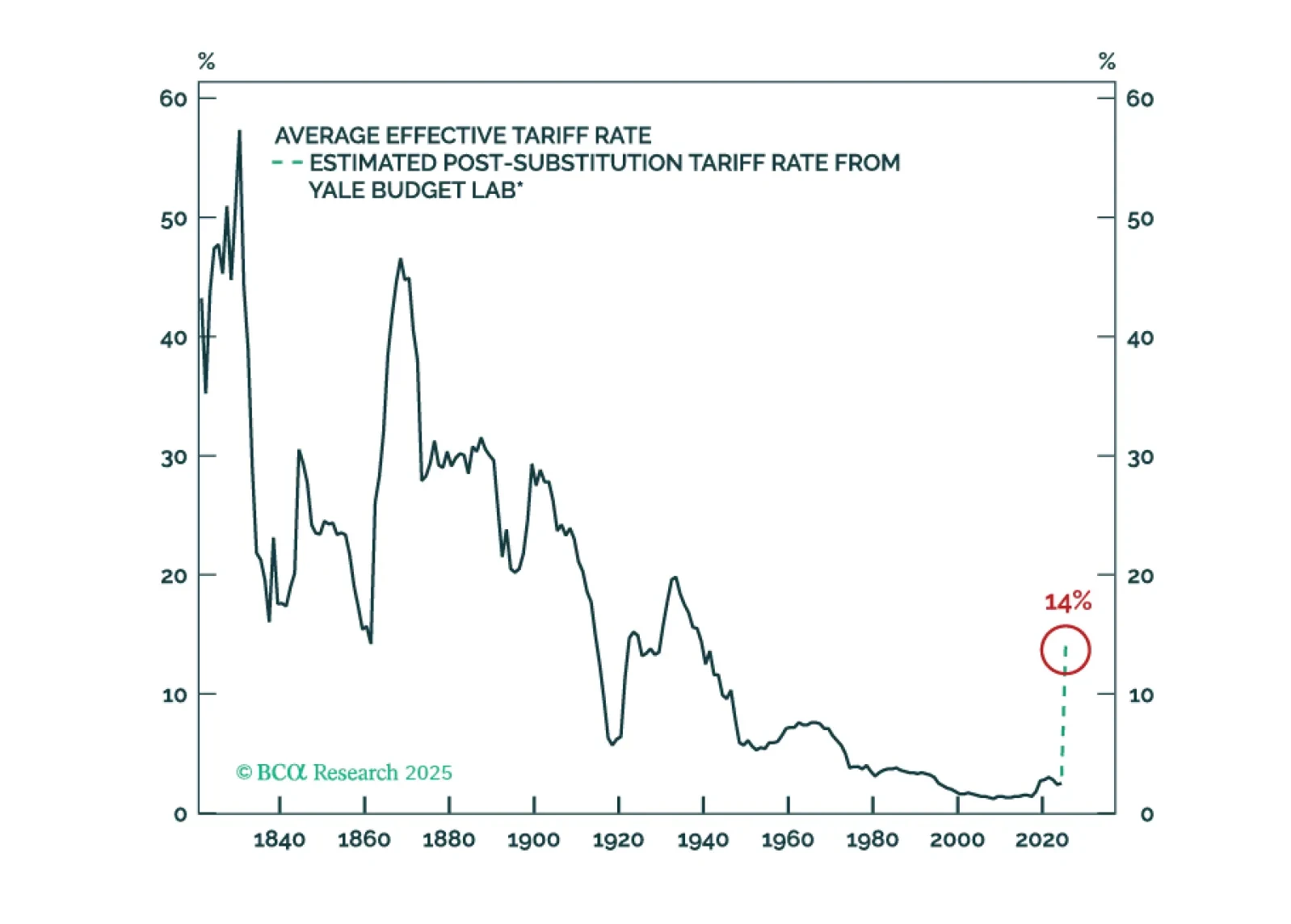

Tariffs

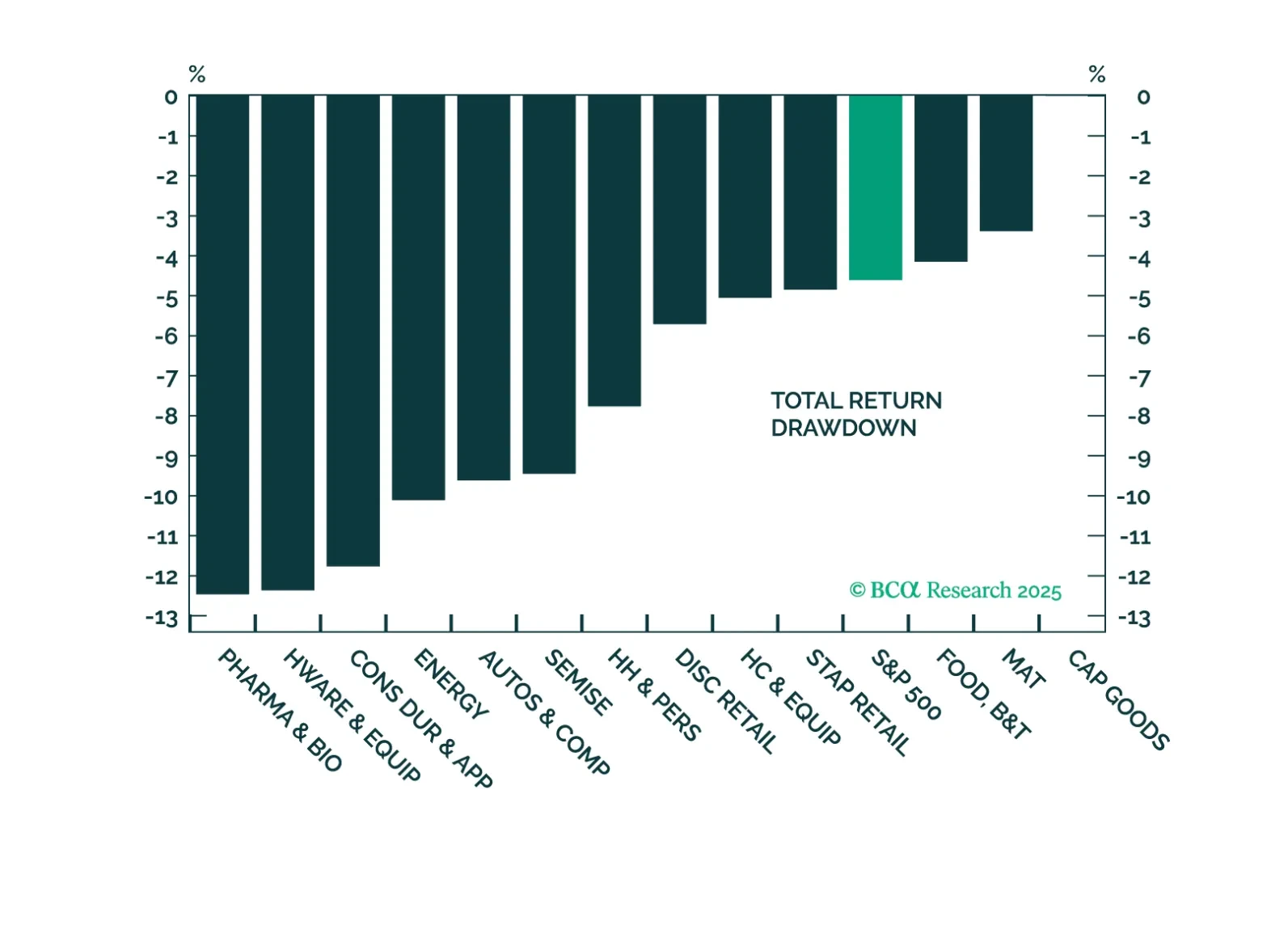

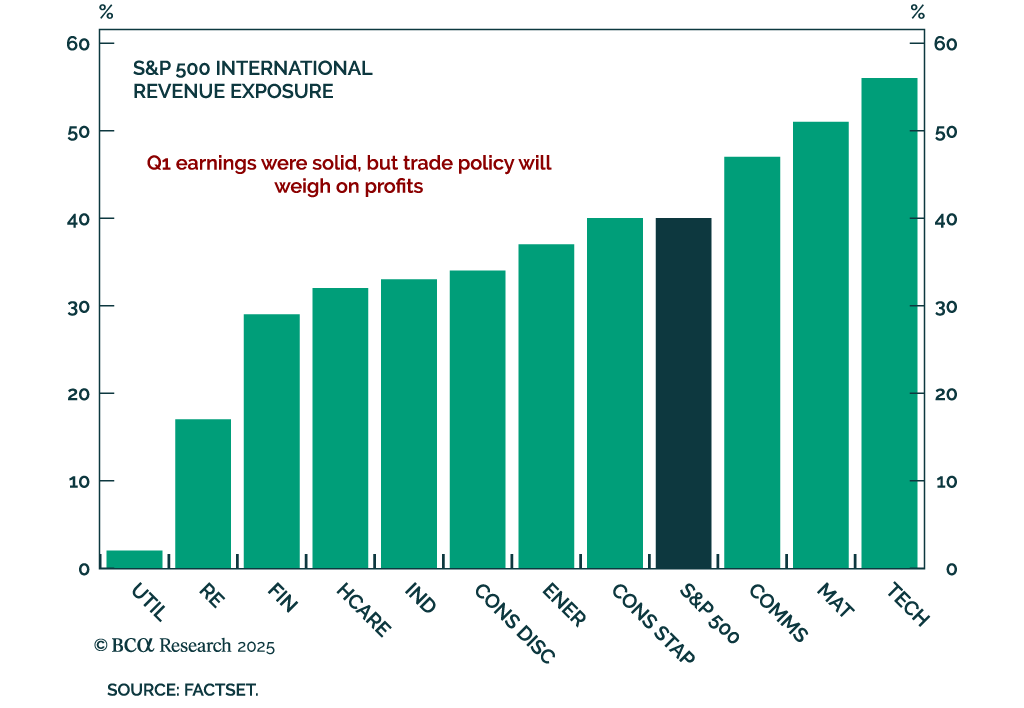

Markets are pricing out the worst trade policy fears, and while tariffs will still dent earnings, the impact looks smaller than initially feared. With sector rotation gaining traction and oversold names rebounding, we are adjusting our portfolio to reflect the rotation thesis.

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.

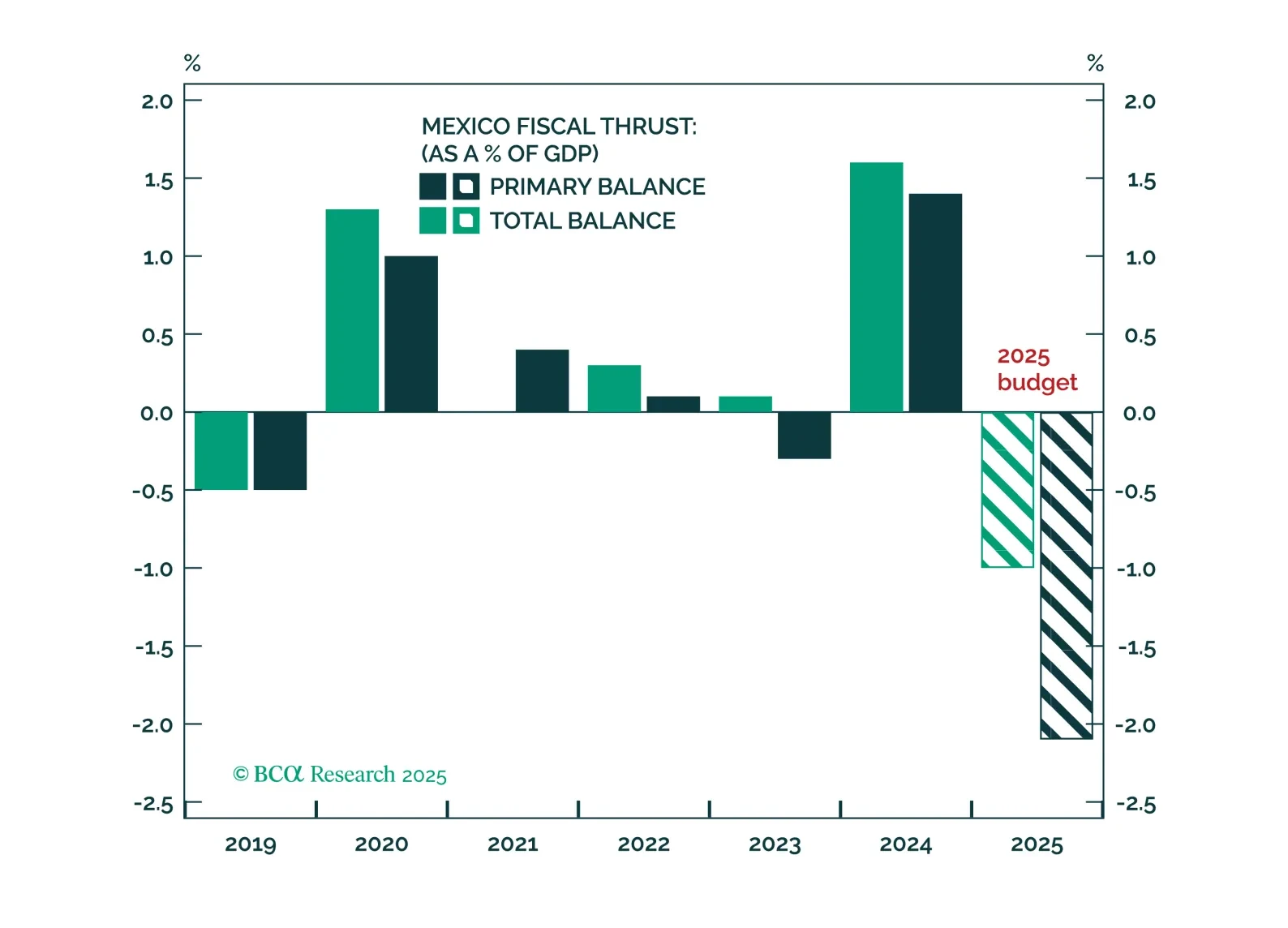

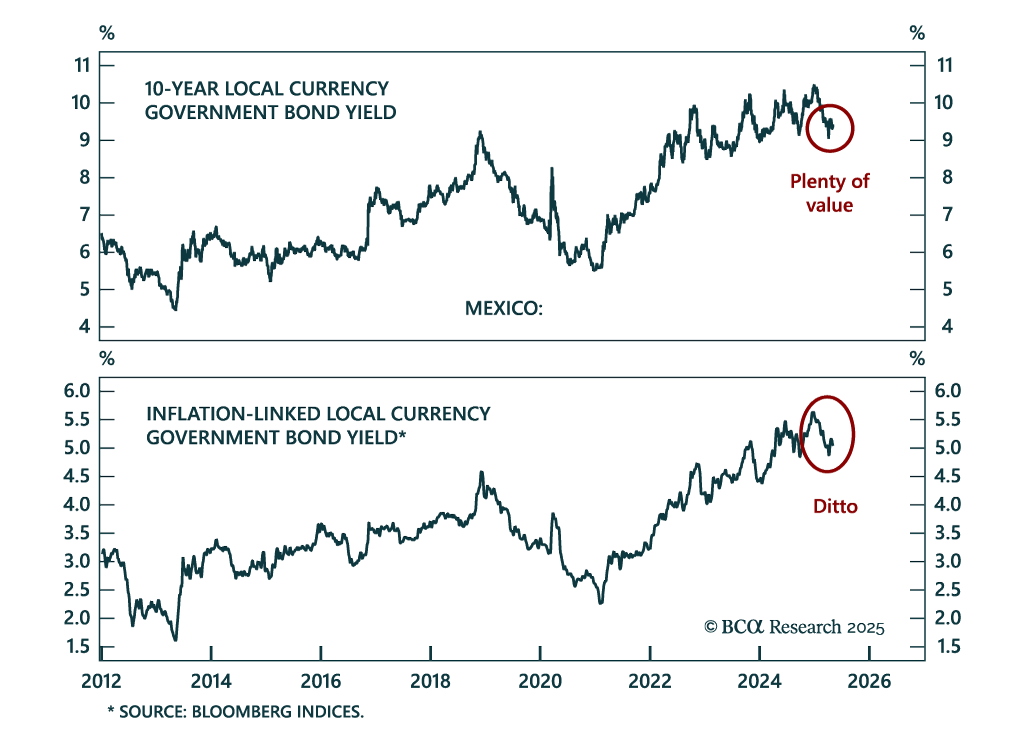

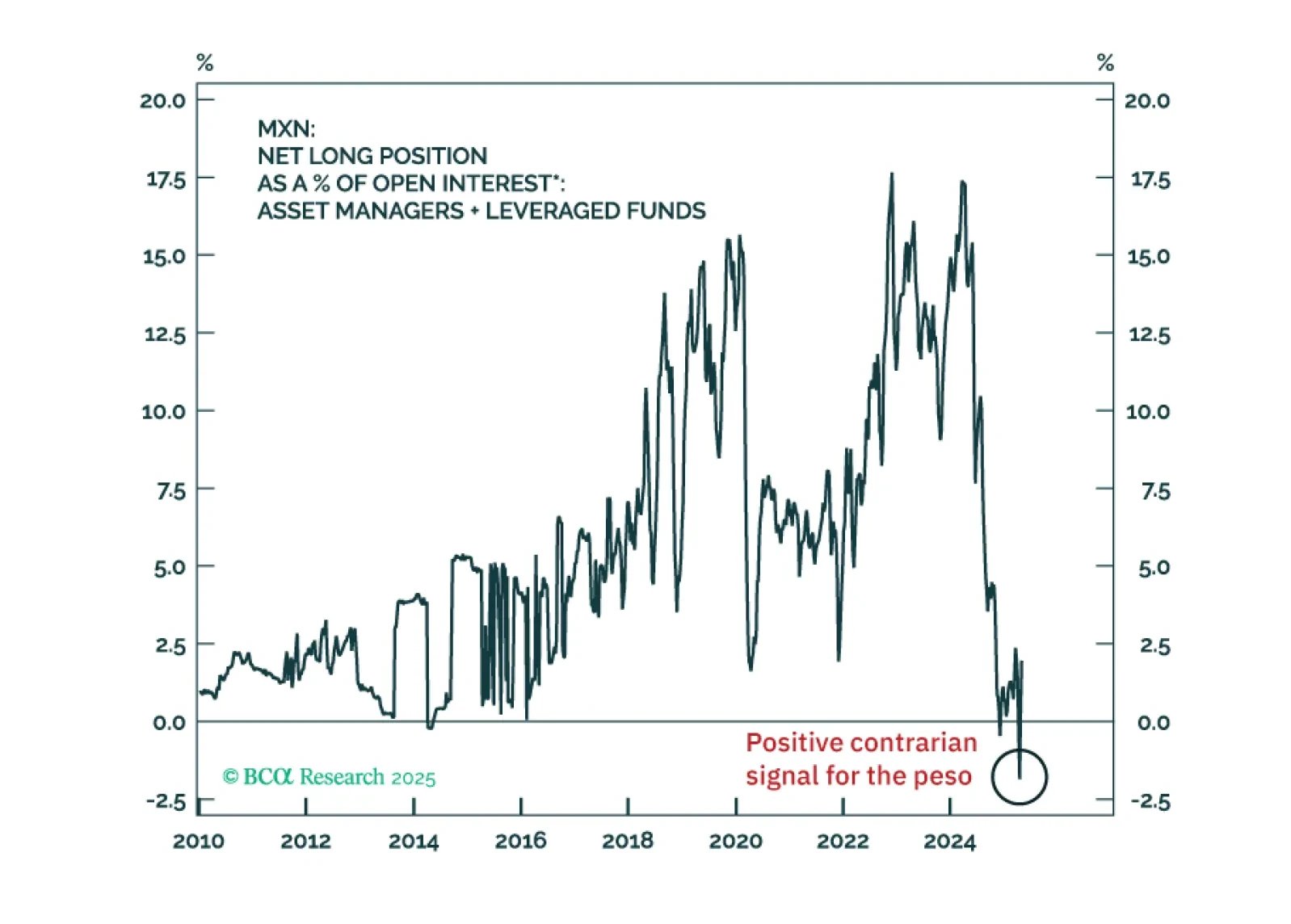

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

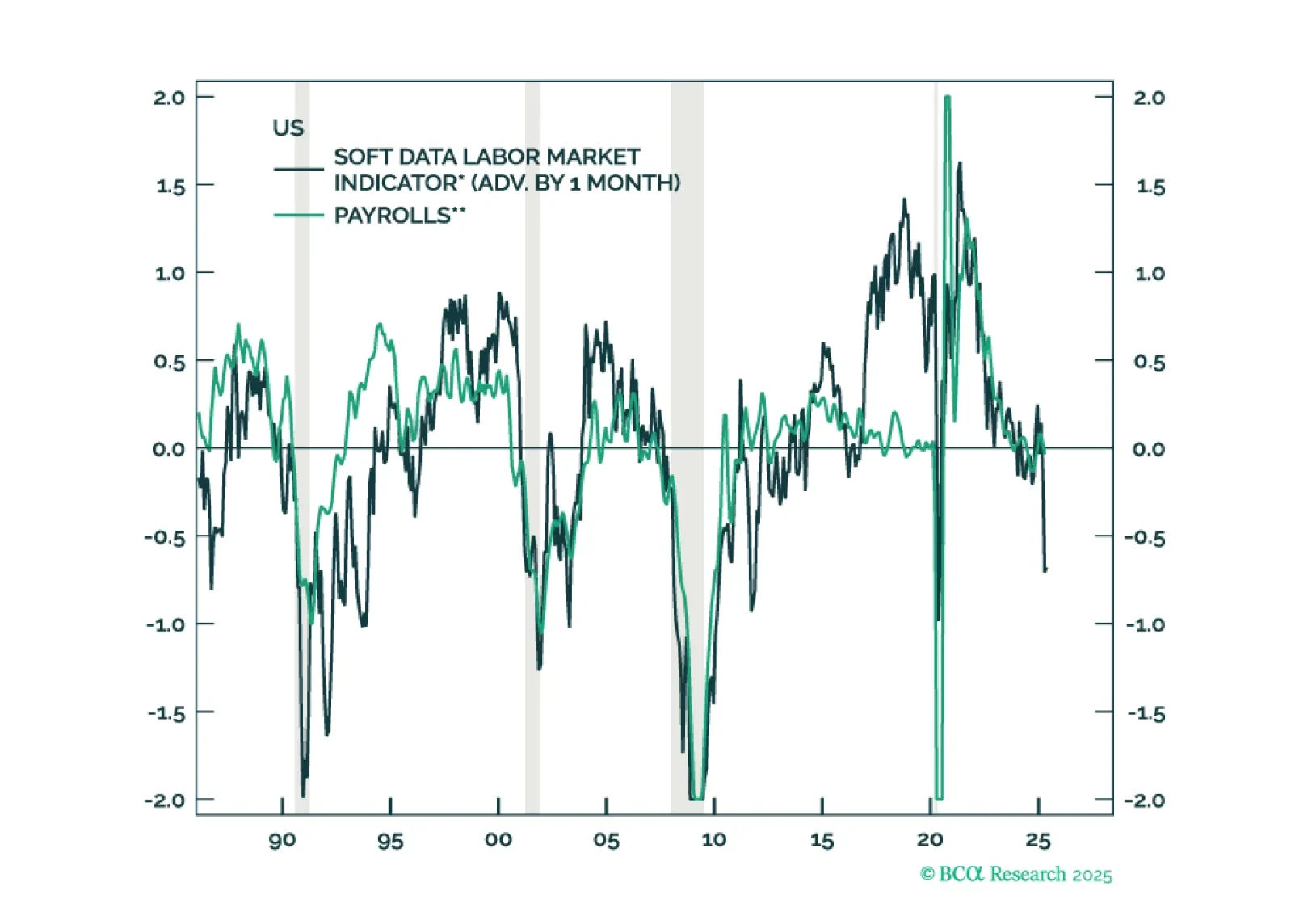

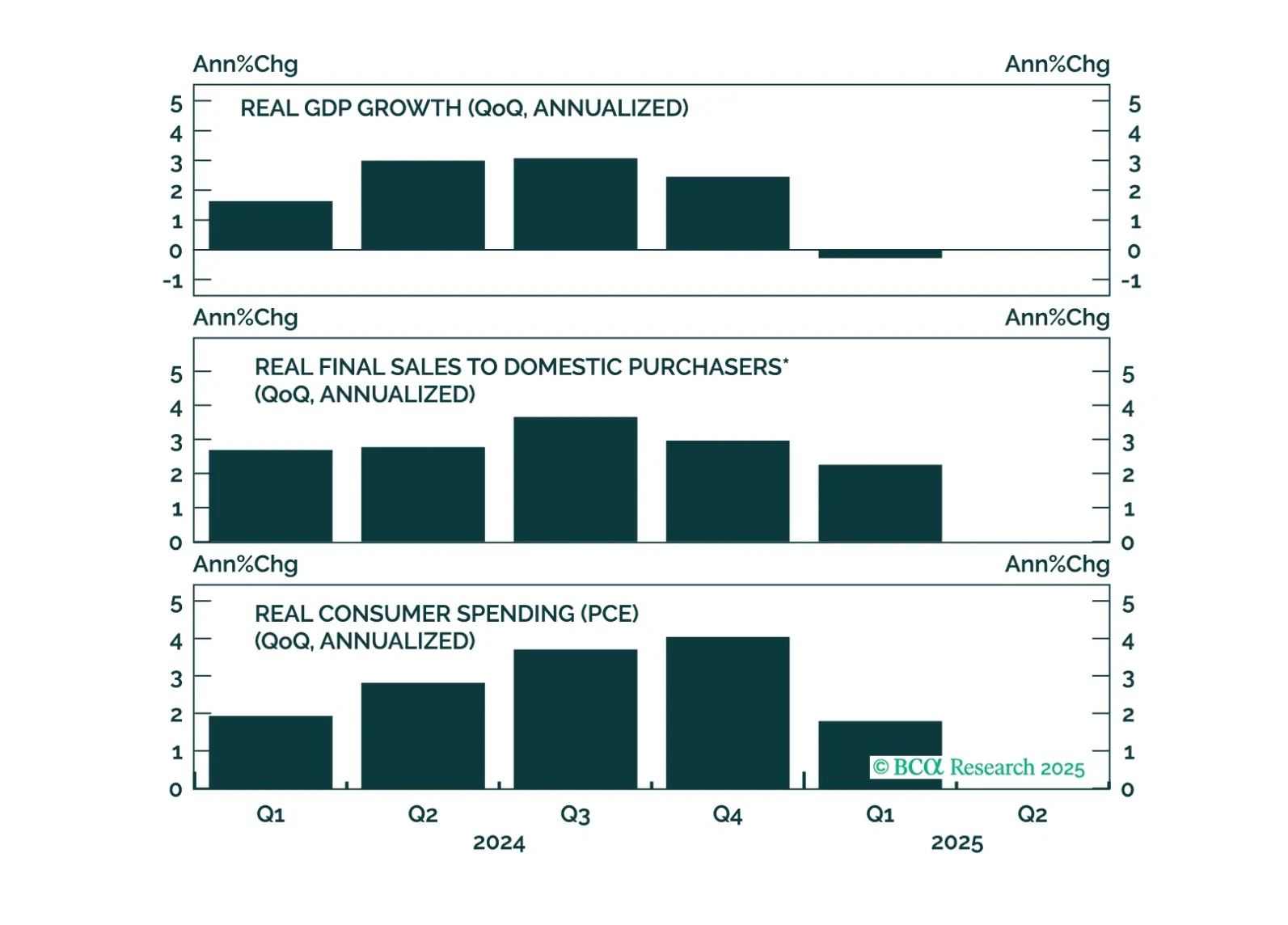

It may take several months for the tariff shock and policy uncertainty to filter through the real economy, but survey-based data are already sending a warning. Equities have priced in a lot of good news, and investors are too sanguine about the risk of a US recession.

The Fed held rates steady this afternoon, and the timing of its next move will be dictated by whether the tariff shock to inflation is transitory or more long lasting.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

In the long run, Mexico will emerge as one of the biggest winners of US tariffs as the US diversifies supply chains away from China. In the medium term, however, a US growth slowdown and tariffs will push Mexico into recession. In EM portfolios, we remain overweight Mexican equities, domestic bonds, and sovereign credit. We are reiterating a buy on 10-year domestic bonds. Go long MXN versus CNH.

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.