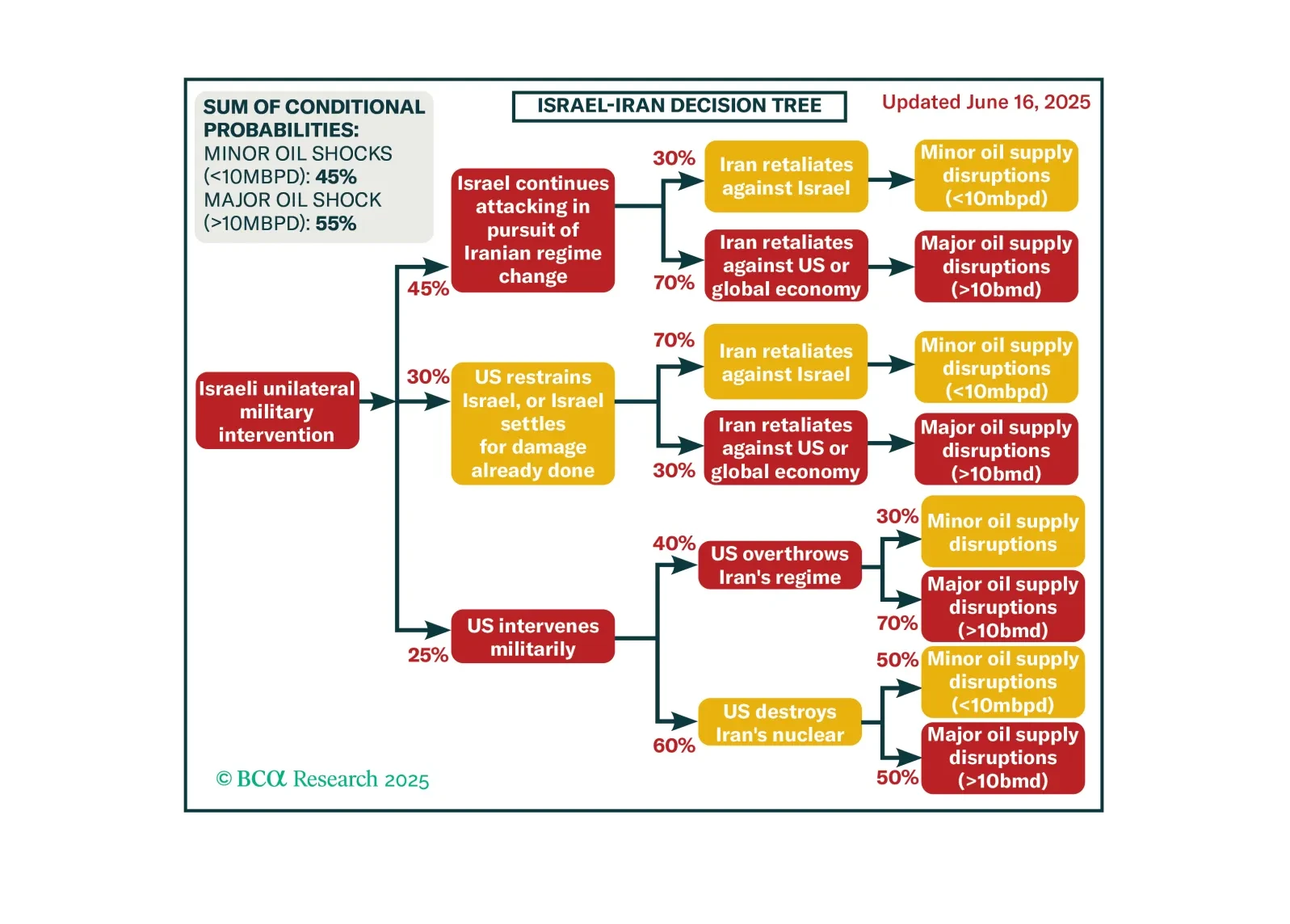

Oil

Israel’s attacks on Iran will continue until Iran is forced to strike regional oil supply to get the US to restrain Israel. That may not work. Investors should prepare for a broader economic impact of the conflict.

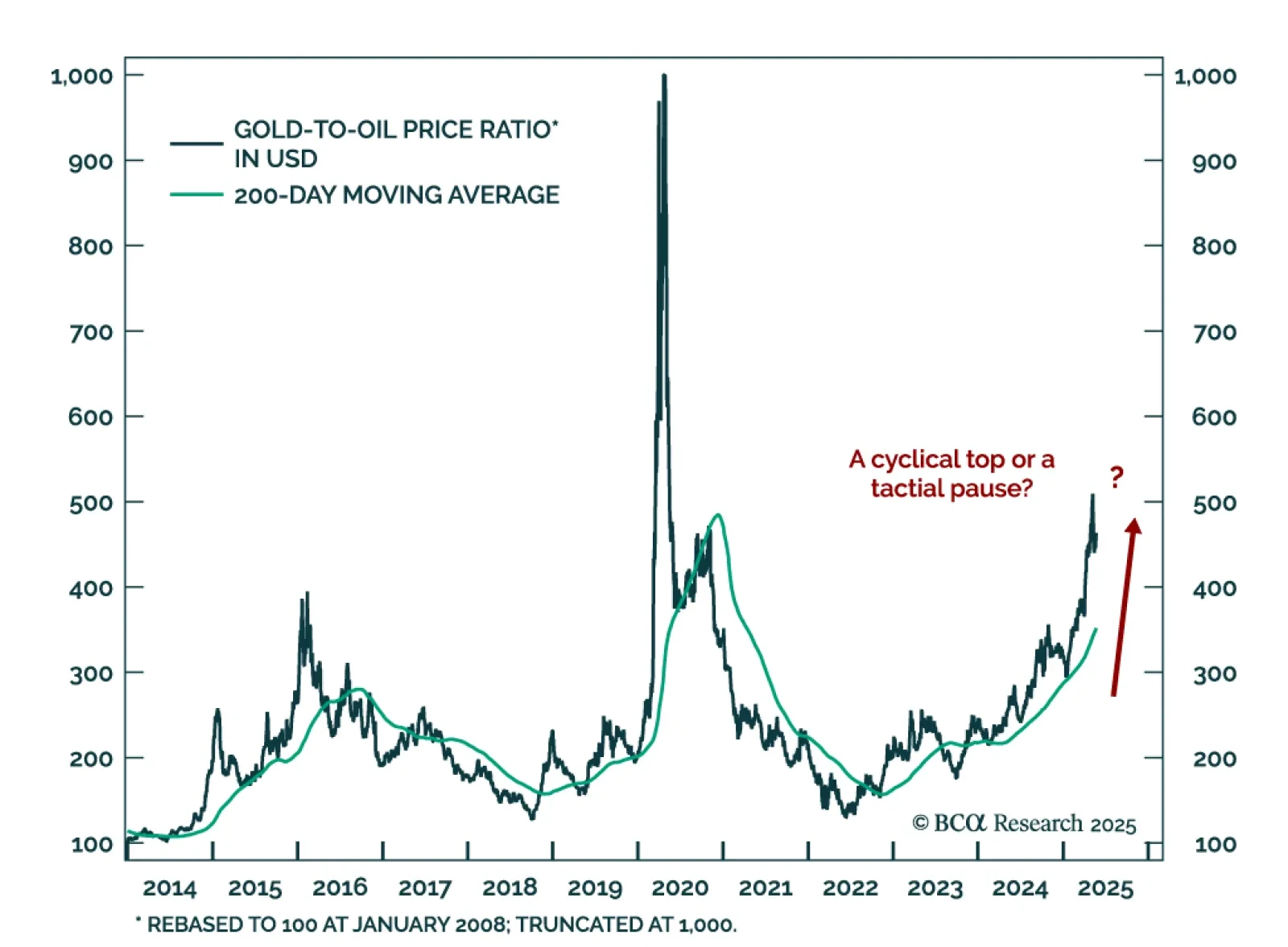

Investors should hold gold, build up some cash, tactically overweight US equities relative to global, and prepare for at least minor oil supply shocks – possibly major shocks – as the Israel-Iran war escalates.

Investors often rely on past relationships to predict future outcomes. This strategy is at risk now that several commodity correlations have broken down. We explore the causes and sustainability of the new commodity relationships.

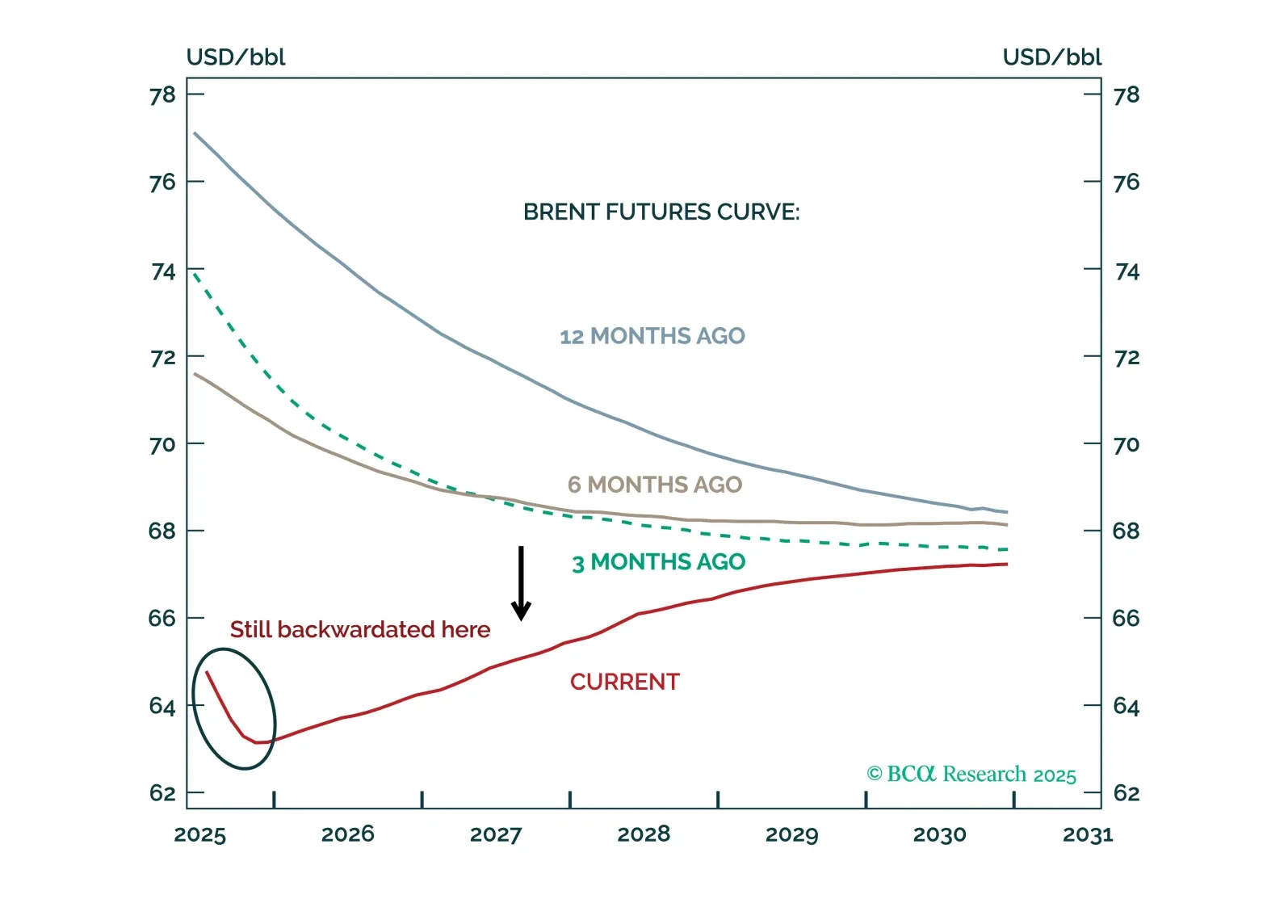

Oil, copper, and gold futures curves have recently experienced abnormal shifts and twists. Brent is no longer fully backwardated, copper curves on the LME and CME have diverged, and gold is in a steep contango.

We examine the drivers and implications of these shifts for prices and curve structure across the three commodities.

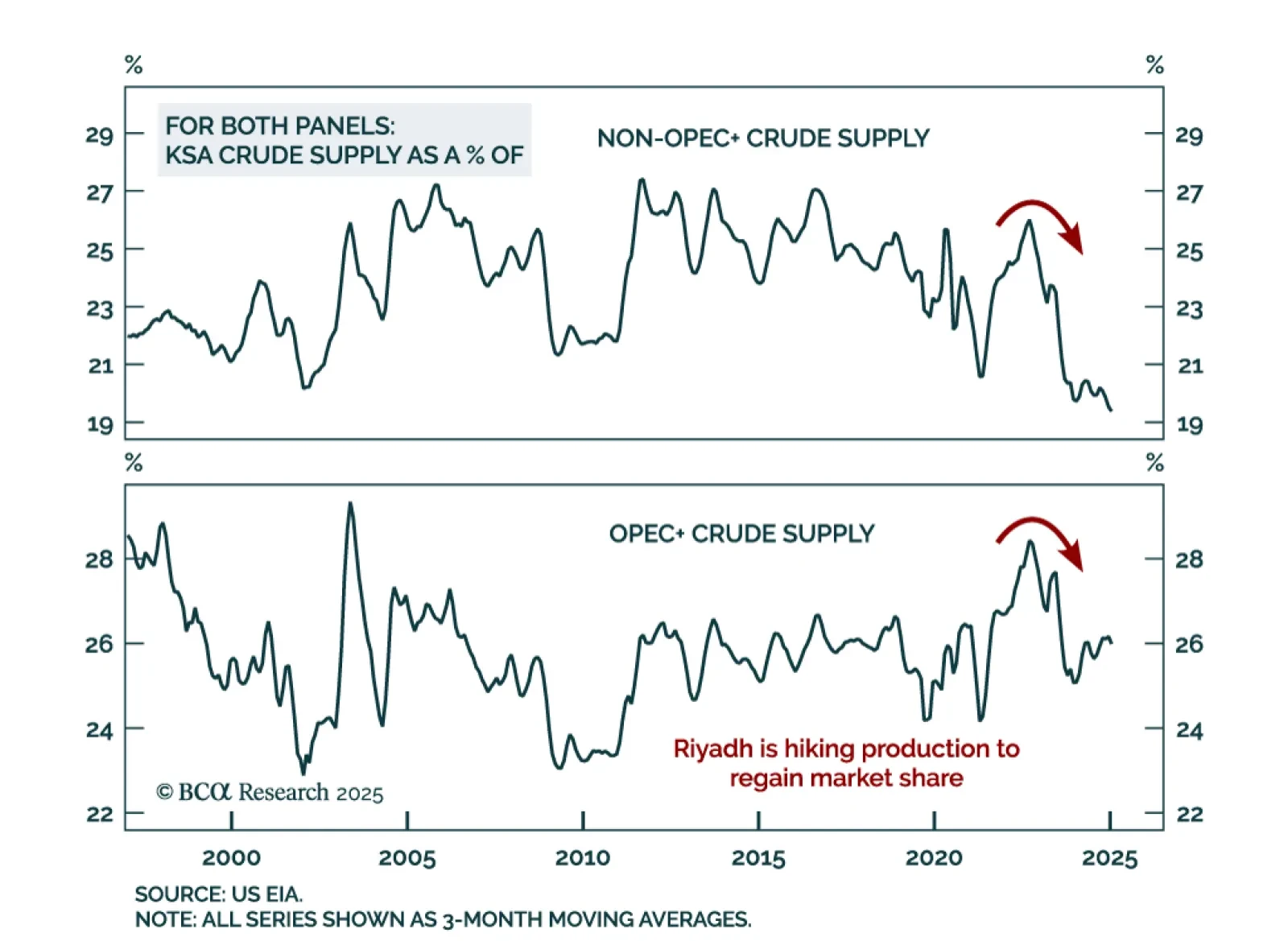

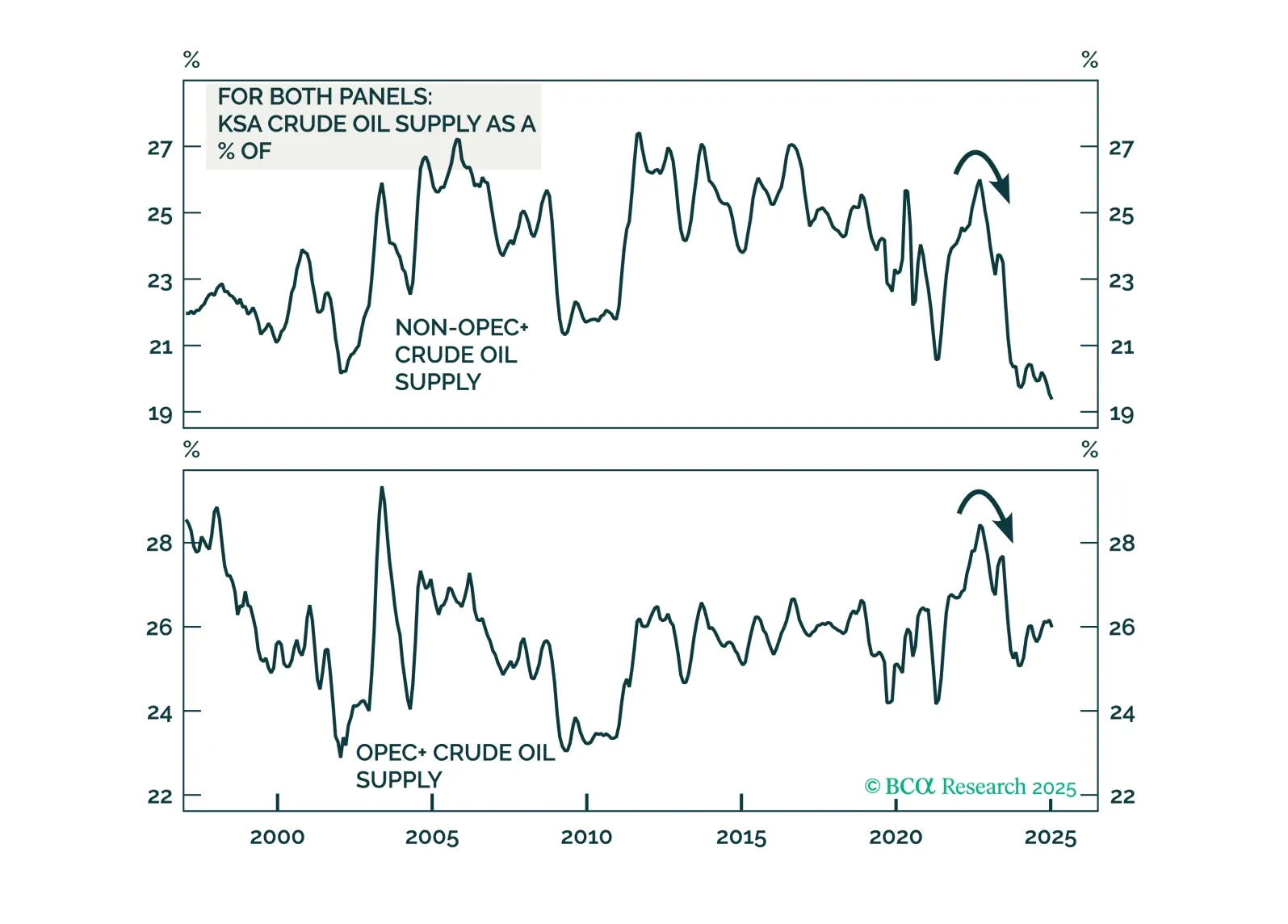

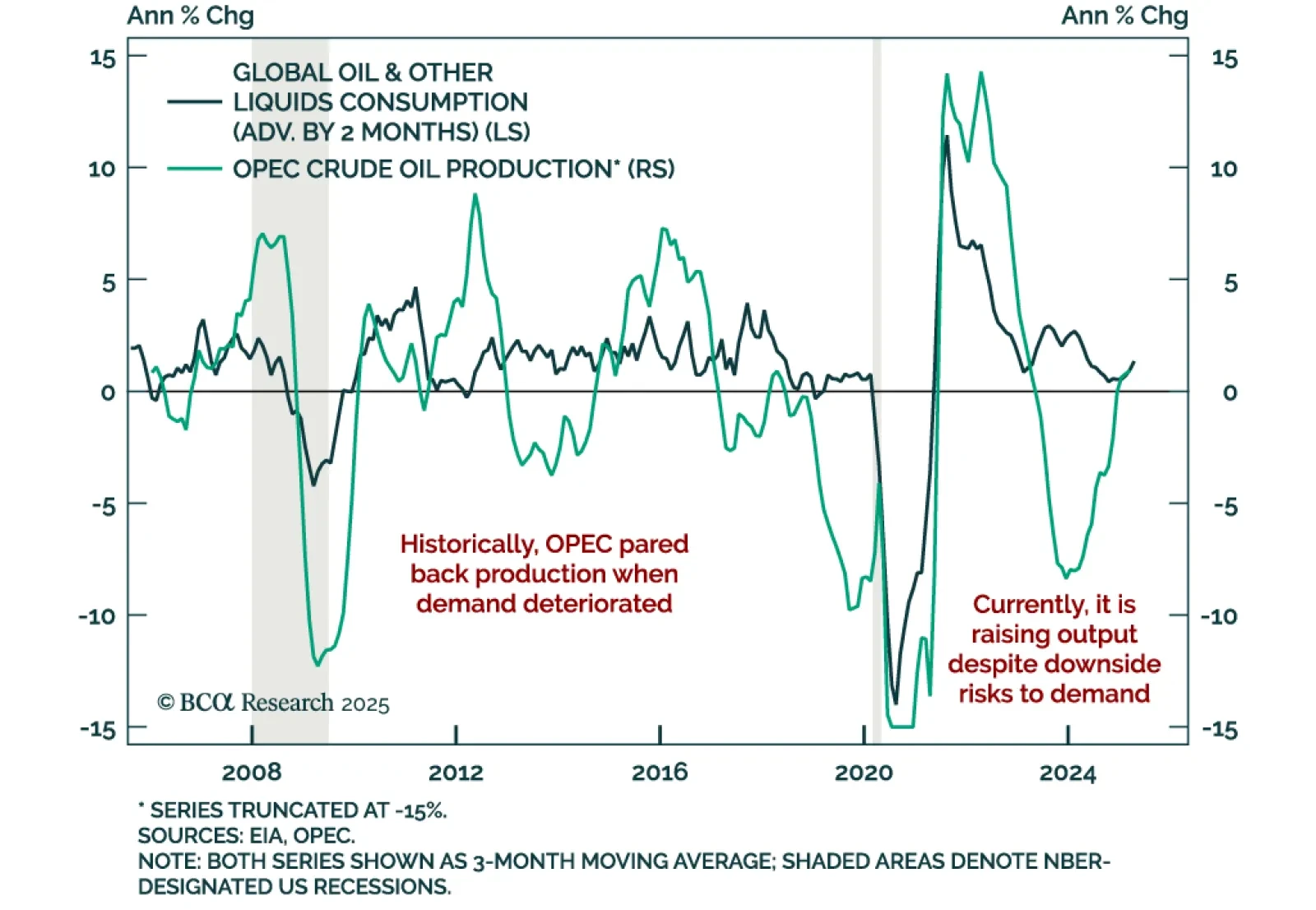

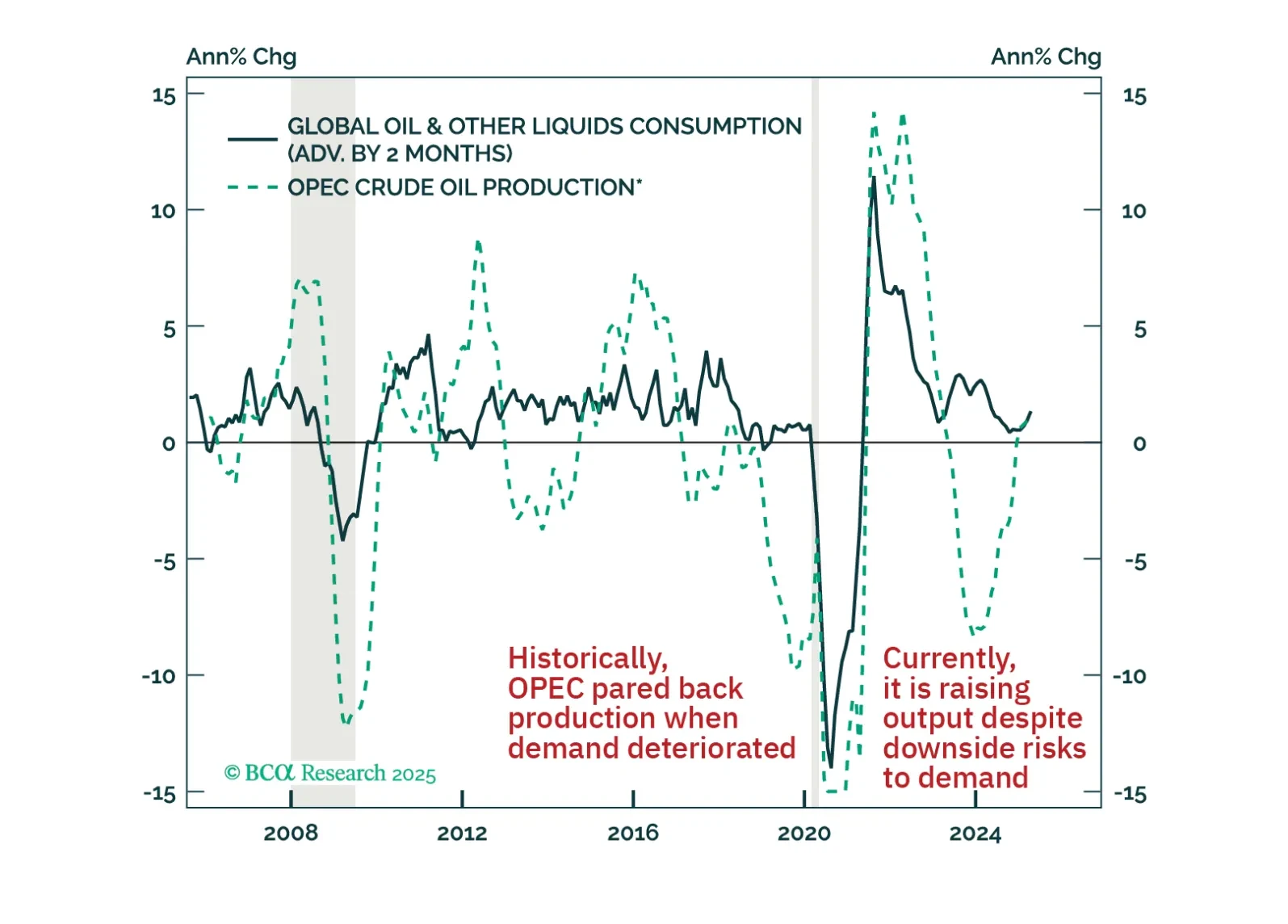

OPEC+ recently announced another outsized oil production hike, tripling its planned June output increase to 411k b/d for the second consecutive month. Our take on why KSA is boosting crude output at a time of heightened downside demand risks is that it is pursuing an oil price war lite. President Trump is not only blessing this strategy but also depending on it.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

Oil has borne the brunt of the year-to-date deterioration in cyclically sensitive financial assets. It is a key underperformer both within the commodity space and among global risk assets. This underperformance underscores that in addition to the trade war-induced headwind to demand, bearish supply-side developments are also weighing down on crude prices. As we discuss in this report, these dynamics will likely continue exerting downside pressure on oil prices over the coming weeks and months.