Policy

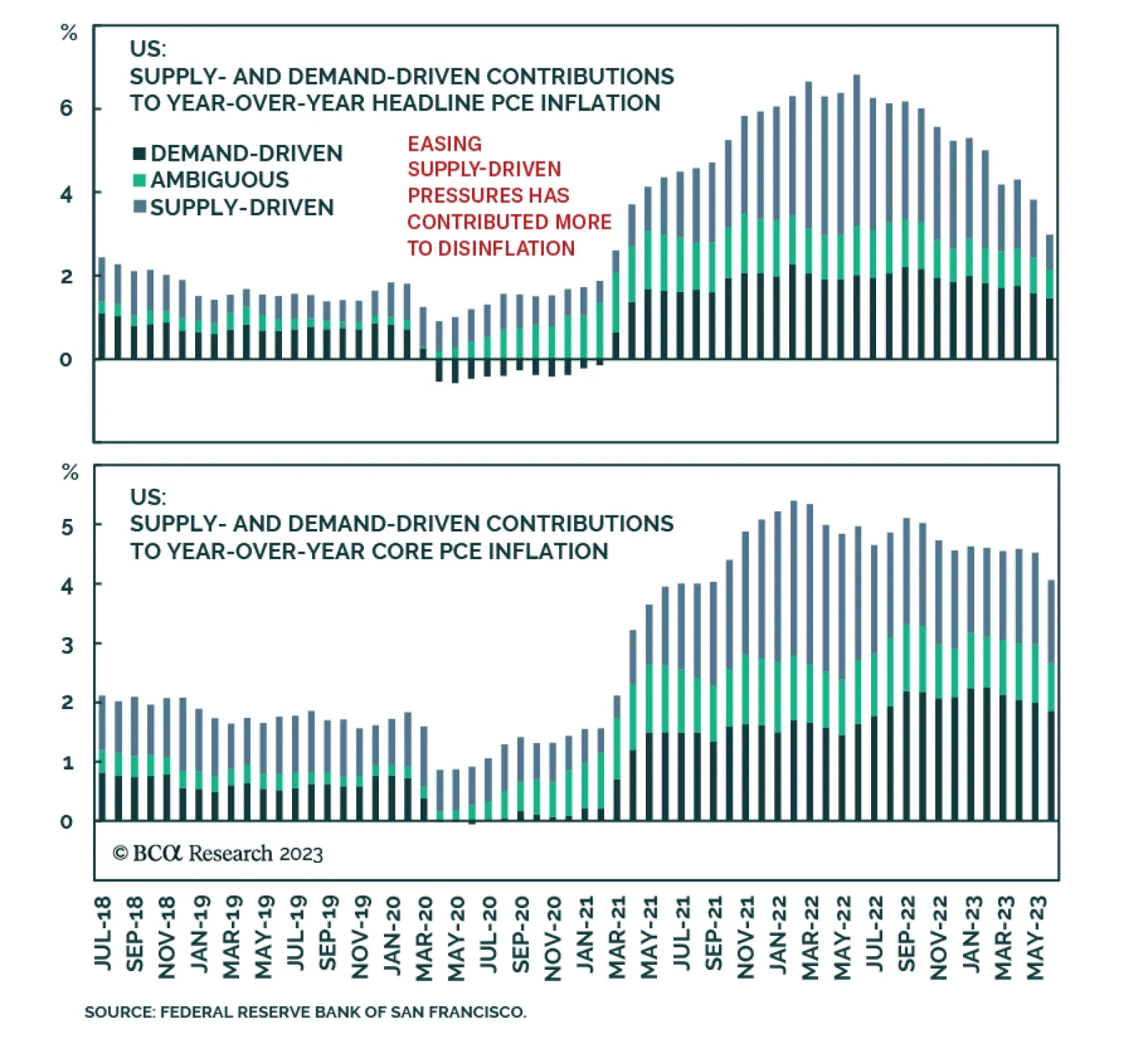

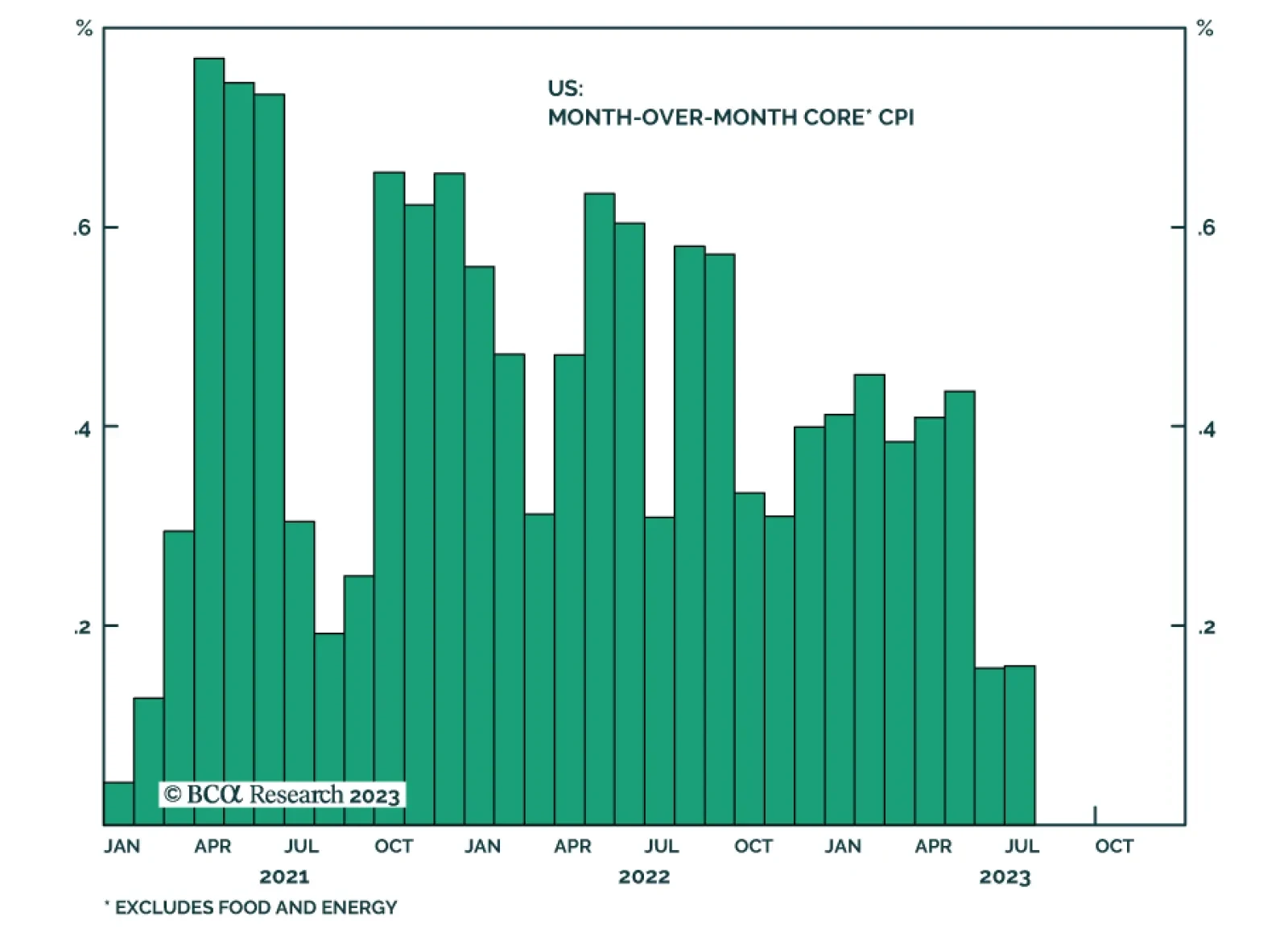

While the July US CPI release provided a positive signal that the disinflationary trend remains intact, a key question going forward is how much more scope is there for this process to run. One way to answer this question is by assessing the progress in…

According to BCA Research’s Emerging Markets Strategy service, the gap that has formed between the S&P 500 price and its operating profit margins, as well as the divergence between the S&P 500 Forward P/E ratio and the 30-year TIPS yield are…

Numerous divergences have opened up between global risk assets and global business cycle variables. These gaps are unsustainable, and odds are that the recoupling will occur to the downside with risk assets selling off.

As expected, the US CPI release shows the monthly headline and core inflation gauges were both unchanged at 0.2% m/m in July. Notably, annualized monthly core inflation fell below 2% for the second consecutive month. Similarly, the annual change in core CPI…

On Wednesday, President Joe Biden announced that a new ban on some US investment into China’s quantum computing, advanced chips and artificial intelligence sectors will come into force next year. This latest escalation is consistent with our Geopolitical…

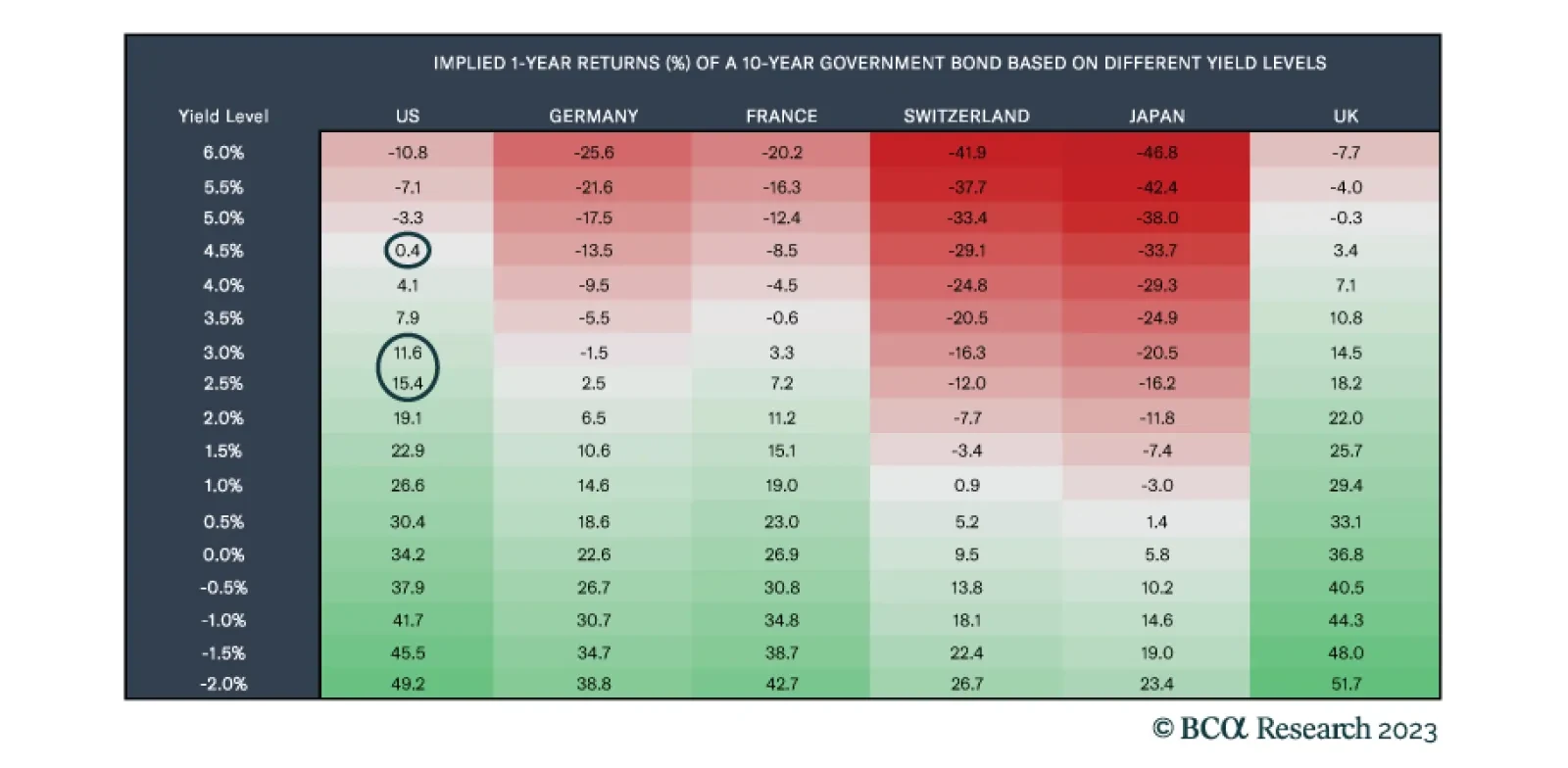

The rise in bond yields over the past few weeks has made some investors wonder whether US Treasurys and other government bonds really are a good hedge against recession. Could there be an environment in which the economy goes into recession but bond yields…

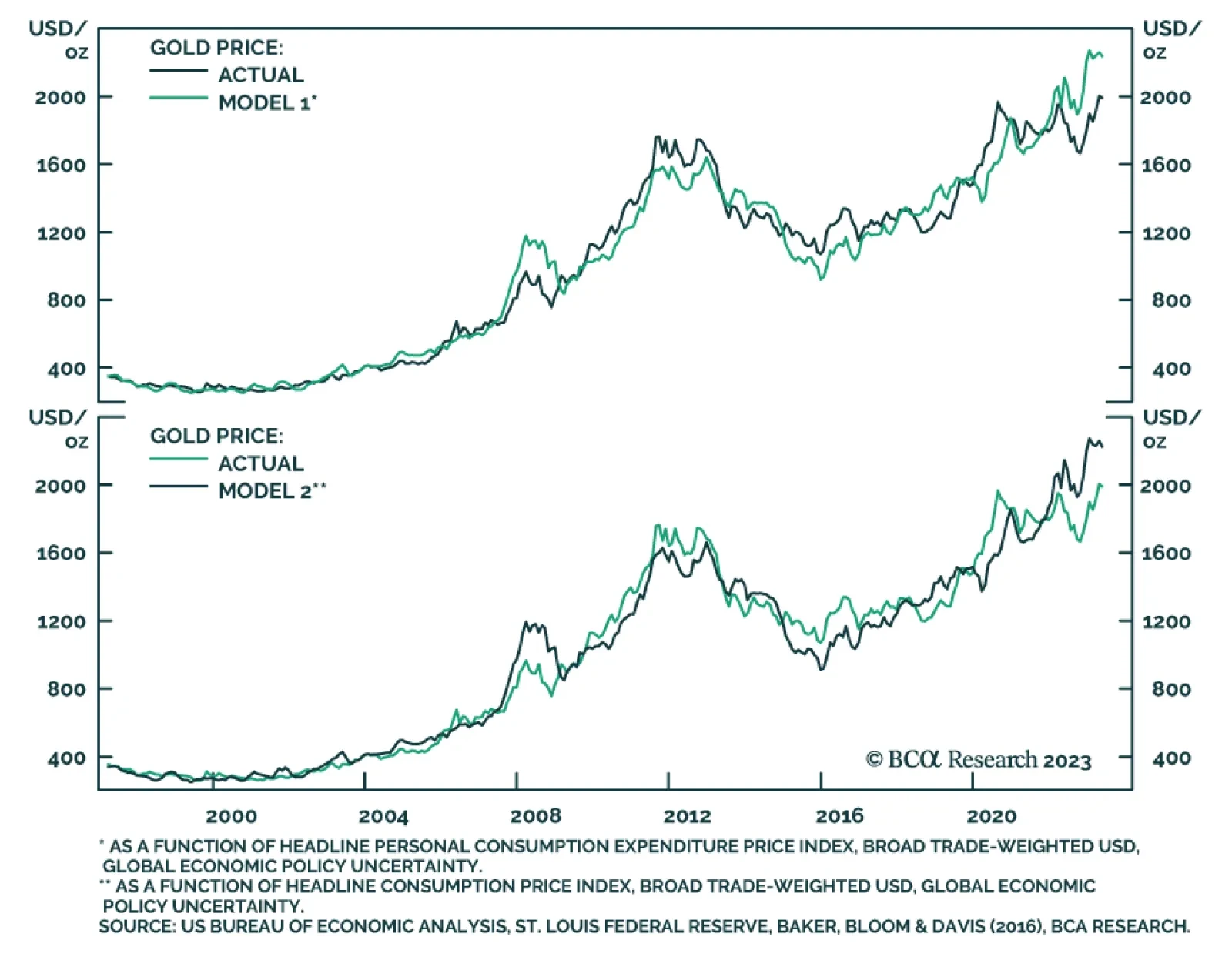

According to BCA Research’s Commodity & Energy Strategy service, gold’s appeal as a safe haven and store of value will increase as fiscal dominance overtakes monetary dominance at the Fed. Fitch’s downgrade of US debt from AAA to AA+ hit markets as the…

Some thoughts on this morning’s inflation number and implications for Treasury yields and TIPS.

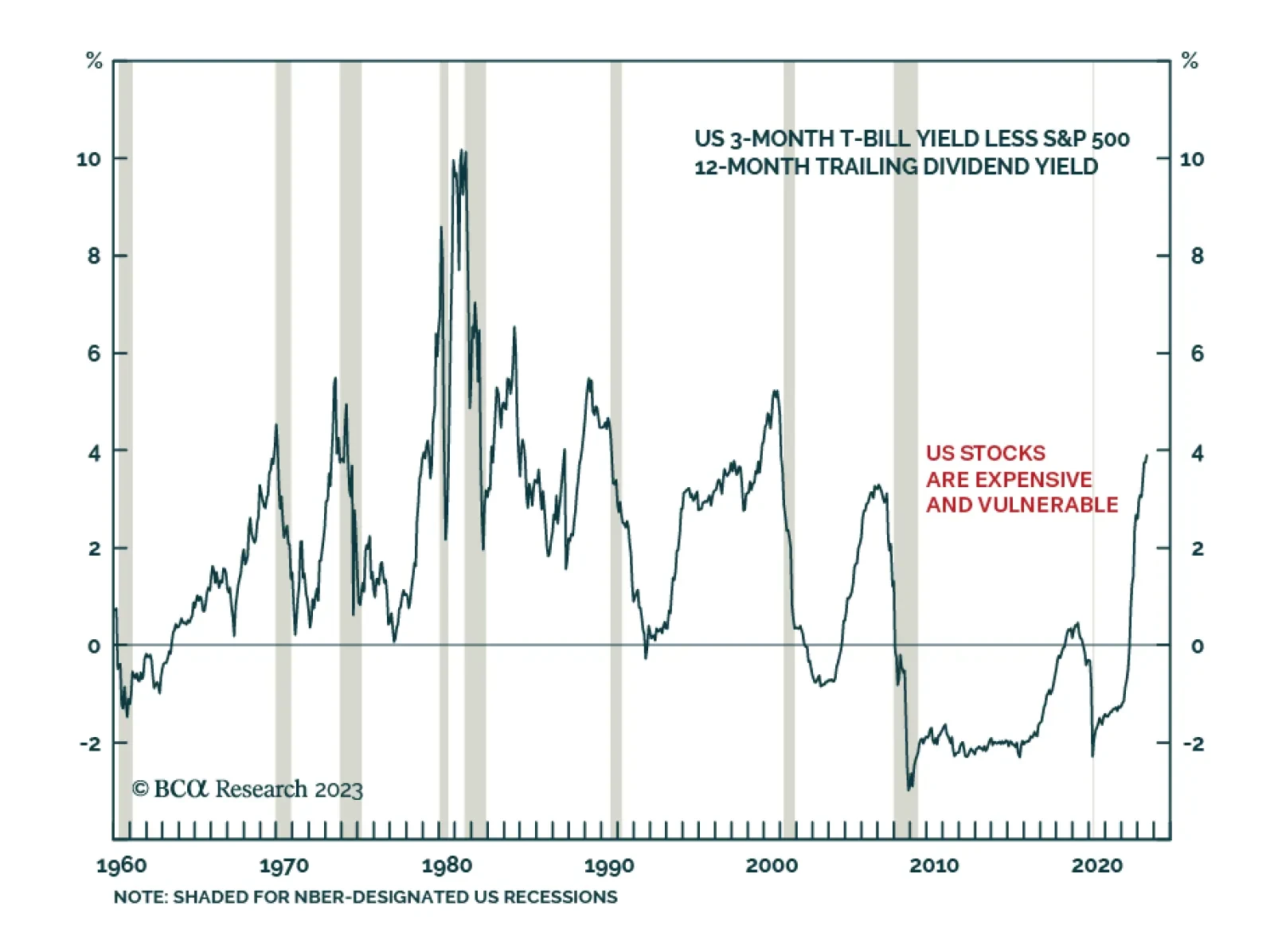

During the last economic expansion, a structurally overweight allocation to stocks was at least partially warranted by the idea that “There Is No Alternative” – or “T.I.N.A.” During the last expansion, very accommodative monetary policy significantly reduced…

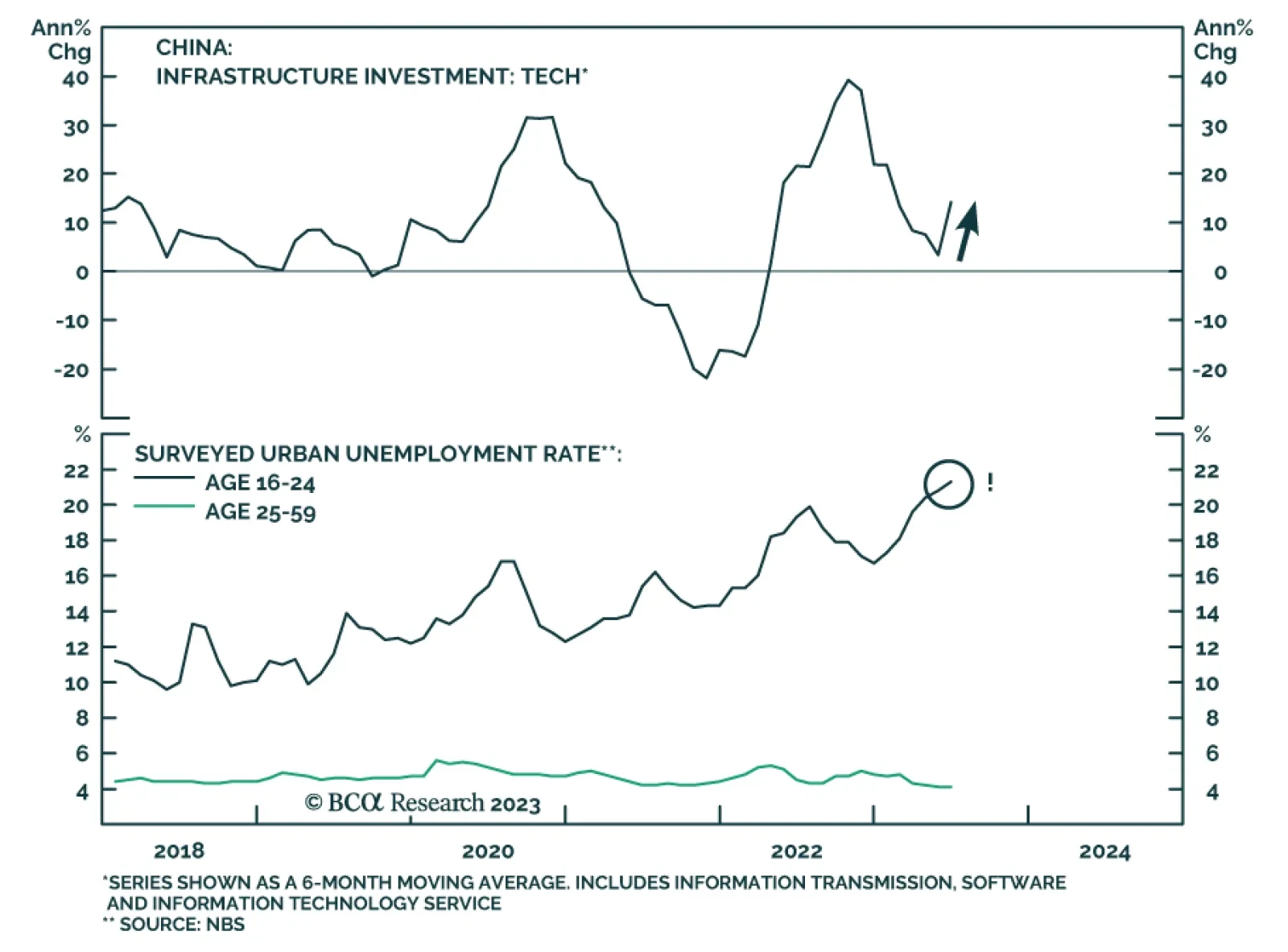

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.