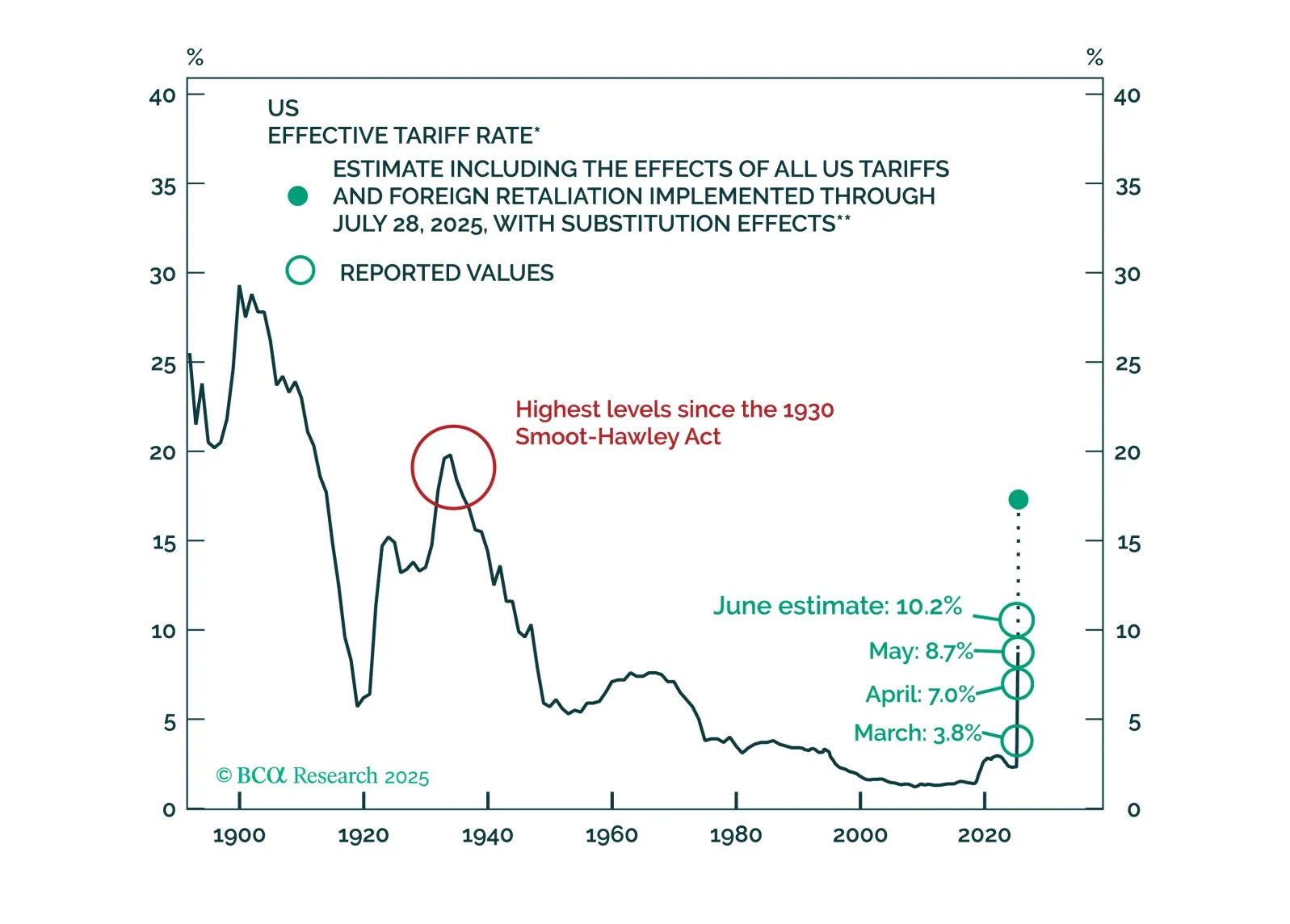

Tariffs

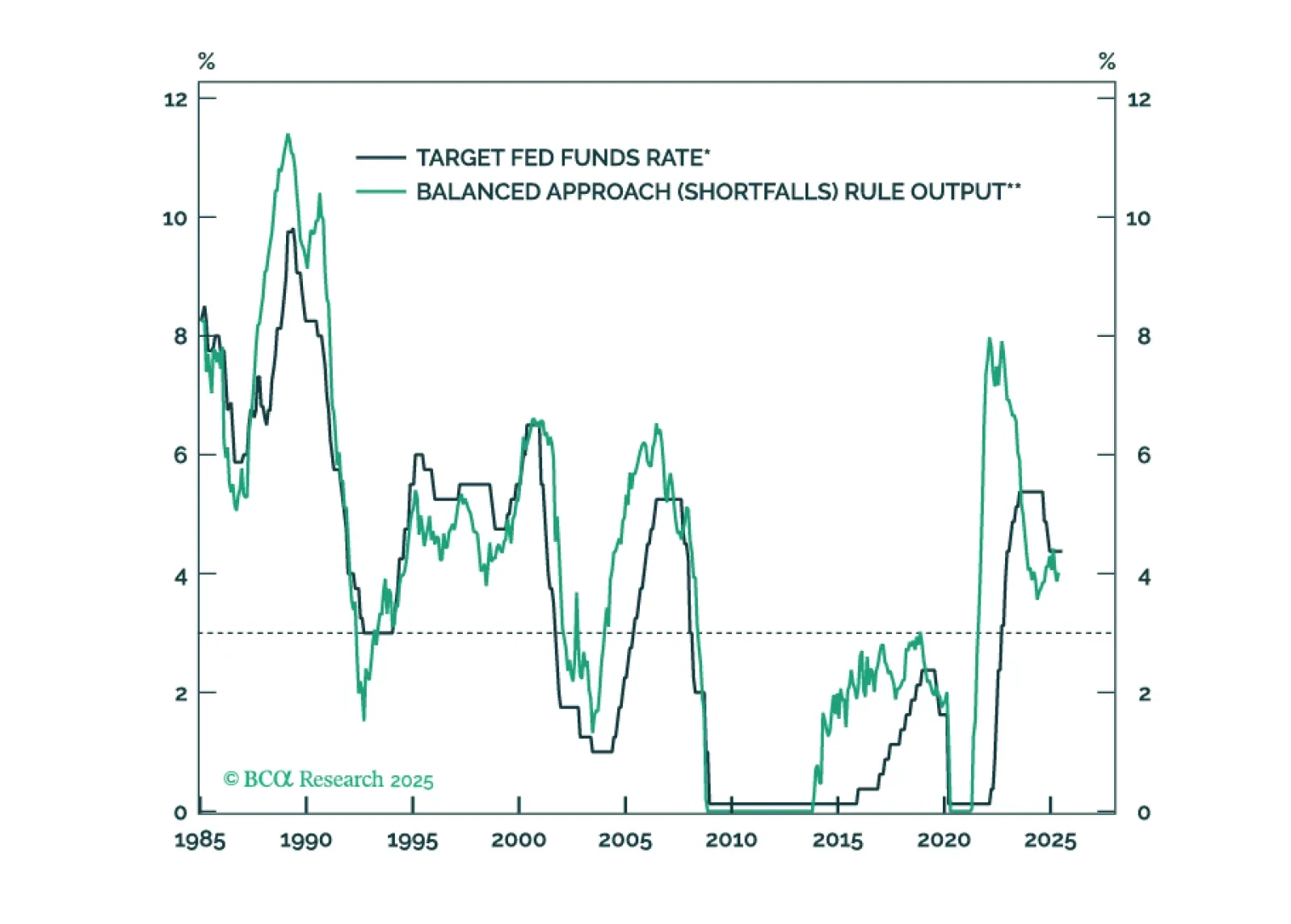

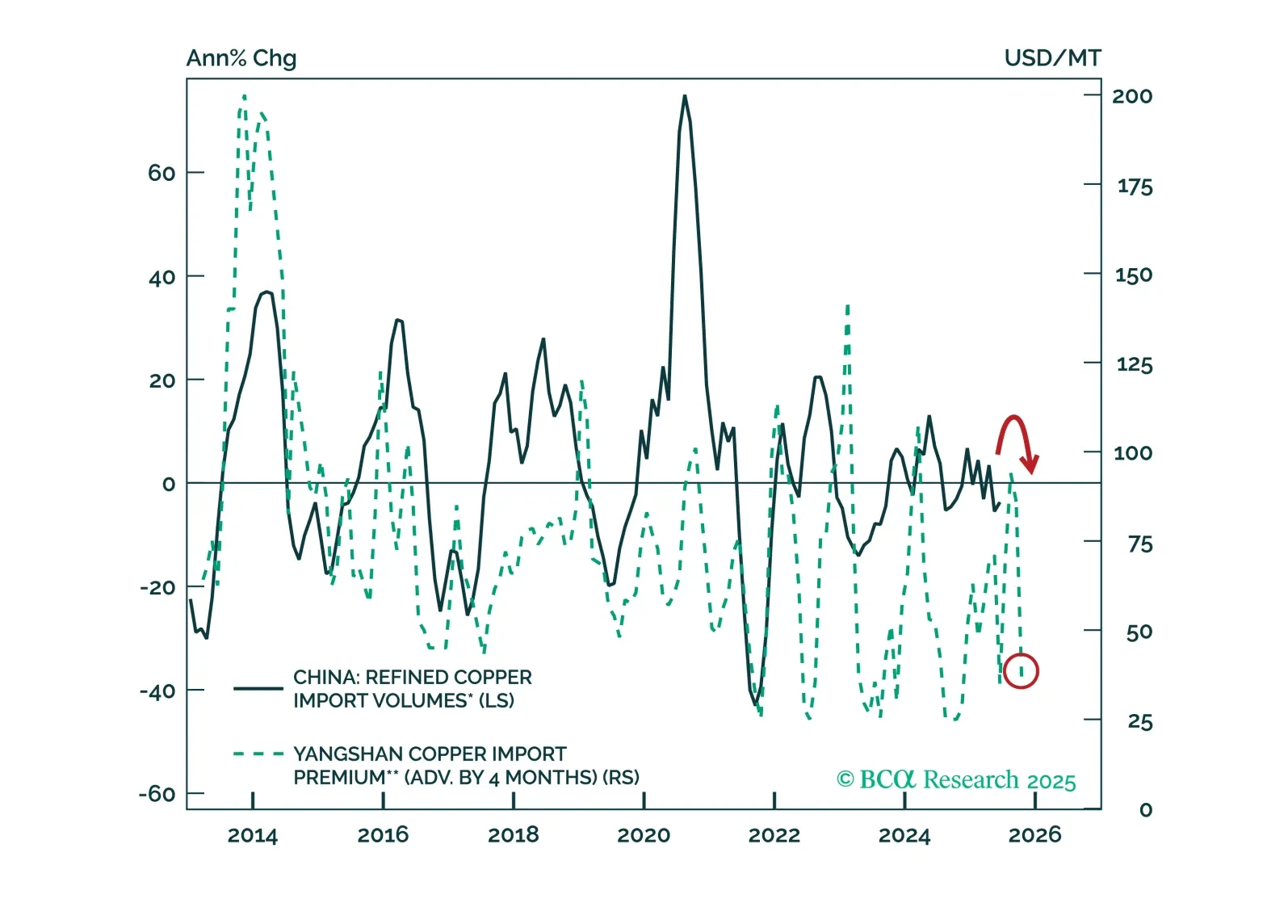

The Fed will keep rates on hold until the unemployment rate forces its hand.

Russia poses an immediate risk to global financial markets, and then perhaps a buying opportunity. Trump is pivoting to ceasefires and trade deals, but Russia could trigger a new tariff shock first.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

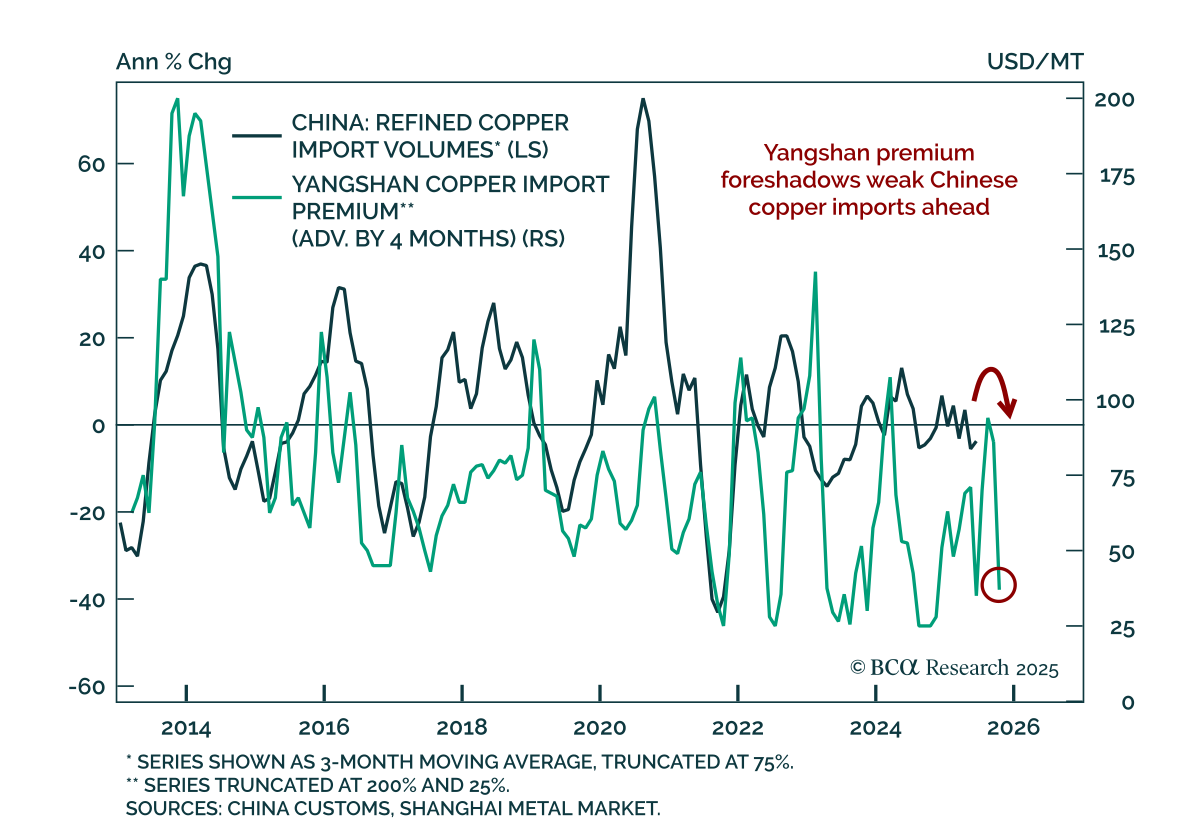

U.S. copper tariffs will redirect the metal’s trade flows from the US to the rest of the world, replenishing depleted inventories abroad. With global copper demand set to soften in H2, the red metal will likely face downward price pressure outside the US.

Stay long gold / short LME copper, and initiate an outright LME copper short.

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

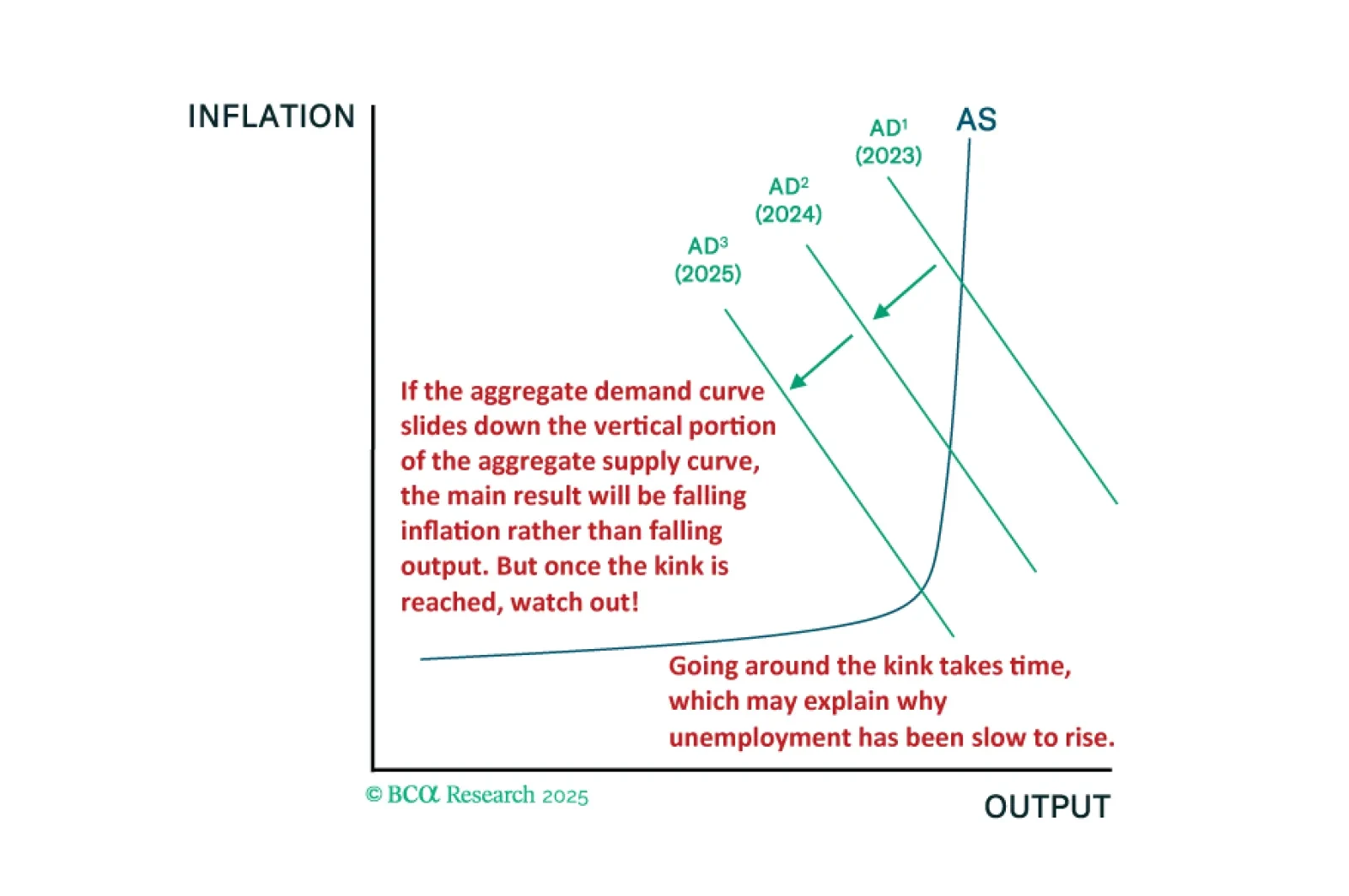

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

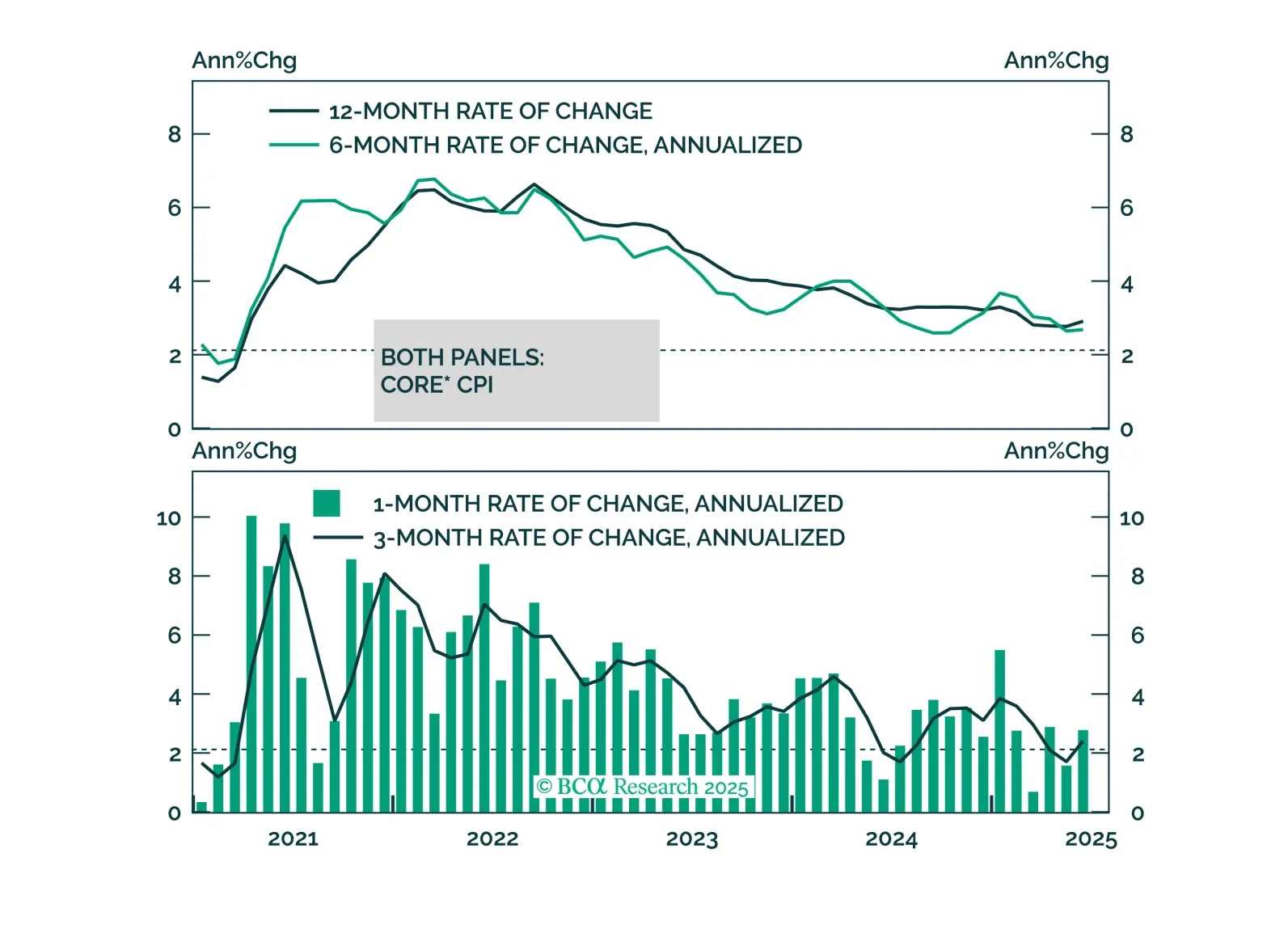

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.