Russia

As part of our new and improved GeoMacro service, please find attached our Global Risk Outlook, a quarterly digest of scenario probabilities and estimated market impacts for all the major geopolitical topics in the world today.

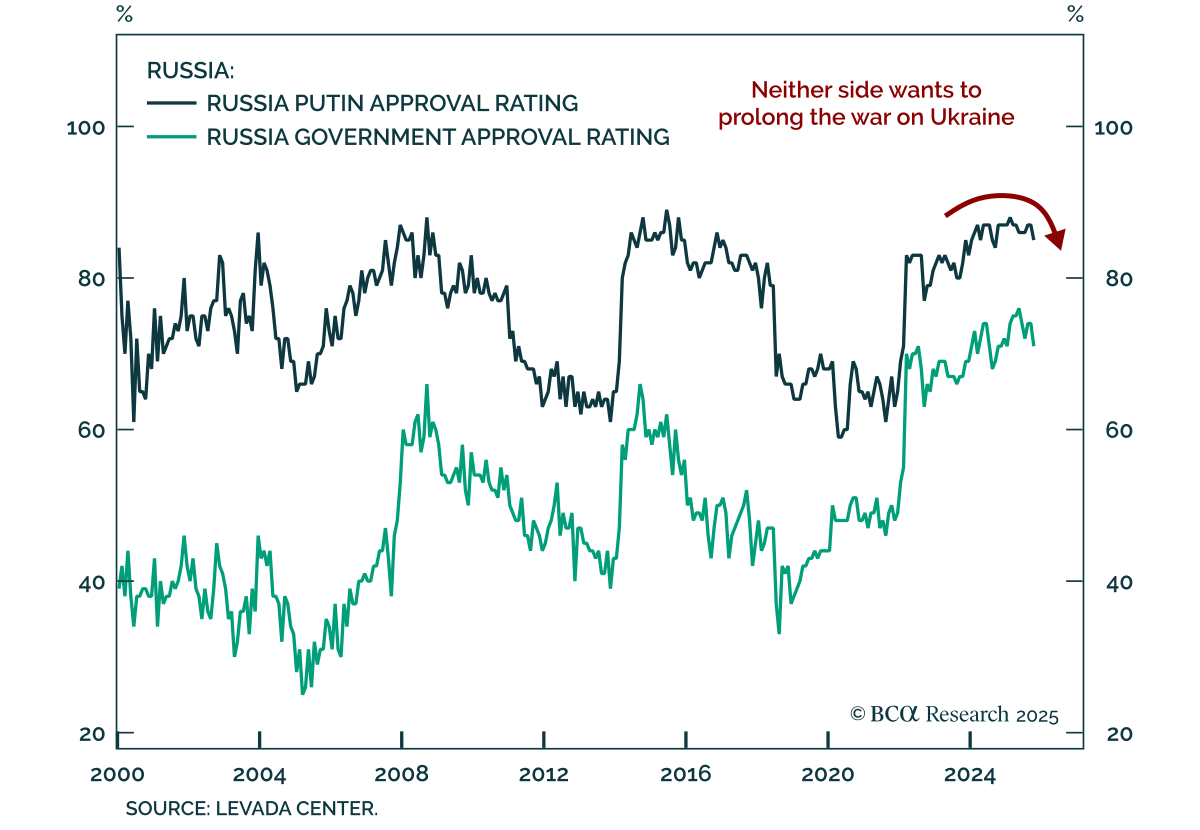

Geopolitical risk may rotate to Russia/Ukraine in Q3, while the Middle East could reignite in Q4.

The odds of a near-term US-Iran deal have gone up slightly, but the odds of a Russian provocation that divides NATO have also gone up.

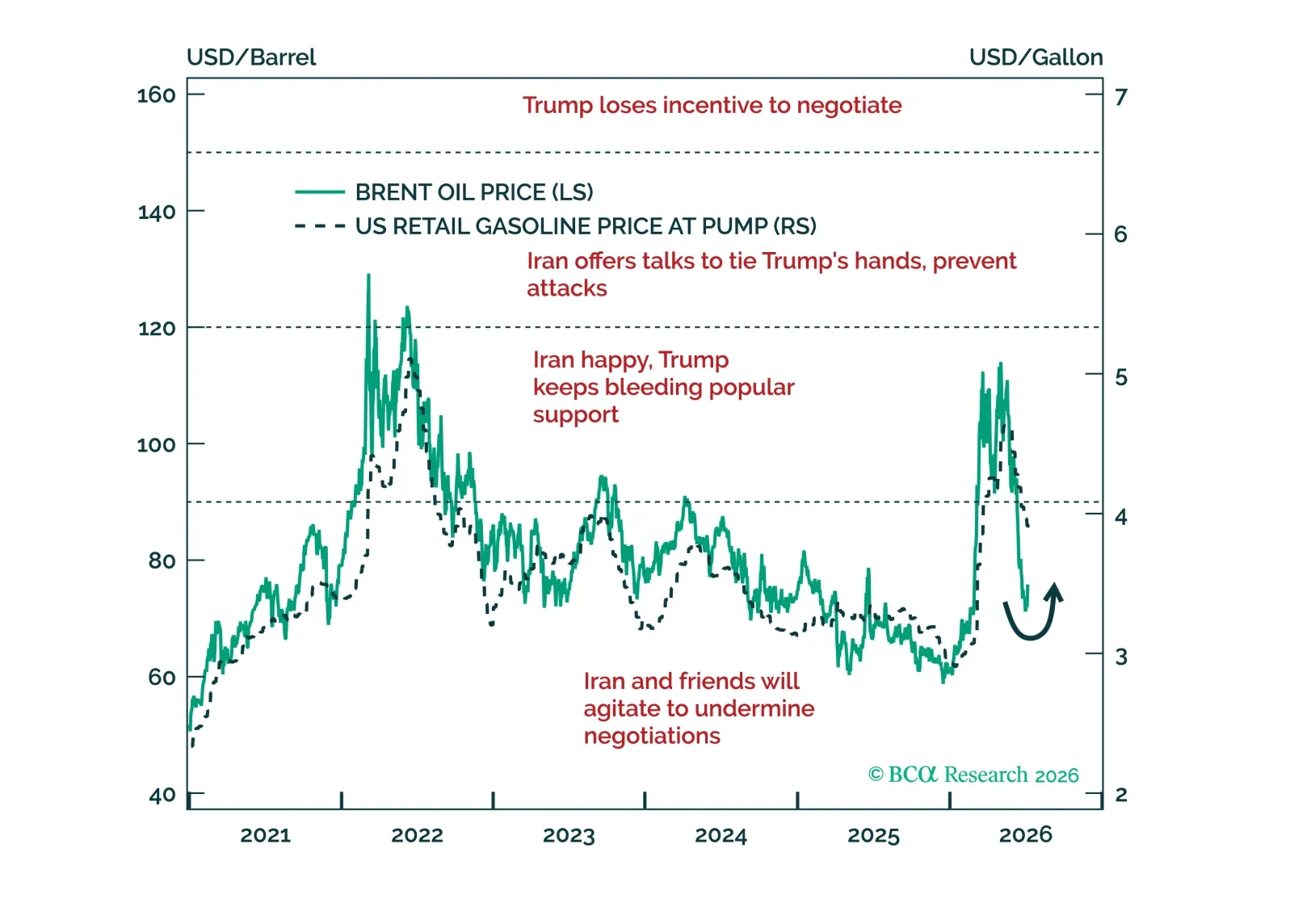

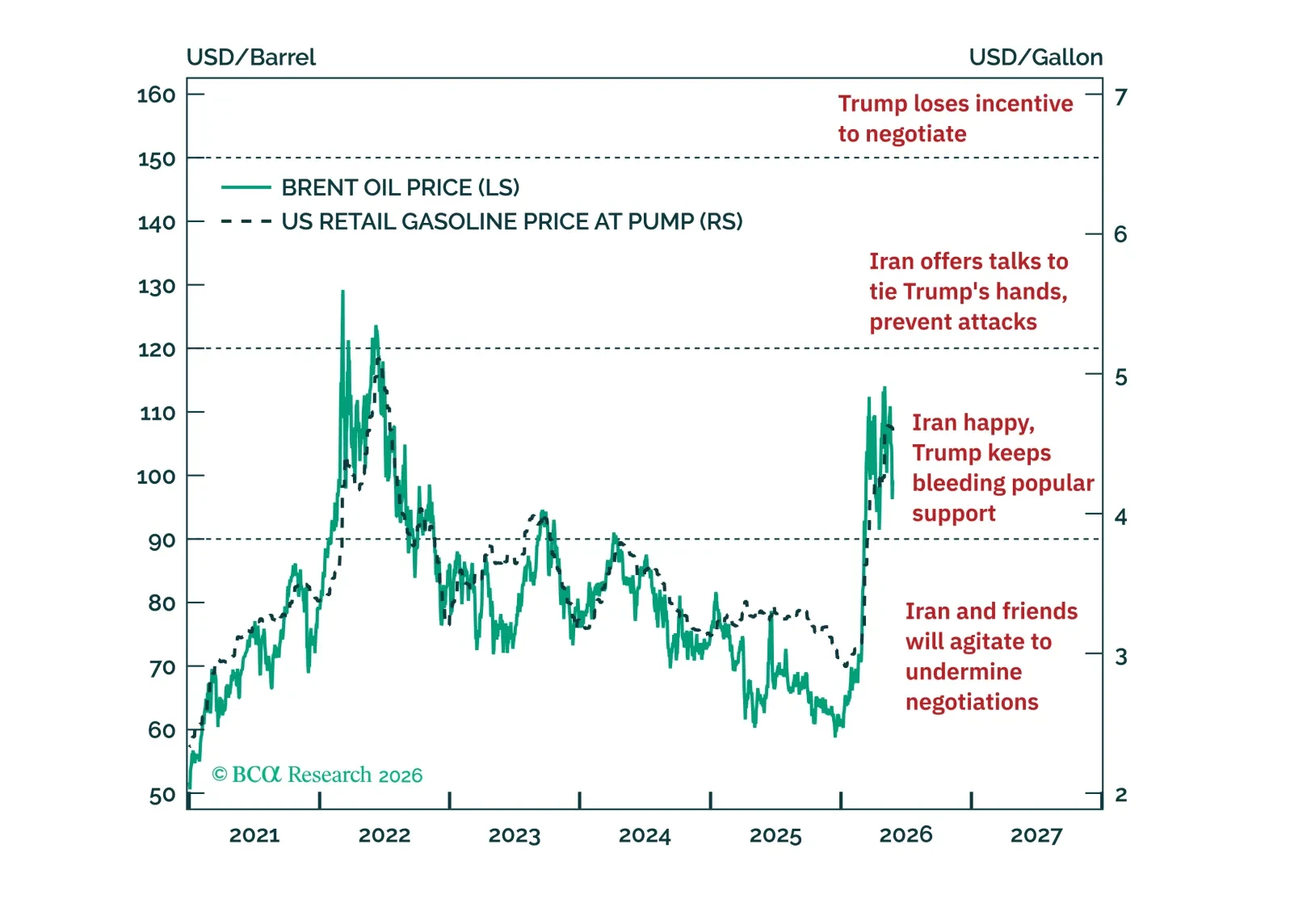

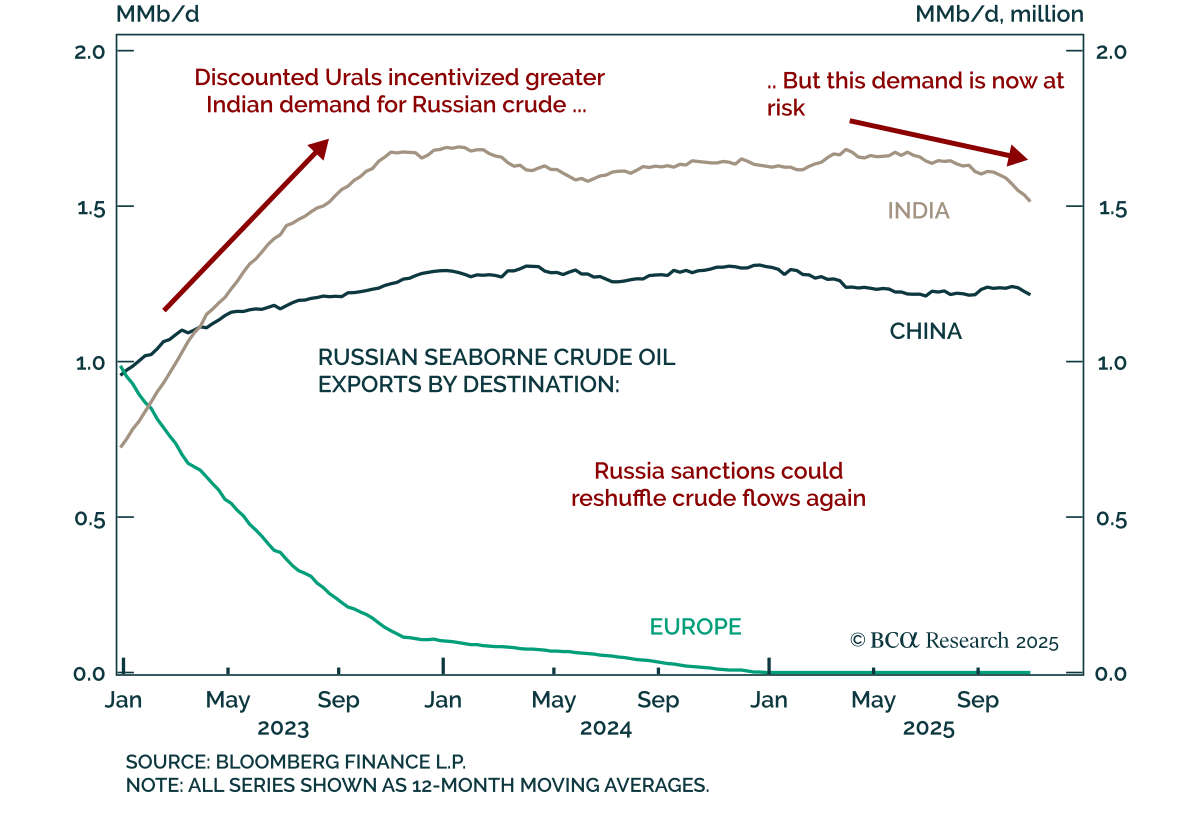

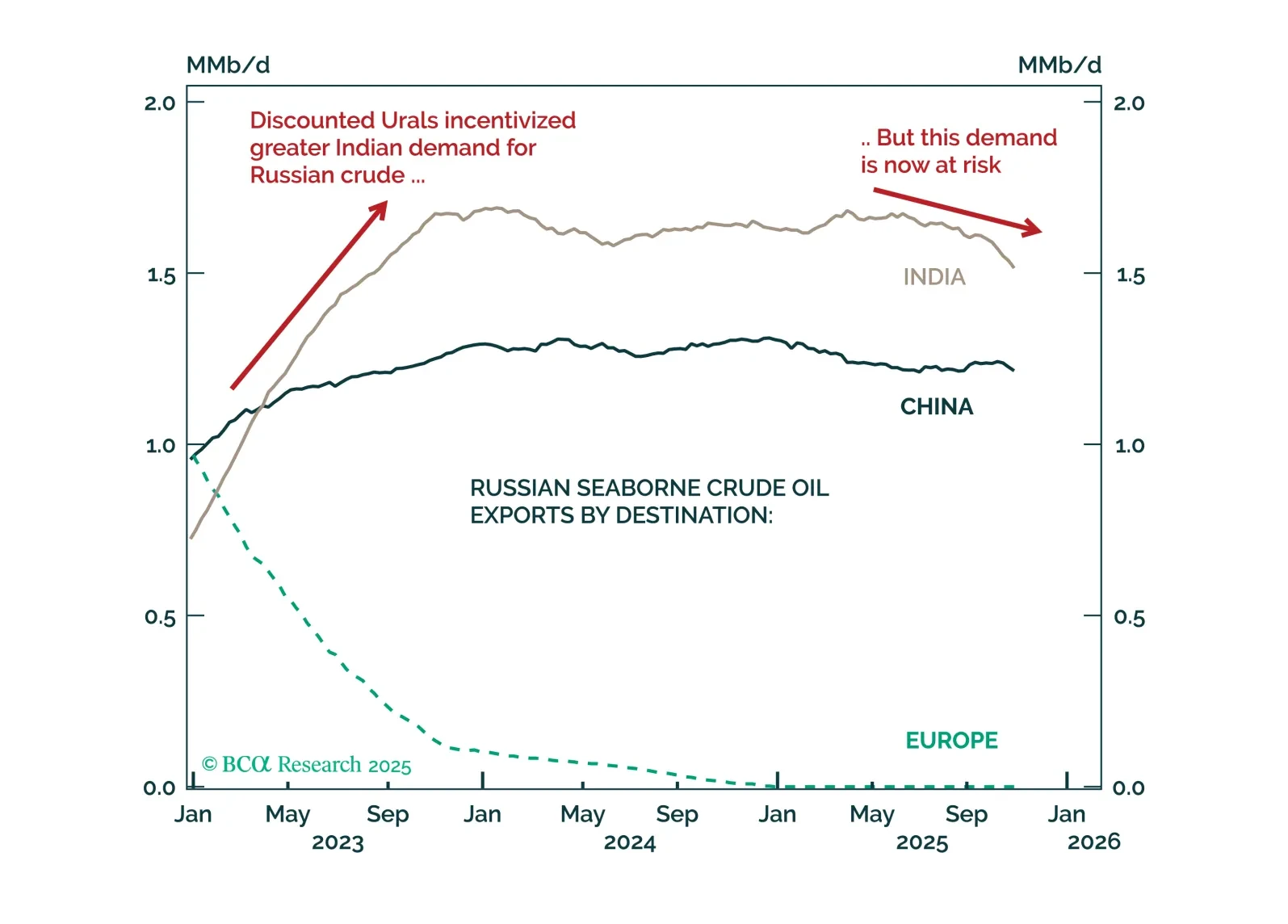

US restrictions on Russian crude exports could disrupt global oil supplies and trade flows over the near term. However, they are unlikely to have a meaningful impact on crude prices over a cyclical timeframe. Stay short Brent.

Reduce risk exposure in the very near term as President Trump's ceasefire effort falters, Russia tensions spike, and US-China trade prospects suffer.

A world of political churn favors safe havens — buy yen, stay overweight US stocks, and avoid chasing the fragile rally in China.

Rising Russia-NATO risks, tactical oil/gold trades, tougher sanctions on Russia (maybe China), China stimulus with ~5% growth target, and US checks on Trump’s ambitions will define Q4.