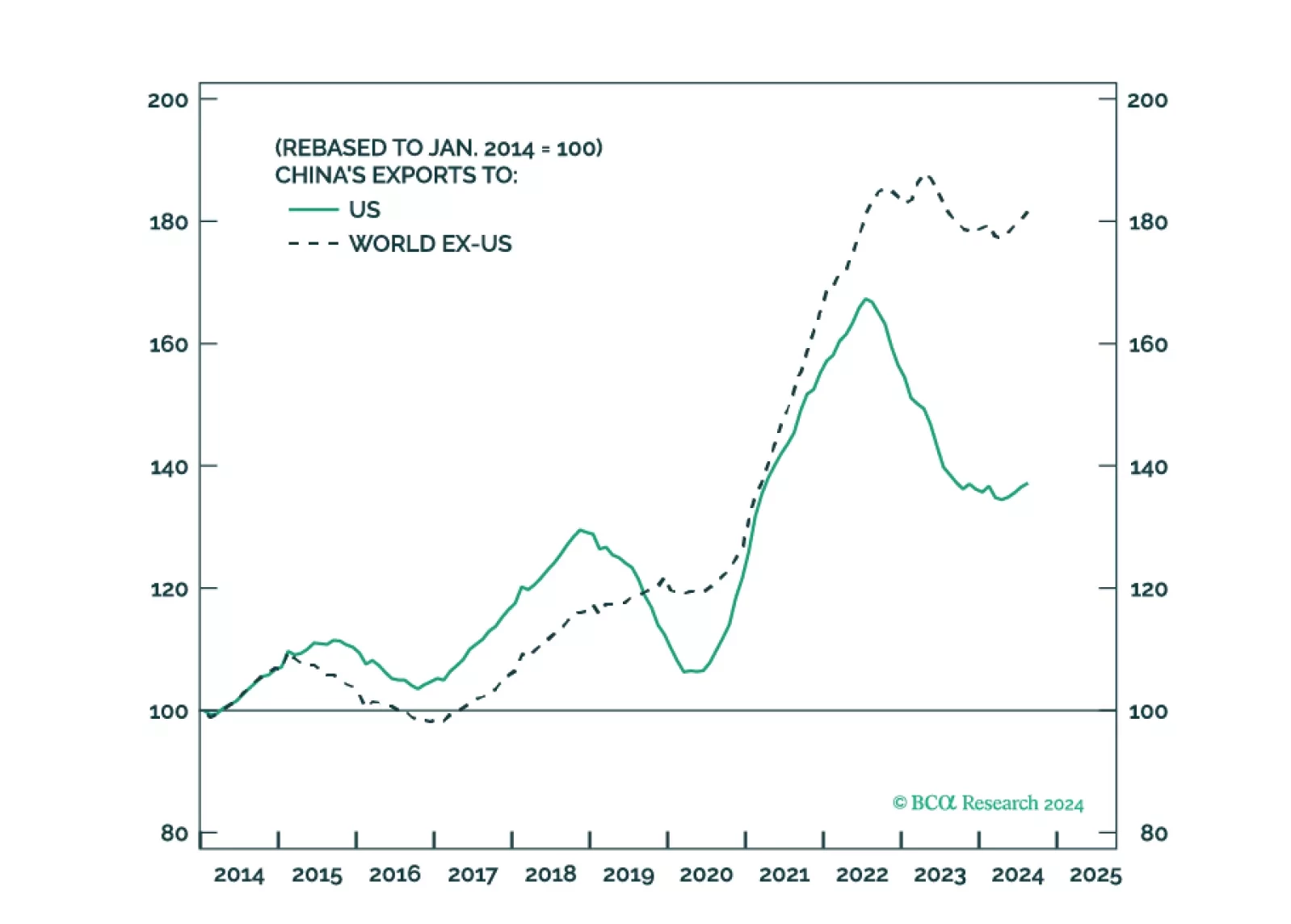

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

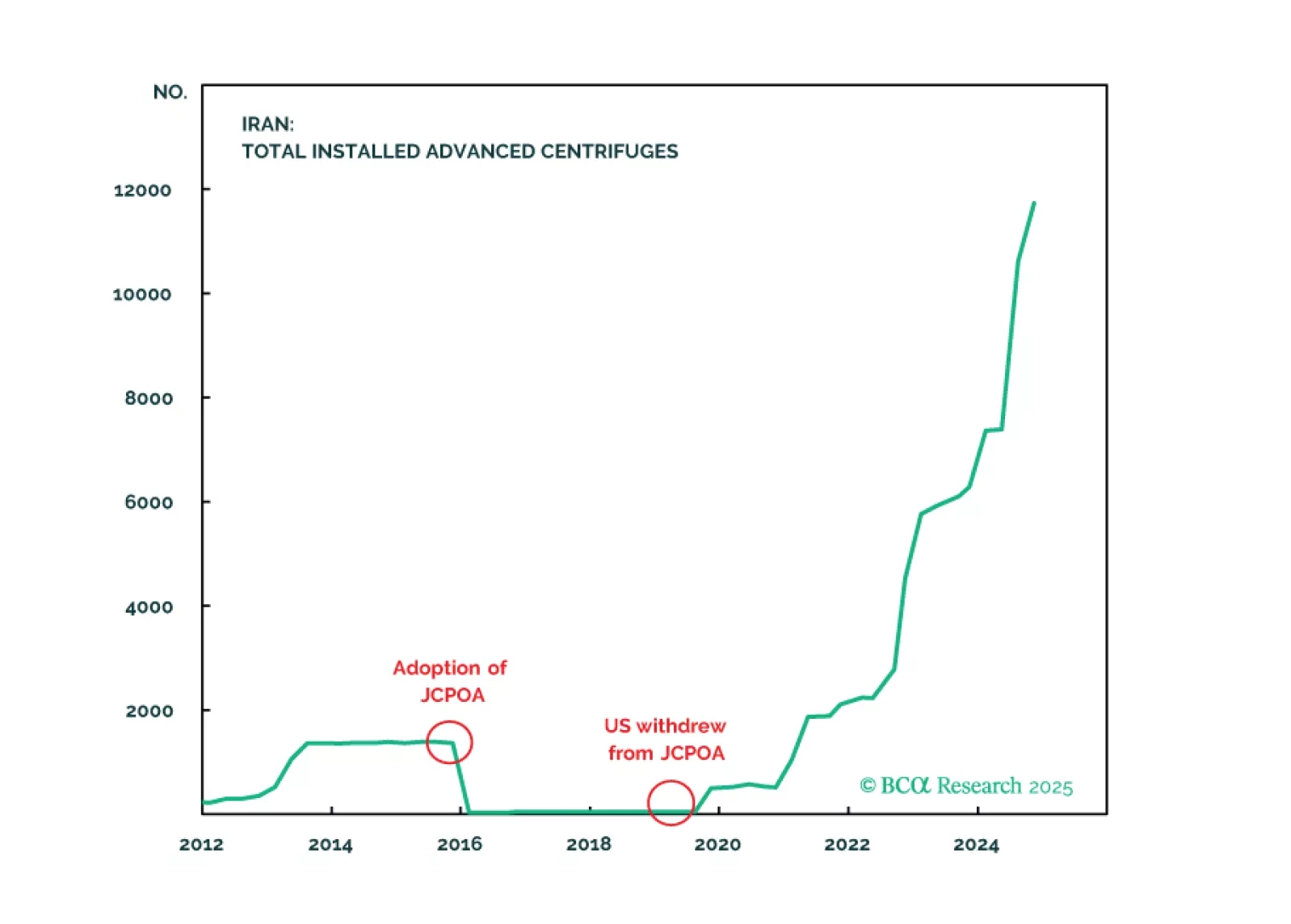

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

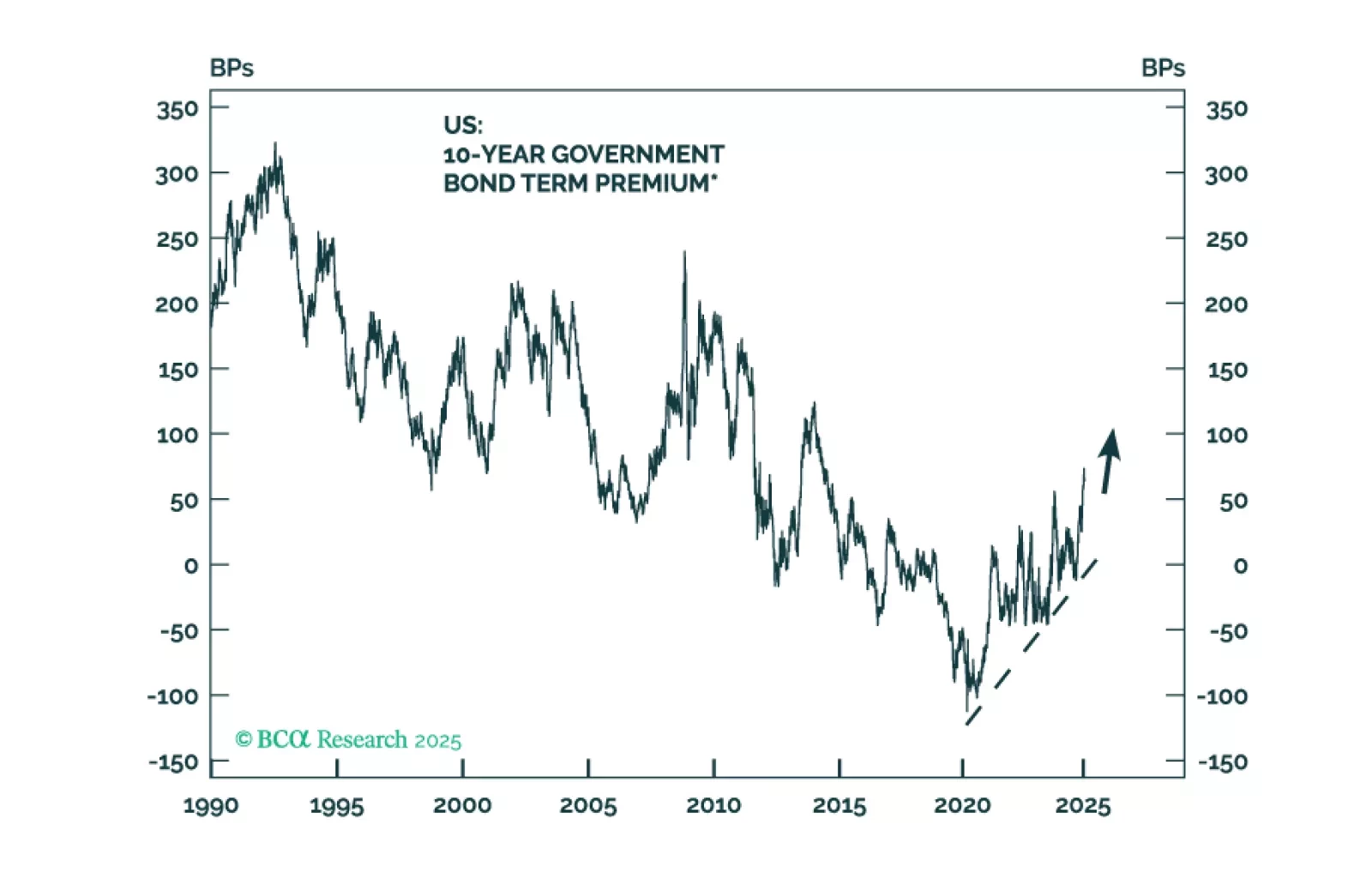

Investors are overstating the positive fiscal impact of the Trump presidency. The bond market will have something to say about the scope for further deficit expansion via tax cuts. As such, the trade after the trade of the Trump 2.0 administration may involve less growth out of the US, not more. In the interim, however, investors should continue to expect higher yields and increased equity volatility. There are plenty of risks ahead, including geopolitics, trade, and uncertainty surrounding fiscal policy.

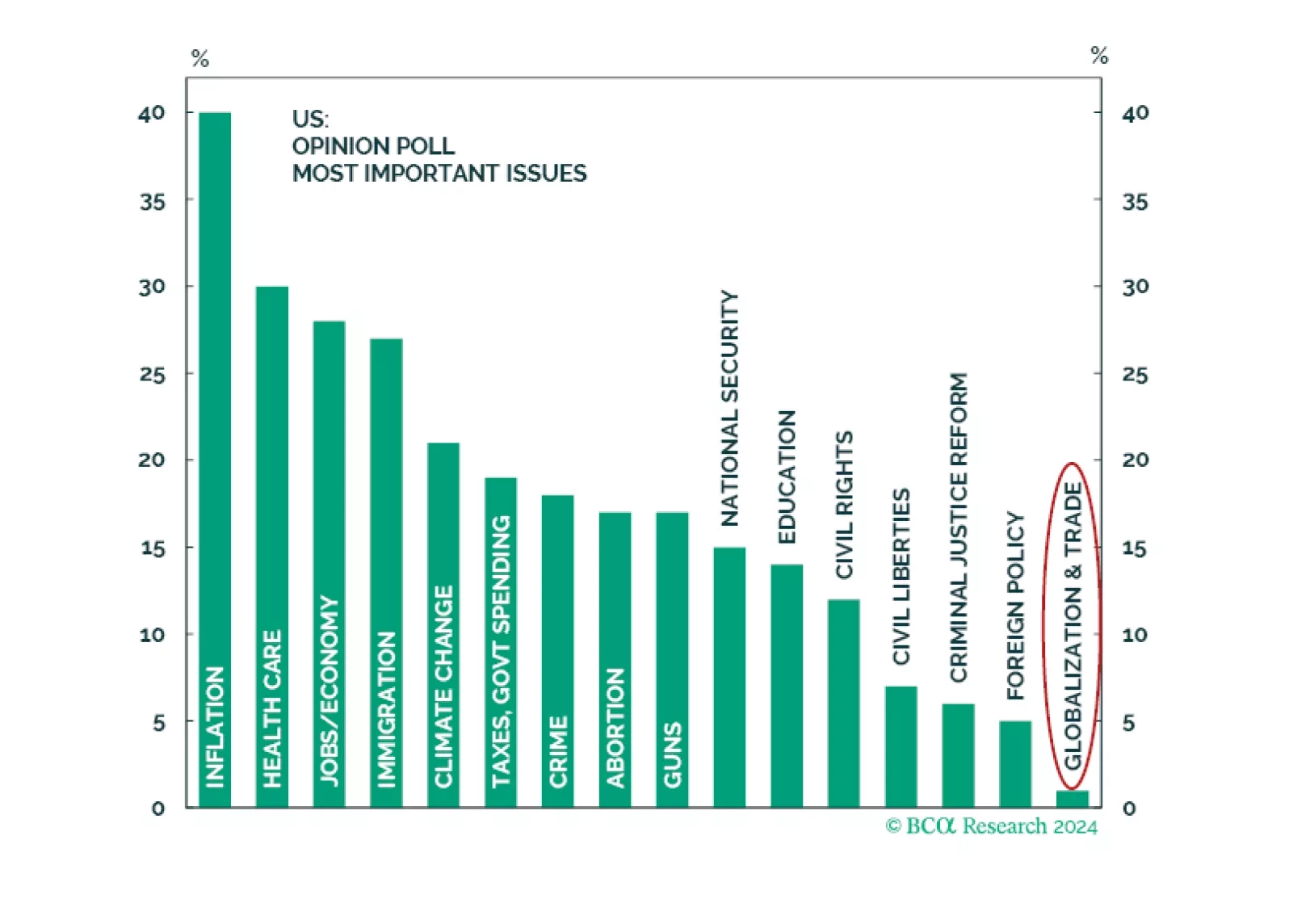

Ultimately, 2024 is not 2016 — a seemingly obvious point, but one with market relevance. In 2016, voters gave Trump a strong mandate for nominal GDP growth. It is not clear if this is the case today. Inflation is the most important issue, least relevant is trade and globalization. As such, Trump’s renewed mandate is for supply side reforms, not more populism and protectionism.