Money/Credit/Debt

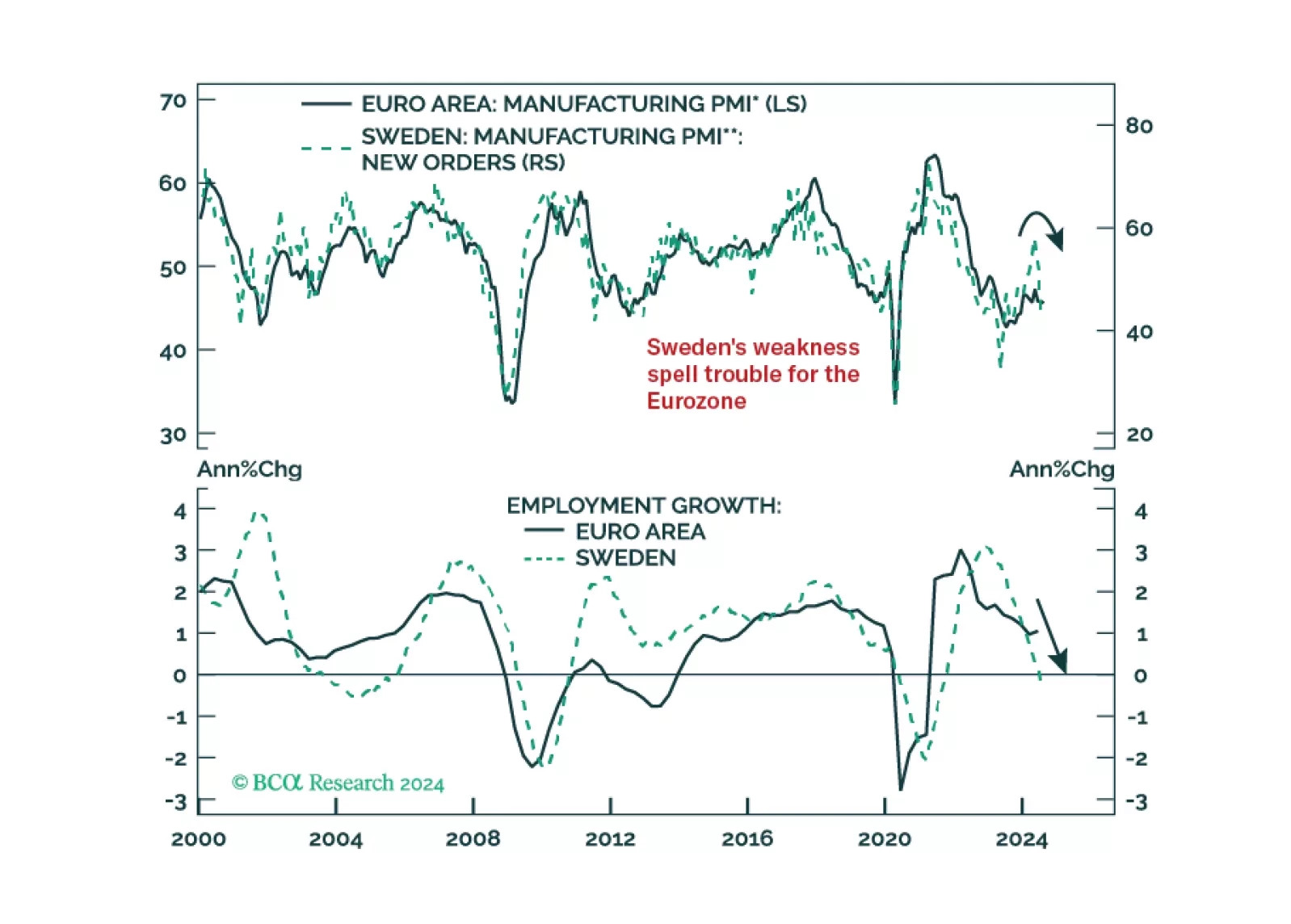

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

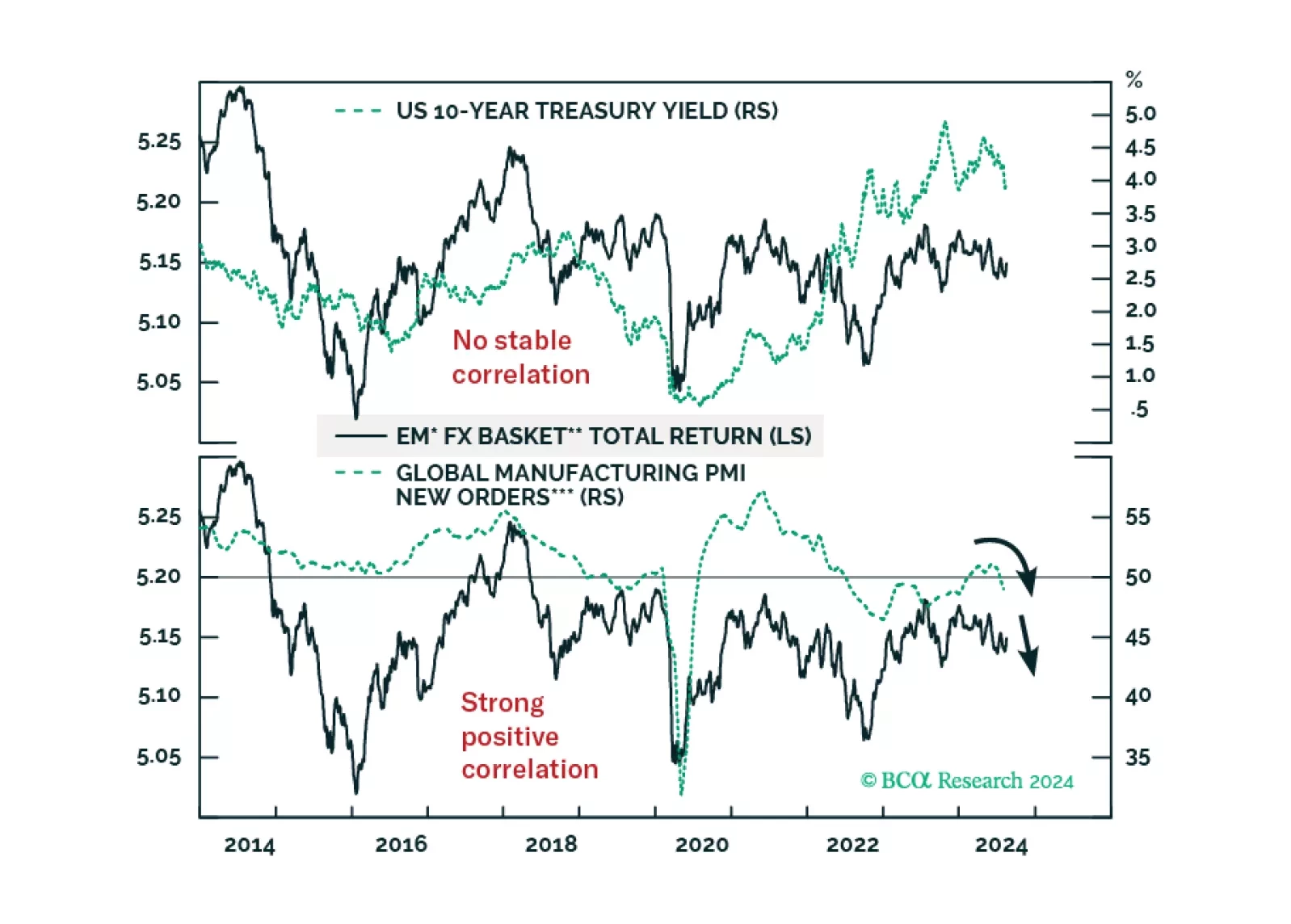

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

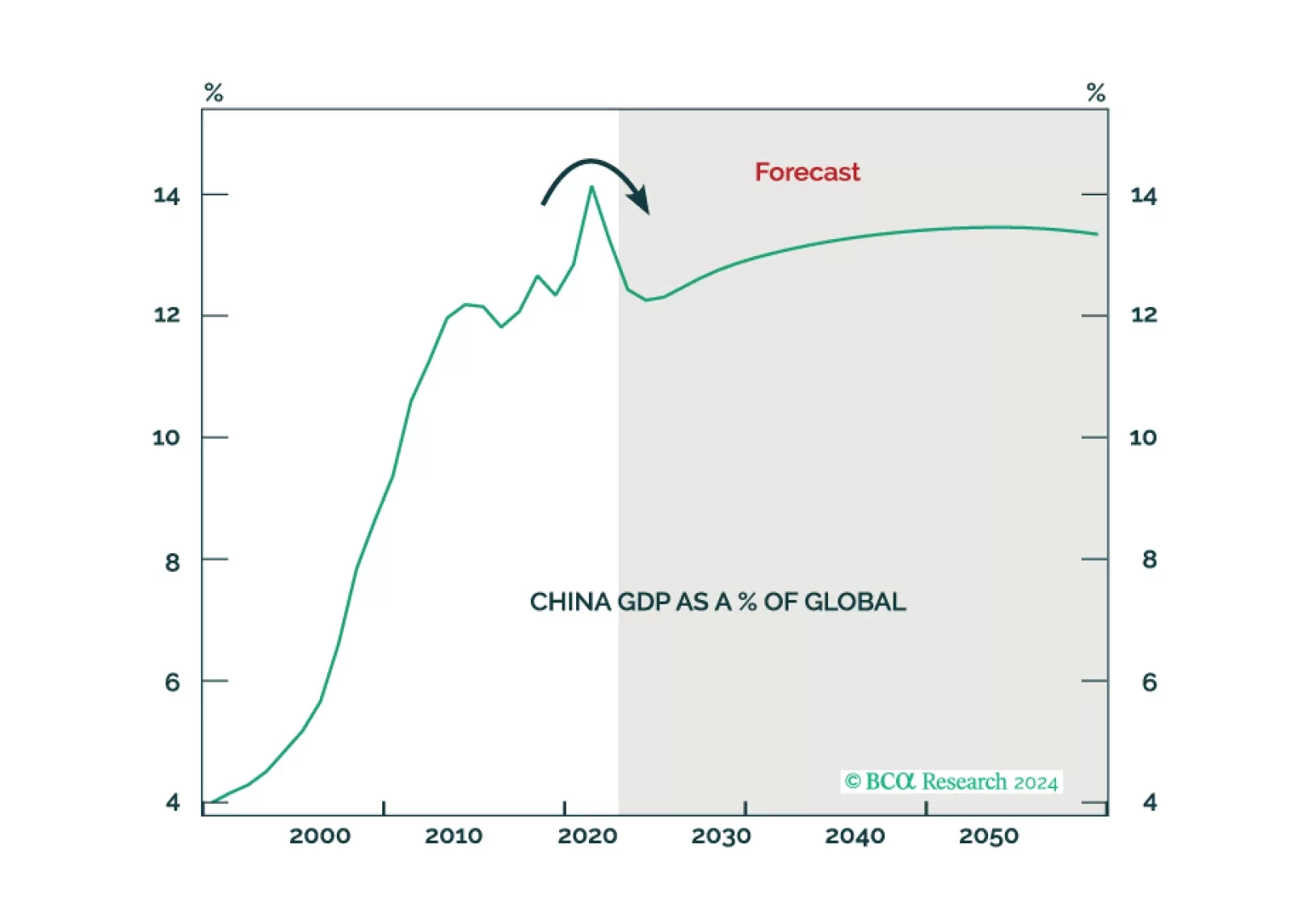

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

The market backdrop changed a lot between the preparation and the publication of our equity downgrade report. We publish this companion Insight to help investors navigate the new environment.