Peru

Peru is well established to elect a pro-market government in the June 7 run-off, with institutional constraints limiting left-tail policy risks. We will go long Peruvian assets when Hormuz volatility subsides.

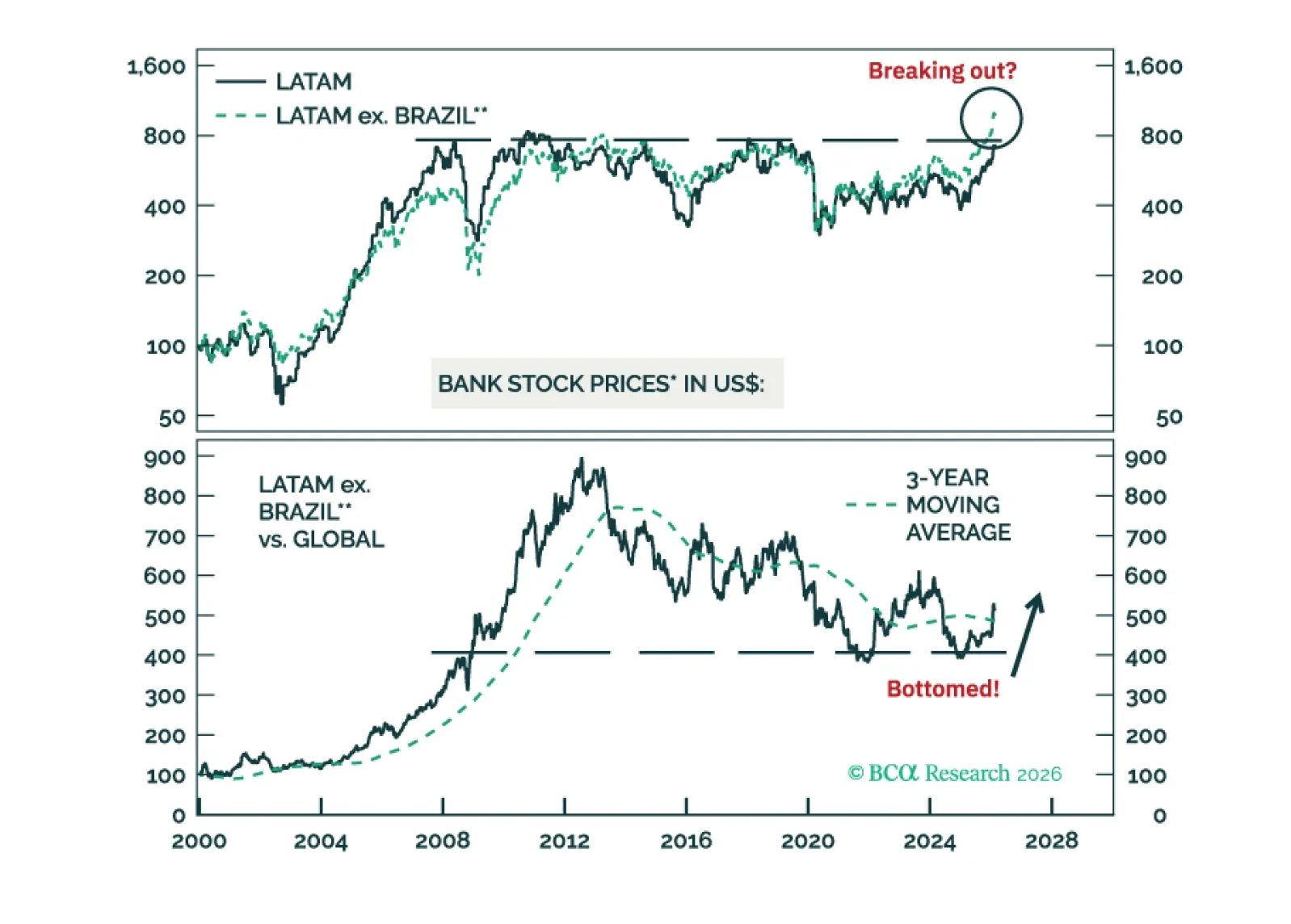

Go long LATAM ex. Brazil banks / short global bank stocks. Brazilian bank equities will underperform due to poor and worsening macro fundamentals.

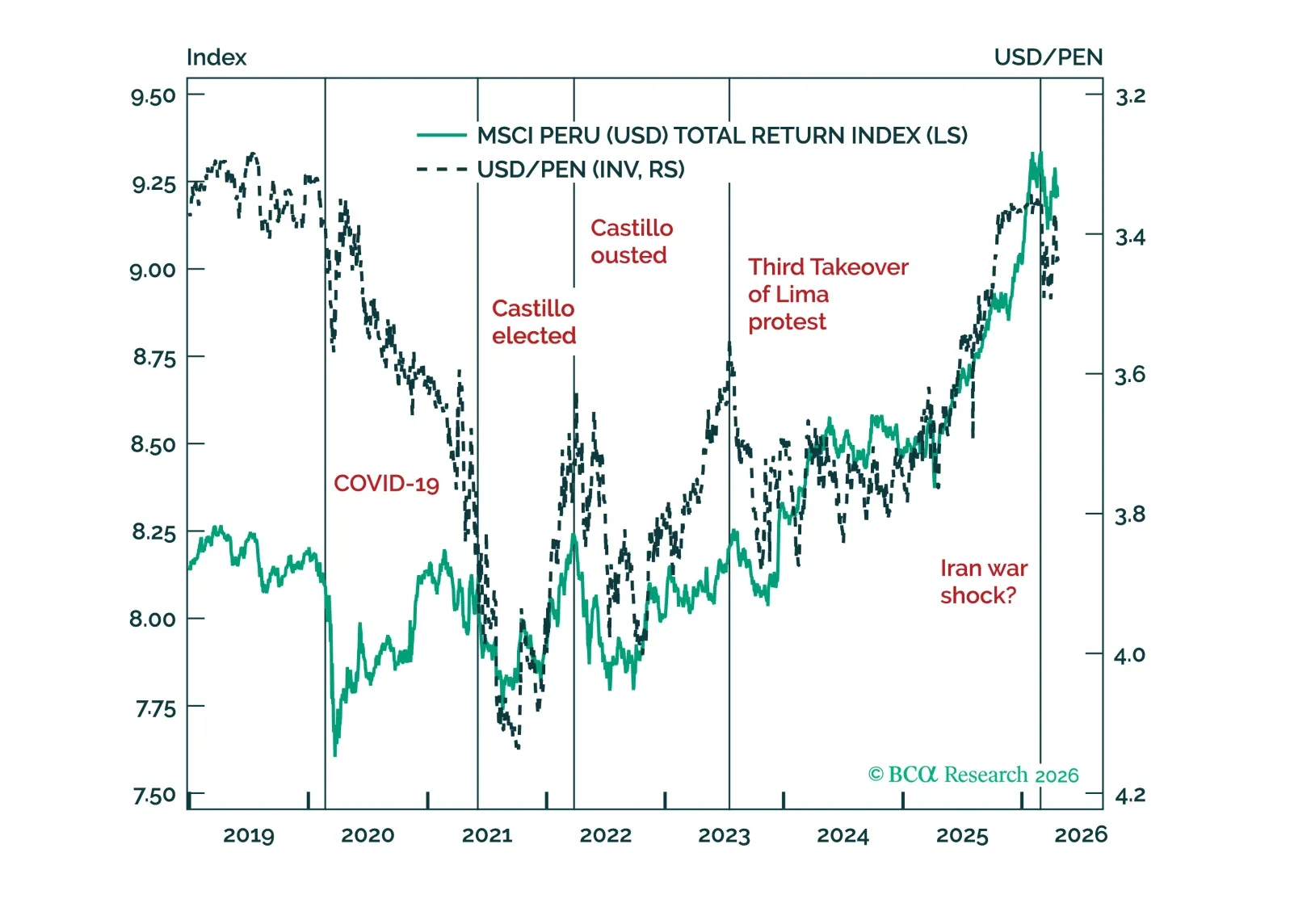

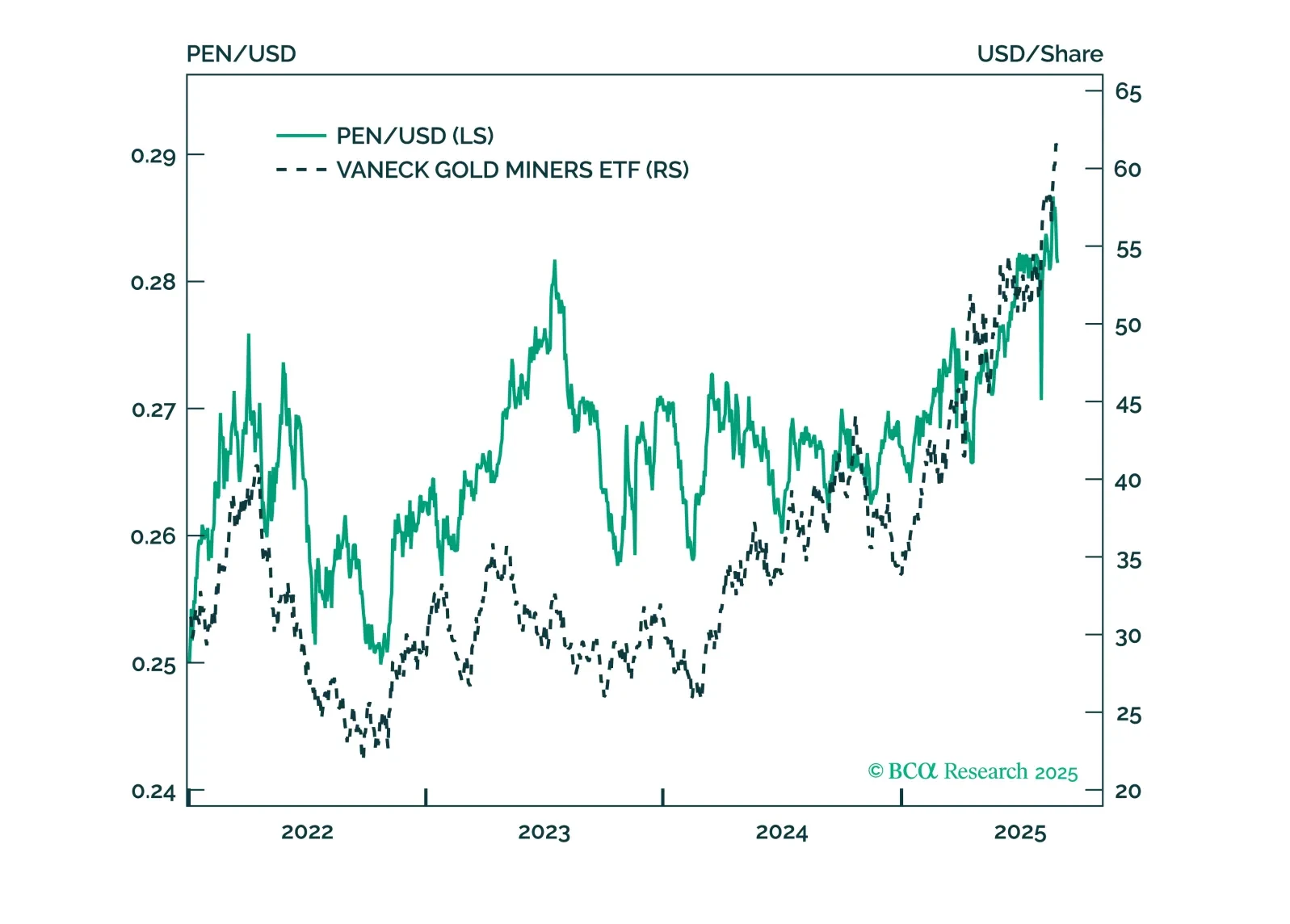

Peru’s April 2026 election will inject political volatility, but fundamentals are strong and we are constructive. Buy gold mining equities and gold on dips to capture the supportive global cycle and wait for a more attractive entry point for Peruvian assets.

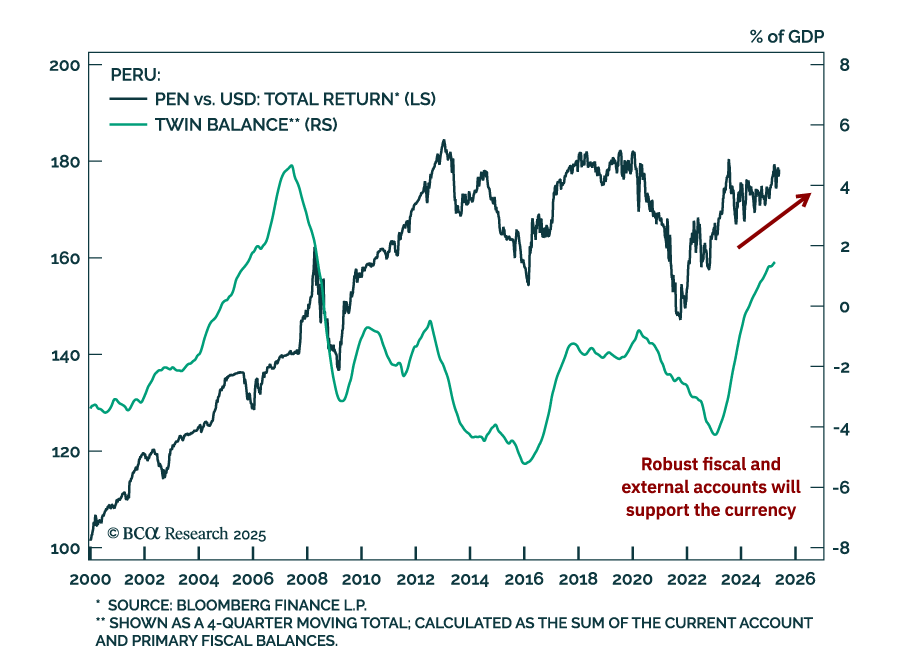

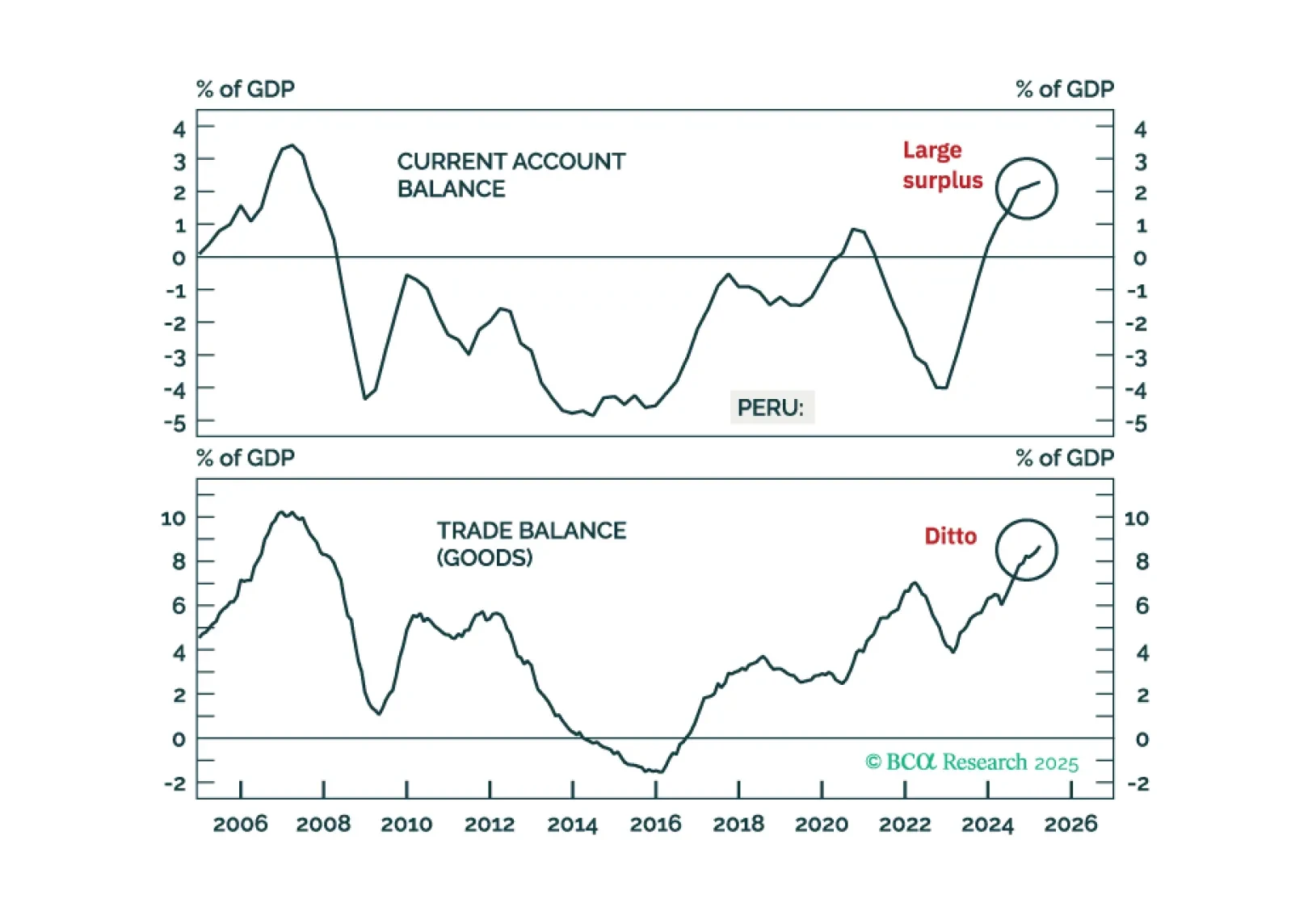

Peru’s economic resilience will help its markets outperform their EM peers. Domestic macro fundamentals are robust, and strong external accounts will lead to a stable-to-strengthening currency versus the US dollar. Overweight Peruvian equities, local bonds, and sovereign credit relative to their respective EM benchmarks, and go long 10-year domestic bonds (currency unhedged).

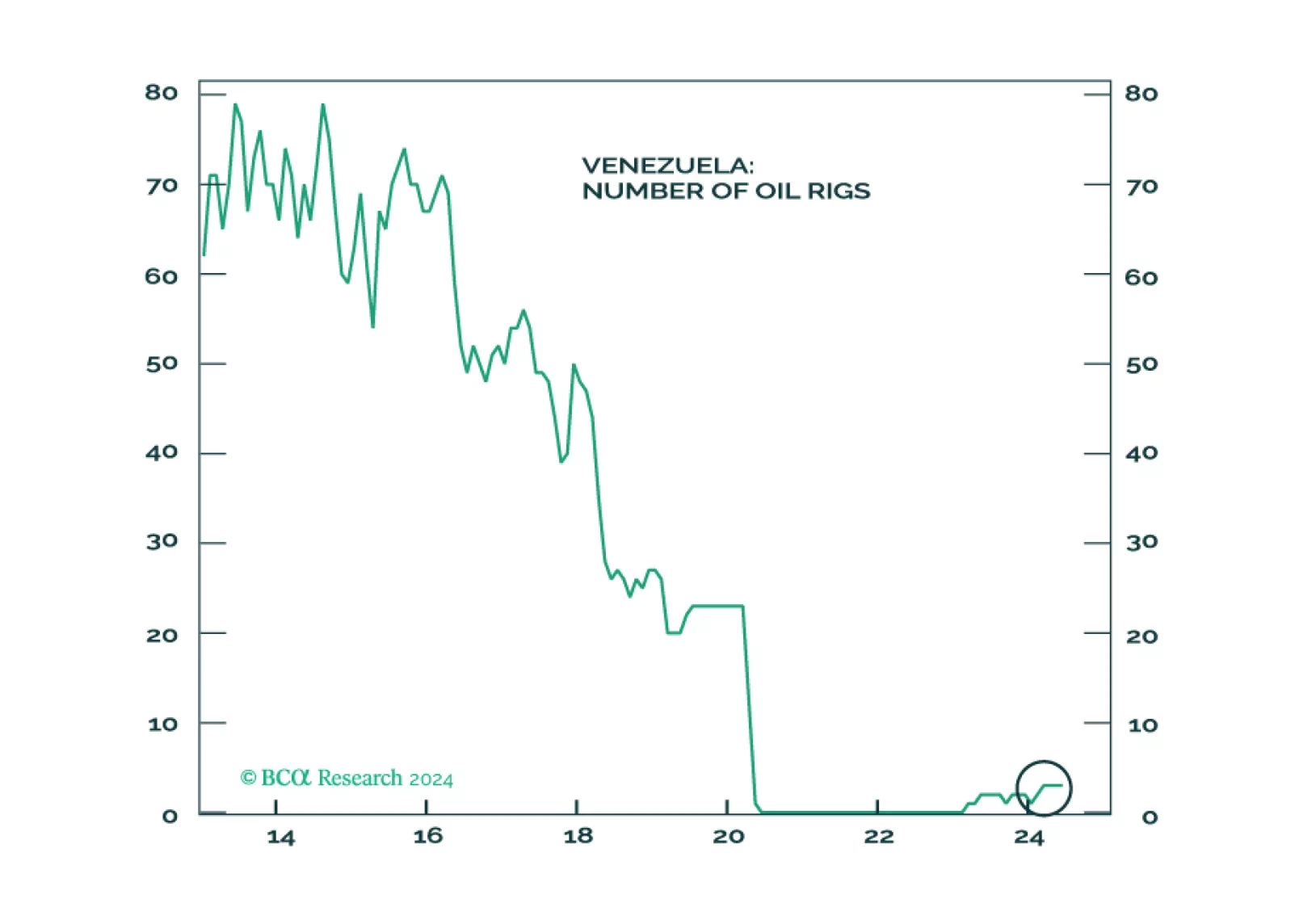

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

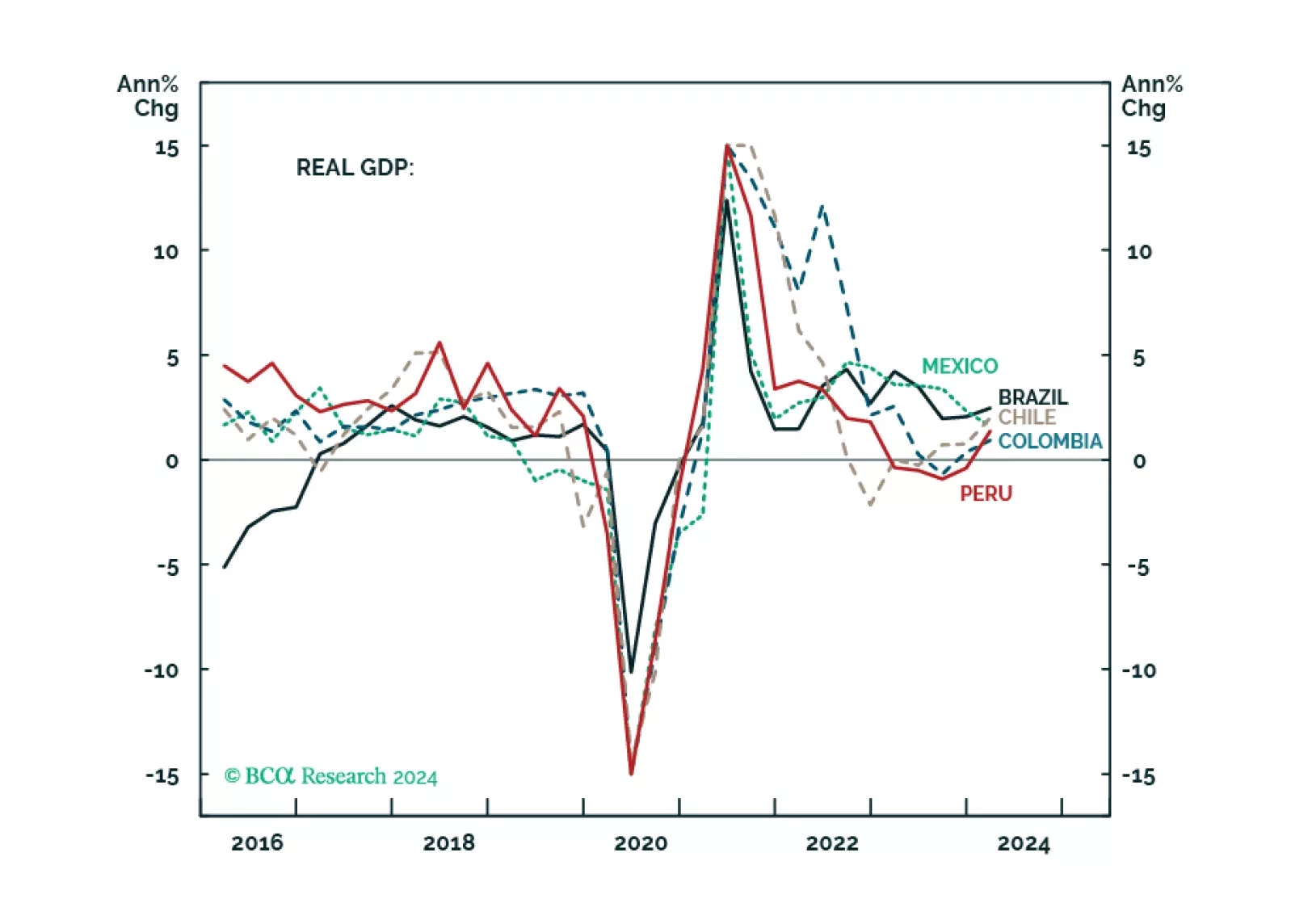

Non-trivial macro divergences have emerged between mainstream LATAM economies. This report compares and ranks Brazil, Mexico, Colombia, Chile, and Peru based on their business cycle outlook, macro policy stance, external accounts, and structural fundamentals. All in all, LATAM risk assets will fall in absolute terms given a strengthening US dollar and a global risk-off move in the coming months. Within LATAM, we favor Mexico, Chile and Peru, are neutral on Brazil, and bearish on Colombia.

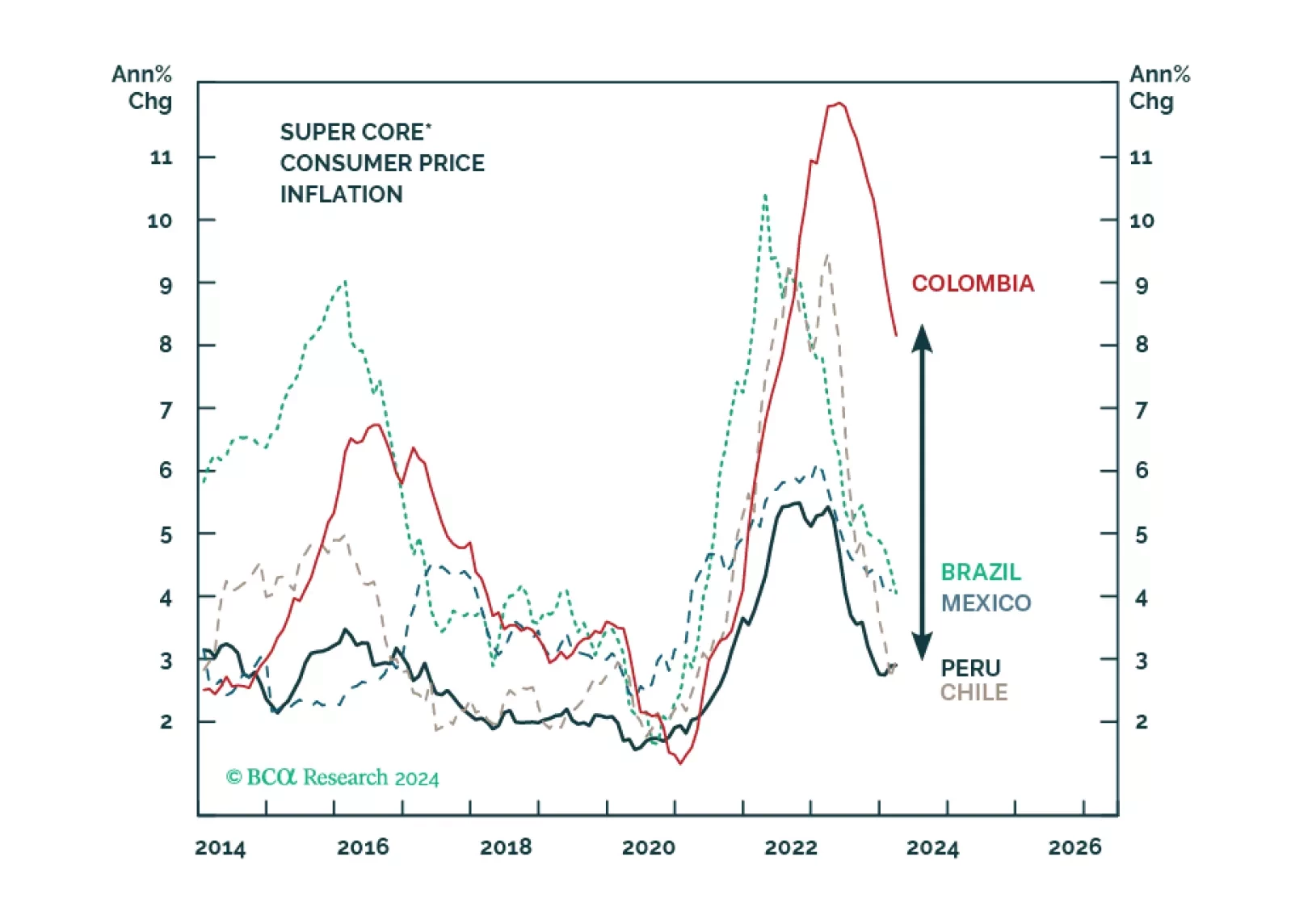

Peru is entering a benign macro environment: low and falling inflation amid a solid economic recovery. The country’s balance of payments position is robust, which will help the PEN depreciate by less than other EM currencies. The political situation is on shaky ground, but a regime shift will have to wait until 2026. We remain overweight on Peruvian equities, domestic bonds, and sovereign credit relative to the EM benchmarks.

Peruvian financial markets will outperform their EM peers given the country’s clear macroeconomic and political visibility. Low and plummeting inflation, a decelerating economy and a lack of economic excesses will allow the central bank to cut rates in the coming months and achieve a soft landing. A reluctant alliance between Congress and the President will ensure political stability until 2026.

Peru is not suffering from economic or financial excesses: genuine inflation is subdued, fiscal and monetary policies are orthodox, and external accounts are healthy. While political instability has risen anew, markets will likely push through the political noise. Given this, we are upgrading Peruvian equities and local and sovereign USD bonds to overweight within their respective EM portfolios.