Oil

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

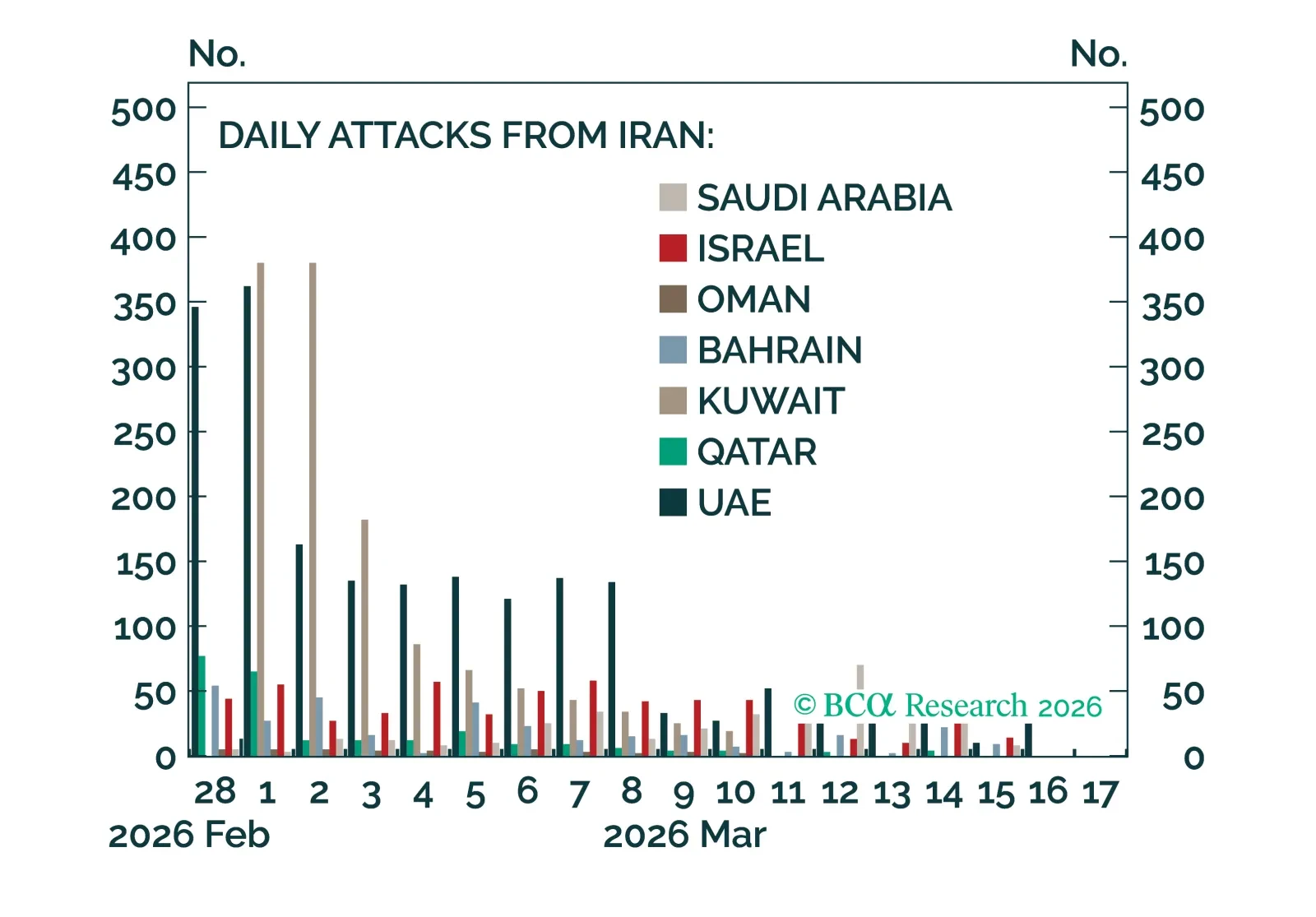

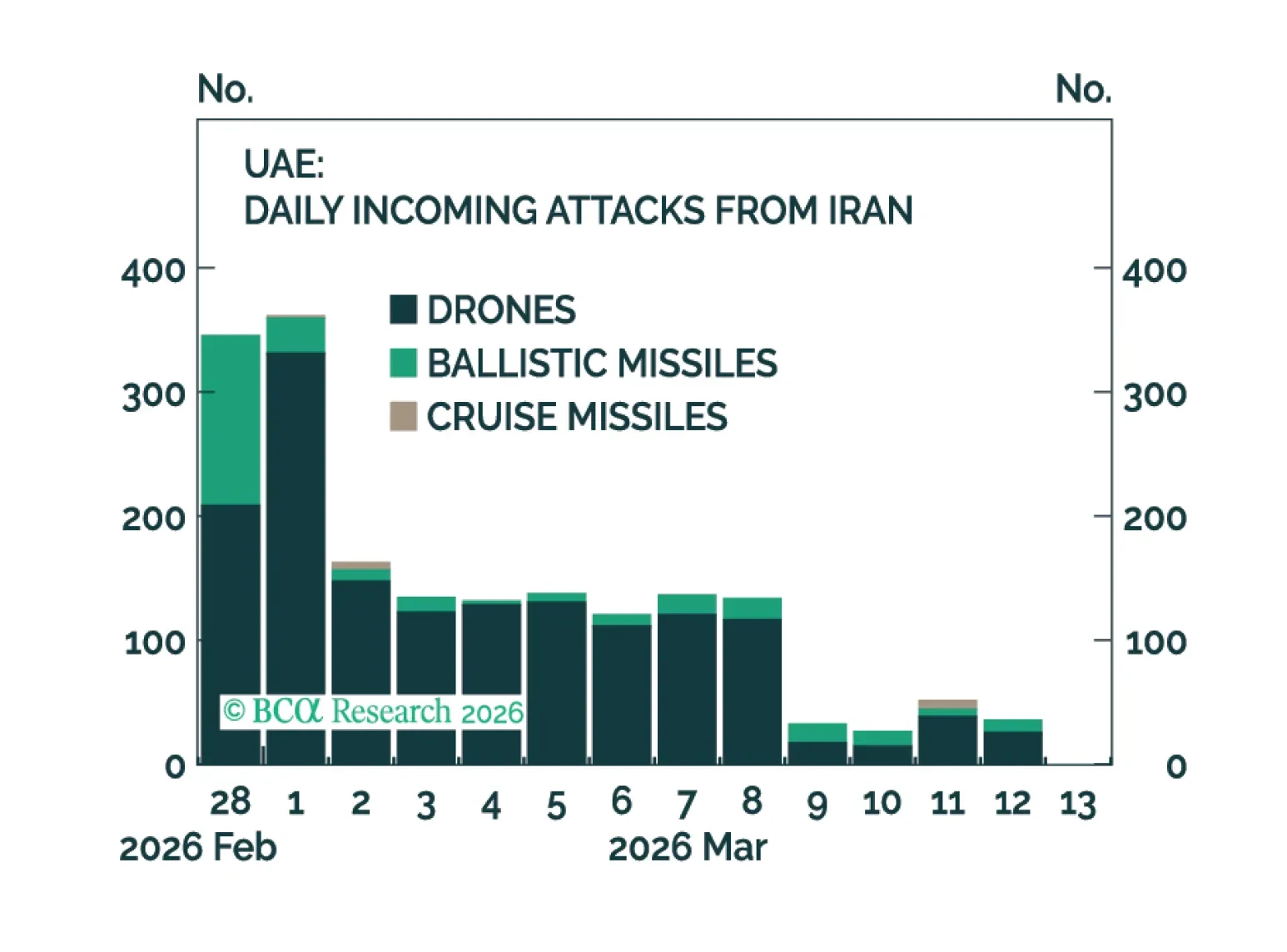

Overnight, the Israeli military reported that it managed to kill two high-profile Iranian leaders: the Secretary of the Supreme National Security Council and the leader of the internal paramilitary group, the Basij. Meanwhile, the Gulf States reported more interceptions of drones and missiles from Iran.

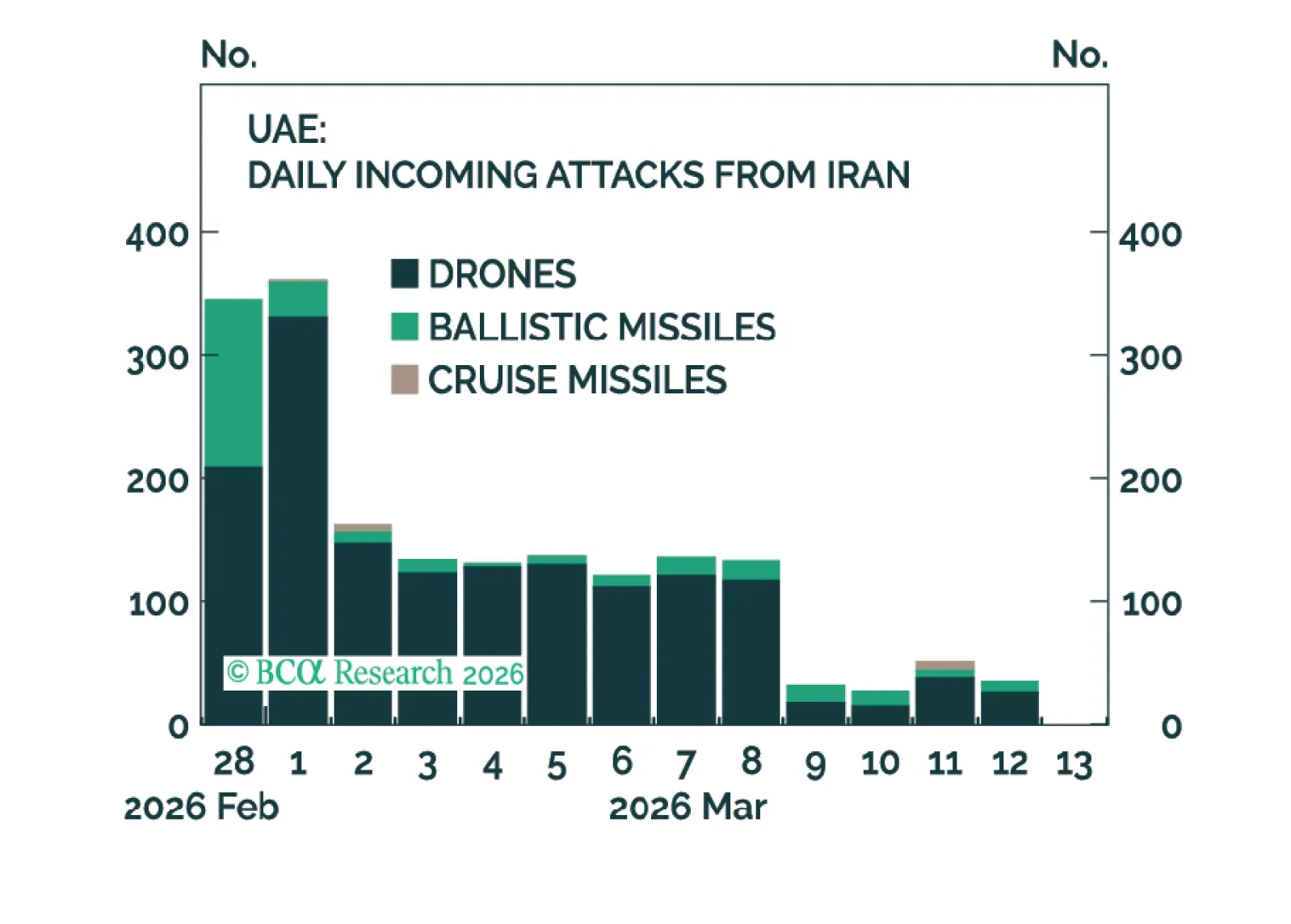

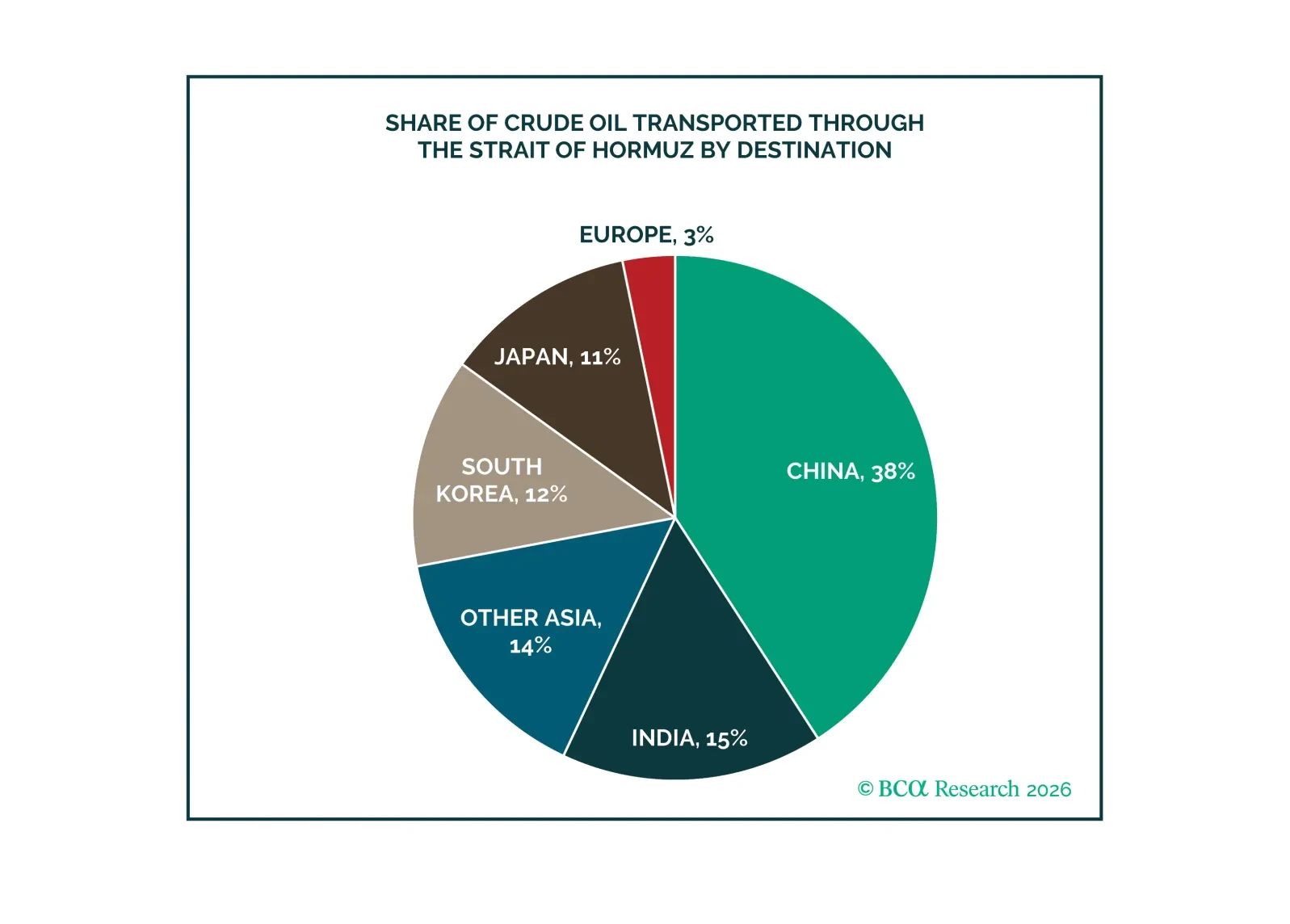

The conflict in the Middle East persists as the US and Israel continue their strikes, and so does Iran’s retaliation with drones and ballistic missiles against the Gulf States. The Strait of Hormuz is still essentially closed, despite some ships being allowed to traverse.

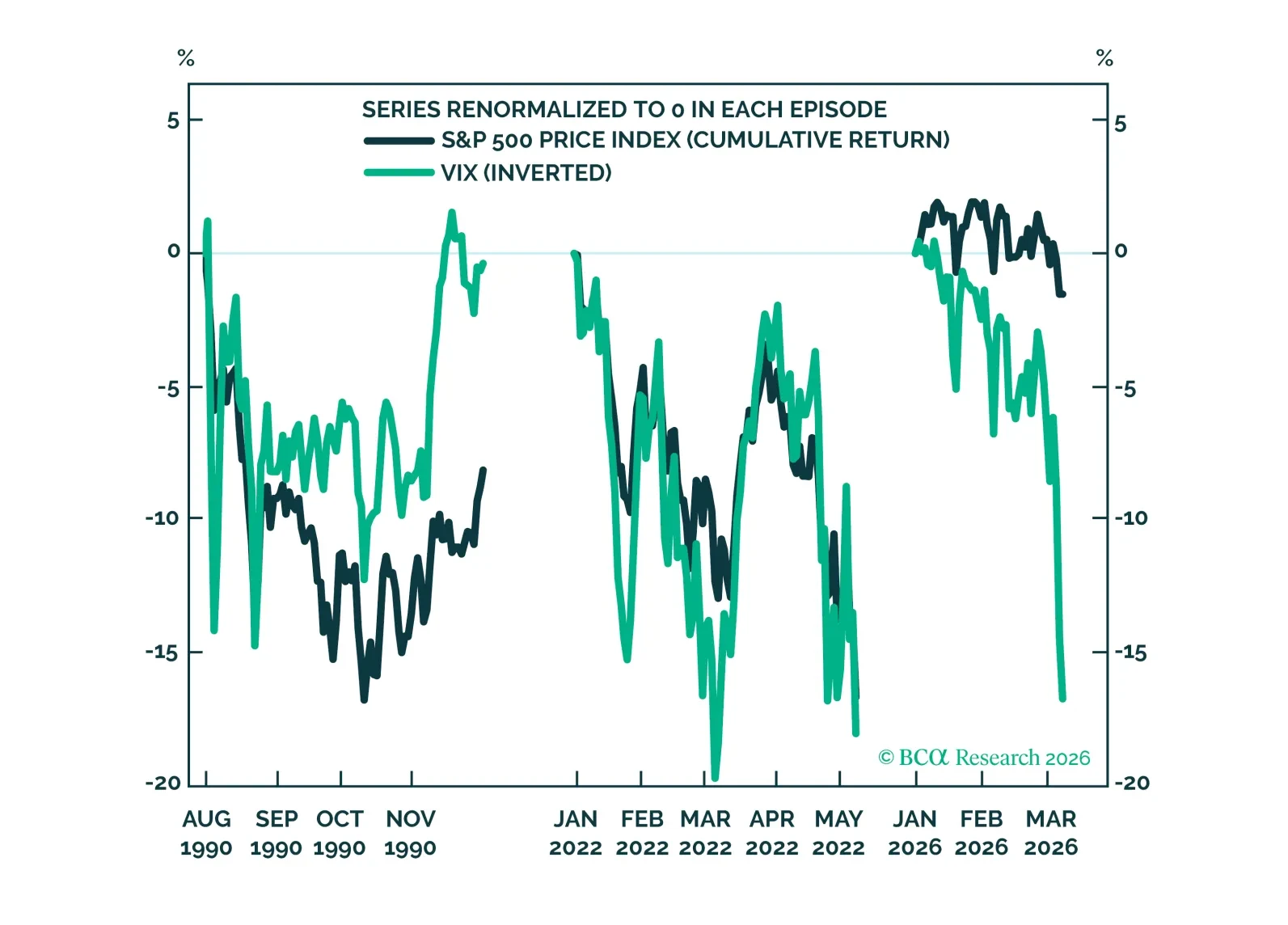

Middle East tensions sparked a surge in volatility, yet the S&P 500 decline has been comparatively modest. Across asset classes, moves seem related to risk preferences and near-term inflation concerns. Within equities, some cyclicals are under pressure, but the equity market’s growth view has been resilient, while the inflation view has climbed.

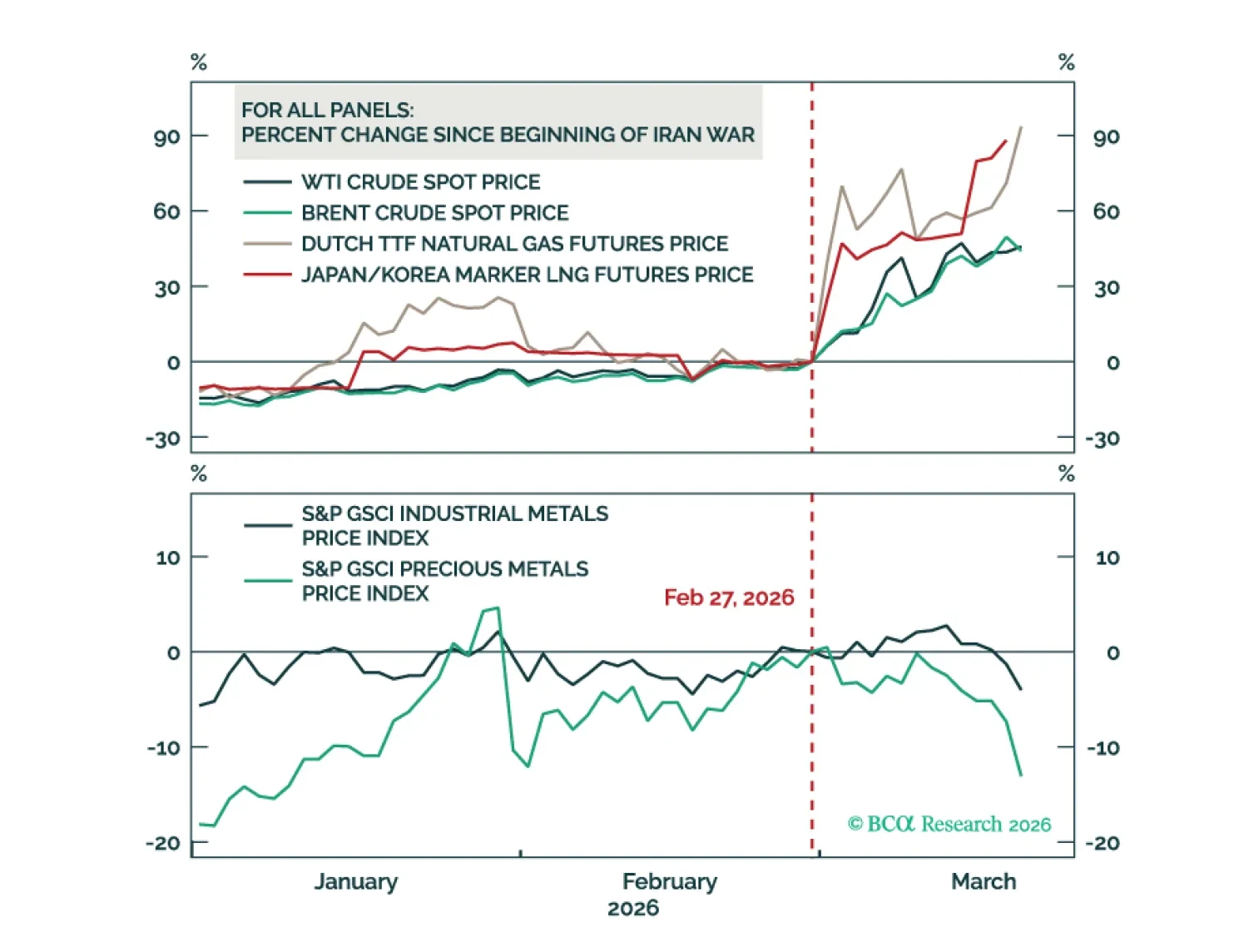

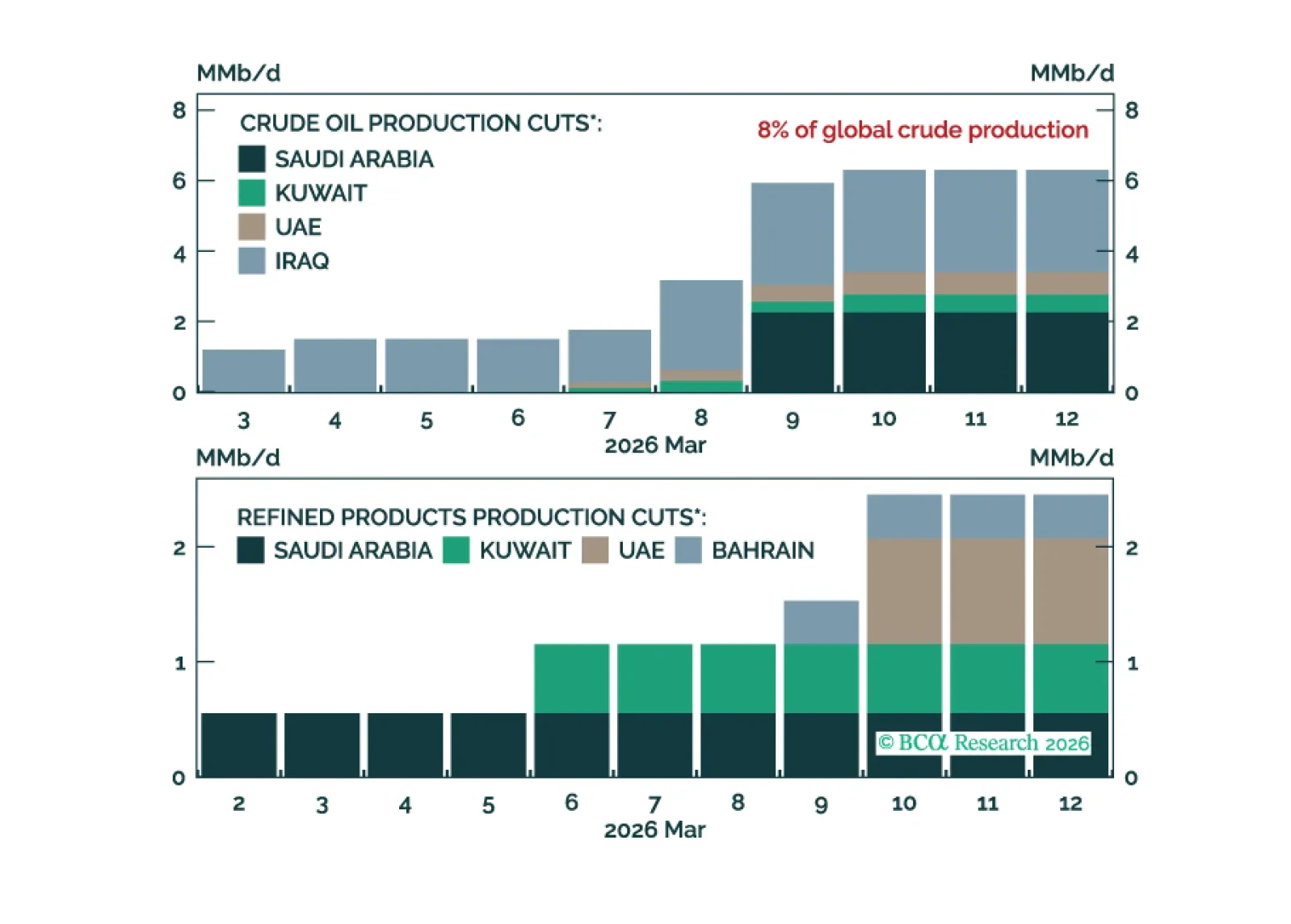

We outline a framework for the Iran war's impact on the commodity outlook in the event of a prolonged Strait of Hormuz disruption. We break it down into three phases: (1) the Initial Shockwave, (2) the Ripple Effects, and (3) the Backwash. The first phase has largely passed, and we are now in the Ripple Effects phase.

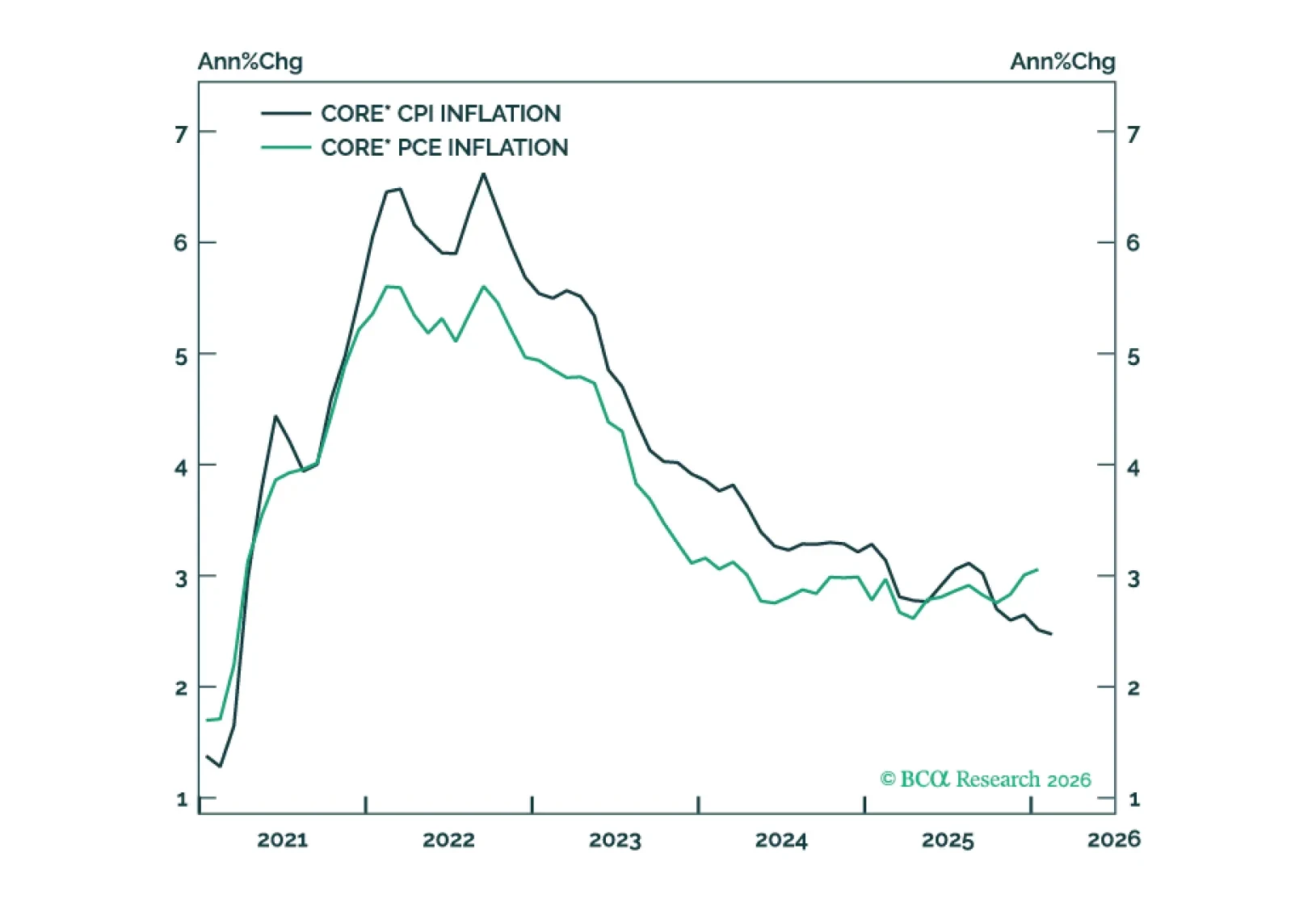

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

The conflict in the Middle East persists as the US and Israel keep striking at Iranian military and internal security sites, and Iran has responded with its own missiles and drones against the Gulf States. Although the pace of Iranian retaliation has declined, it appears to have stabilized, as evidenced by attacks against the UAE.

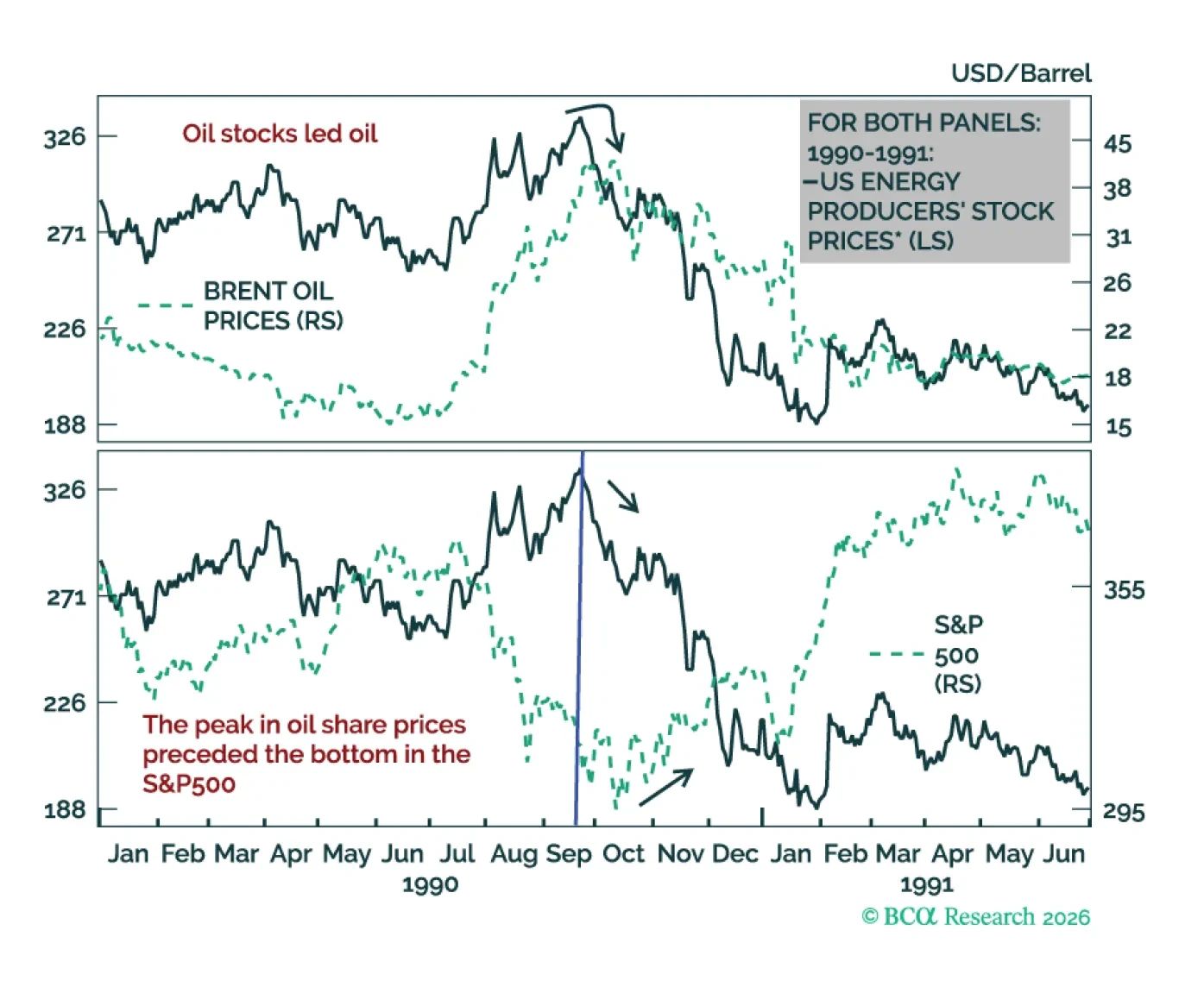

Oil prices will likely rise in the near term, irrespective of developments in the Strait of Hormuz. Given that global share prices have become correlated with crude prices, global stocks will continue selling off. Go short the EM equity index and take profits on our open trades that have benefited from the global risk-on environment.

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.

The war in Iran is disrupting global oil and LNG flows and remains a threat to regional energy infrastructure.

Energy price risks remain skewed to the upside over the near term.