Policy

A brief recap of the July FOMC meeting and its investment implications.

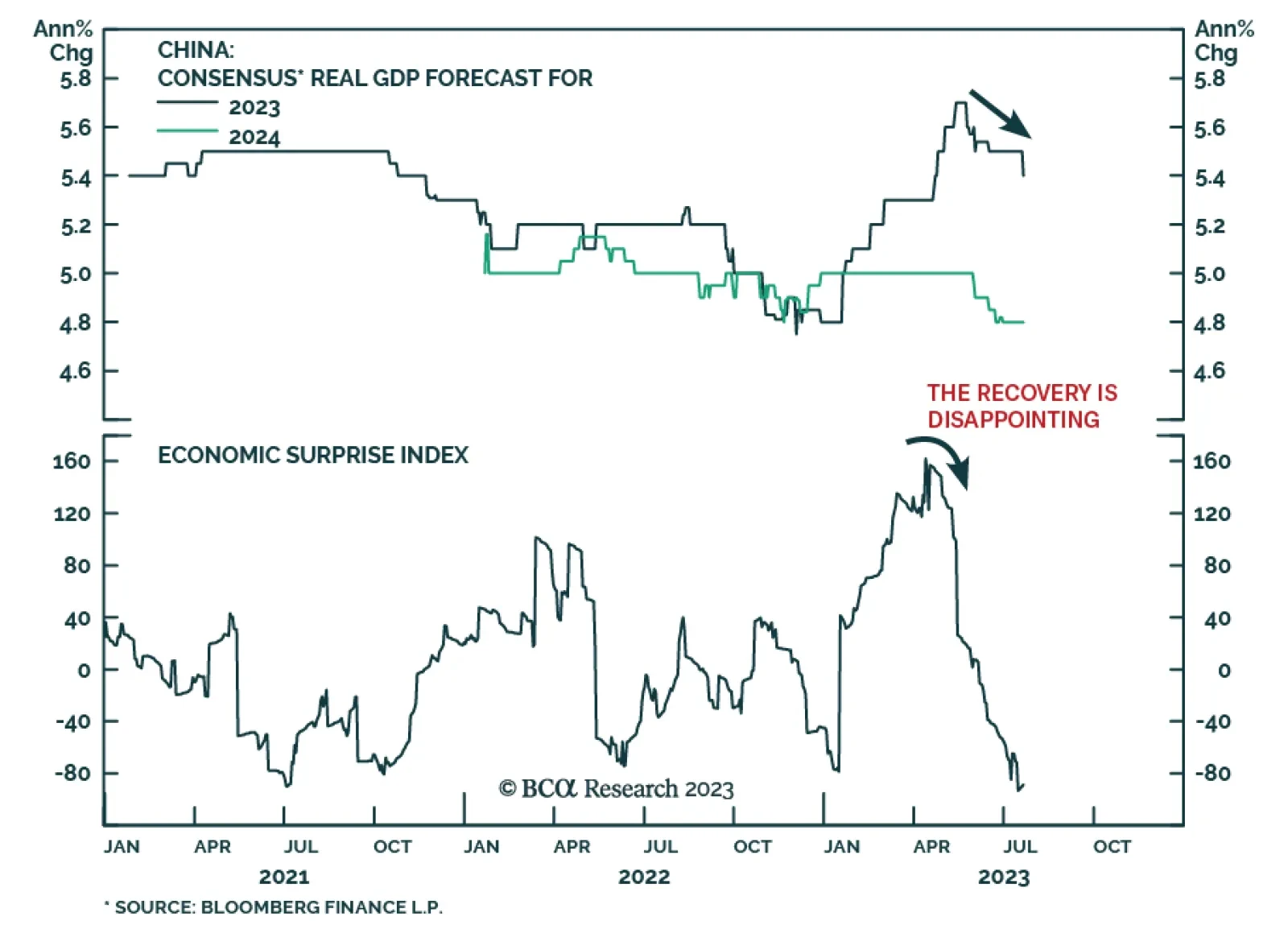

Stay cautious on Chinese stocks. Equity investors should use any rebound in onshore stock prices to downgrade A-shares from overweight to neutral within global and EM equity portfolios. Remain underweight Chinese investable/offshore stocks. Onshore bond yields will drop to all-time lows. Continue receiving 10-year swap rates. The currency will continue depreciating versus the US dollar in the coming months.

The snap election which took place on Sunday resulted in a political deadlock in Spain. No single party has won enough seats to form a government. More importantly, both the left-wing bloc and the right-bloc fell short of the 176-seat majority needed in the 350-seat lower house. Negotiations are taking place as we publish, but neither side can see a clear and straightforward path to form a working government. Spain is heading into a political deadlock.

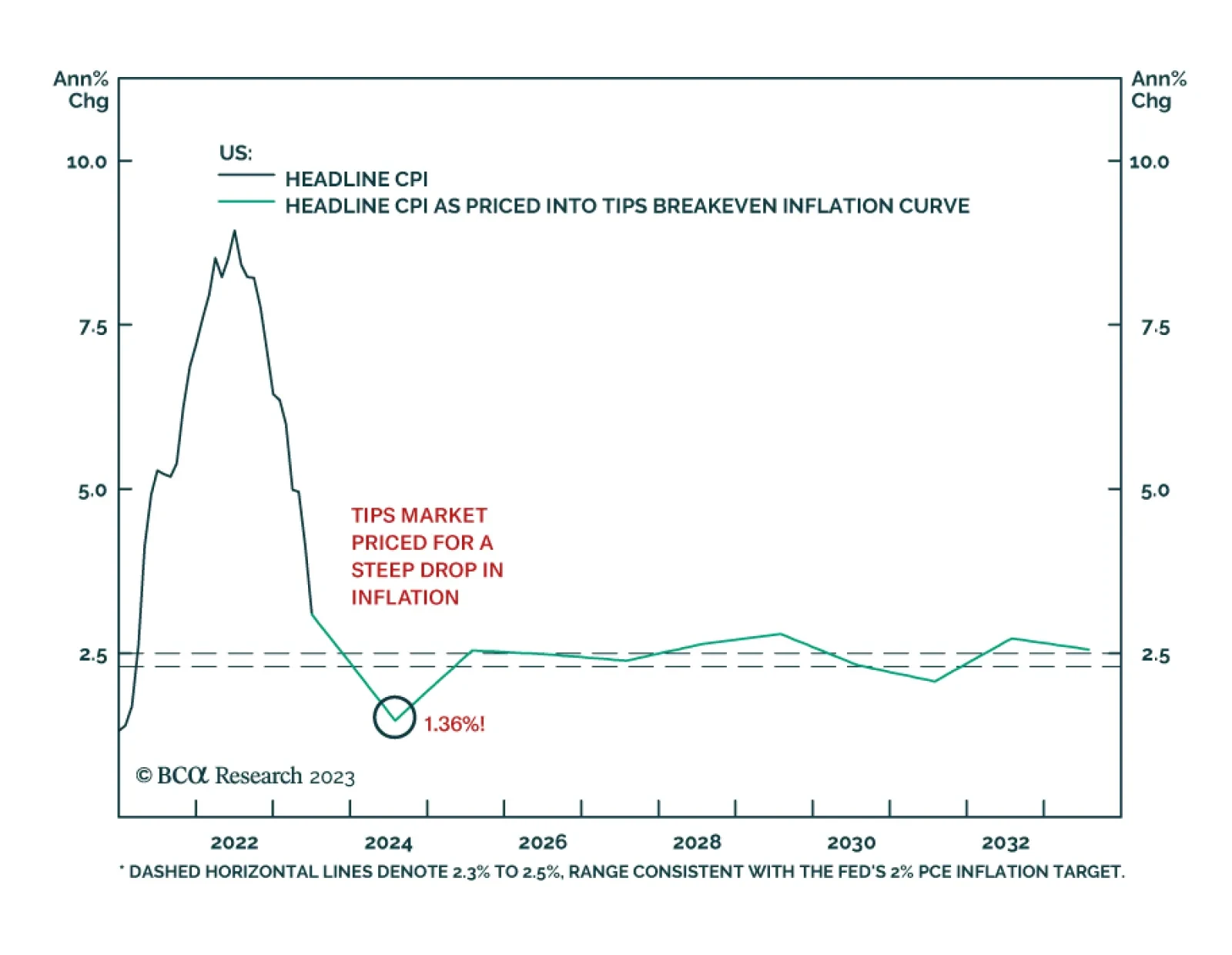

This week we preview the July FOMC meeting, provide an update on the Fed’s balance sheet and recommend a new TIPS trade.

In this report, we present our performance review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for the Q2/2023, and the outlook and scenario analysis for the next six months. The portfolio return exactly matched that of the benchmark index during the quarter, as modest gains on government bond allocations in the US, UK and core Europe completely offset losses on spread product underweights. Looking ahead, the portfolio is positioned to capitalize on an expected slowing of global growth over the rest of the year through an overweight stance on government bonds versus spread product and above-benchmark duration tilts in the US and core Europe.