Sovereign Debt

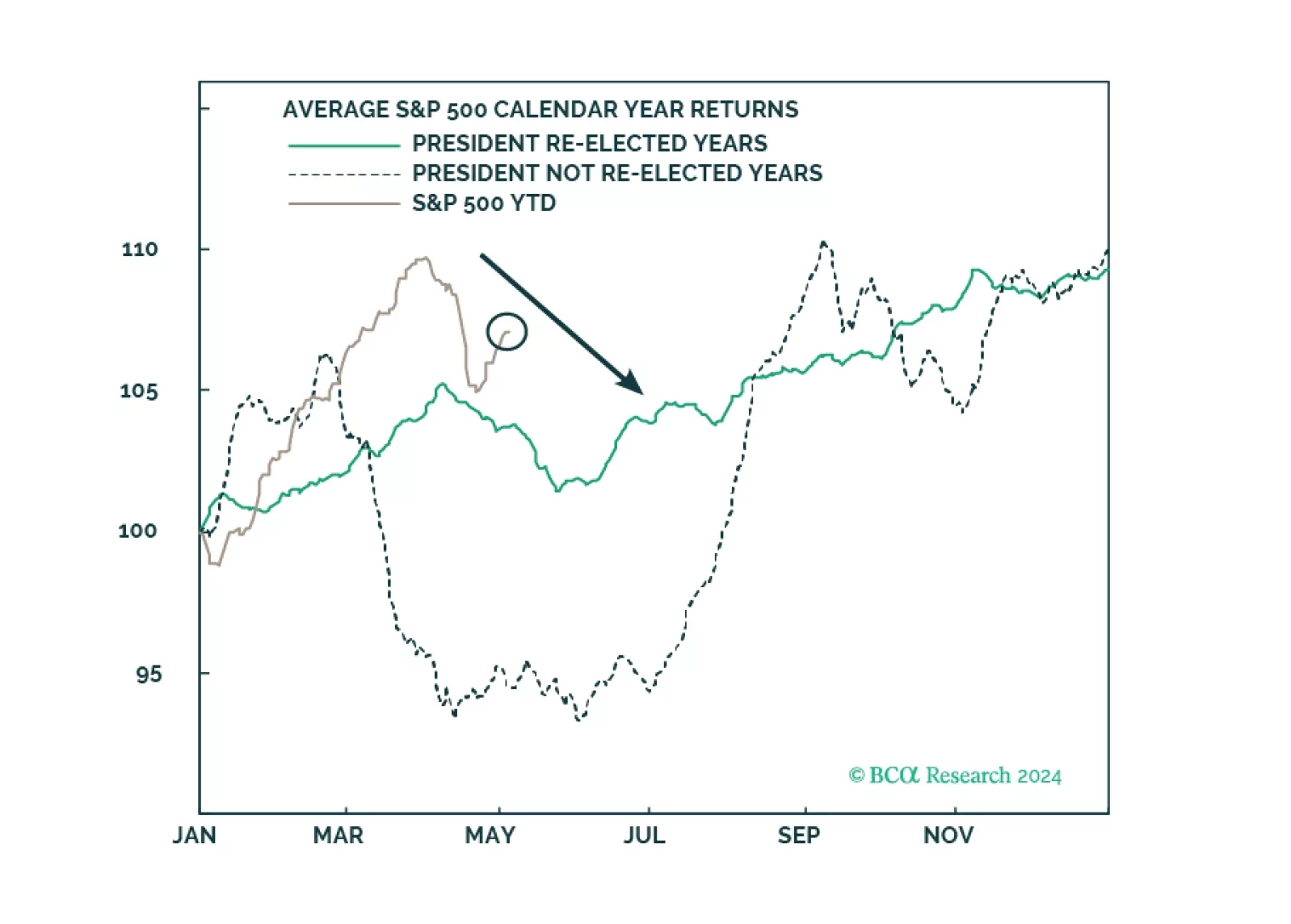

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

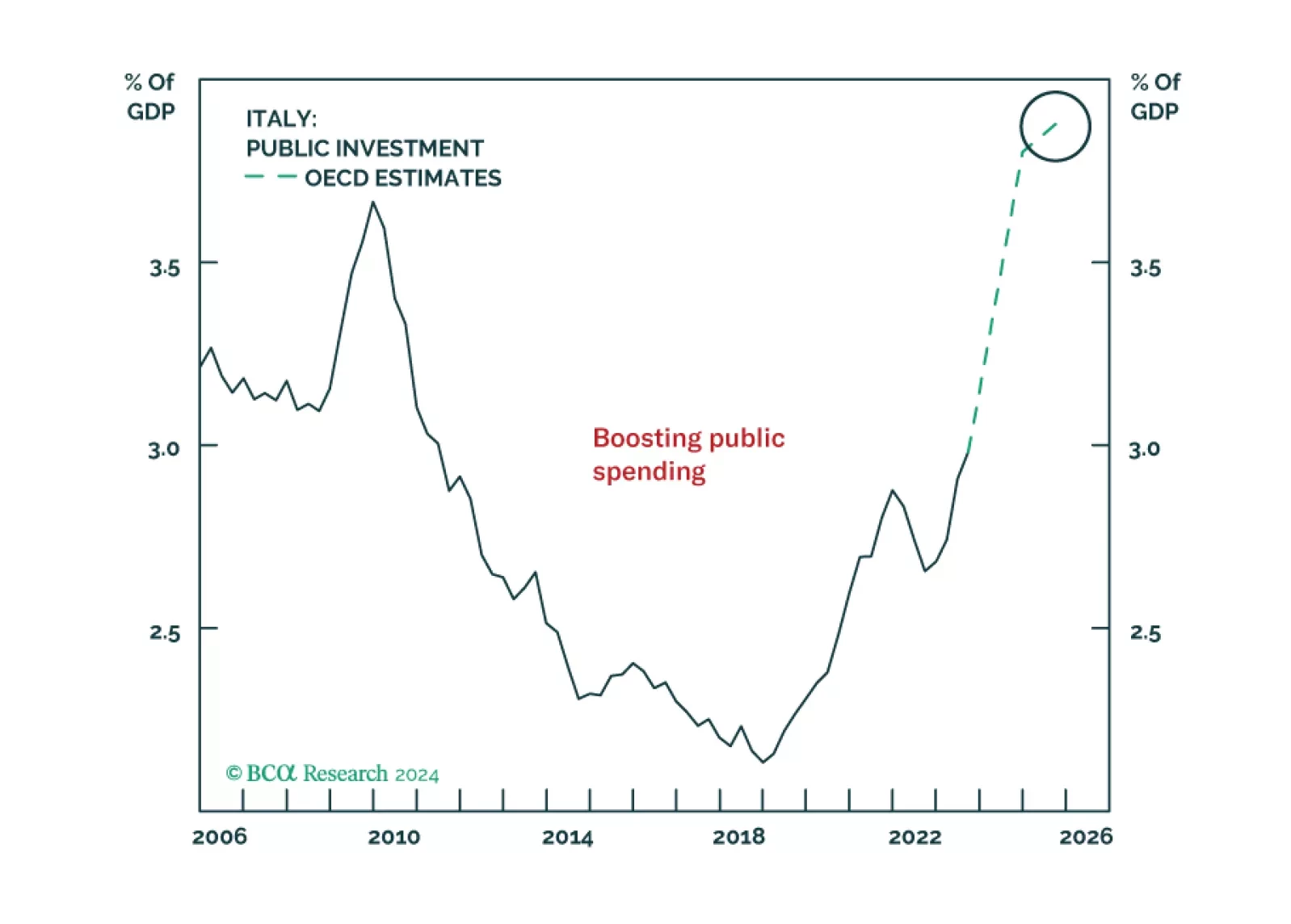

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.