Oil

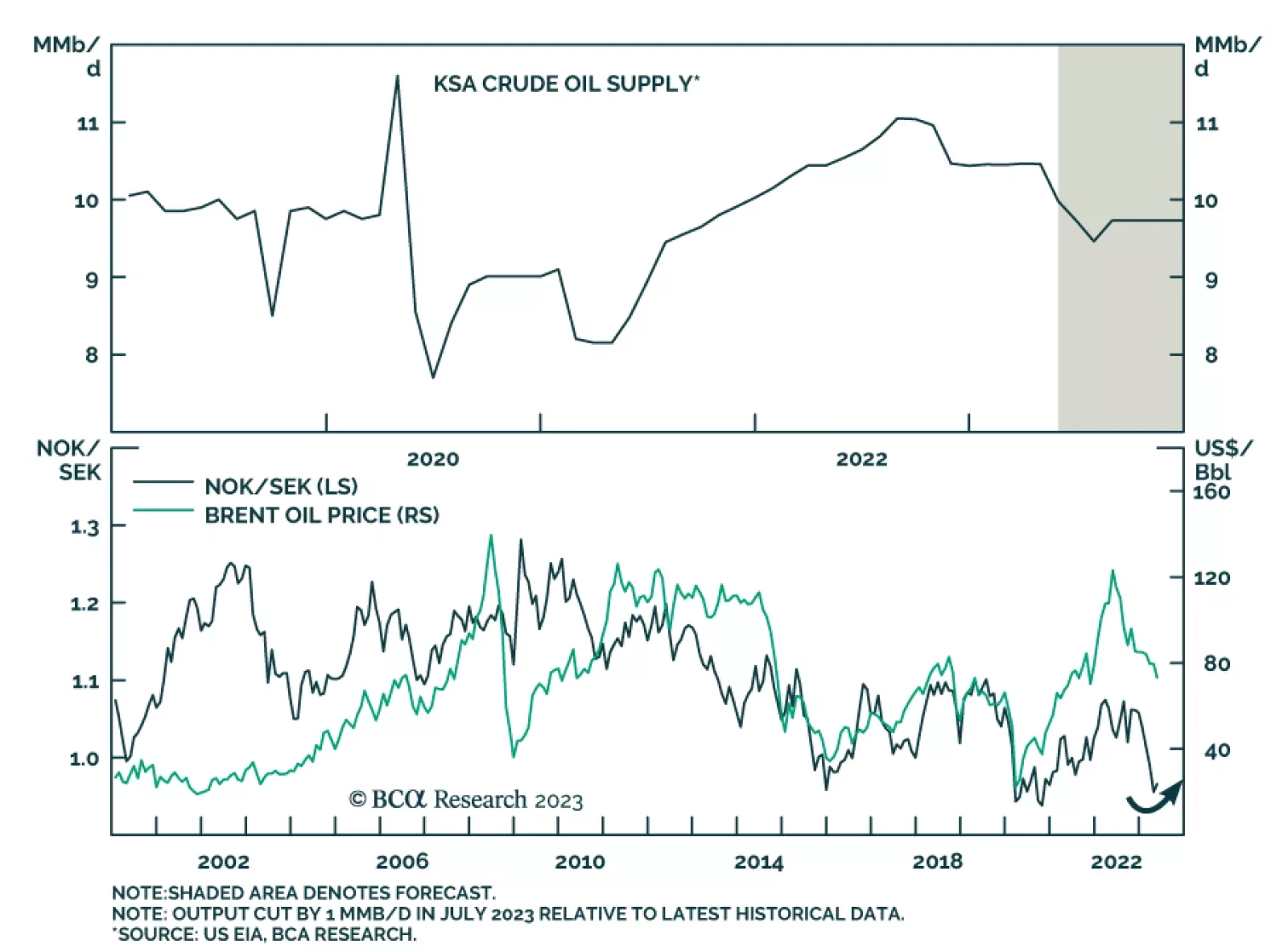

Following this weekend’s OPEC 2.0 meeting, KSA announced a 1mm b/d crude output cut, slated for this July or August, as it attempts to support weak oil prices. The new output quotas, reduced to reflect members’ weak crude oil production will continue until end-2024. UAE’s quota was the only one raised in acknowledgement of its higher production capacity. On the back of this announcement, we continue to expect brent prices will average $90/bbl this year.

Risk assets would perform well over 12 months only if inflation falls to 2% without triggering a recession. That would be unprecedented. We recommend investors stay defensive.

Expectations for oil demand growth through 2023-24 are way too optimistic. Until these expectations fall to -0.5-1 percent, the oil price has further downside. Plus: collapsed complexity confirms that AI is in a mania, while basic materials stocks and ZAR/EUR are rebound candidates.

EM oil demand remains resilient and will continue to be propelled by global growth this year. Supply management by OPEC 2.0 and production discipline outside the coalition will be maintained, forcing inventories lower. Recent price weakness – largely reflecting political uncertainty – has pulled our 2023 Brent forecast down to $90/bbl (from $95/bbl); our 2024 forecast remains at $115/bbl.

The crisis hitting regional and local banks in the US is adding to oil-price volatility and gold demand. The crisis arguably is fallout from the Fed’s aggressive monetary policy tightening, and contributes to the upending economic relationships that reliably informed policy, investments and forecasts in the past. This feeds into higher price volatility, which reduces liquidity in the short run, and impedes capex in the long run, which limits future supply growth.

Pent-up demand for services is keeping the global economy going, but we still expect recession over the next 12 months. Investors should keep a cautious portfolio stance.

The Gulf’s political economy – particularly that of KSA – drives the supply side of oil-price discovery. This has been evolving since 2017, when OPEC 2.0 was formed. It is now fundamental to the market. We expect Brent to average $95/bbl this year, unchanged from last month, and $115/bbl (up $5/bbl vs. last month). WTI will trade $4-$6/bbl below Brent over the forecast interval. We remain long the XOP and COMT ETFs.

Bullish equity sentiment may persist in the second quarter on the Fed’s pause, but tight monetary policy, financial instability, elevated recession odds, extreme US polarization and policy uncertainty, and still-high geopolitical risk should encourage investors to maintain a defensive position for the coming 12 months.

The OPEC 2.0 supply cuts announced over the weekend will be fundamentally bullish international crude oil prices. According to our model, brent will cross the USD 100/bbl mark by August this year. We believe the cohort is pre-emptively cutting oil supply in response to threats to their economic interest, including risks arising from the higher possibility of recession and rising market volatility following the banking crisis.