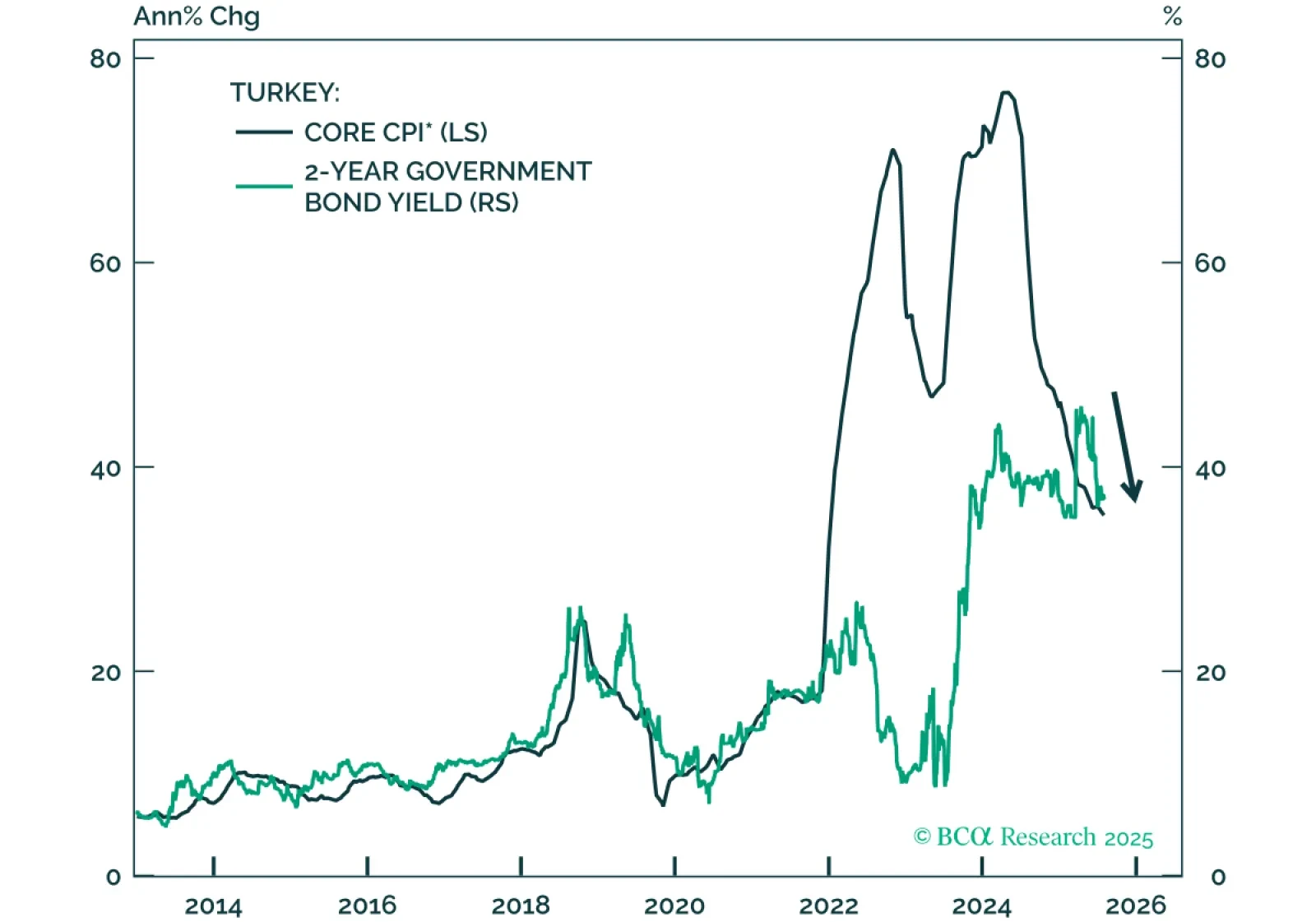

Turkey’s financial policymakers have pursued a disciplined and restrictive policy mix so far, delivering high real interest rates and curbing fiscal expansion even as the economy slows. This commitment to inflation control has paved the way for a pronounced decline in price pressures, prompting BCA’s Emerging Markets Strategy team to upgrade Turkish domestic bonds to overweight in its EM domestic bond portfolio. Similarly, Moody’s has recently upgraded Turkey’s credit rating and outlook. The lagged effects of the restrictive stance are now increasingly evident: real bank lending rates hover near 30%, real domestic demand growth is decelerating, and fiscal expenditure increases are barely keeping pace with inflation. Collectively, these conditions point to further disinflation and declining bond yields in the coming quarters (Chart 1).From an FX strategy perspective, the Turkish lira (TRY) presents a less precarious profile than many fear and what the forward markets currently imply.First, the current account deficit has narrowed considerably in recent years. As tight policy weighs on domestic demand, it will further curb goods imports and keep the current account deficit in check (Chart 2). This improvement should offset much of the expected export contraction due to slowing demand from the European manufacturing sector, reducing pressures on the lira from external balances. Second, the combination of receding inflation and very high nominal yields creates a compelling environment to attract sizable foreign portfolio flows into local currency debt. With foreign ownership of Turkish domestic government bonds currently low by historical standards, there’s significant room for new inflows (Chart 3). As such, the TRY depreciation over the next year will likely fall well short of the 26% pace currently implied by forward markets vis-à-vis the USD. Historically, periods of falling inflation have coincided with slower lira depreciation (Chart 4). A weaker trade-weighted US dollar could reinforce this trend, further curbing pressure on the currency. In this context, short-end local currency bonds are becoming increasingly attractive to global investors.Bottom Line: Falling inflation and a narrow current account deficit in Turkey have historically gone hand-in-hand with a less vulnerable currency. This time should be no different: the pace of the lira’s depreciation against the US dollar will likely ease in the coming months.