Policy

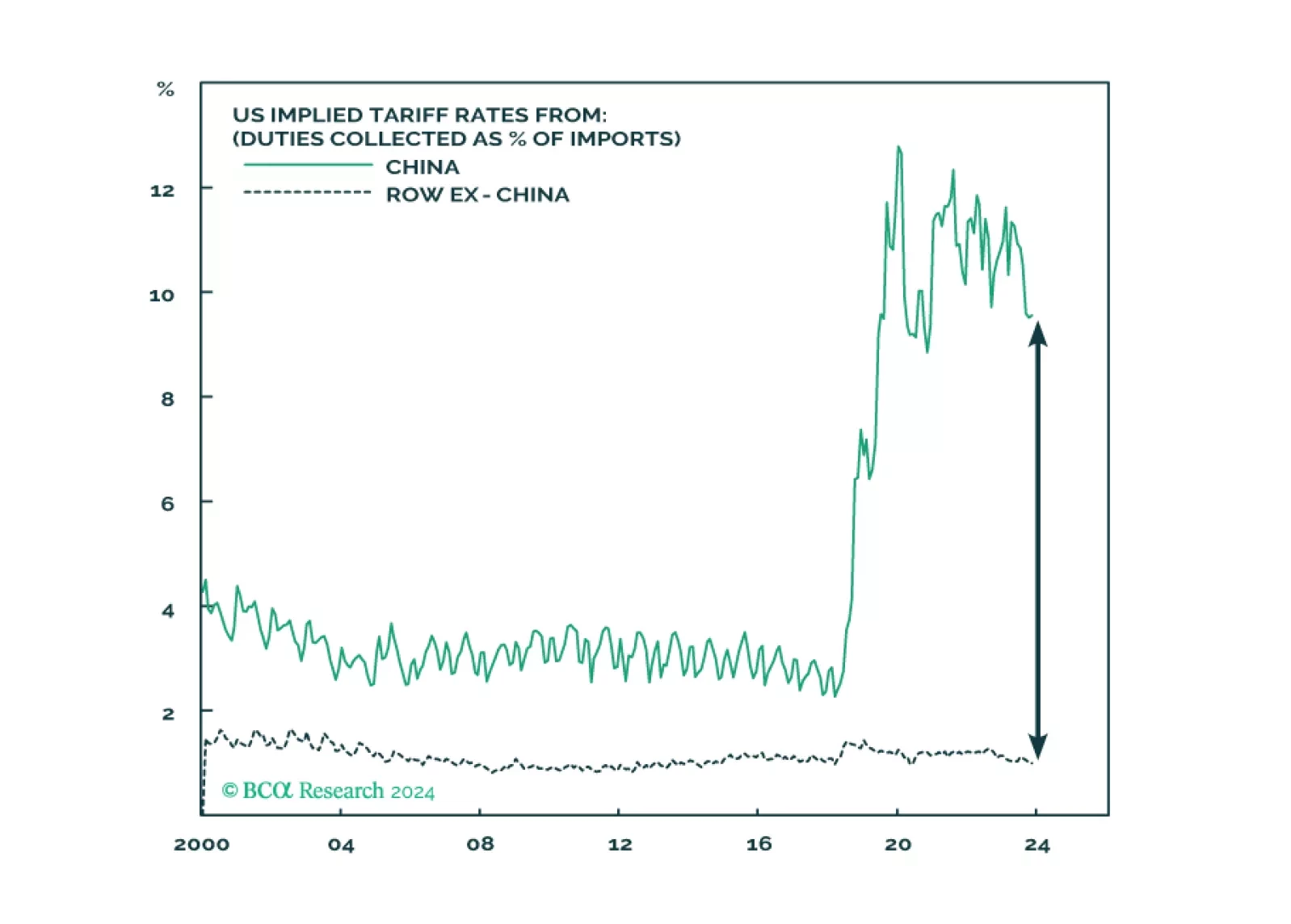

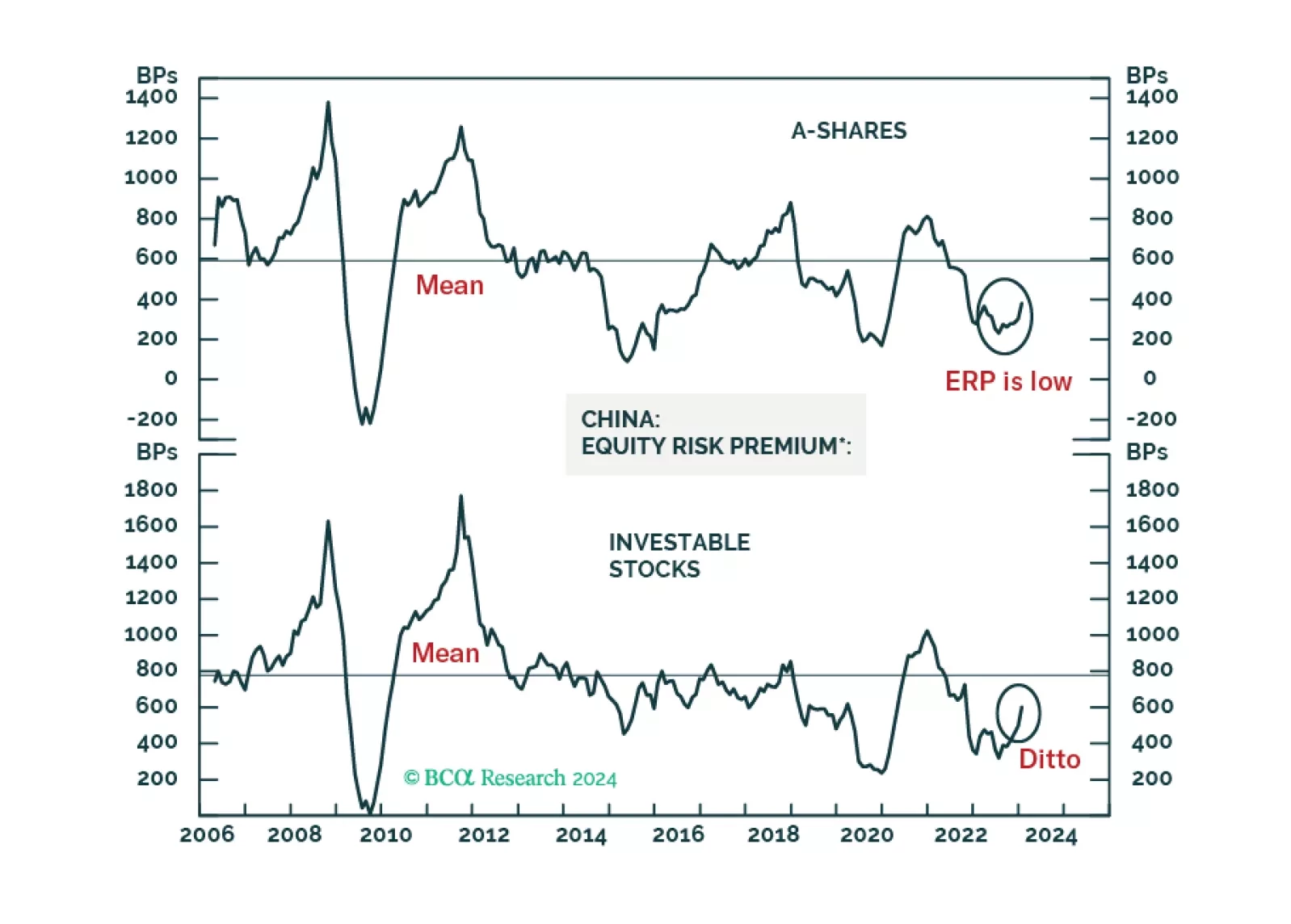

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

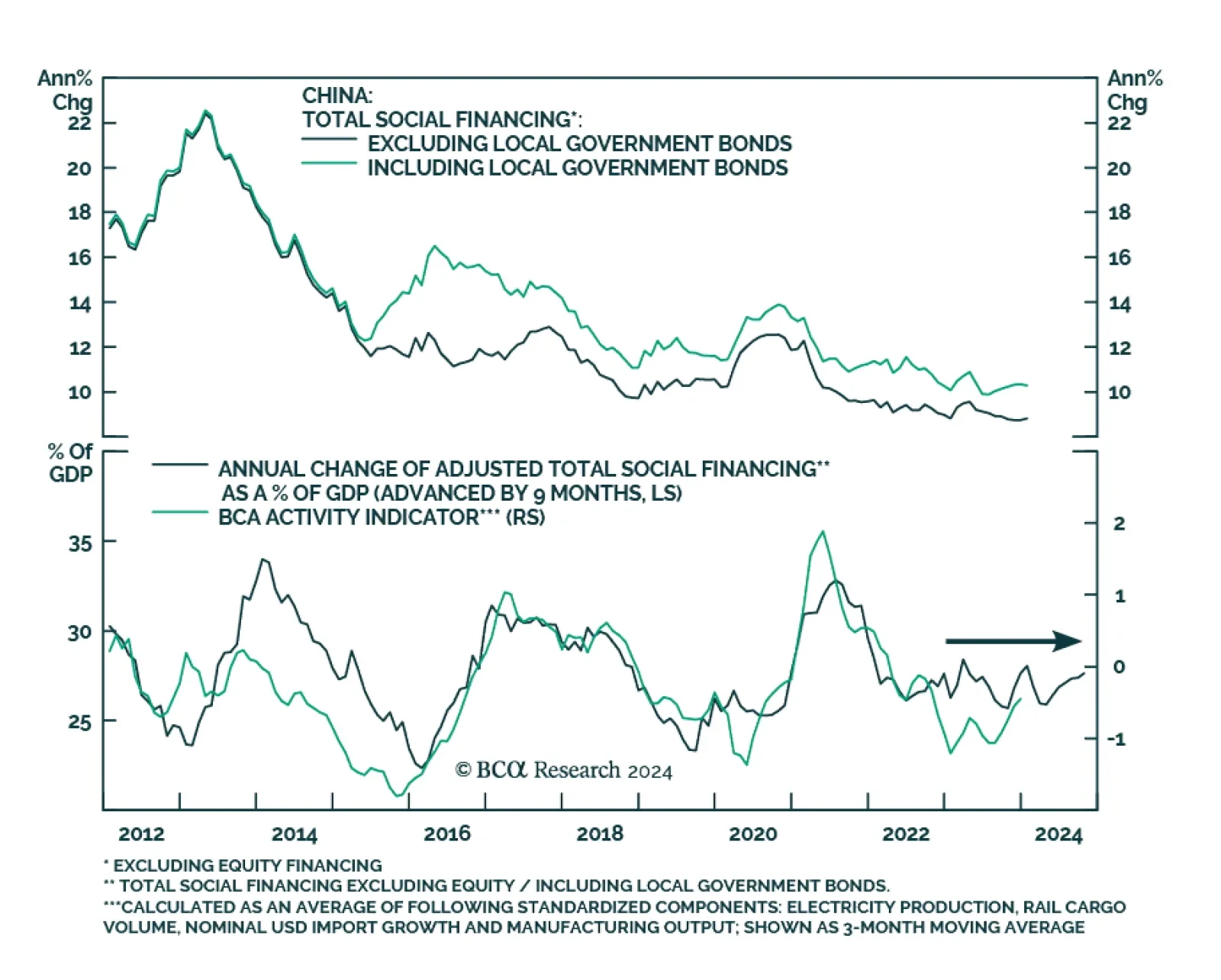

China’s credit data update for January delivered a mixed signal on Friday. The CNY 6.50 trillion increase in aggregate financing beat expectations of CNY 5.60 trillion and marked a significant acceleration from CNY 1.94 trillion in December. Similarly, the…

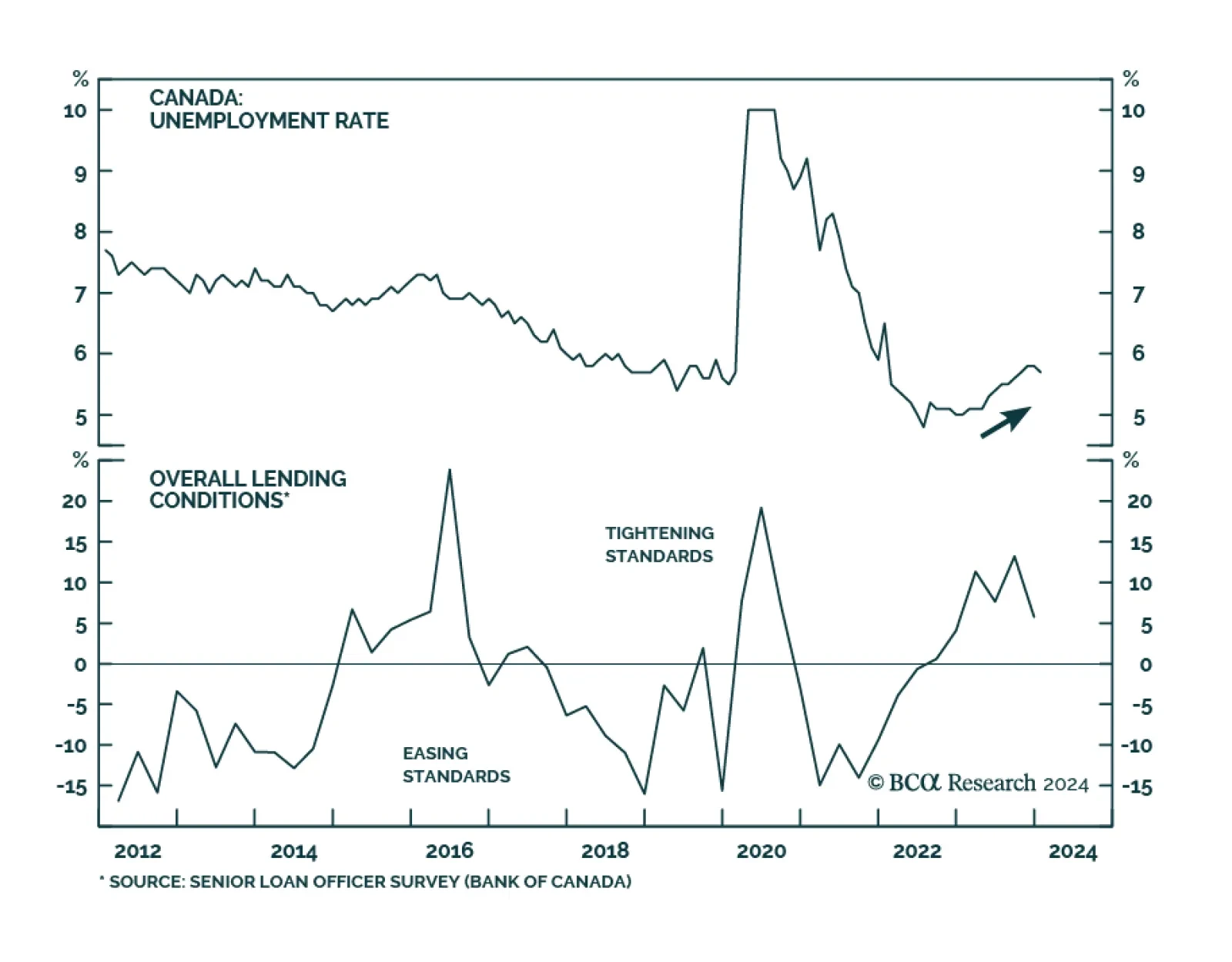

The latest Canadian data suggest that although demand is cooling down, the Canadian economy is not in freefall. The unemployment rate fell for the first time since December 2022, declining by 0.1 percentage points to 5.7%, compared to consensus…

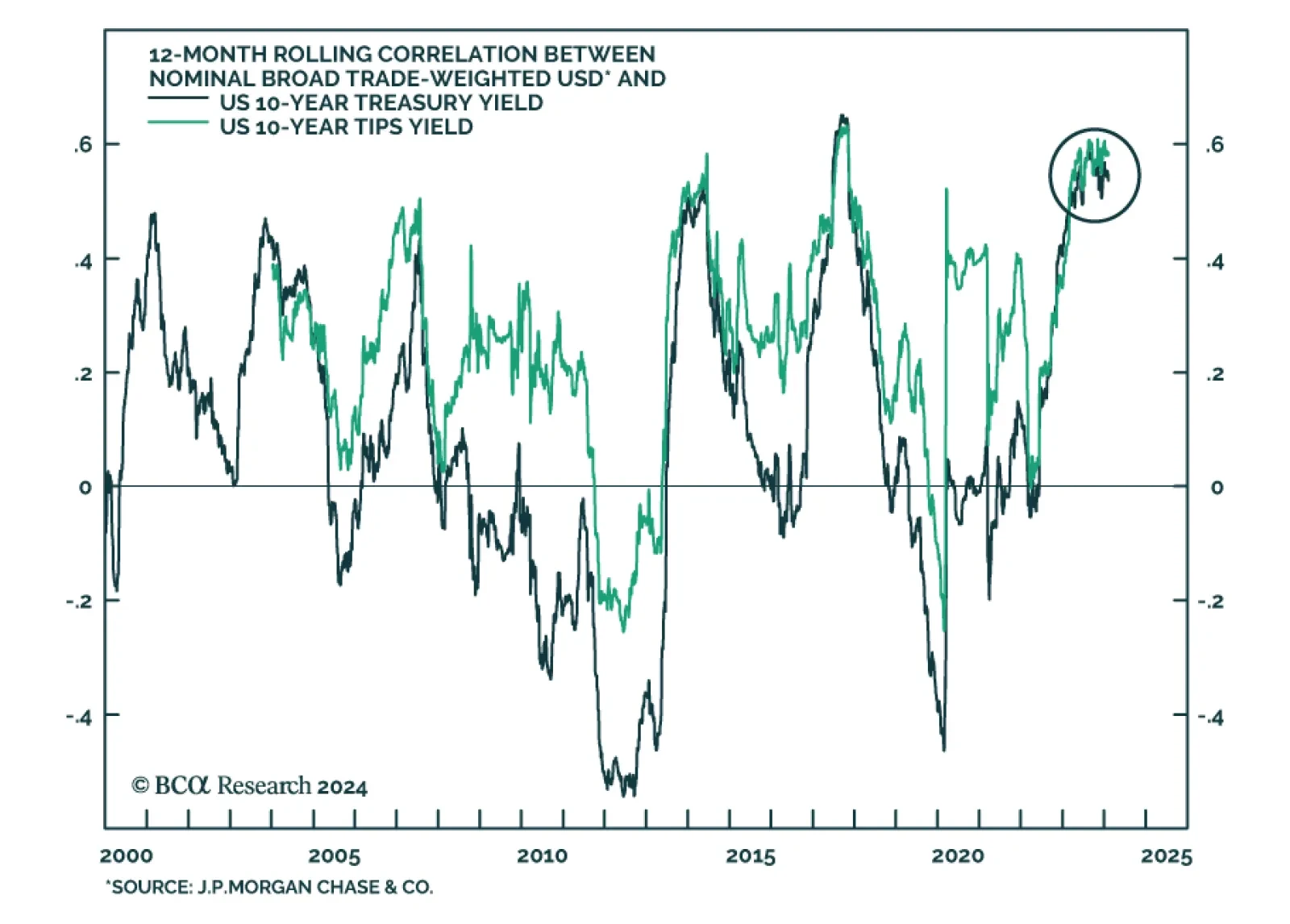

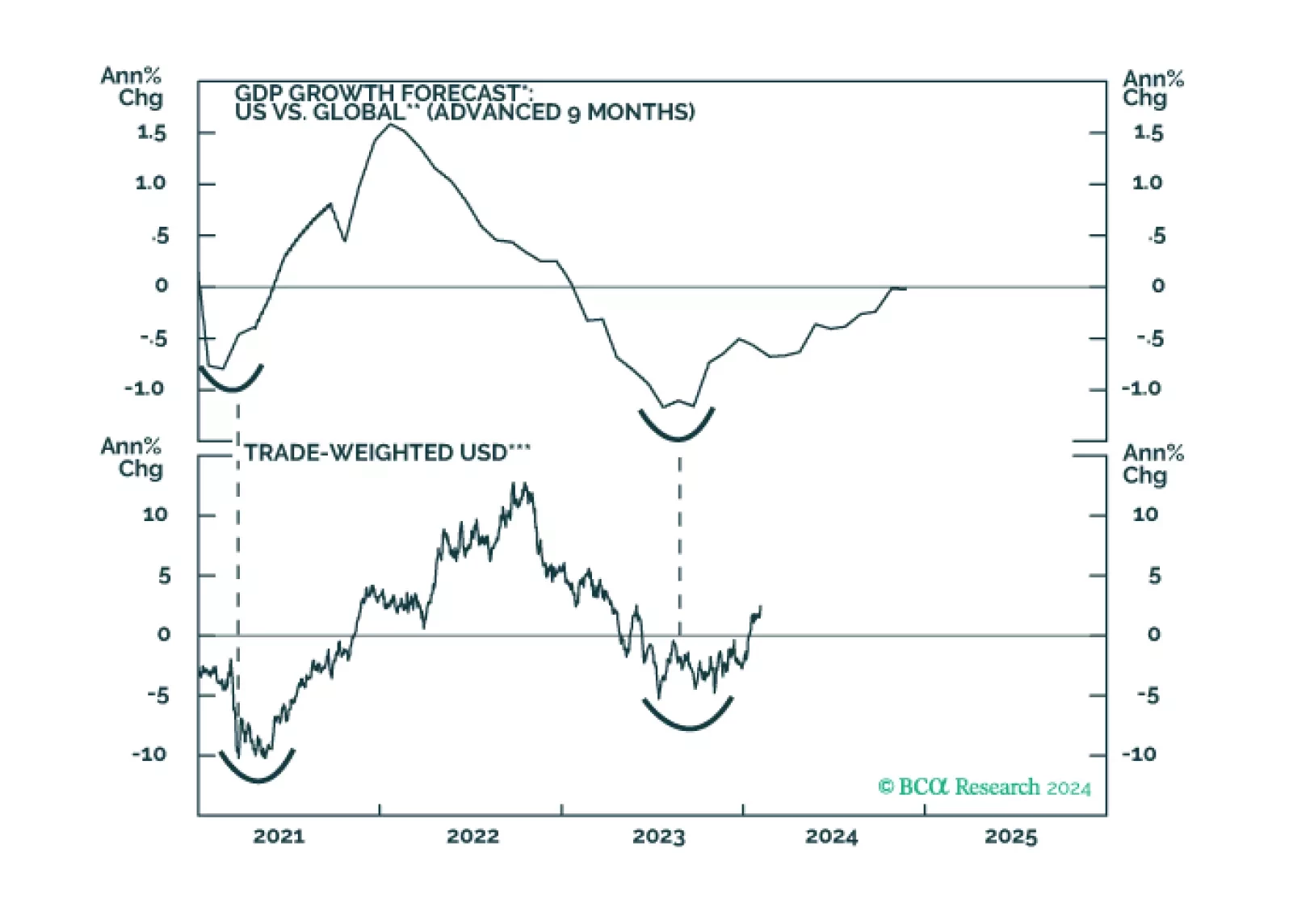

Our Emerging Markets team believes that the risk-reward profile of the US dollar remains very attractive. First, if US growth stays robust, US interest rate expectations will rise because rate cuts priced in will not be realized. Rising interest rates will…

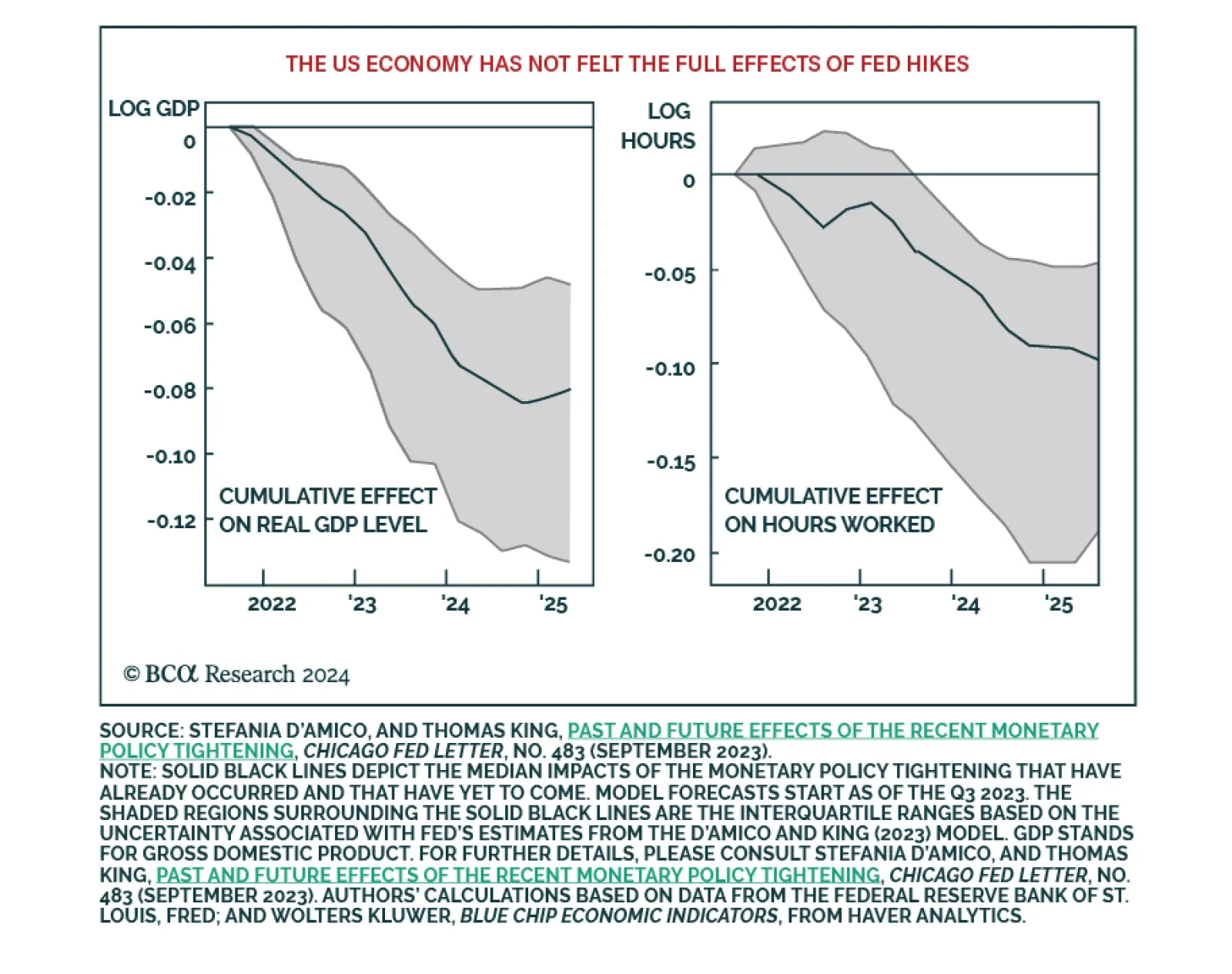

BCA Research’s Global Investment Strategy service’s revised forecast is centered on a recession starting in late 2024 or early 2025. The strong pace of US growth has continued into early 2024. Preliminary estimates from the Atlanta Fed’s GDPNow model…

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.

This week’s report explores factors behind the recent rise in the dollar, and whether this could continue in the next month.

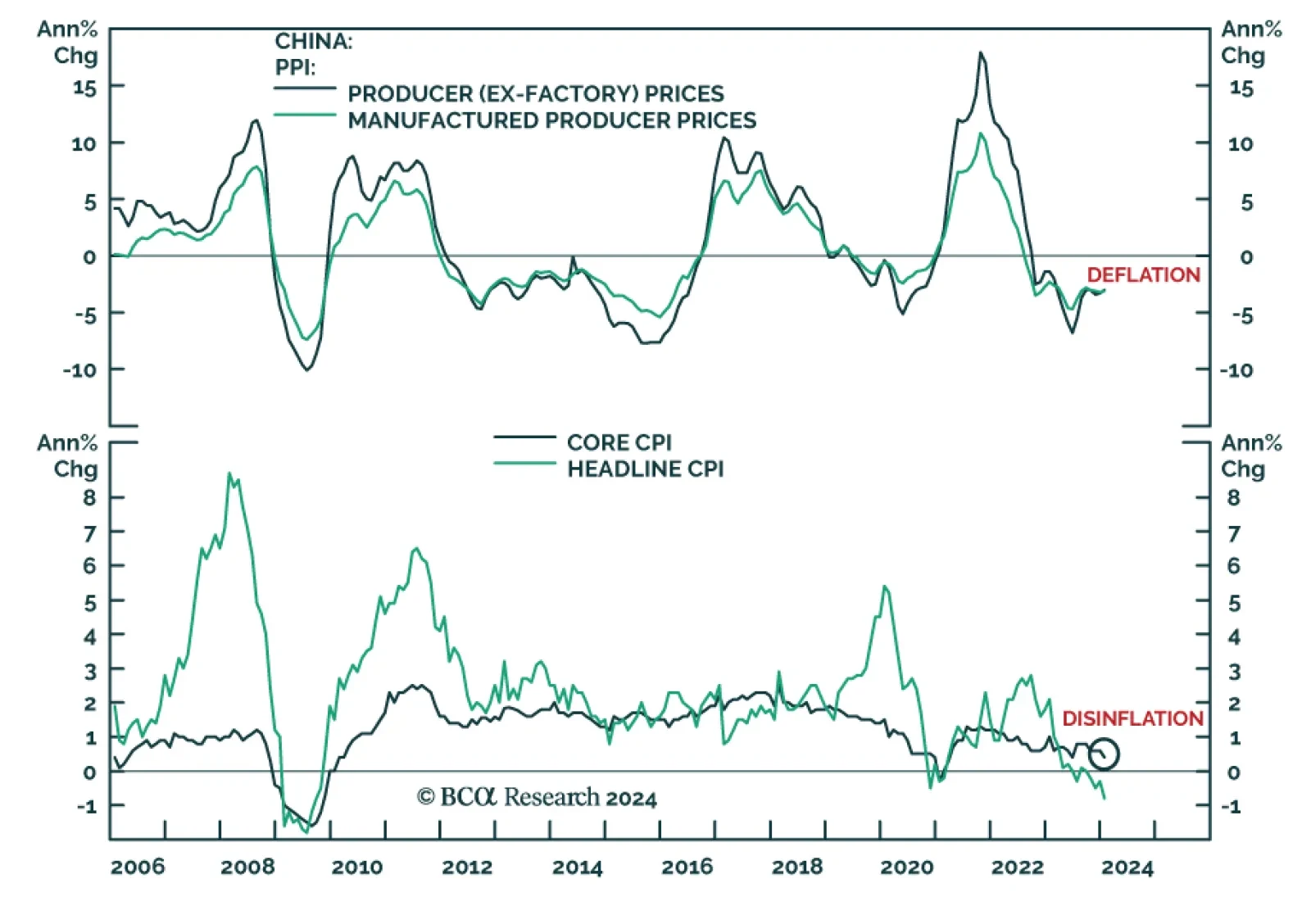

Thursday’s Chinese CPI and PPI release for January indicates that deflationary pressures continue to dominate the domestic economy. On the consumer side, prices registering the fastest pace of annual decline in 15 years. The CPI’s 0.8% y/y decrease is more…

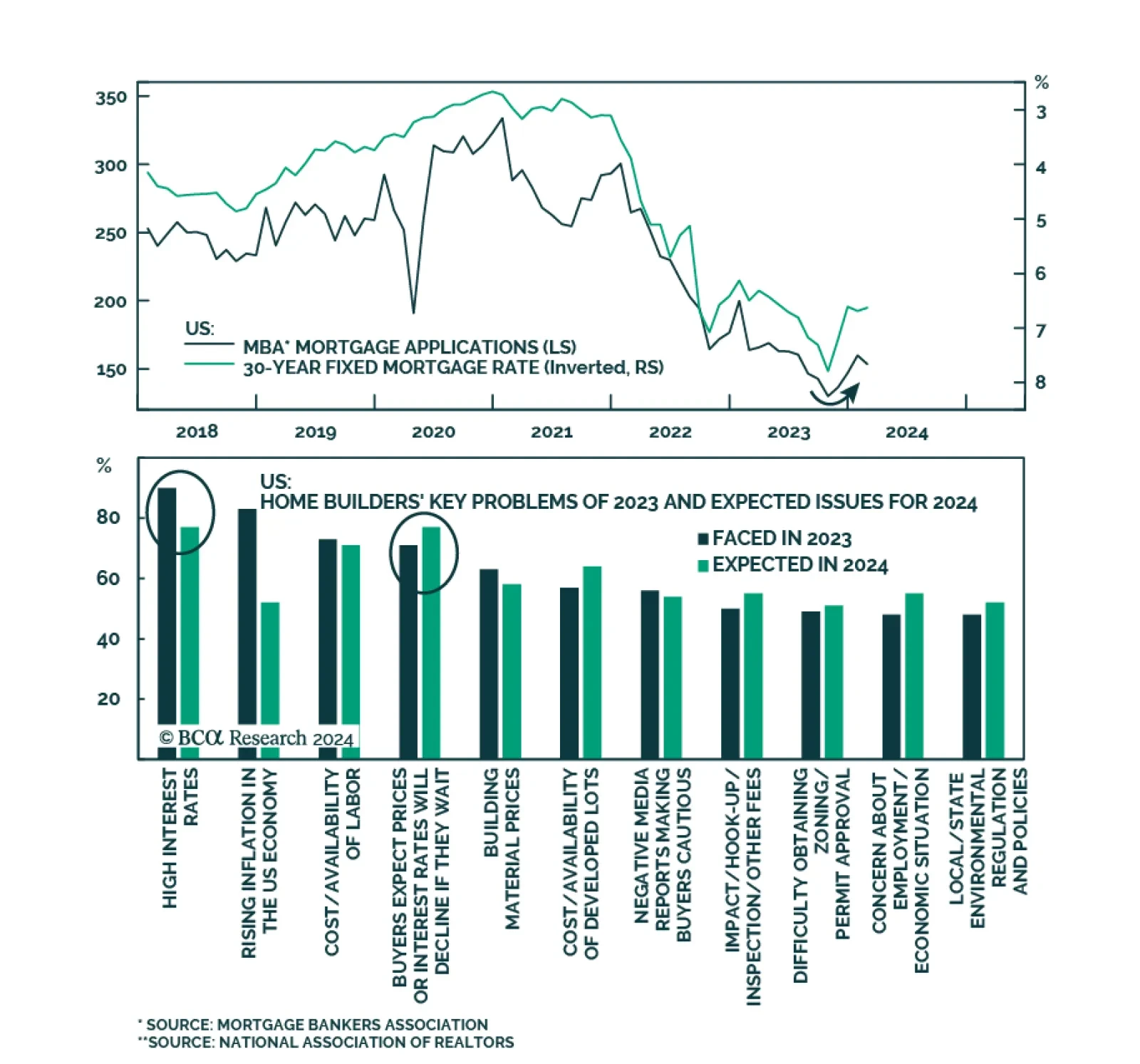

According to the latest MBA weekly survey, mortgage applications increased 3.7% in the week ending February 2. The contents of the report were mixed. A 12.3% jump in the refinance index drove the increase while mortgage applications to purchase a home fell by…

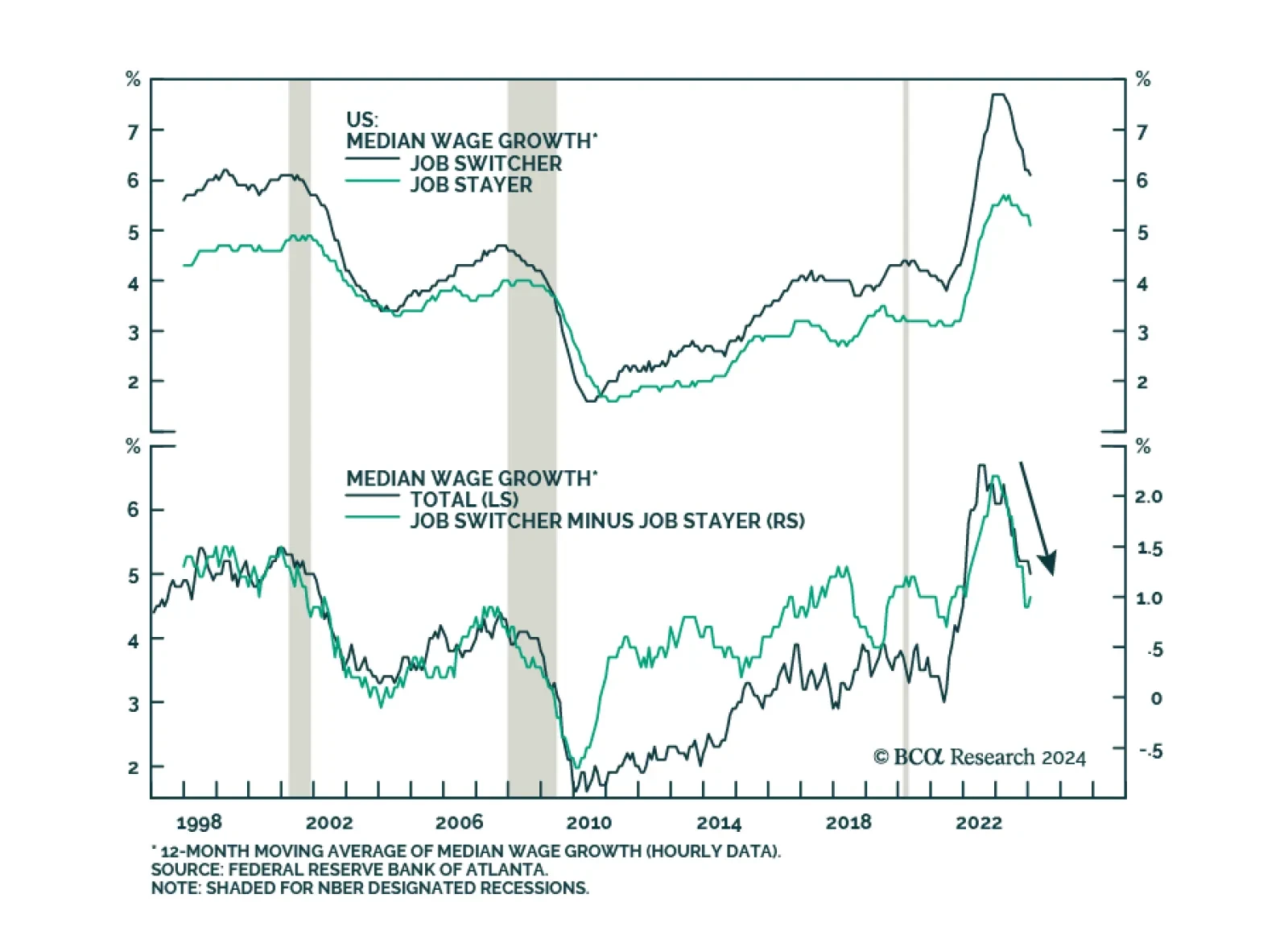

After having surged in the second half of 2021 and early 2022, the Atlanta Fed’s Wage Growth Tracker peaked in mid-2022 and has since been on a general downtrend. The latest reading of 5.0% in January is a continuation of this process, marking the lowest pace…