Policy

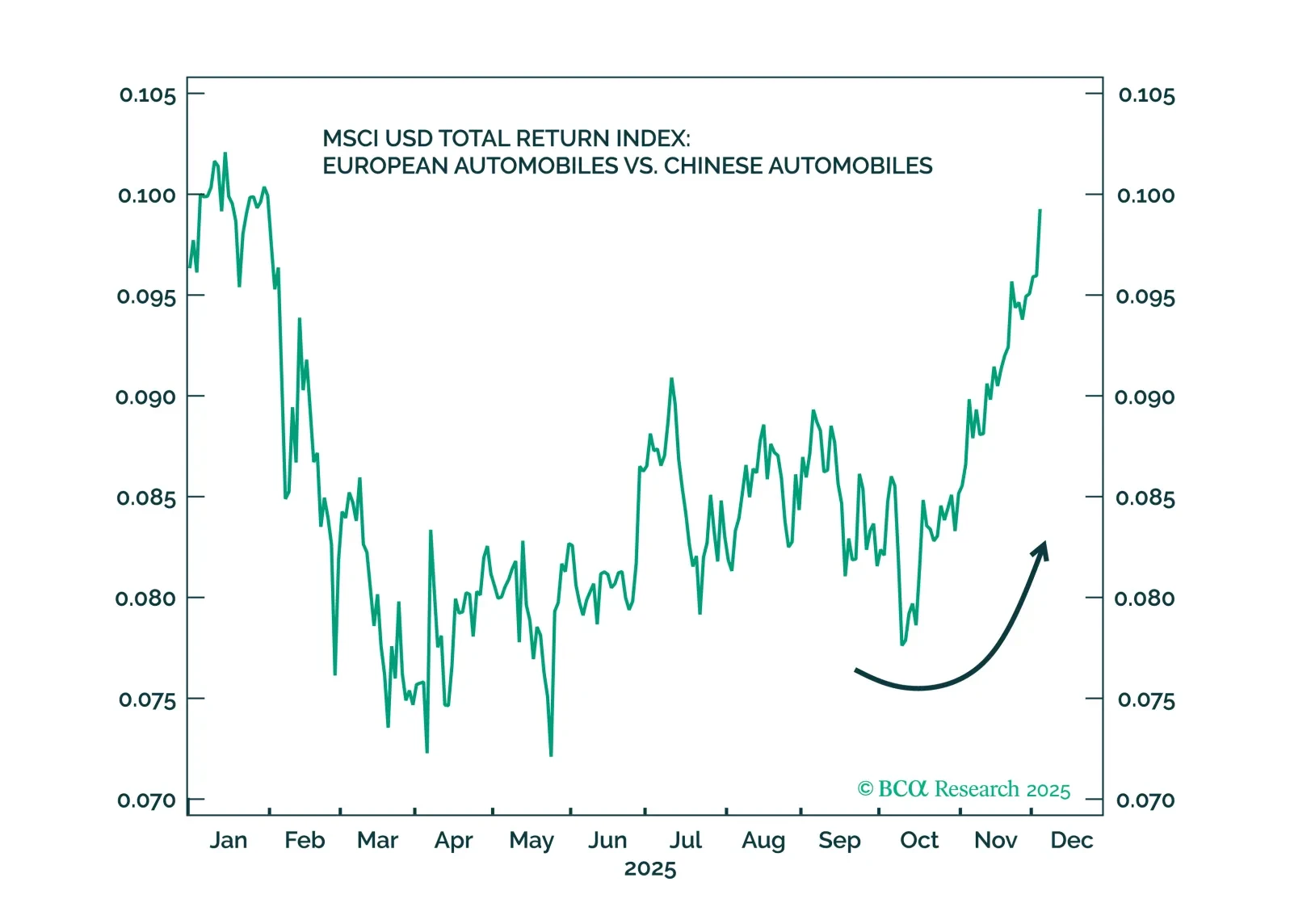

We got Trump's tariff shock and backtracking correct and predicted Israel's attack on Iran. But we missed the China rally — and there is still no Ukraine ceasefire.

Our Portfolio Allocation Summary for December 2025.

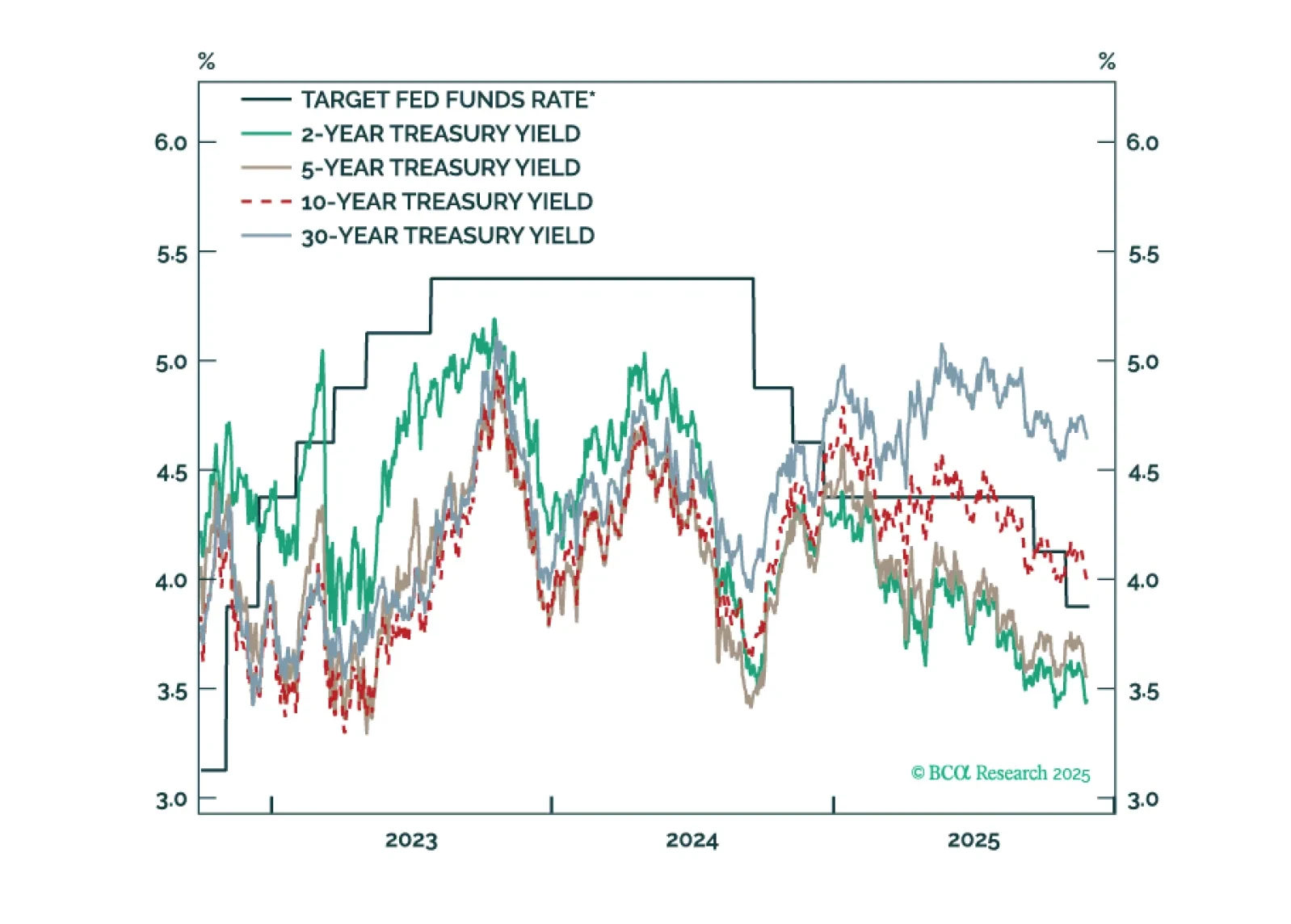

Our key US fixed income views for 2026.

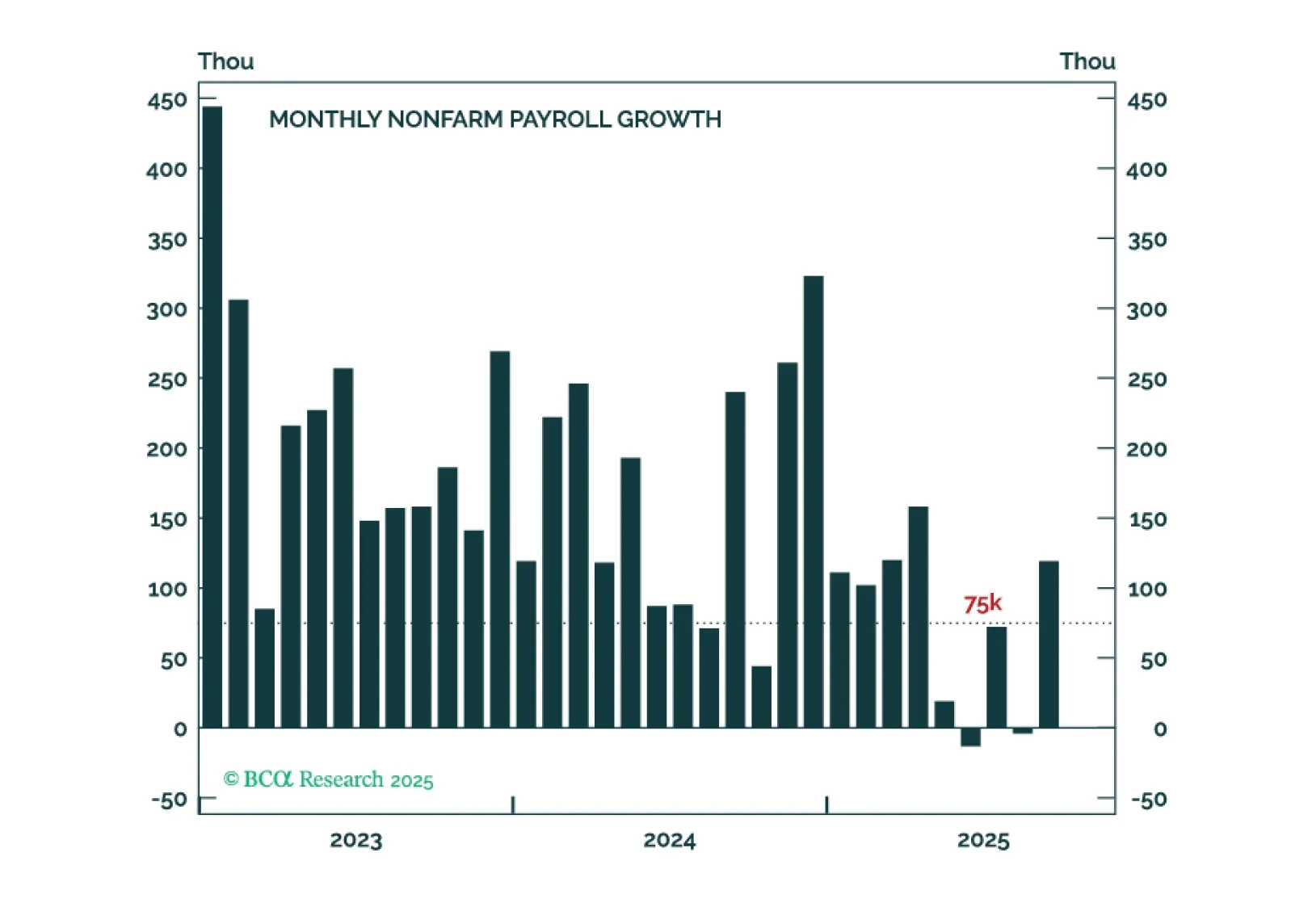

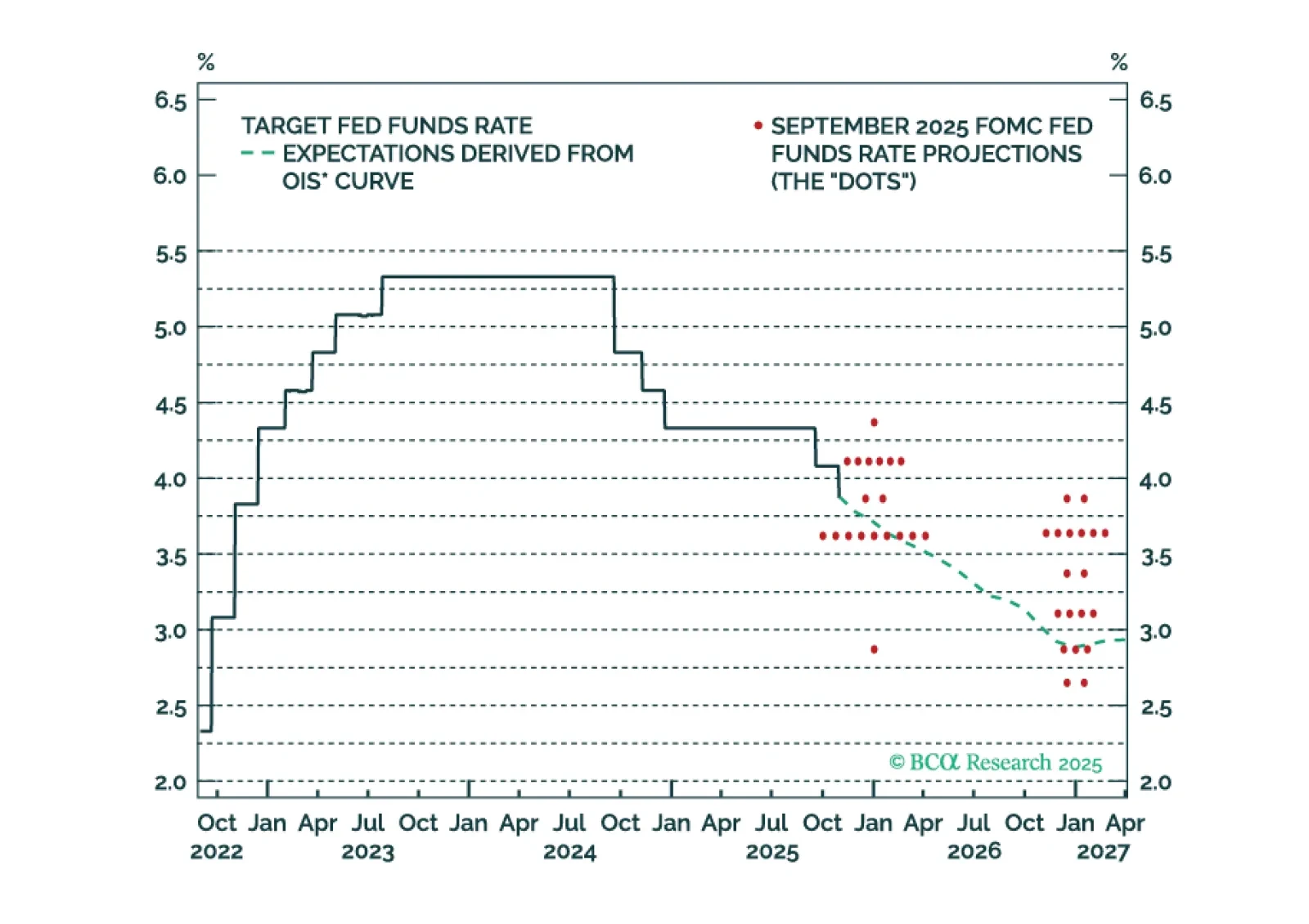

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

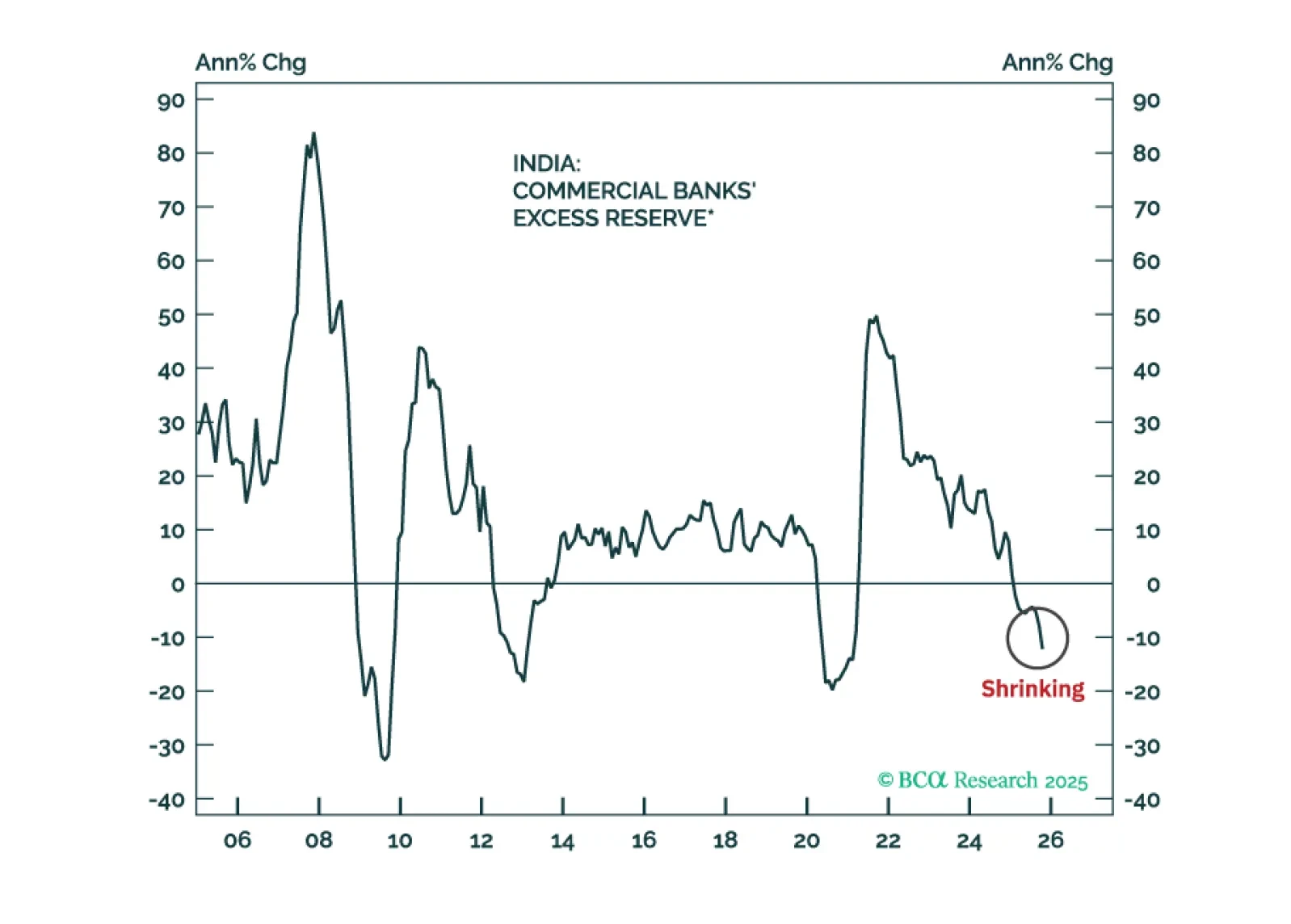

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

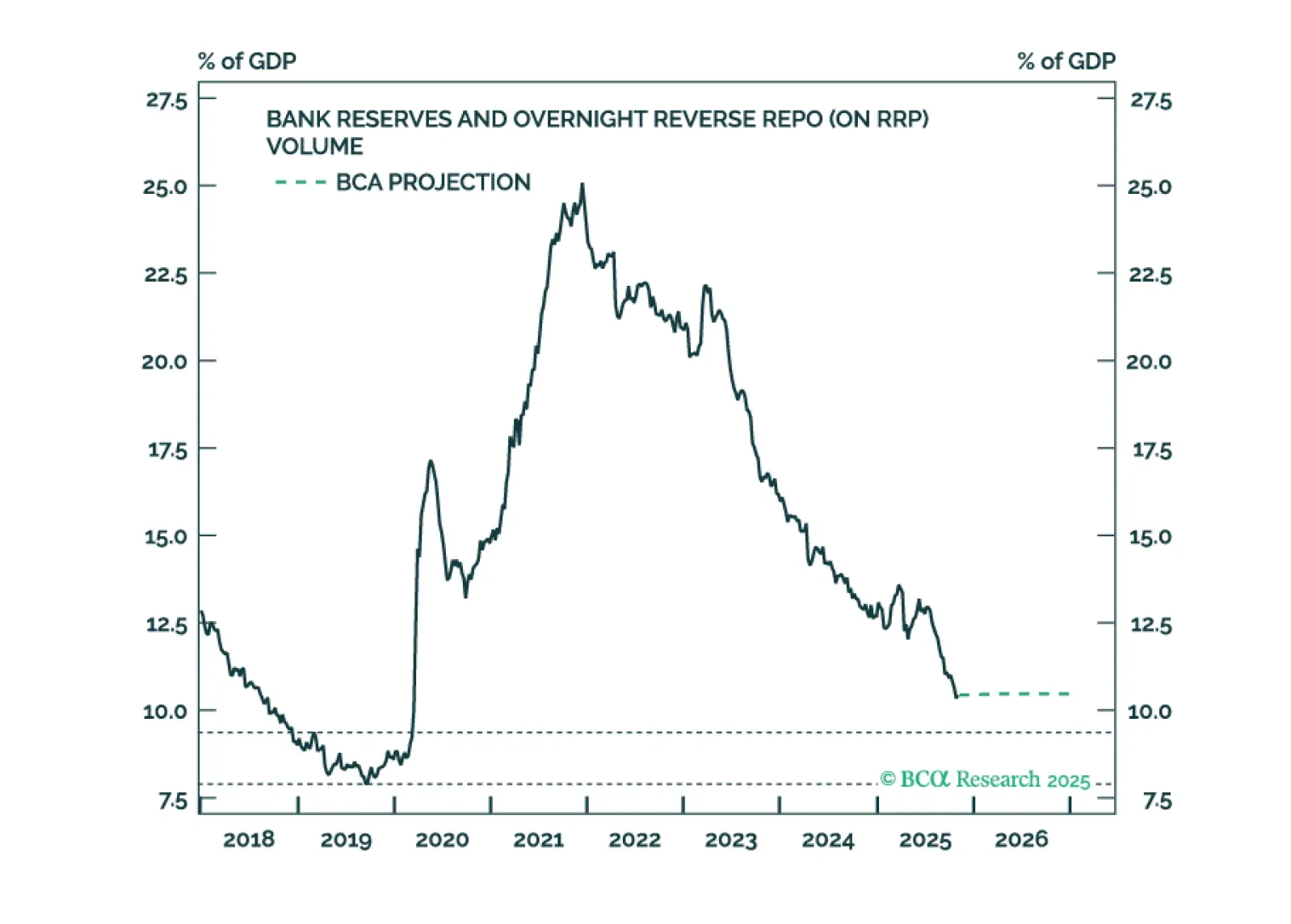

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

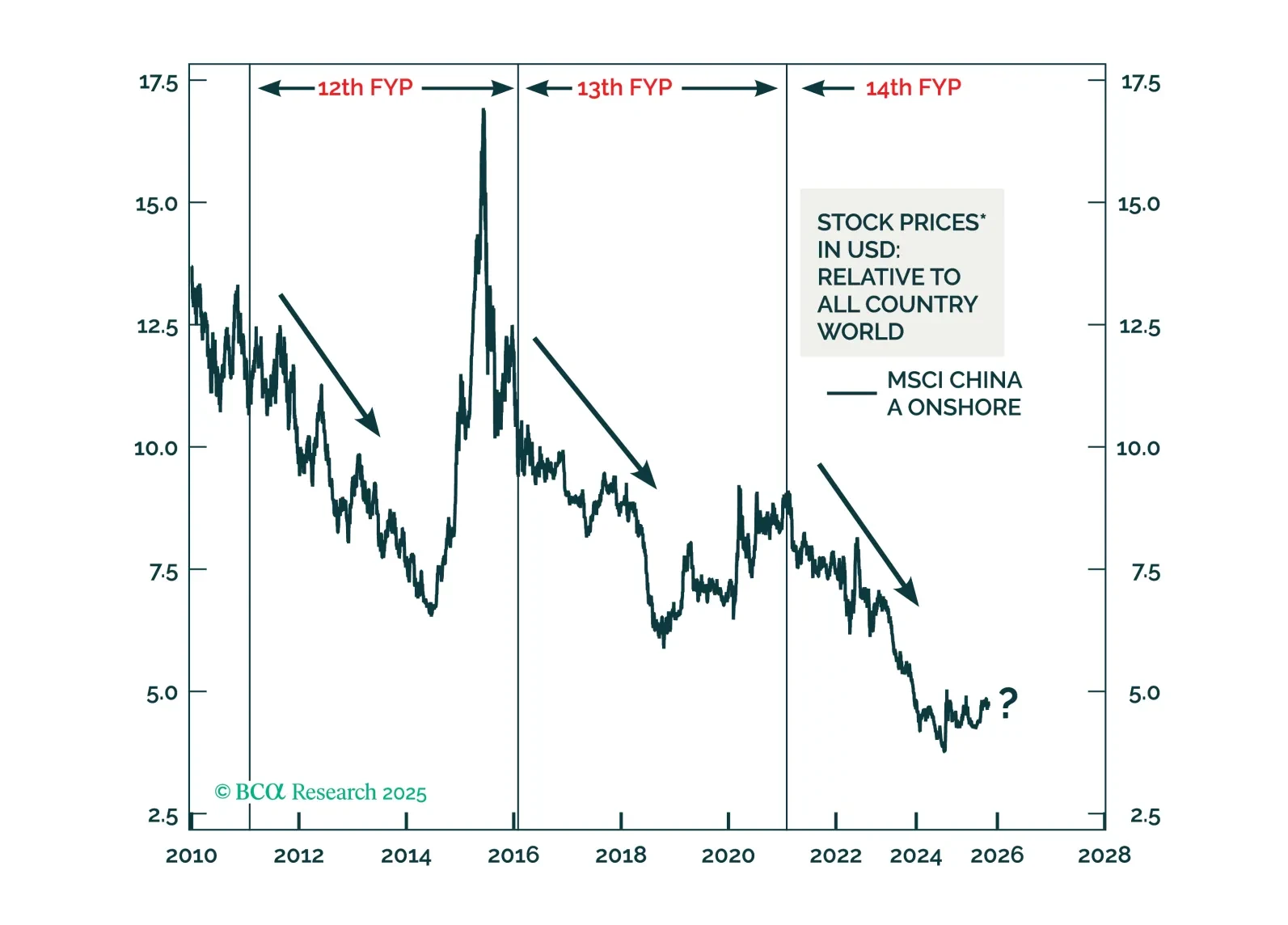

By tracing patterns across China’s past three Five-Year Plans, we reveal how policy cycles shape markets—and what investors should expect in the next five years.

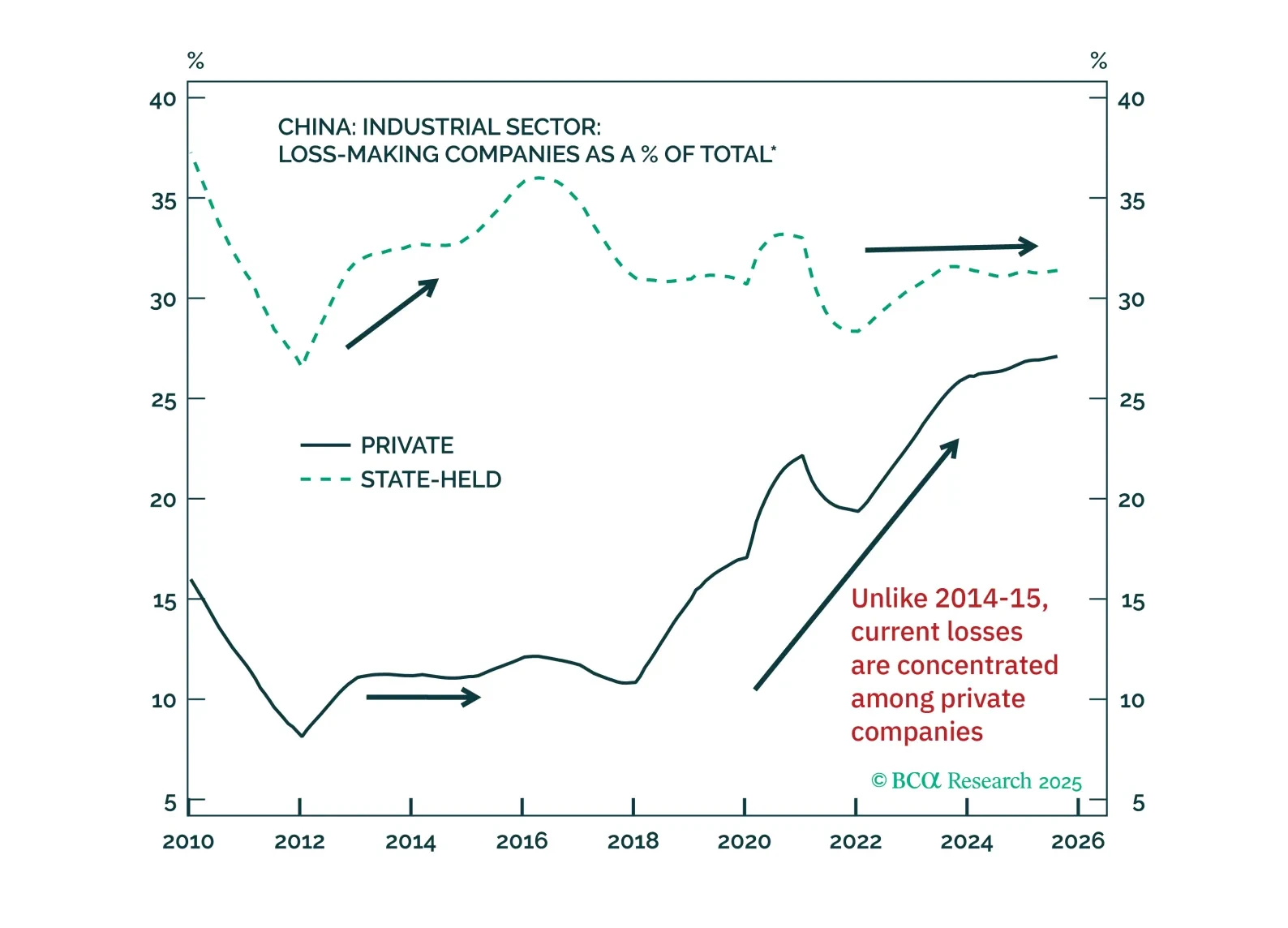

China's anti-involution policies will not end deflation or boost corporate profits on a sustainable basis. Authorities will be reluctant to cut industrial capacity as doing so would lead to layoffs. Consequently, production will continue to exceed demand, and price deflation will persist.

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

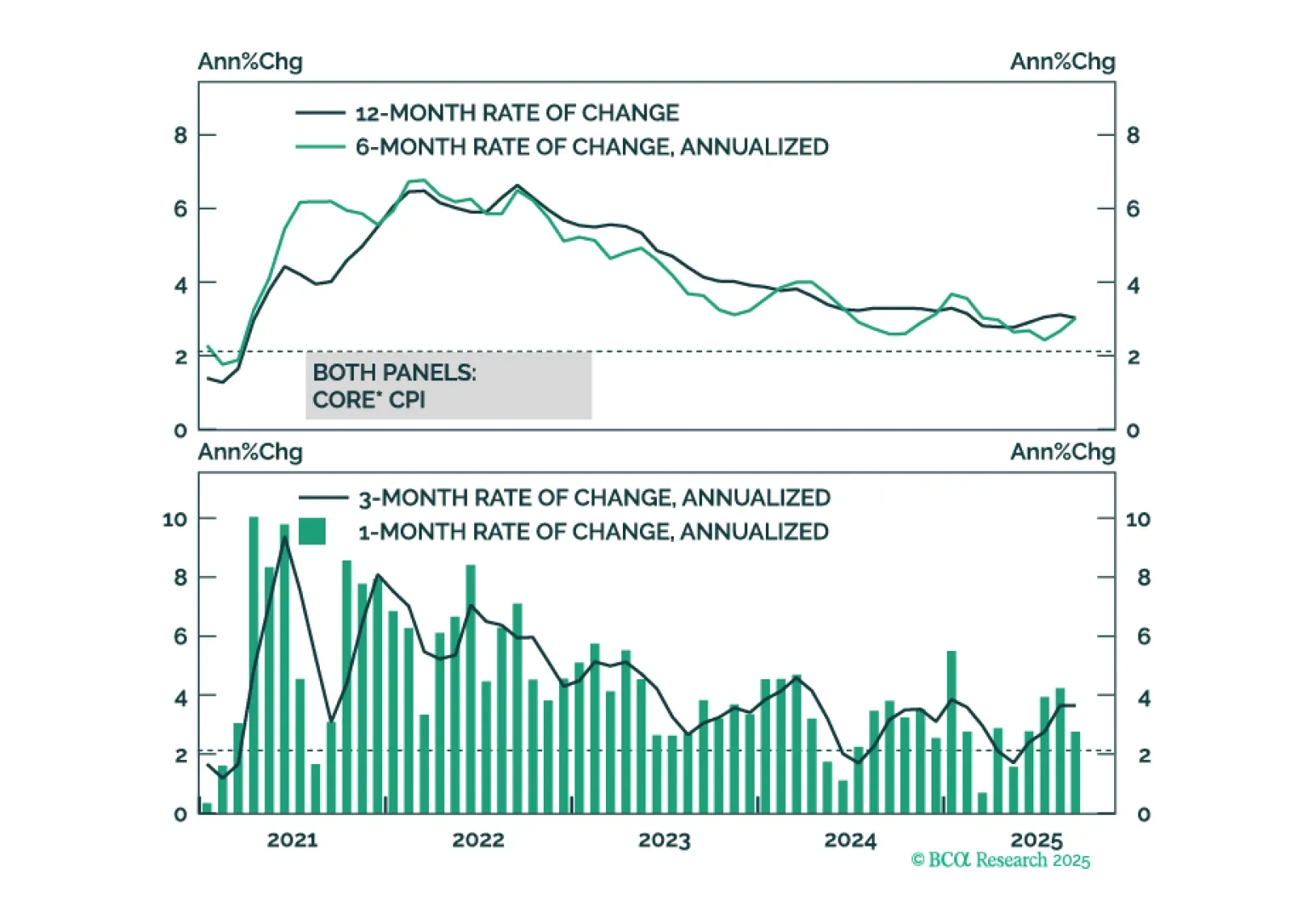

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.