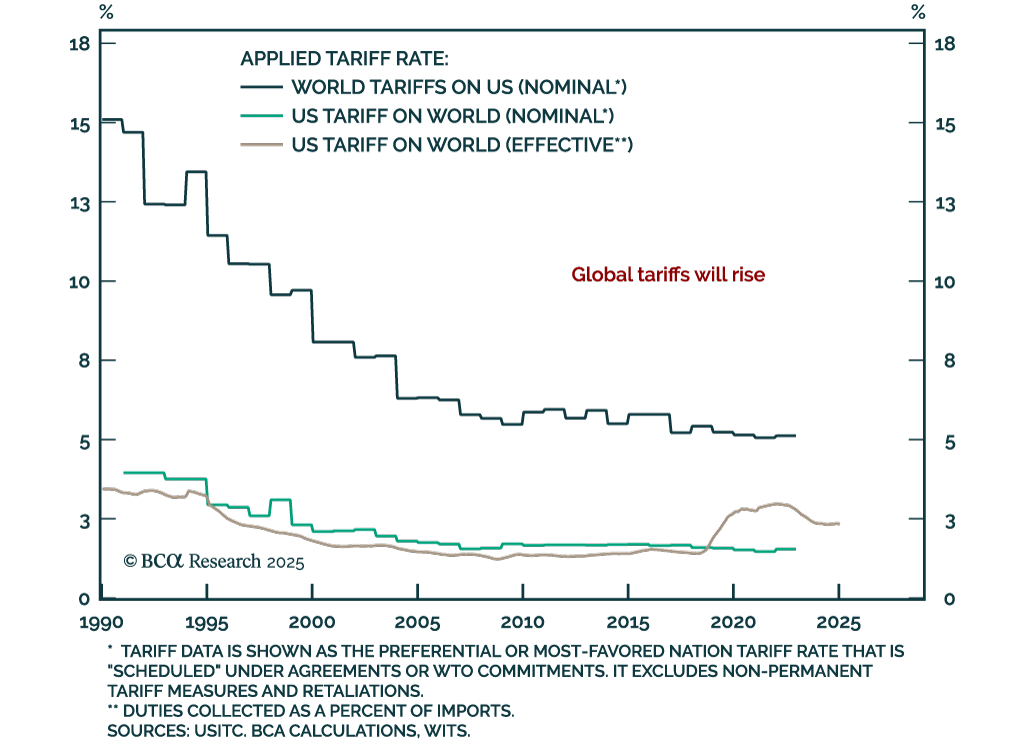

Tariffs

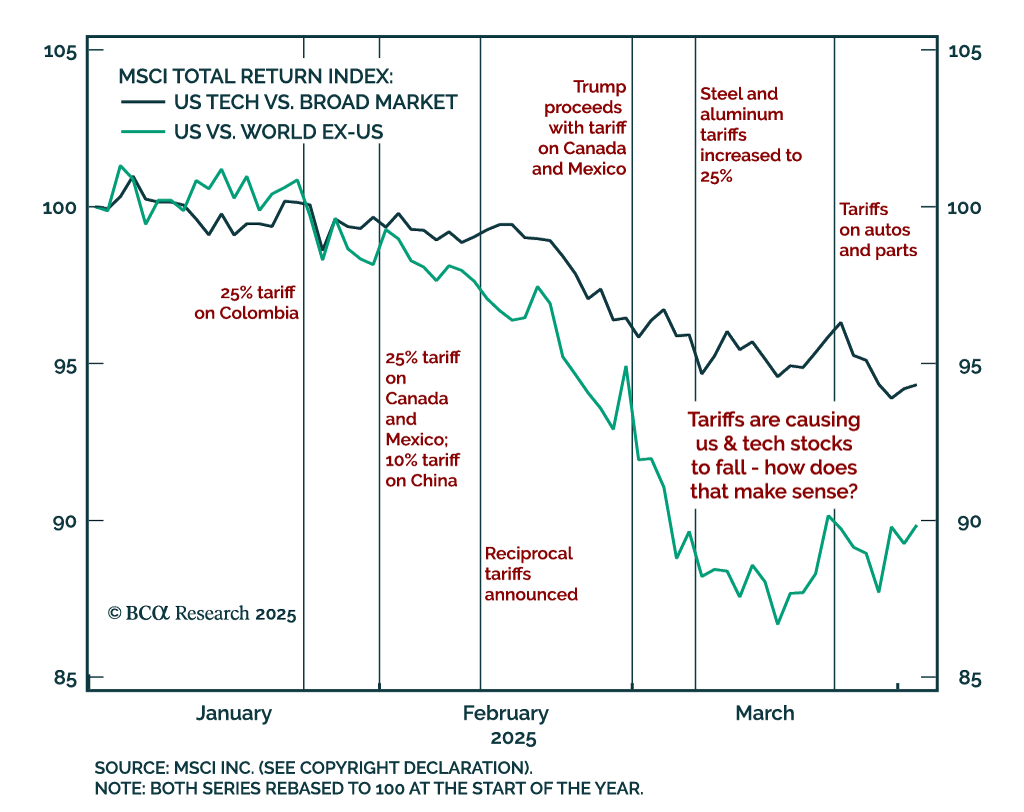

The world is focused entirely on the trade war between the US and… well everyone. This is fair given that there has been no greater market catalyst than Liberation Day since the pandemic. However, we continue to stress that the BIG PICTURE for macro investors is the rotation out of the US. A rotation that started well before April 2, despite the understanding of the investment community that some tariff action would be afoot.

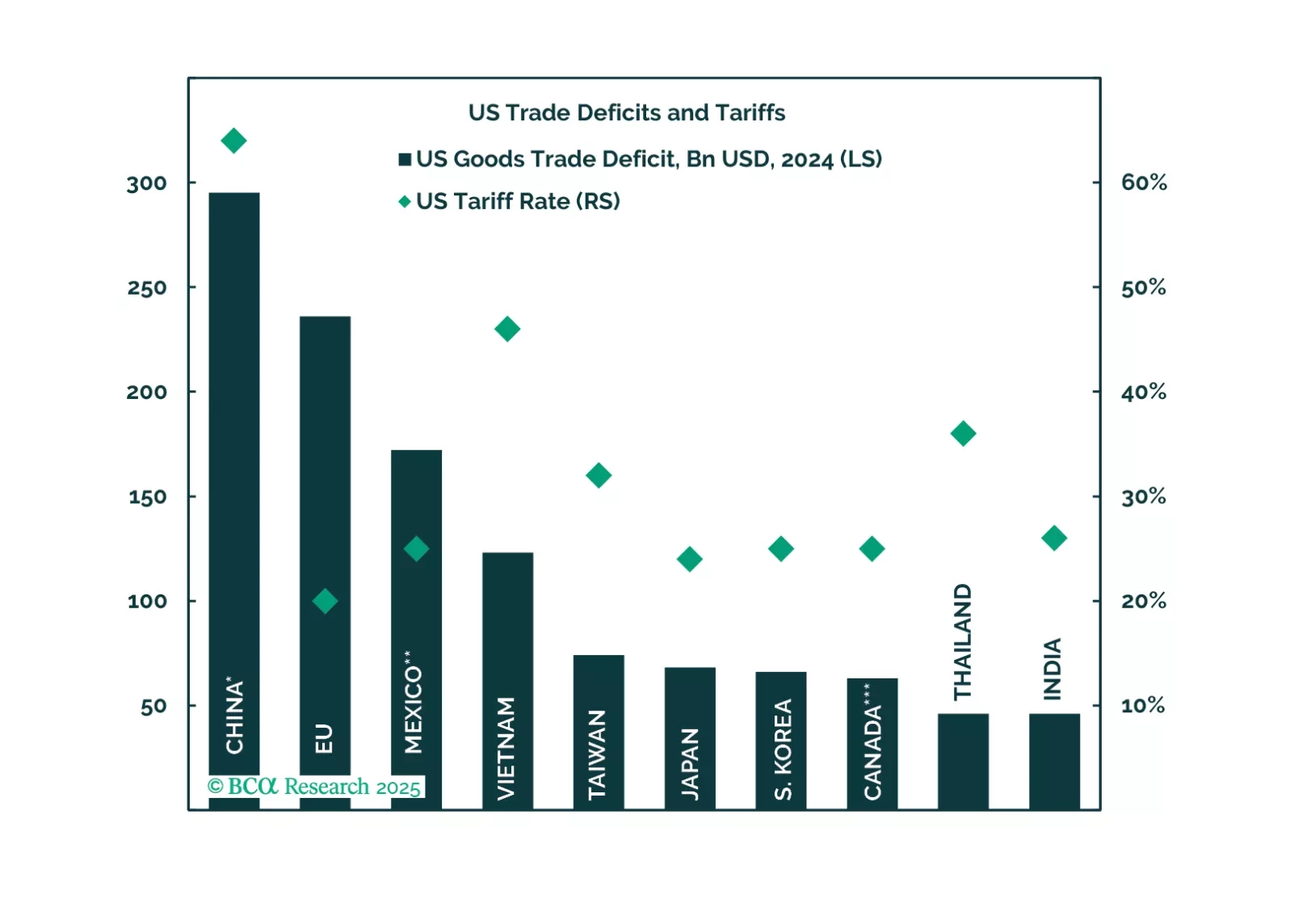

President Trump imposed tariffs on the world in his first 100 days, as we expected. Tariffs may have catalyzed a recession in the US, given the weakness in consumer sentiment and demand. Trump will soon backpedal and grant exemptions to countries that are negotiating, which he will showcase as proofs of his successful trade policy. While he may backpedal on his tariffs on other countries, China is not likely to receive the same treatment due to the US-China strategic competition.

Equities will find a bottom when the full effects of tariffs on earnings and economic growth are priced in. The bottom of the market appears a long way away, and the S&P 500 may end up as low as 4,300, barring any reversals in trade policy that could undo the damage.

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

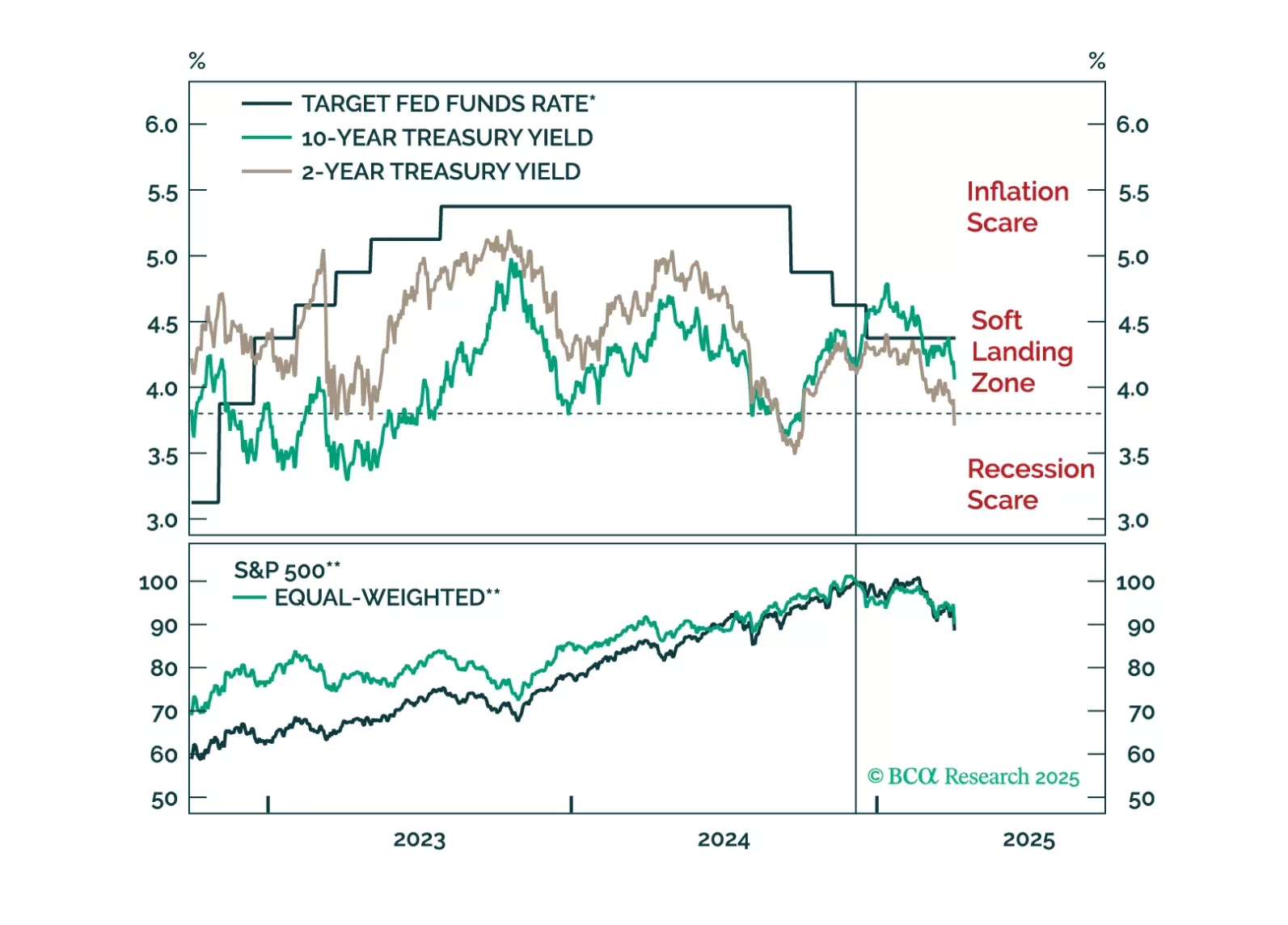

The March employment report showed strong job growth, but the labor market remains in a fragile state and the demand shock from tariffs could be the catalyst that tips it over the edge into recession.

On the one hand, US tariffs are much more deflationary for the rest of the world than for the US, so interest rate differentials might move in favor of the US dollar in the near term. On the other hand, portfolio outflows from the US will weigh on the greenback over a cyclical horizon. We recommend buying Mexican and Central European domestic bonds.

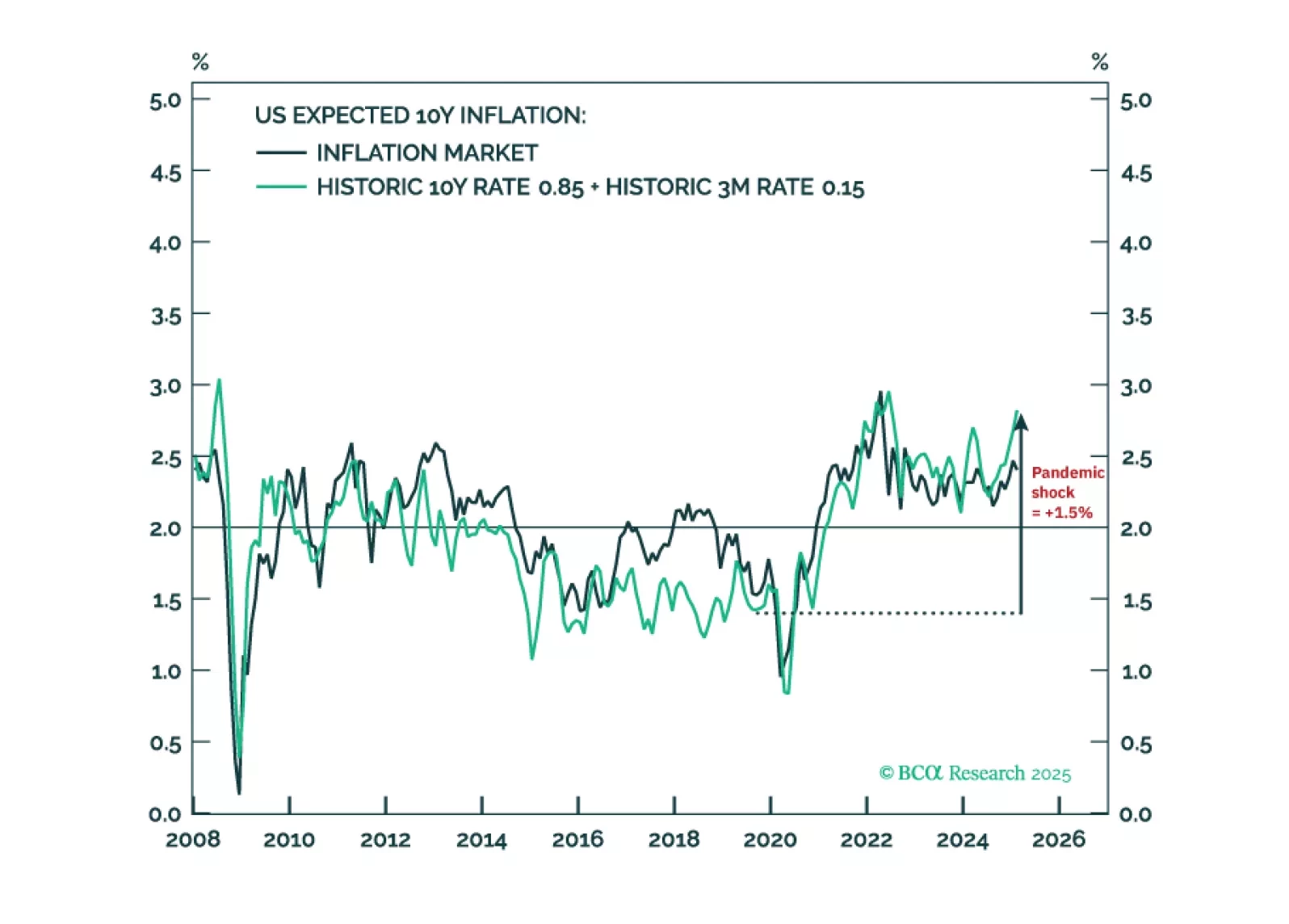

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.