Trump's Policies

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

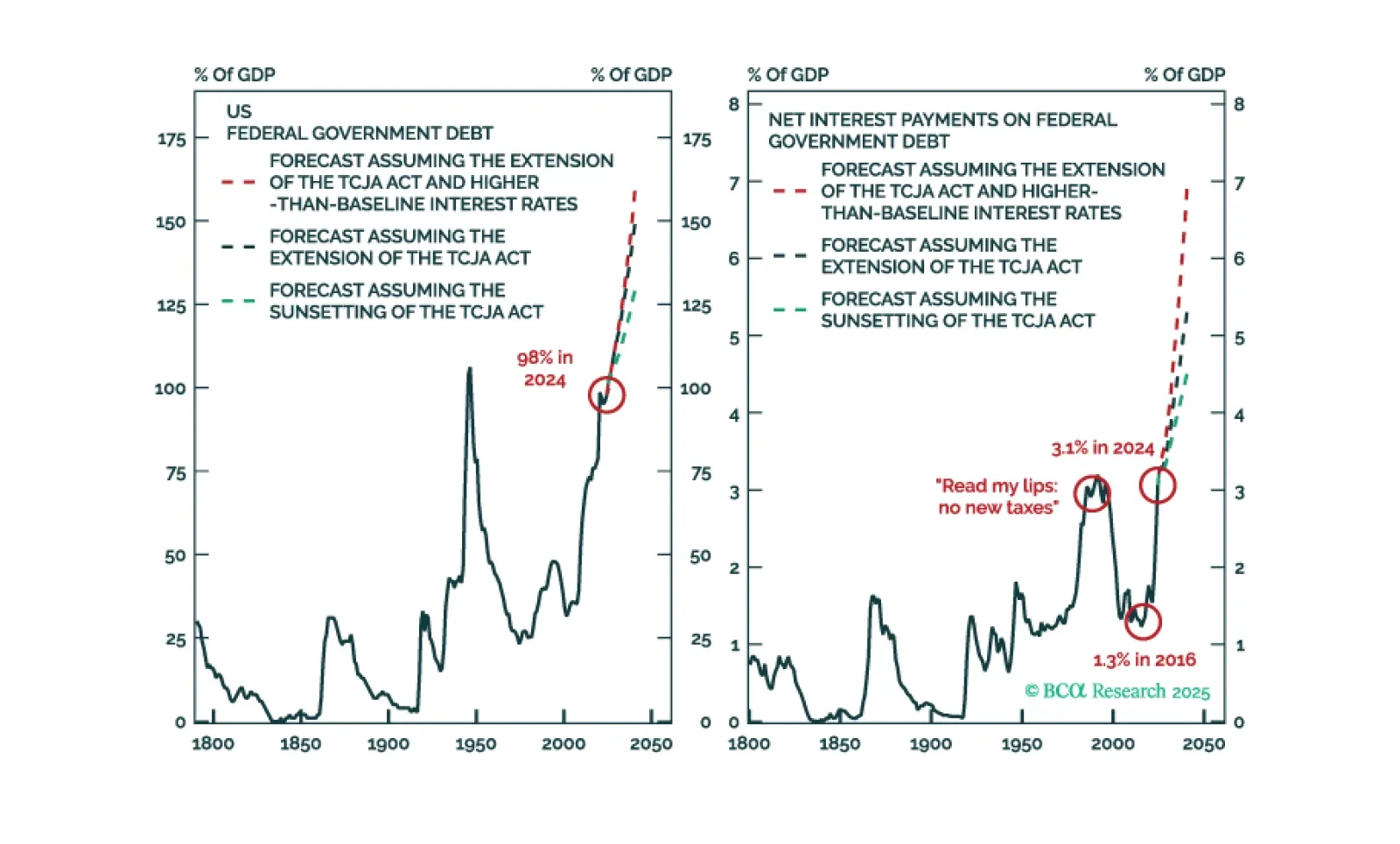

This month, we focus on the One Big Beautiful Bill Act (OBBBA). Our assessment in the Alpha report is that there won’t be any remaining alpha to harvest by shorting duration. The team that coined the “Human Steepener” moniker for President Trump is, effectively, throwing in the towel on looking for more upside to yields. There are many reasons for that view, but the main one is that the OBBBA legislation is just not that profligate, especially not relative to the investors’ expectations in the early days of the Trump 2.0 term.

After considering some of the most common bullish arguments, we stand by our recession view and reiterate our defensive asset allocation recommendations.

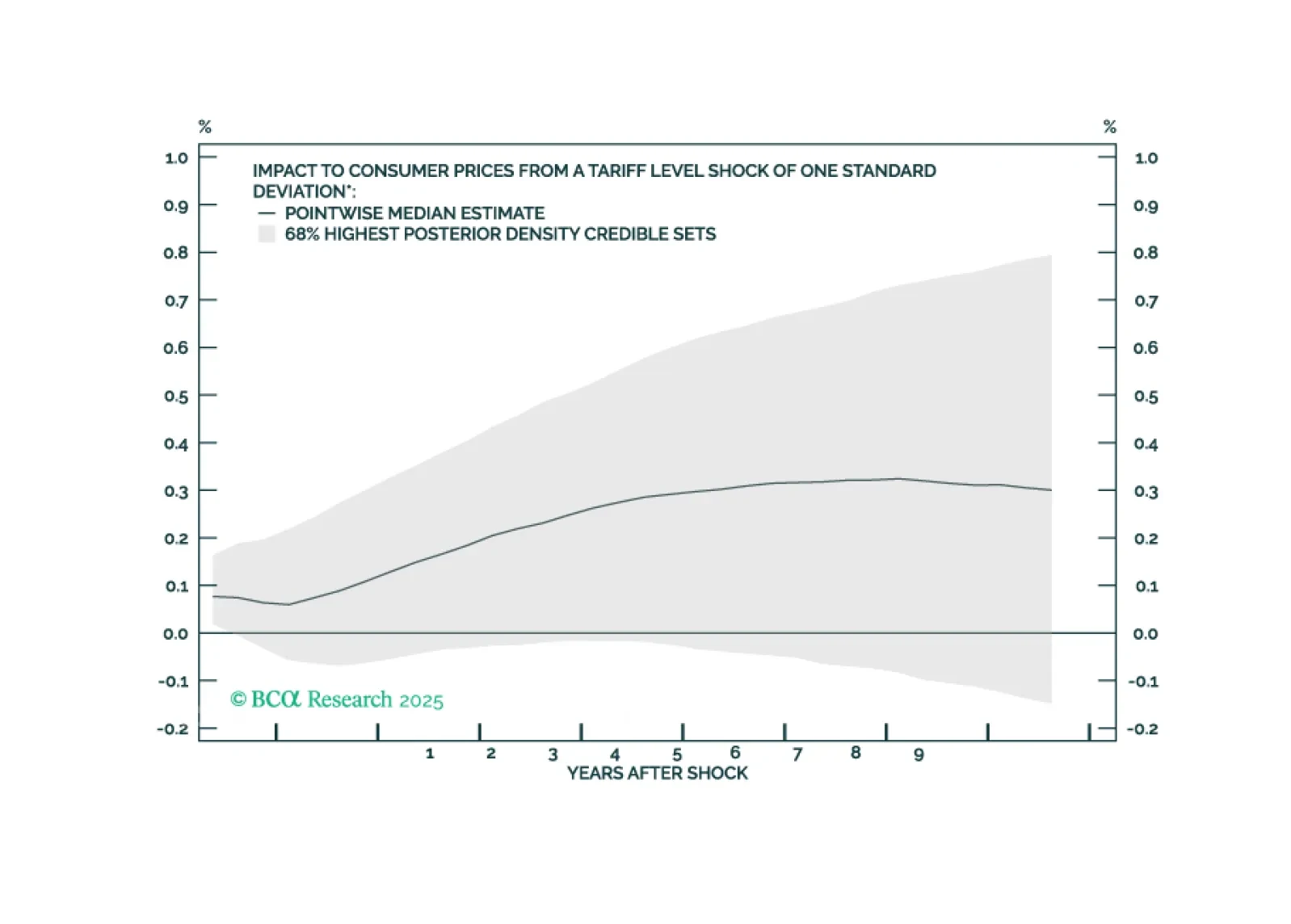

In Section II, Jonathan discusses the arguments in favor and against the view that US inflation will be structurally elevated over the longer term. Our base case view remains that US inflation will not be significantly above 2%, but this view may change if US tariffs are put in place permanently and the US avoids a recession.

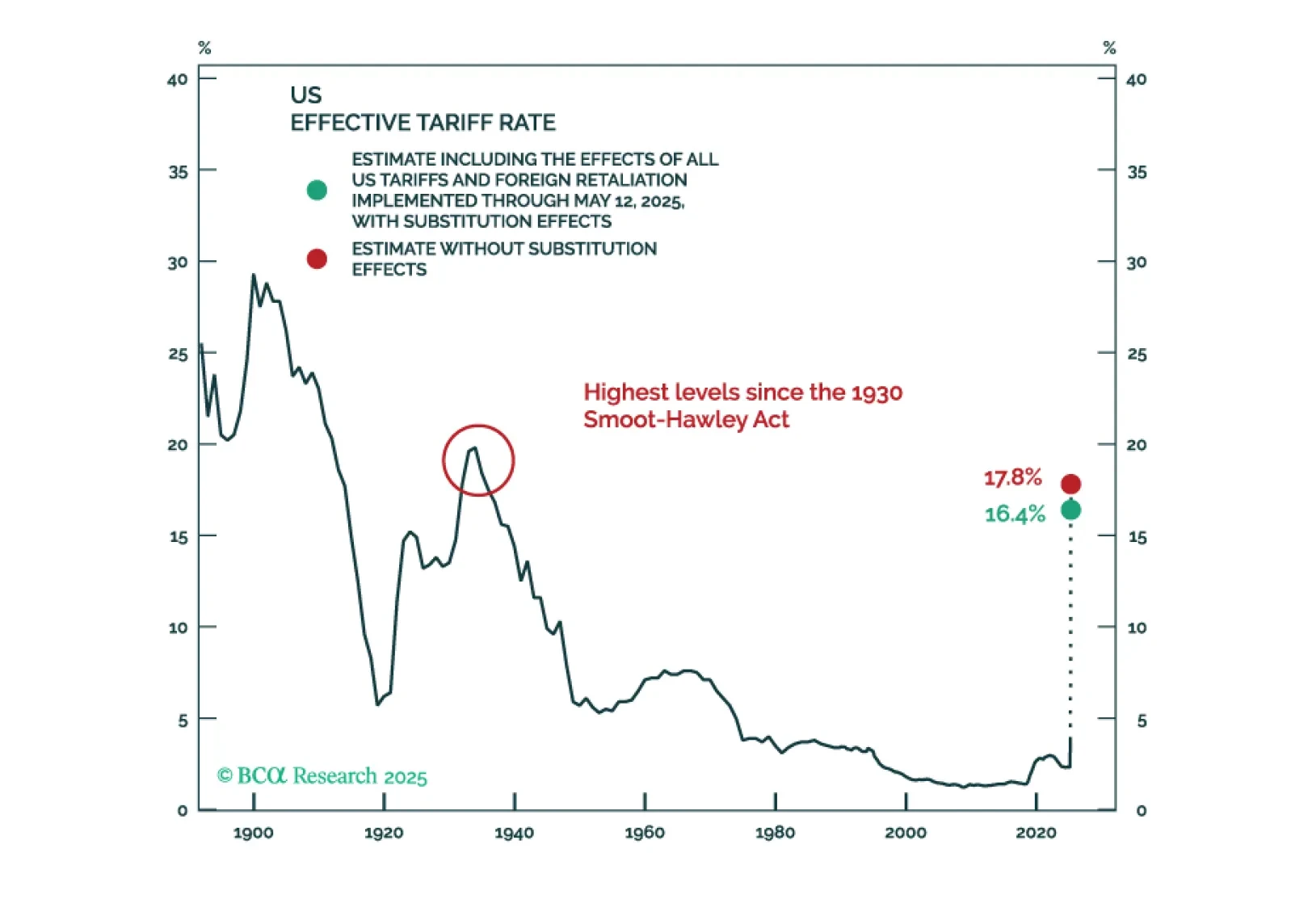

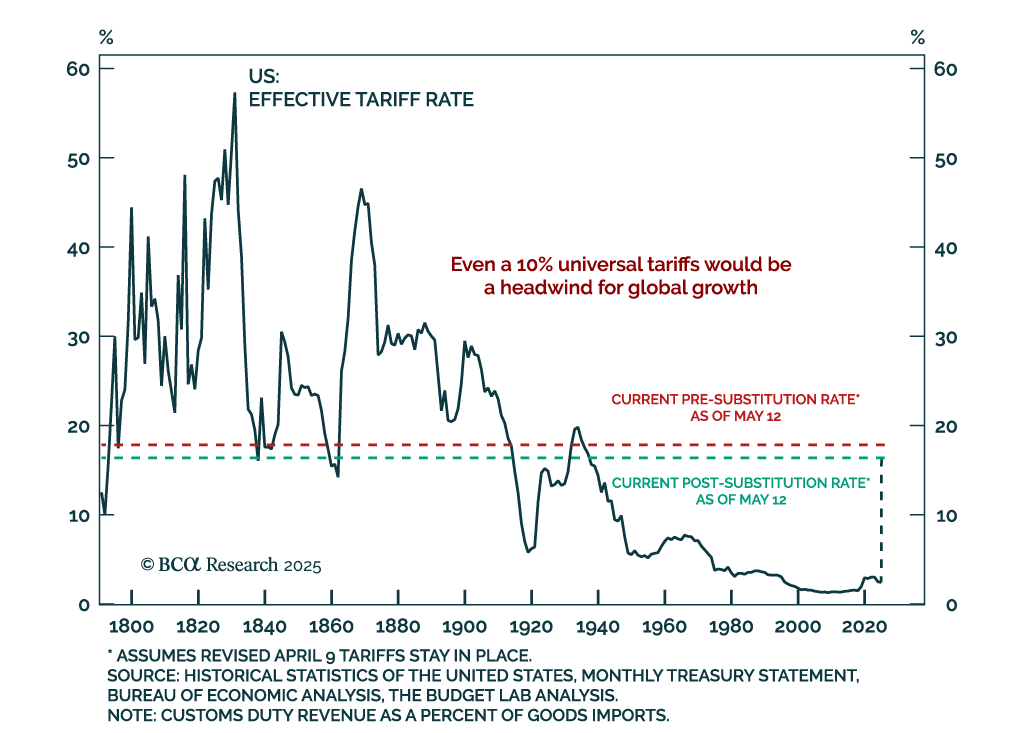

In Section I, Doug warns that US trade policy may produce a considerably worse outcome than investors currently expect. The administration’s apparent 10% tariff baseline is likely to be negative for the US economy and particularly the small business sector. Investors should remain defensively positioned for now, although judicial constraints on the administration’s ability to wage a trade war, if confirmed, would sharply reduce our estimated recession probability. In Section II, Jonathan discusses the arguments in favor and against the view that US inflation will be structurally elevated over the longer term. Our base case view remains that US inflation will not be significantly above 2%, but this view may change if US tariffs are put in place permanently and the US avoids a recession.

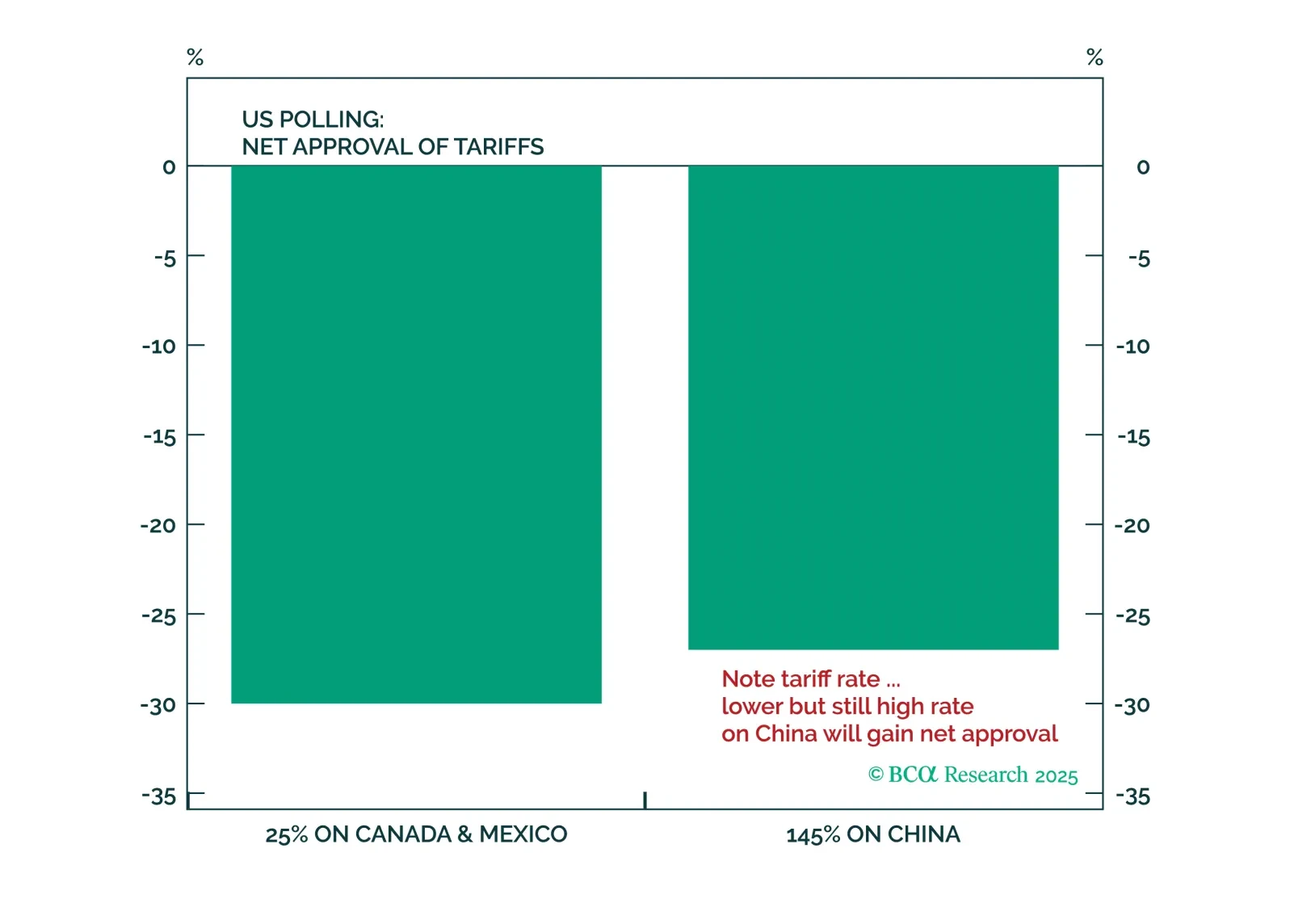

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

Rising bond yields may present an even greater danger to the global economy than the trade war. With equity valuations no longer discounting much economic risk, investors should position themselves defensively.

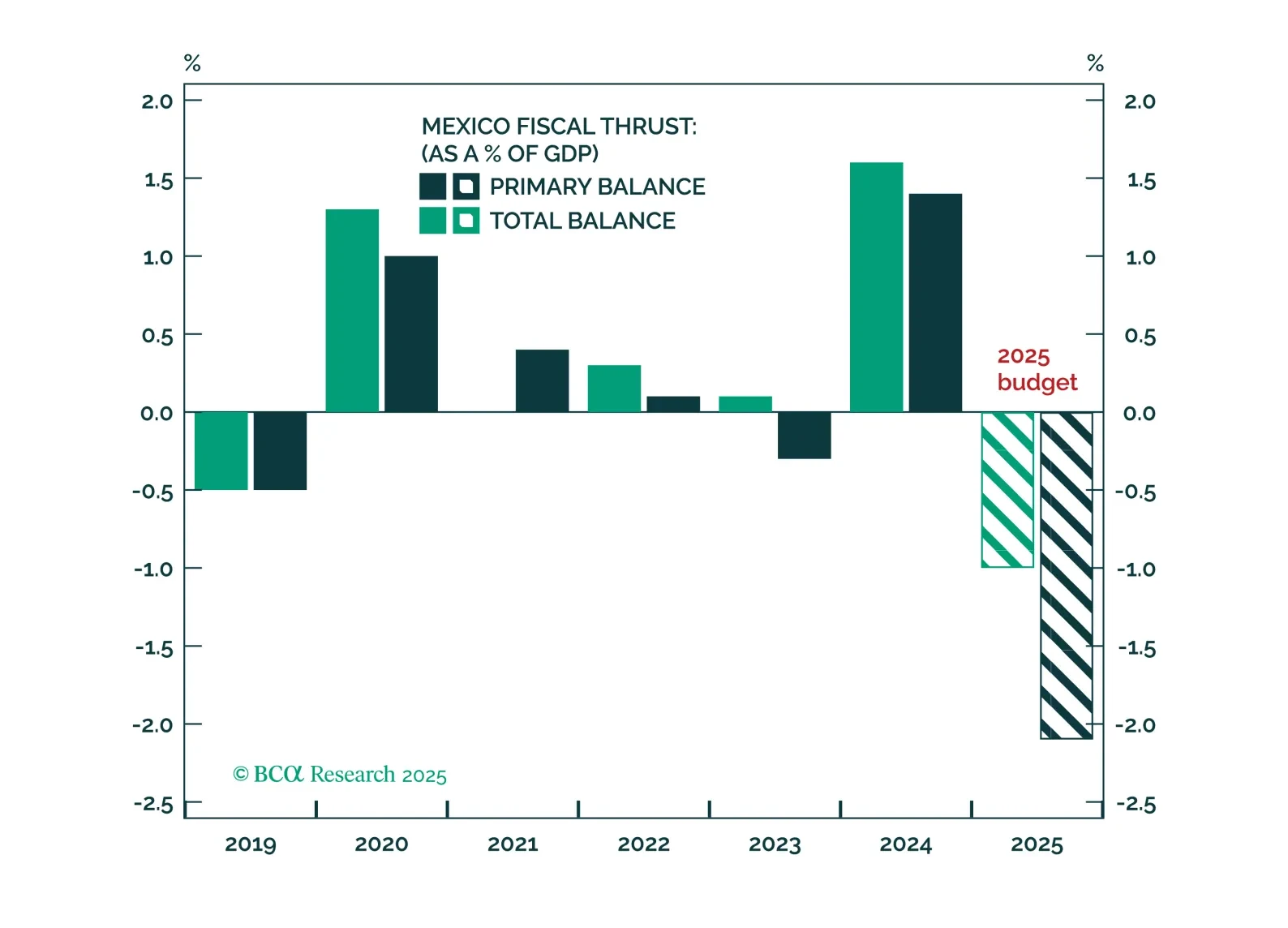

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

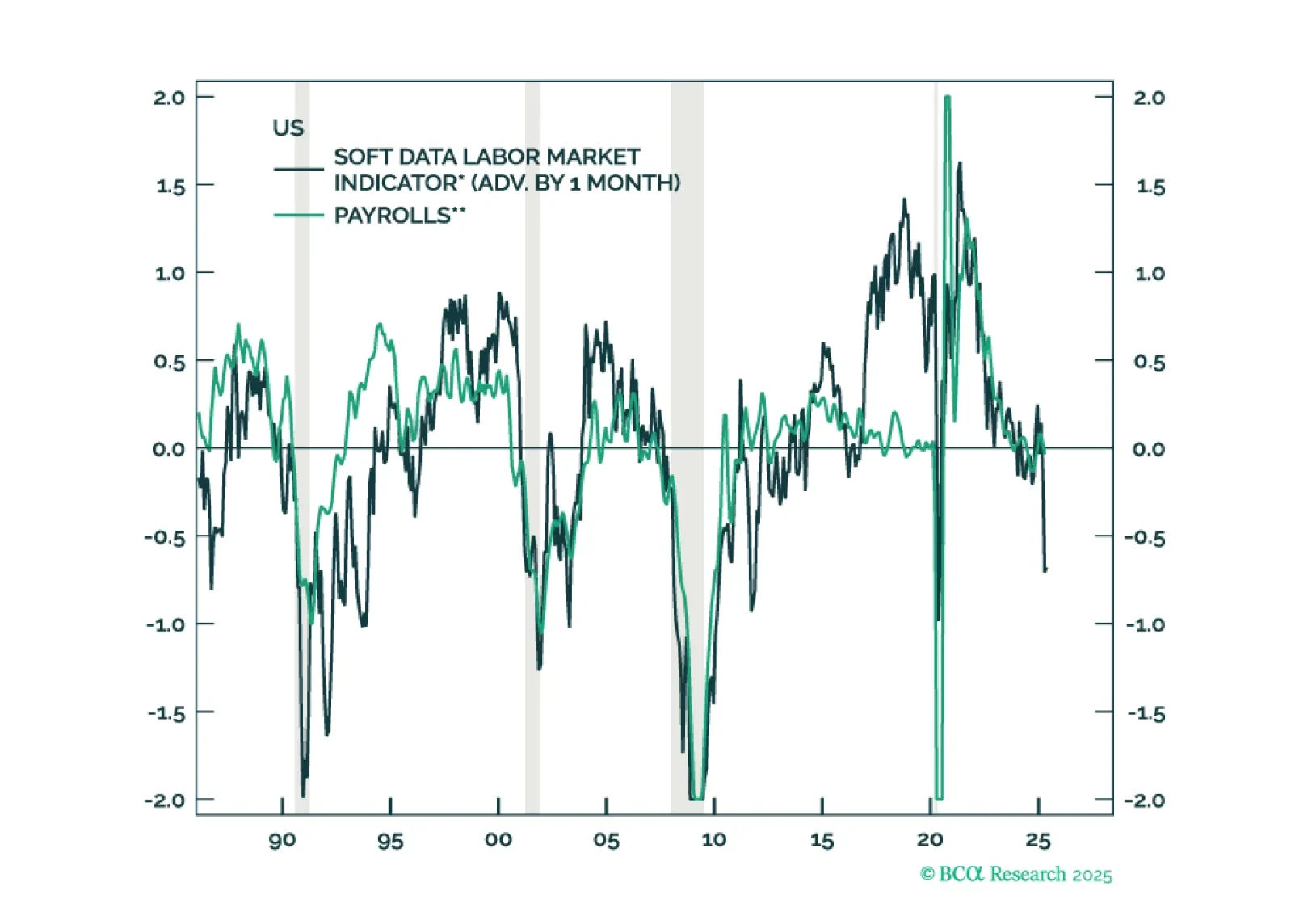

It may take several months for the tariff shock and policy uncertainty to filter through the real economy, but survey-based data are already sending a warning. Equities have priced in a lot of good news, and investors are too sanguine about the risk of a US recession.