Policy

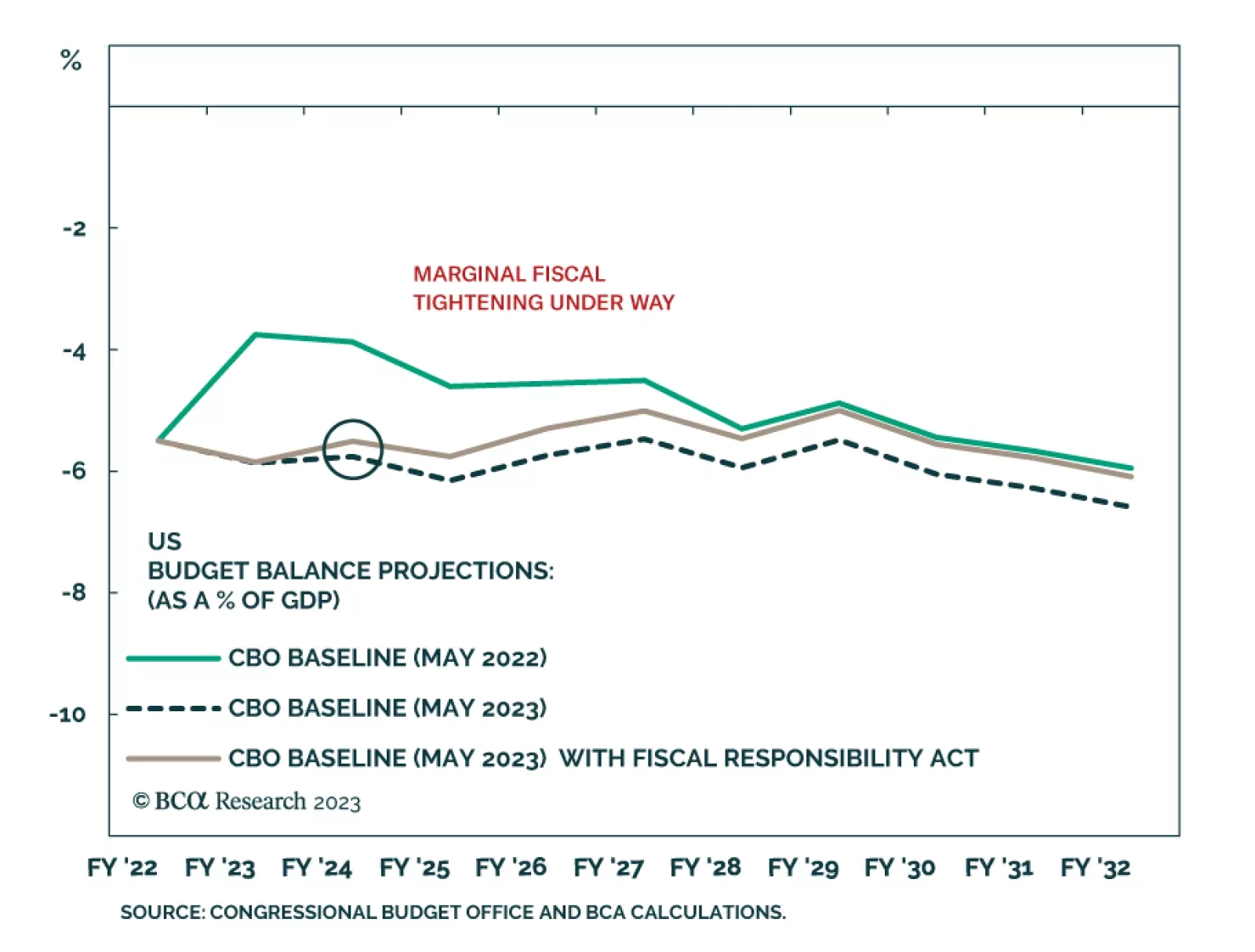

According to BCA Research’s US Political Strategy service, US fiscal policy is marginally negative for the economy and marginally increases the odds of recession in 2023-24. It is not a positive catalyst for equities in the third quarter. Fiscal policy is…

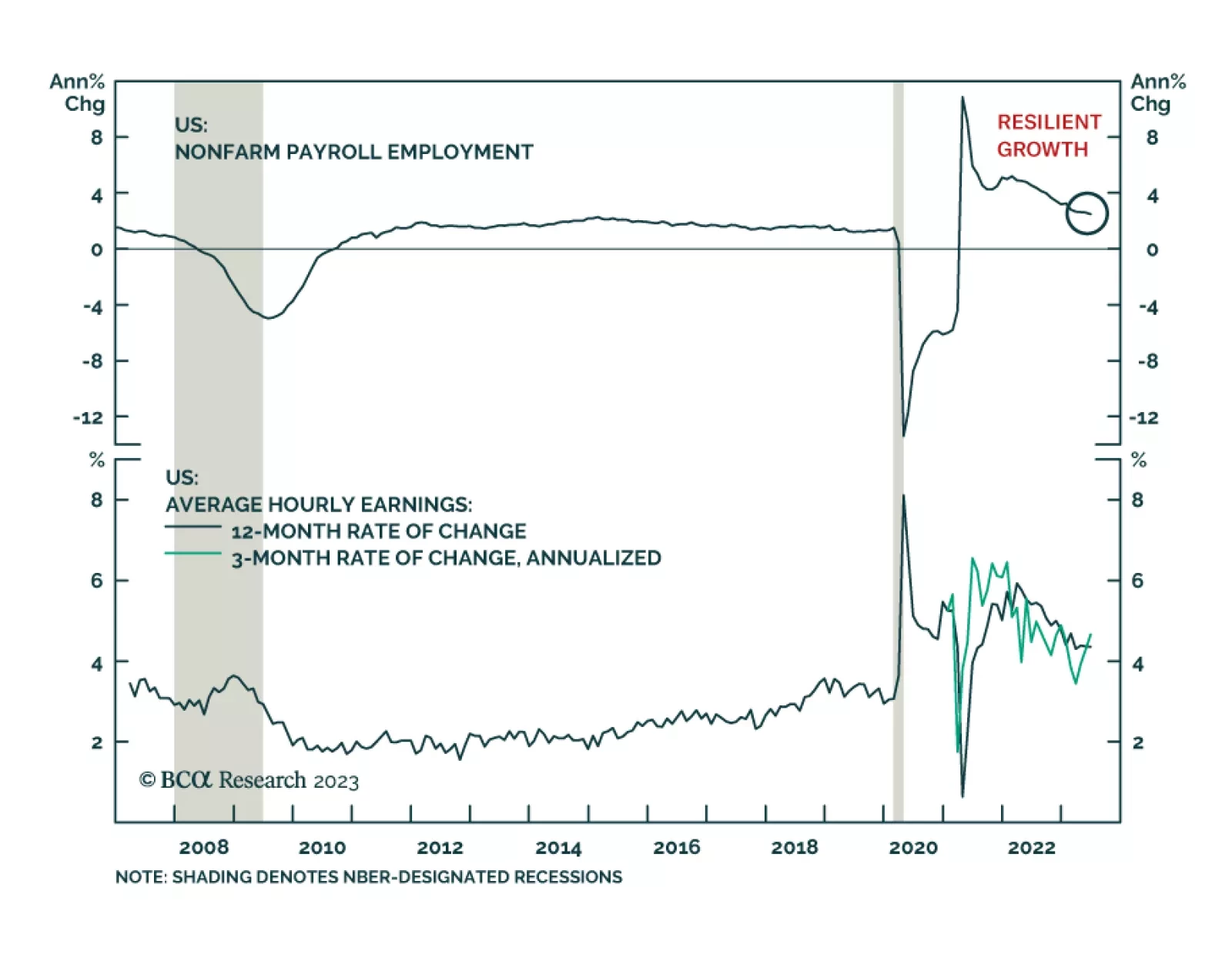

Last week’s labor market data signal that US employment conditions remain strong – solidifying the case for a 25 bps rate hike at the Fed’s next meeting later this month (see The Numbers). Yet in order for the Fed to continue tightening beyond July,…

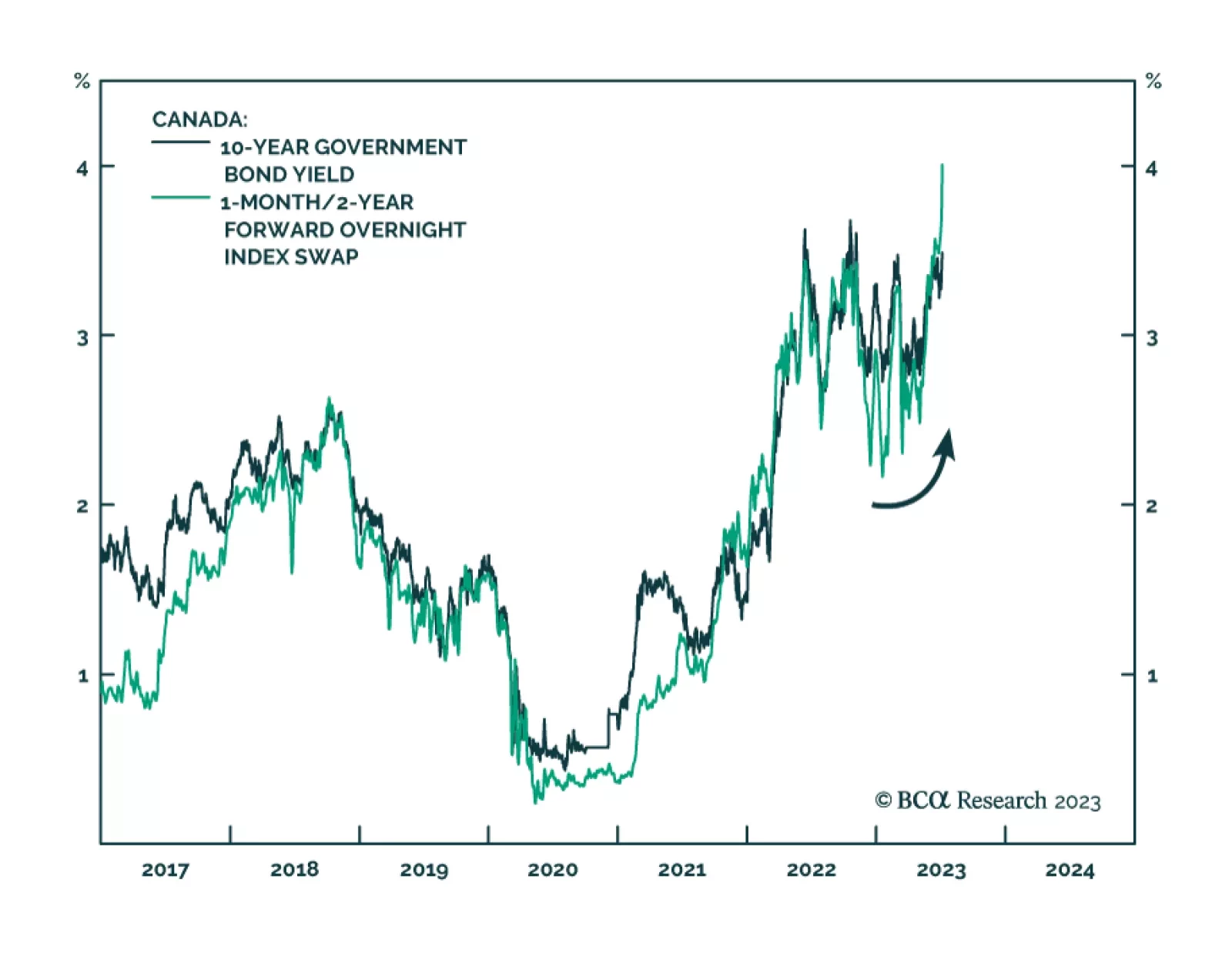

Canadian hiring surprised to the upside in June. The 60 thousand increase in employment last month – the highest since January – came in triple expectations of a 20 thousand rise and follows a 17 thousand decline in May. The increase mainly reflects a sharp…

On the surface, the lower-than-anticipated job gains suggest that US labor market conditions softened last month. Friday’s jobs report revealed that the increase in nonfarm payrolls slowed from a downwardly revised 306 thousand to 209 thousand in June – below…

Positive economic surprises have delayed the onset of recession in the United States. But tighter monetary and fiscal policy, slowing global growth, and a looming rebound in policy uncertainty and geopolitical risk suggest that investors should buy insurance while it is cheap.

A perspective on the recent increase in US bond yields and this morning’s employment report.

In this short weekly report, we review some of the most common questions clients asked us in the last few weeks.

Global stocks fell and sovereign bond yields surged on Thursday following the release of stronger-than-anticipated US labor market data. Data released by Challenger, Gray, & Christmas showed job cuts declined to 40,709 last month from 80,089 in May.…

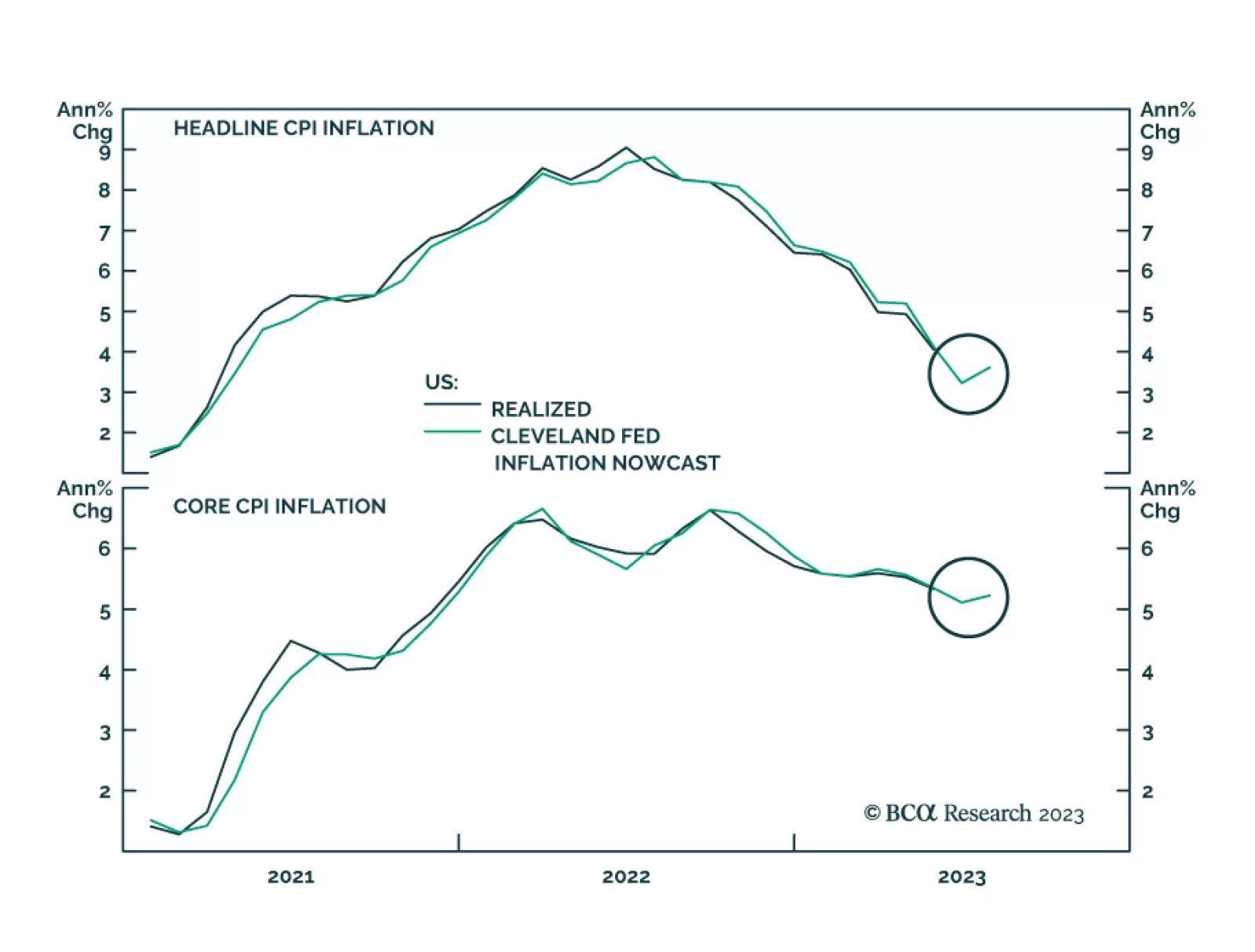

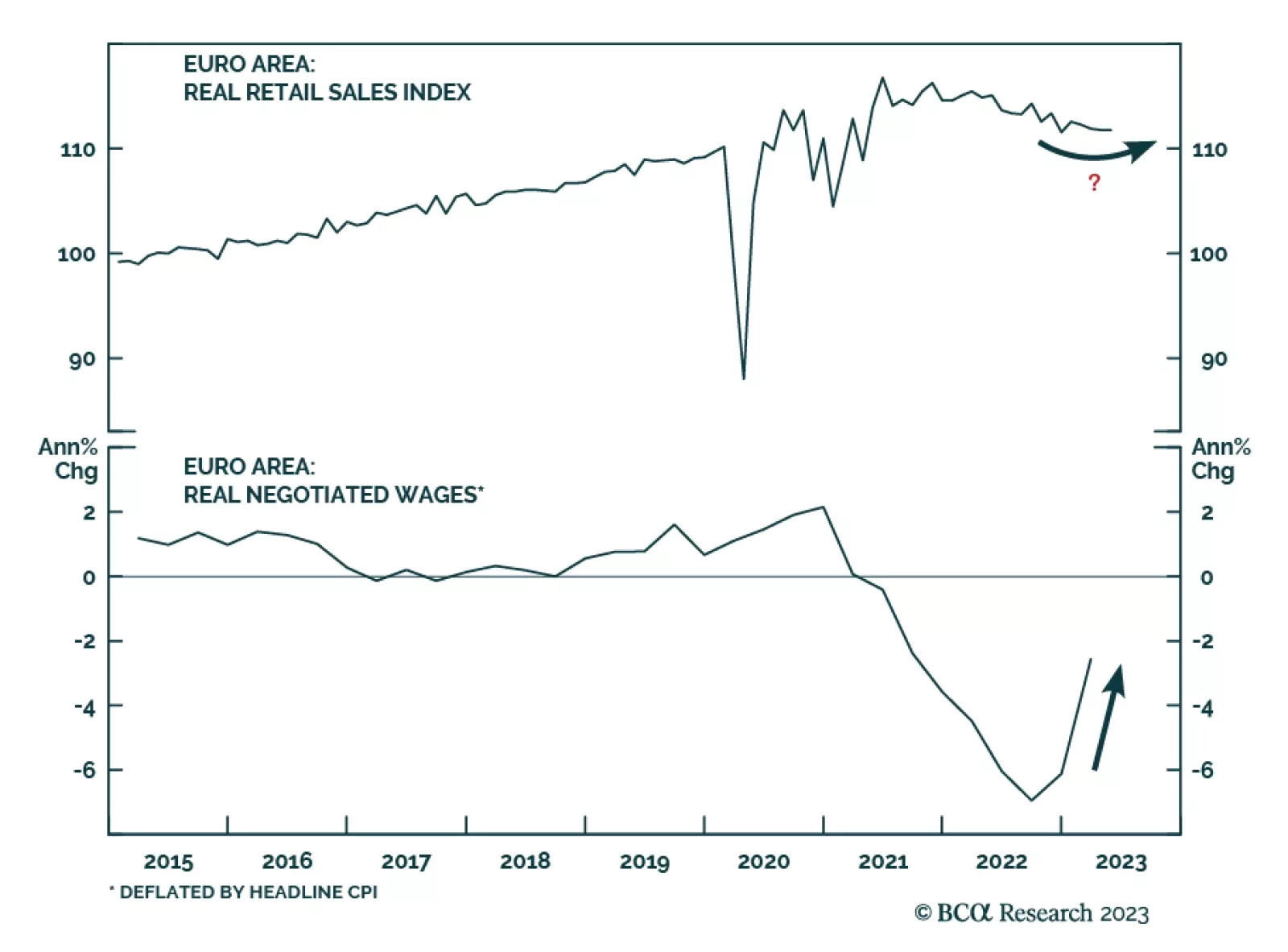

Yesterday we highlighted that falling producer prices foreshadow lower CPI inflation in the Eurozone and argued that this dynamic is positive for the bloc’s consumption outlook. Easing price pressures will ultimately lift real wages, reducing the drag on…

On one hand, China will be exporting deflation to the rest of the world. On the other hand, core inflation is sticky in the US, making the Fed err on the hawkish side. Altogether, these crosscurrents are creating a toxic mix for risk asset prices.