Policy

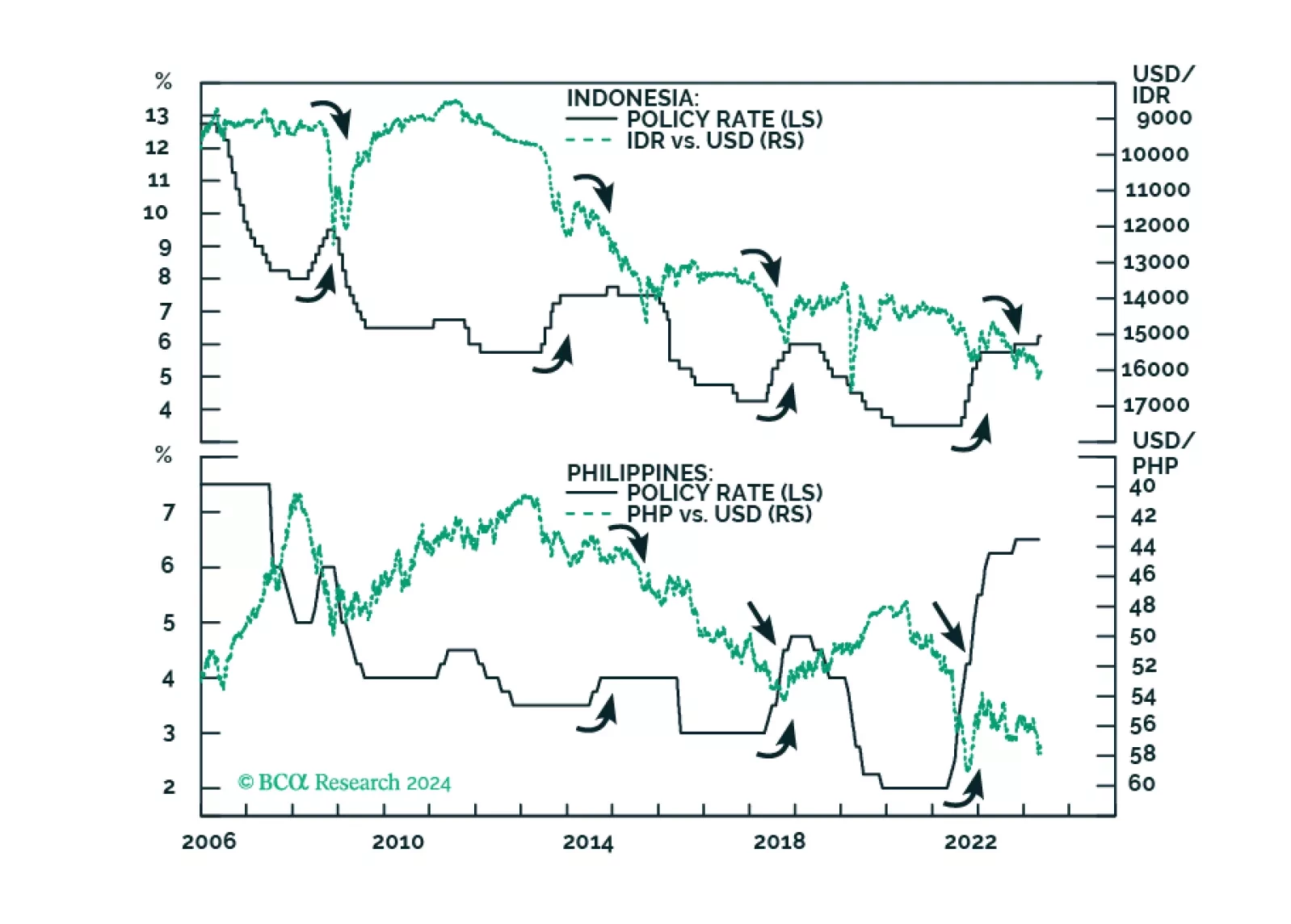

ASEAN stocks and currencies will weaken further as these economies face multiple headwinds. Raising policy rates did not stop a sliding currency in the past, it is unlikely to do so now.

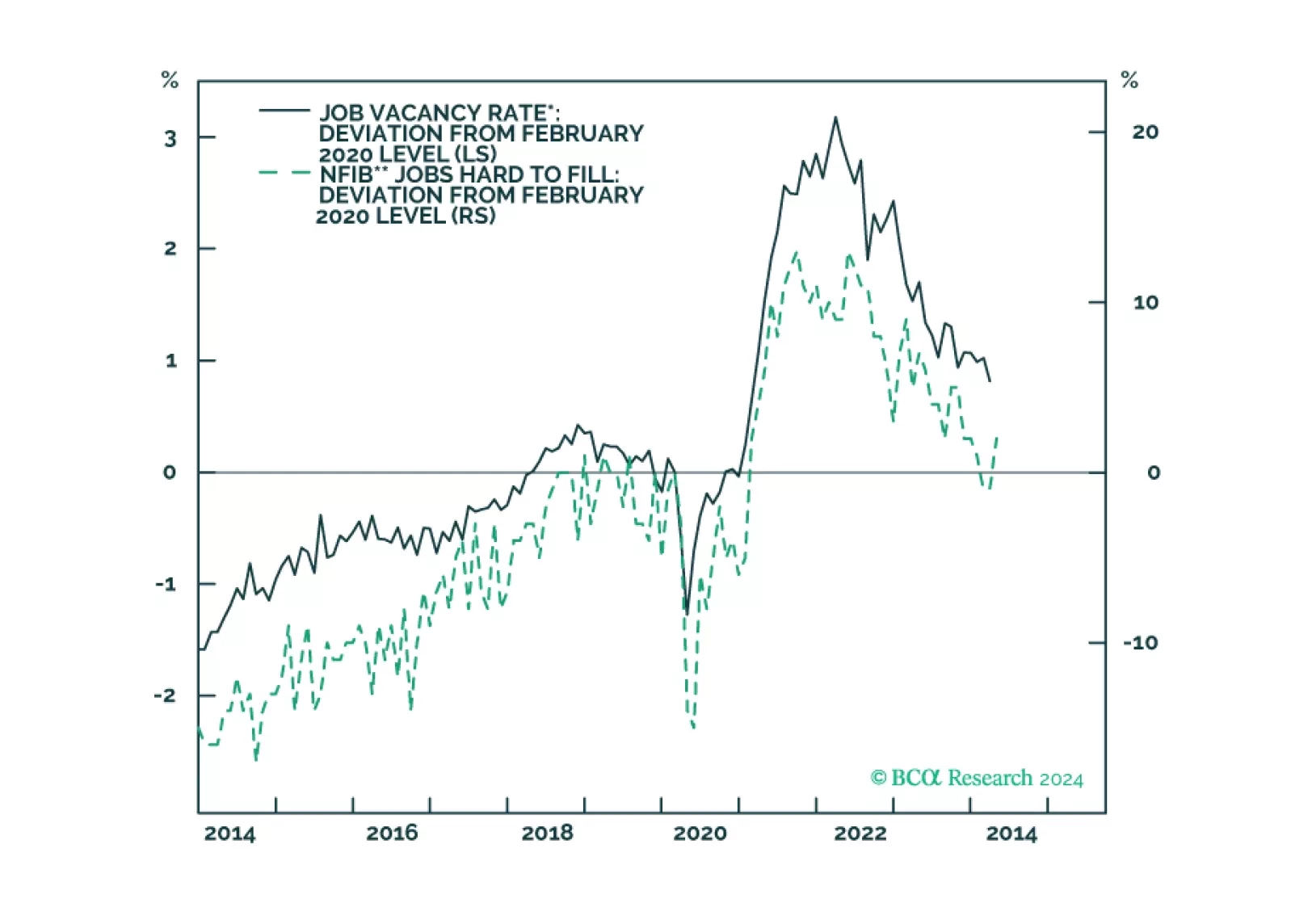

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.

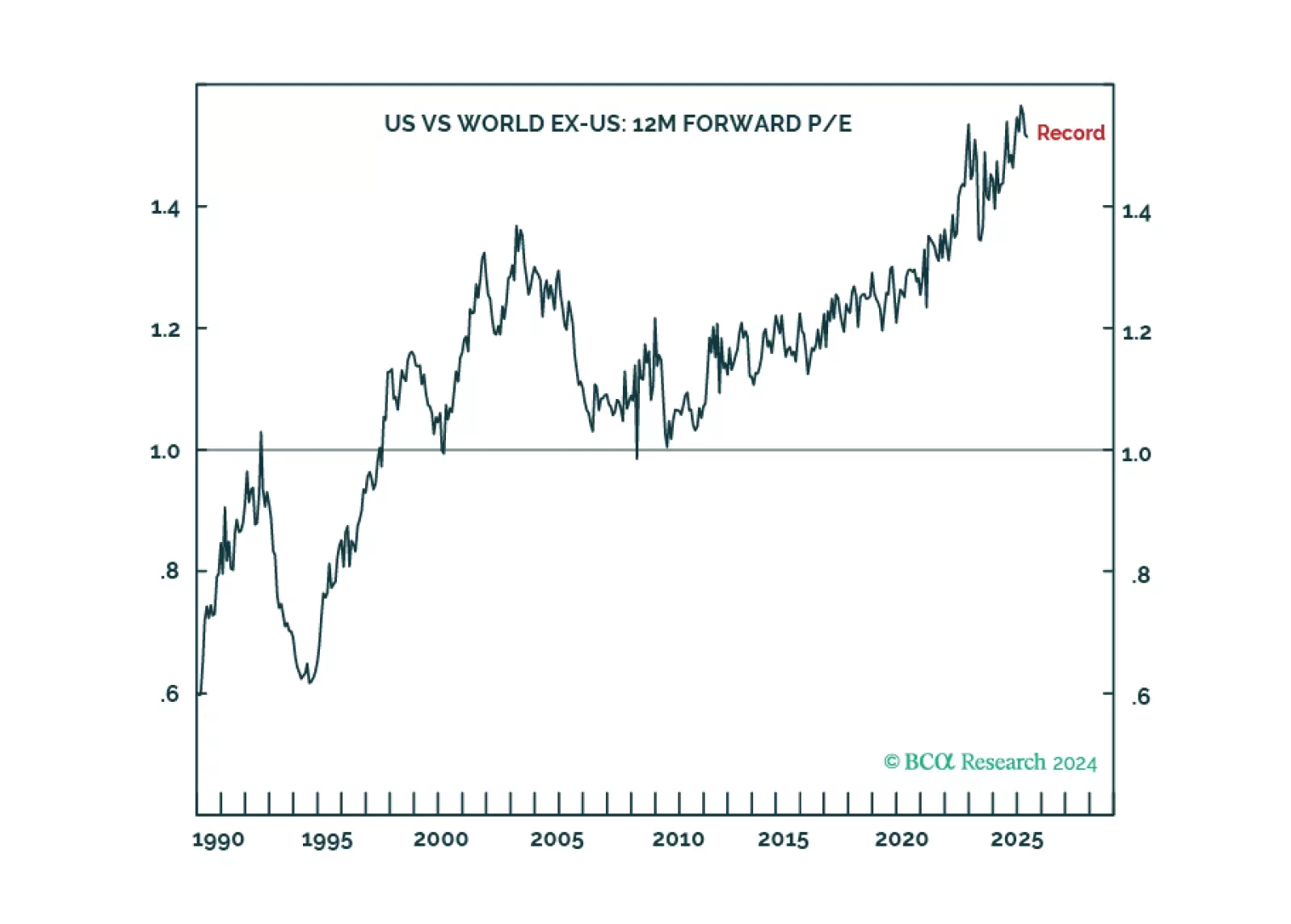

The US stock market’s record 50 percent valuation premium versus the non-US stock market is pricing generative AI to do through the next decade what the Web 2.0 network effect did through the last decade. But this is a huge ask, as it will be very difficult for the Web 2.0 superstar companies to become generative AI superstar companies, assuming there are indeed any lasting generative AI superstar companies. We go through the main long-term investment implications.

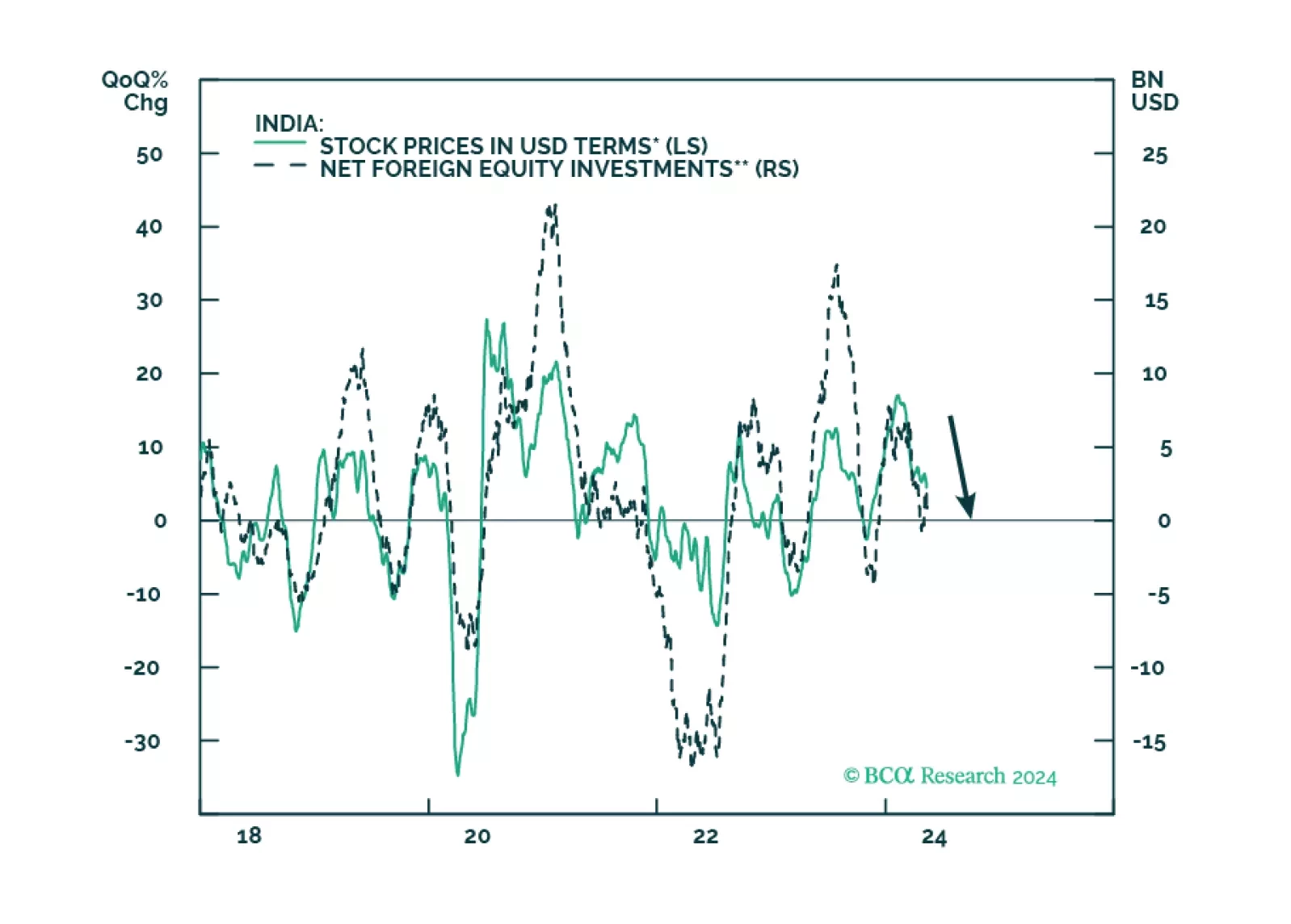

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.