Recession-Hard/Soft Landing

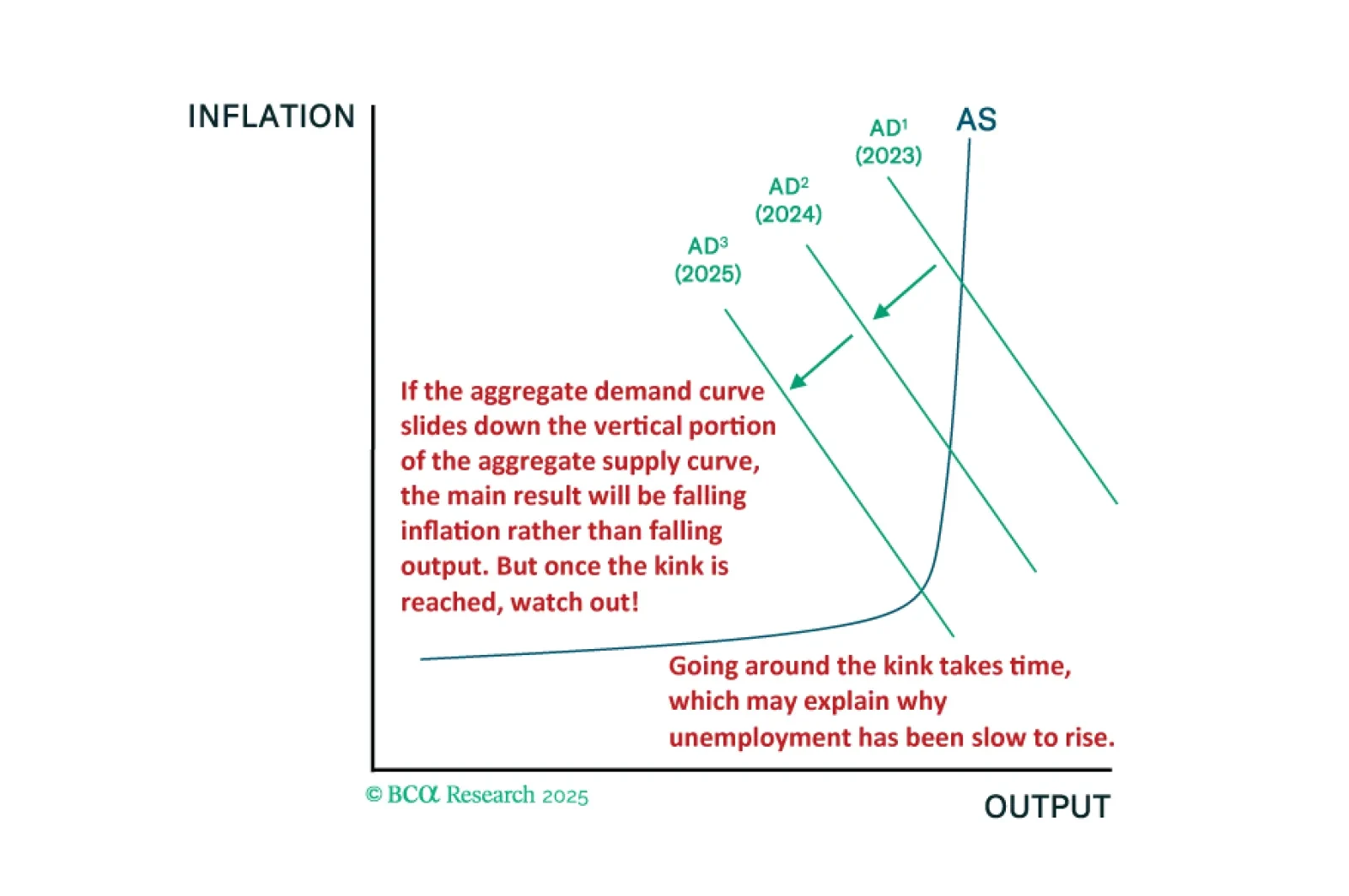

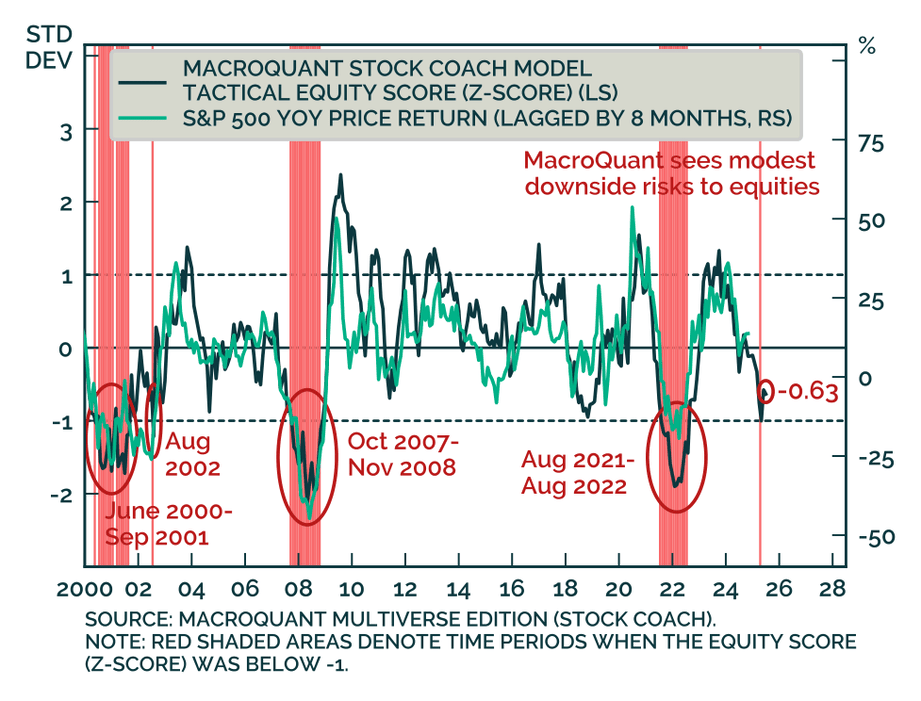

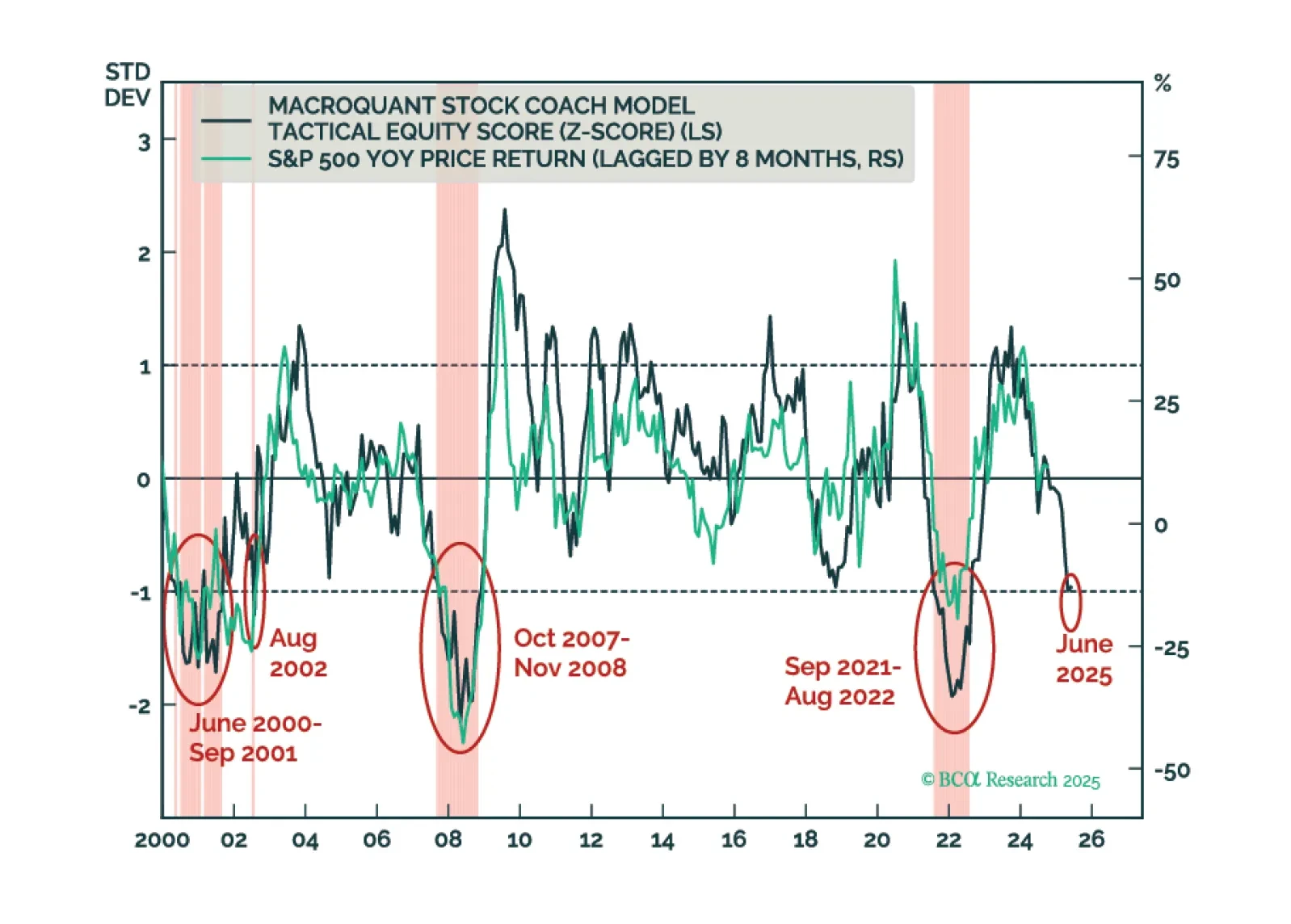

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

We will abandon our recession call if US economic data show clear signs of stabilization over the summer months. For now, that has not happened. Maintain a modest underweight to stocks but look to get more defensive if MacroQuant’s equity z-score falls below -1.

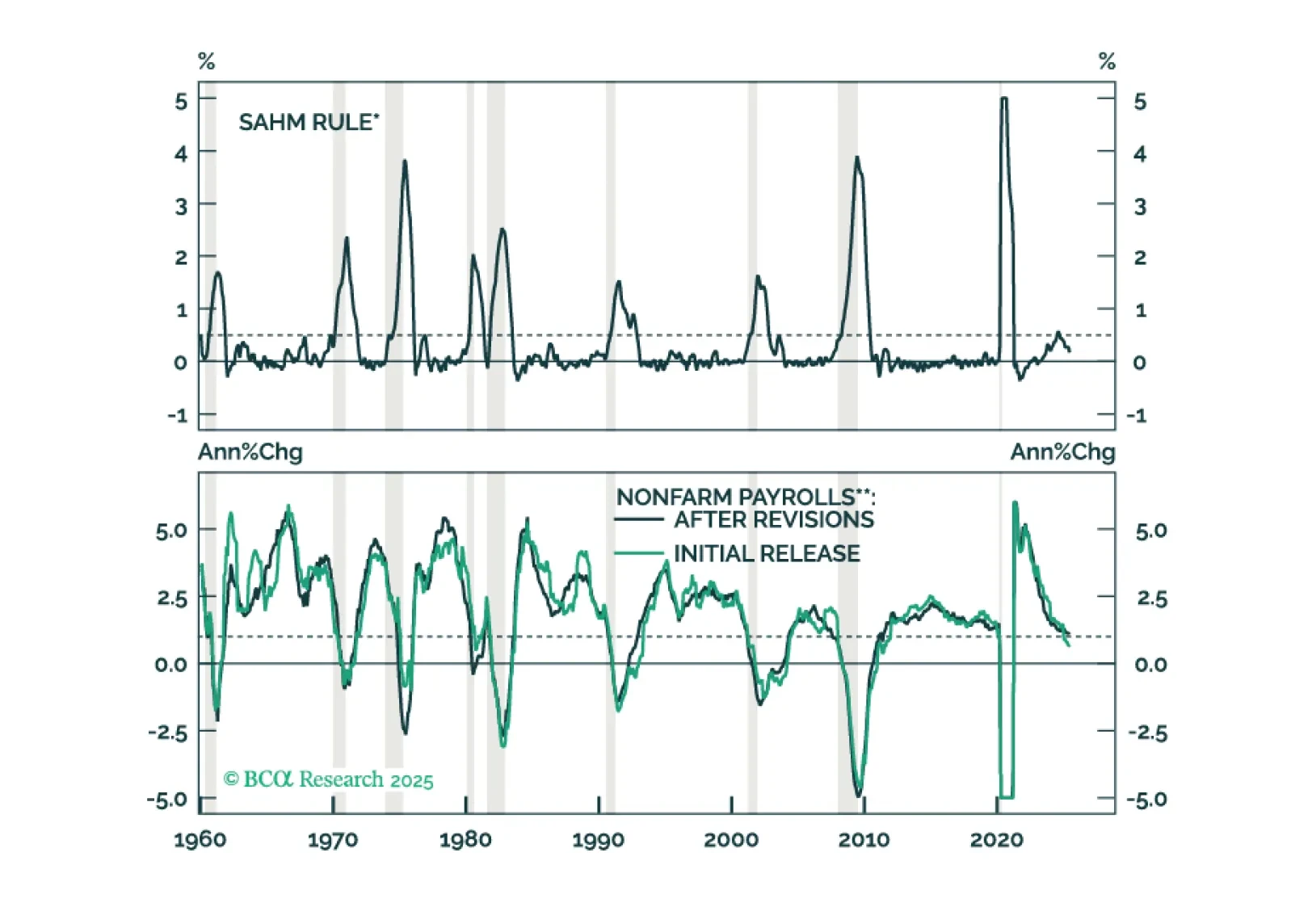

June’s employment report showed a tick down in the unemployment rate, an improvement that rules out a Fed rate cut later this month.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

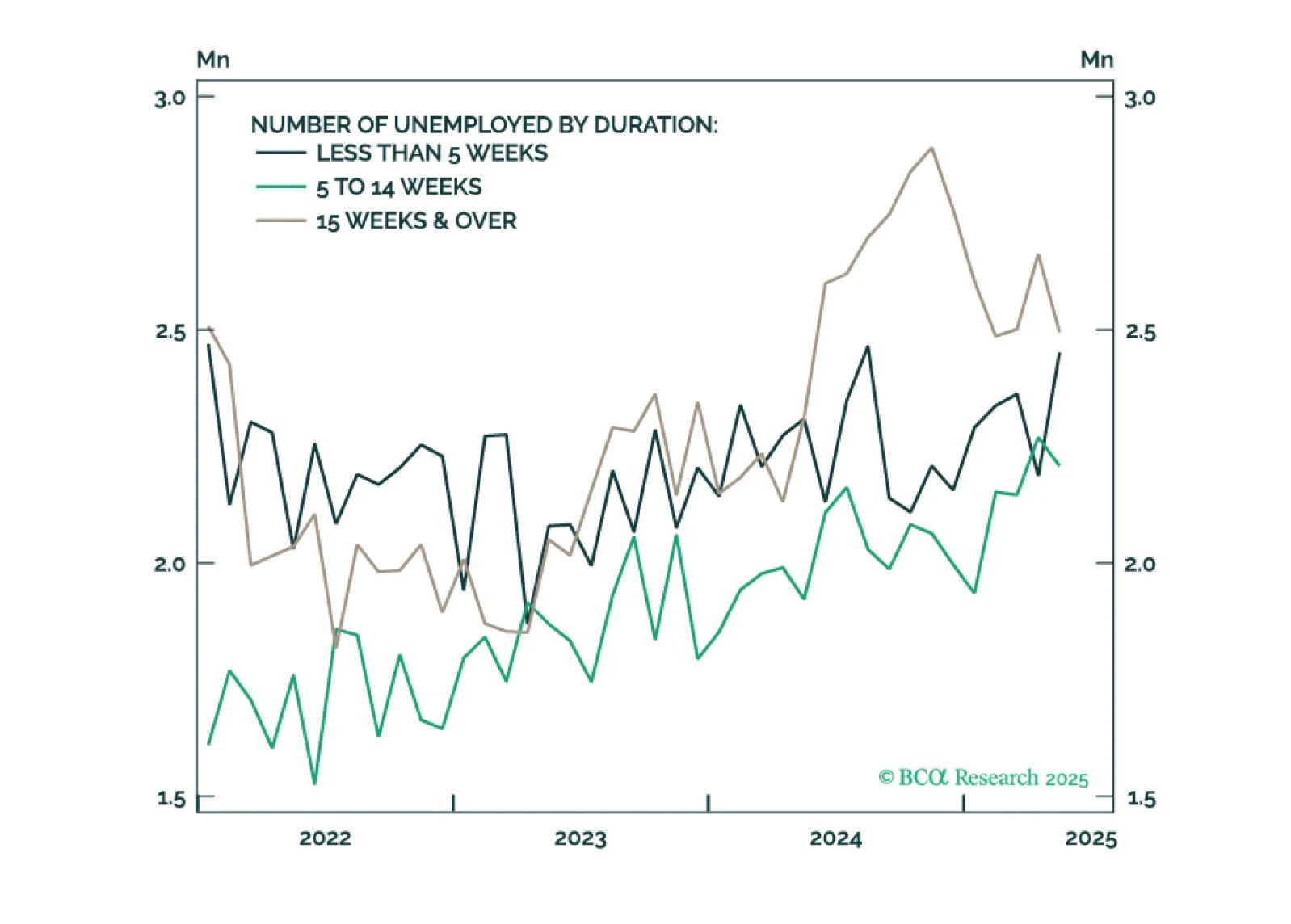

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.