Monetary Policy

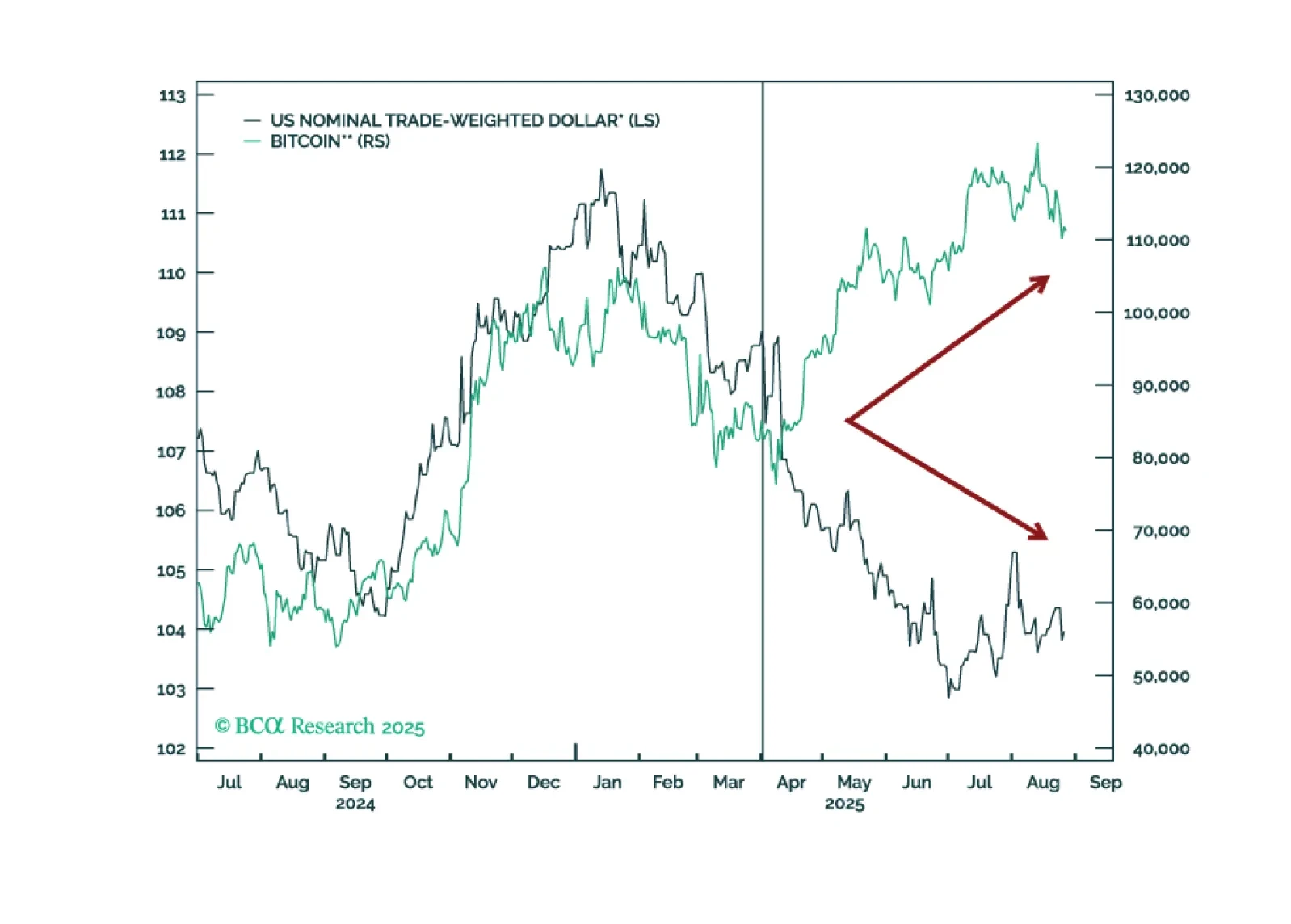

In Section II, Chester reviews the outlook for stablecoins, cryptocurrencies, and central bank digital currencies.

In Section I, Doug notes that a negative stance toward stocks will require a meaningful and imminent deterioration in the US macro data given the ongoing impact of AI optimism on the global equity market. In Section II, Chester reviews the outlook for stablecoins, cryptocurrencies, and central bank digital currencies.

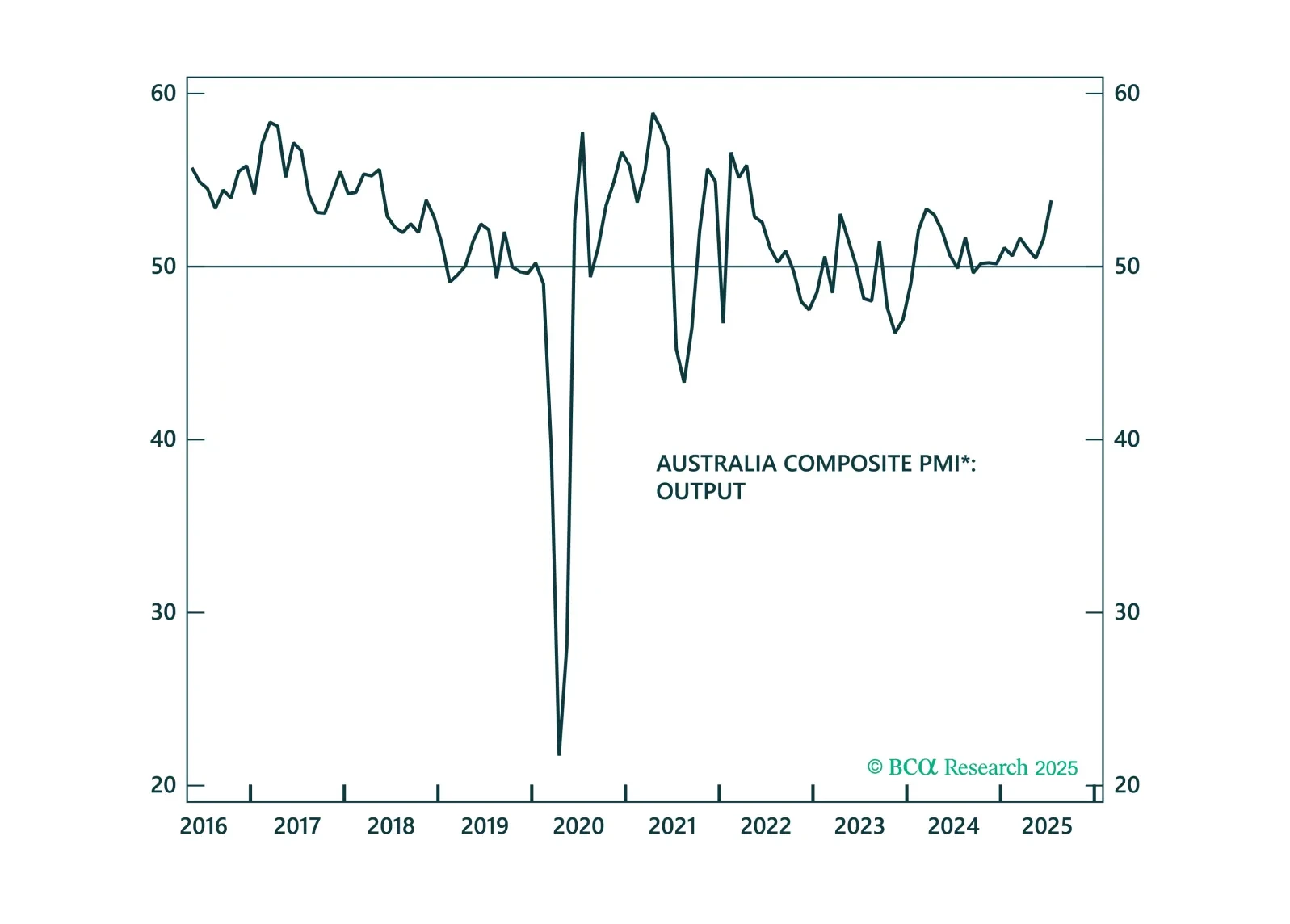

In a widely anticipated move, the RBA resumed cutting rates. However, with housing, consumption, and PMIs improving, we see little scope for the RBA to ease beyond market expectations.

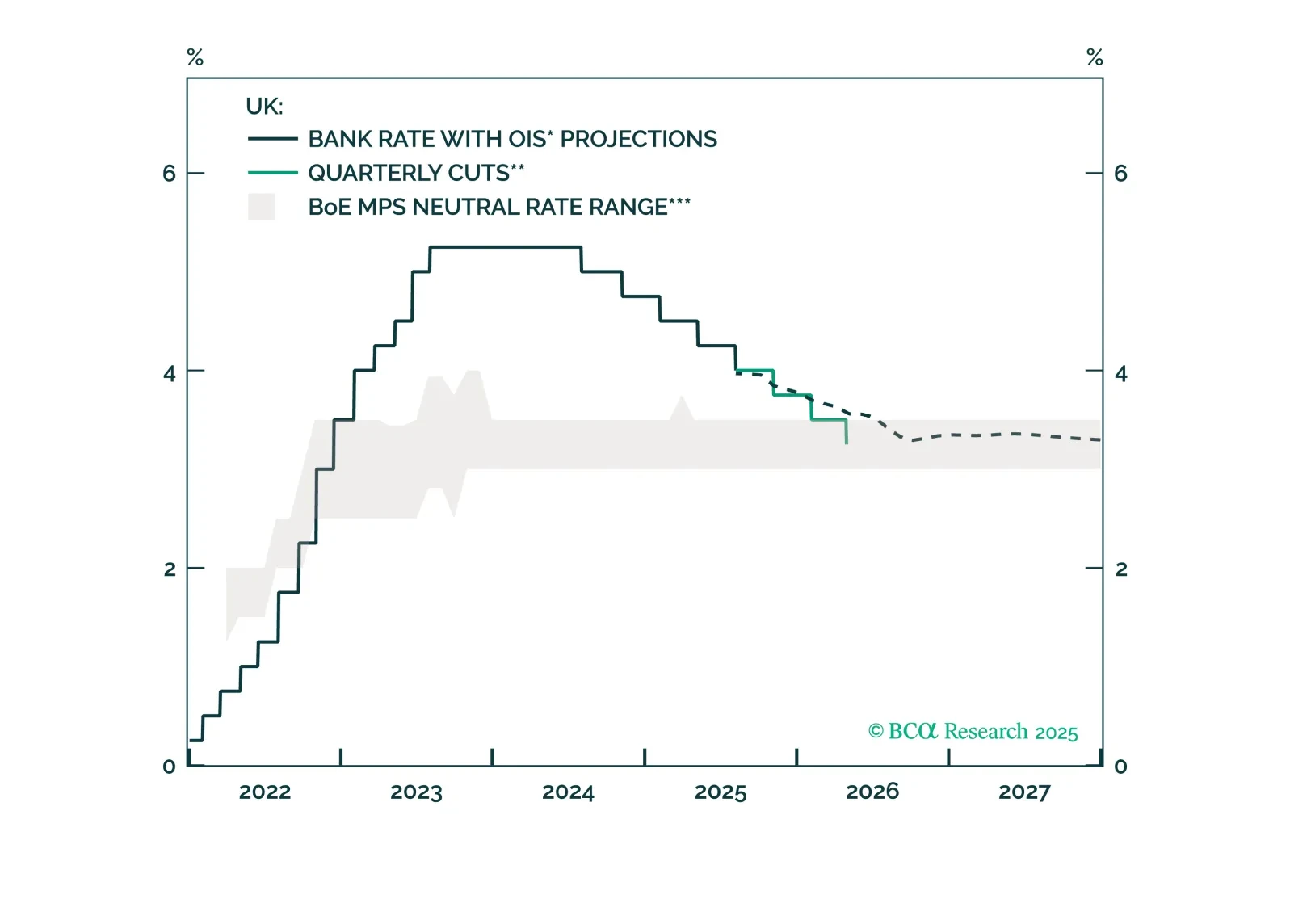

The BoE is easing, but risks falling behind. Labor and growth cracks are starting to emerge, and the Bank may soon be forced to move more decisively. This report outlines why gilts remain a buy and sterling’s path is diverging vs. USD and EUR.

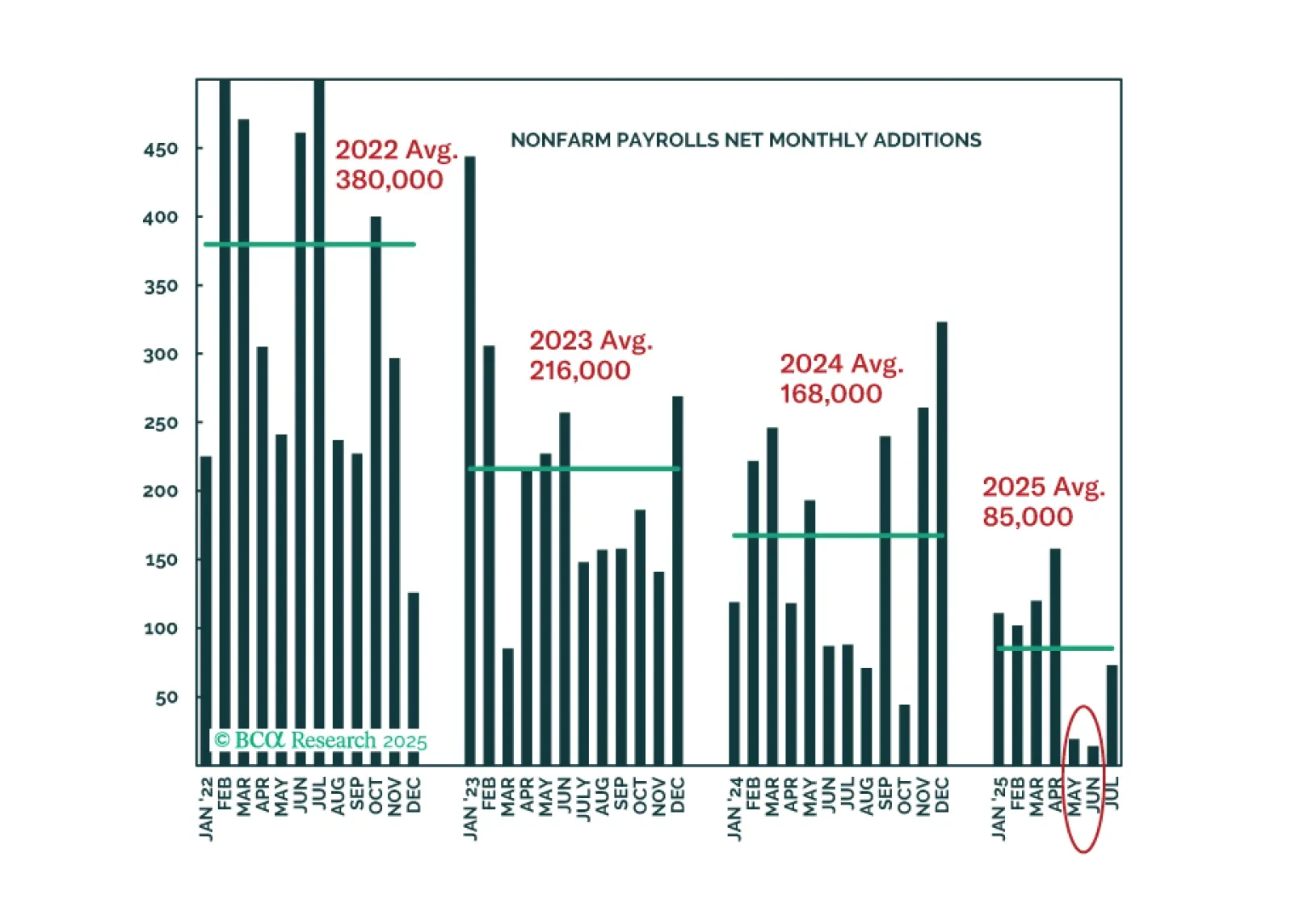

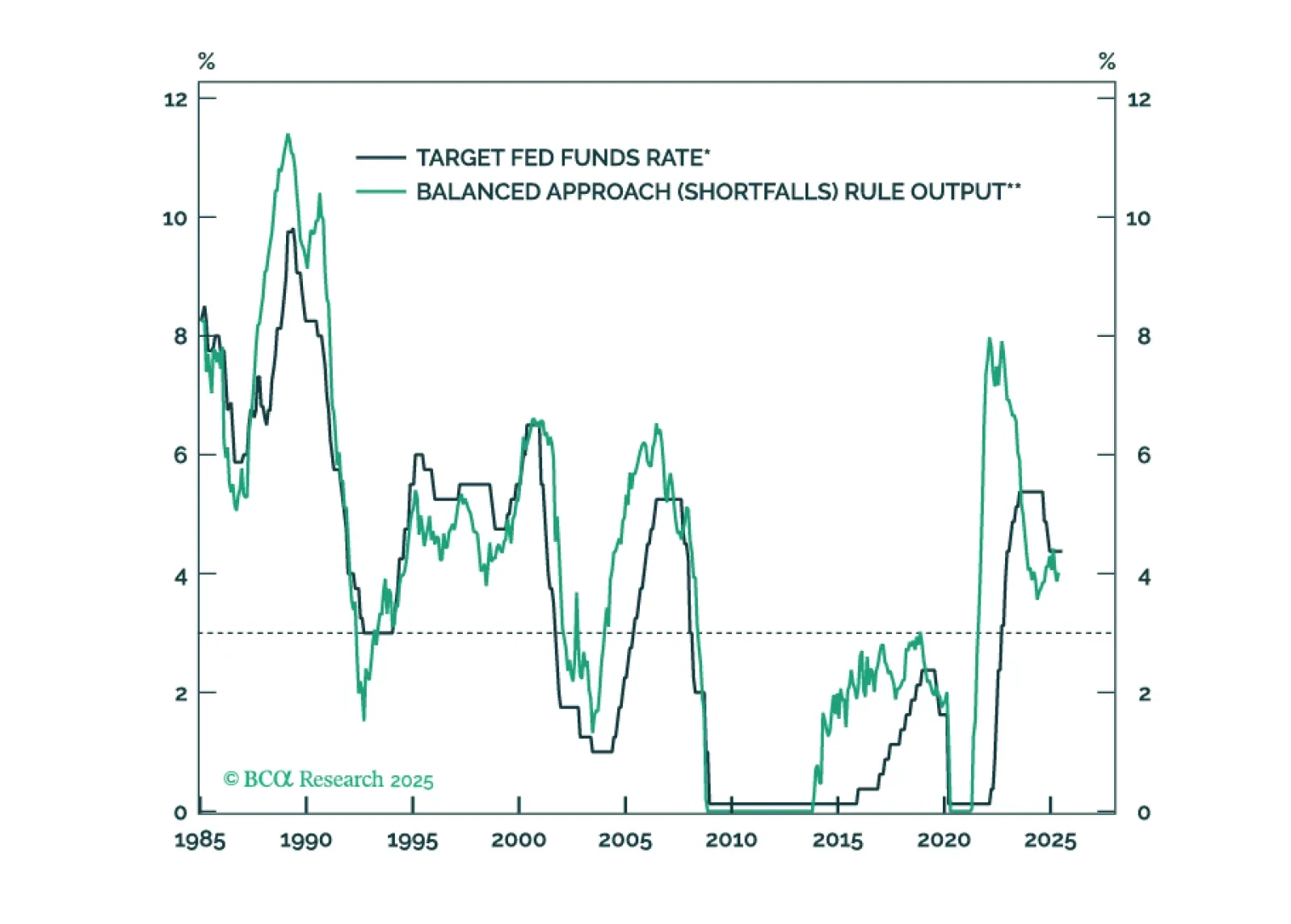

The Fed will keep rates on hold until the unemployment rate forces its hand.

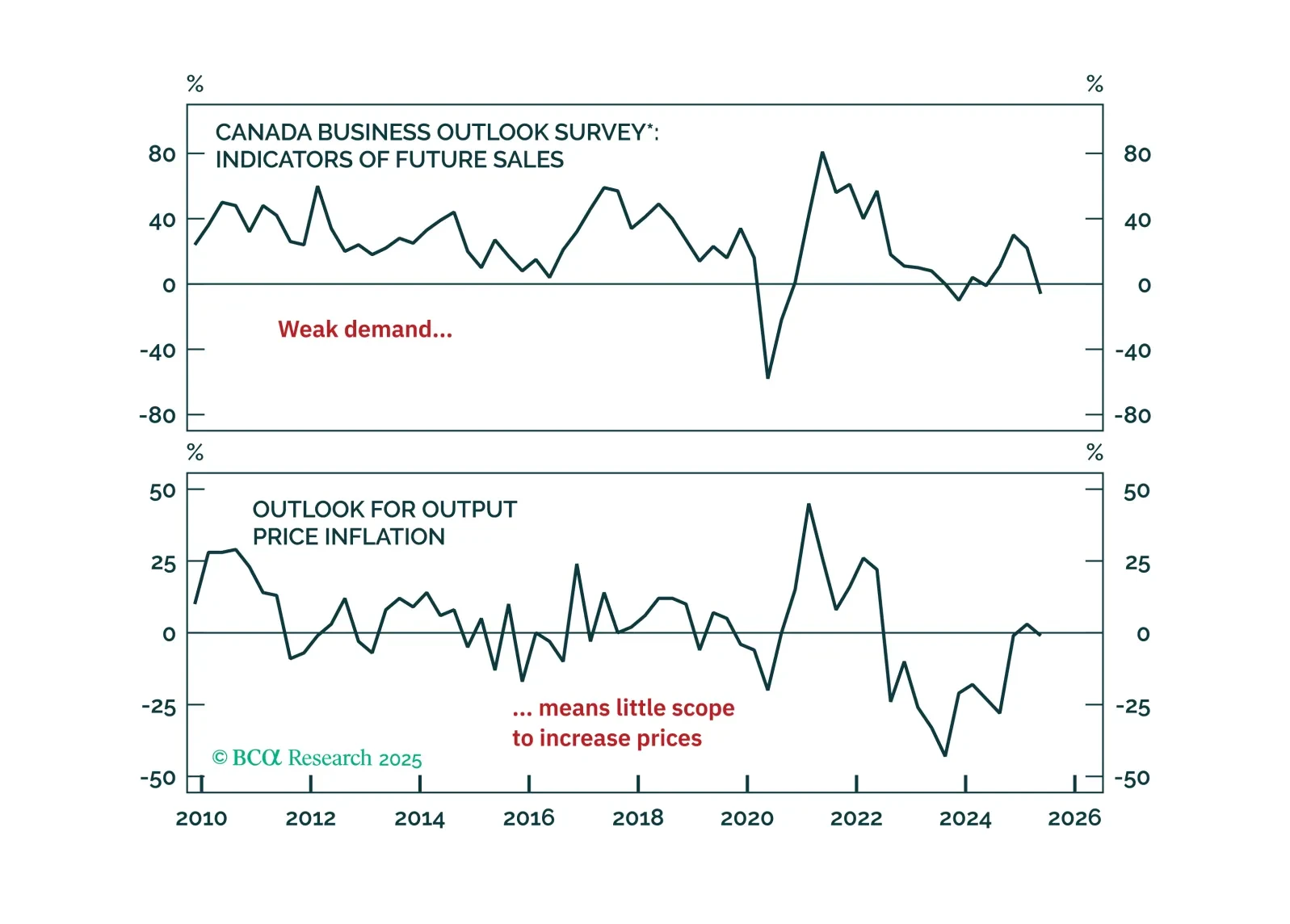

The Bank of Canada continues to hold its policy rate amid trade uncertainty and shows little concern about the potential economic damage from tariffs. We judge the risks differently and view a bet on more rate cuts this year as attractive.

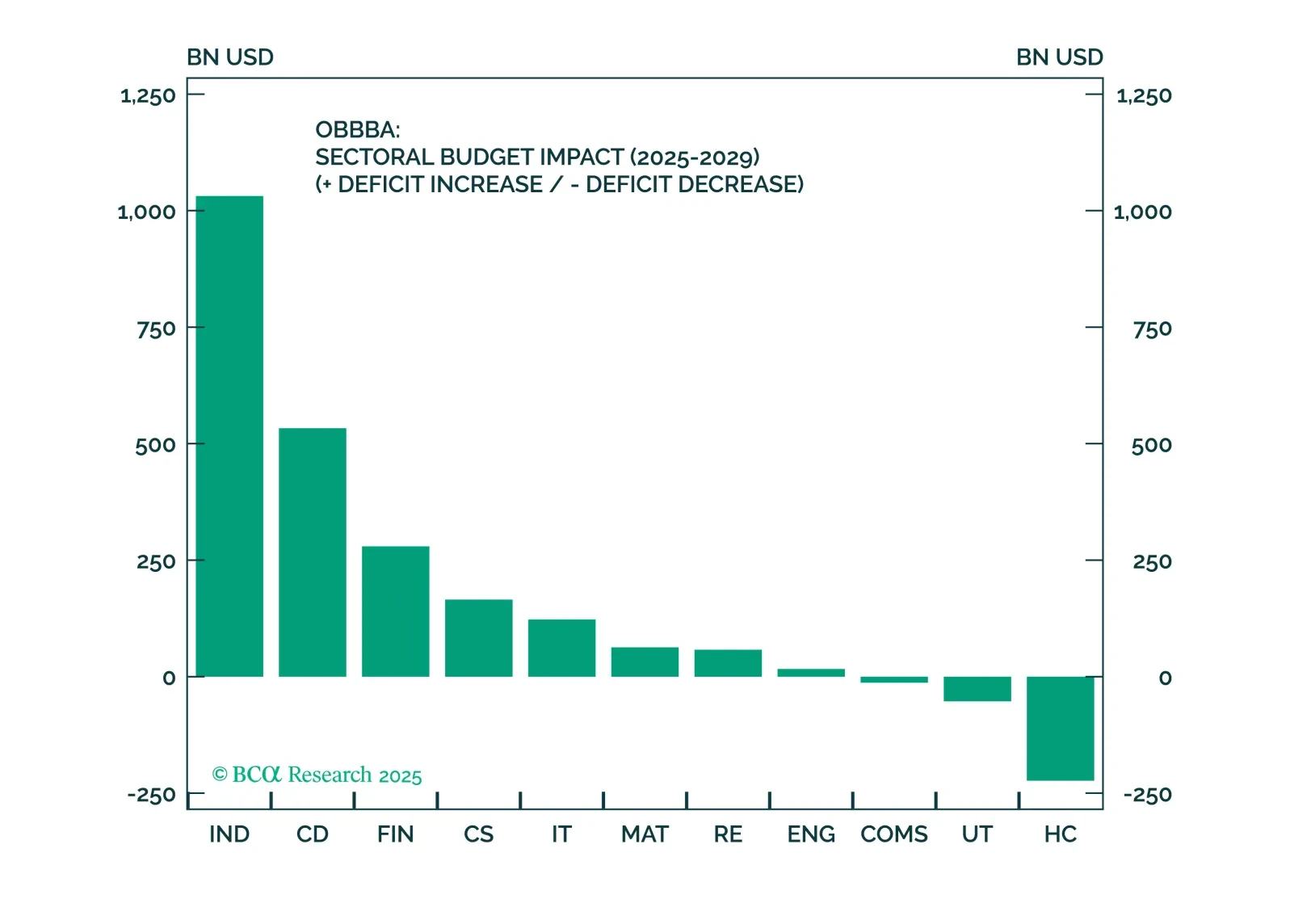

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

We still believe a recession looms, but it has yet to rear its ugly head. We continue to recommend investors position defensively, but we will change tack if clear signs of a recession don’t emerge soon.

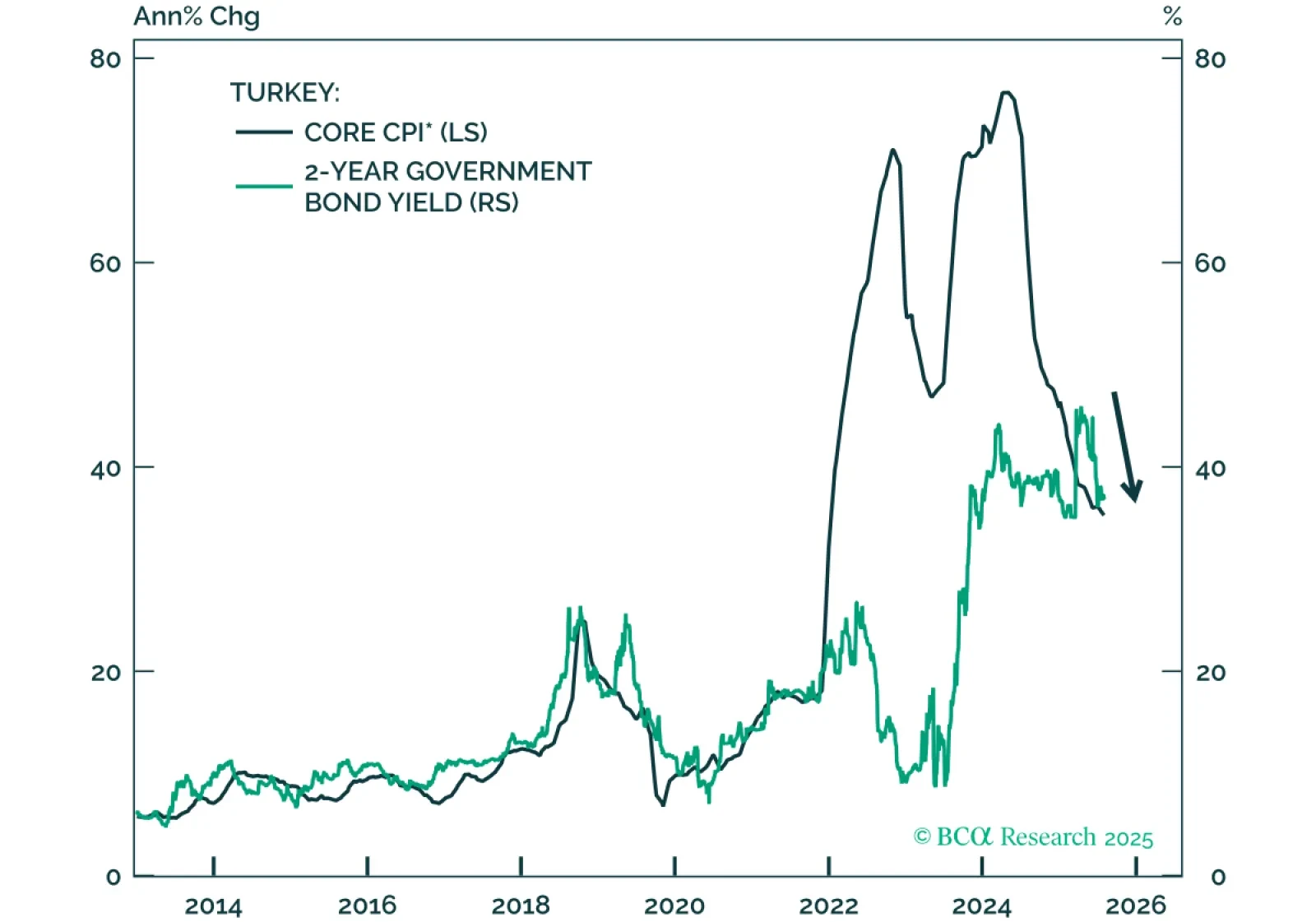

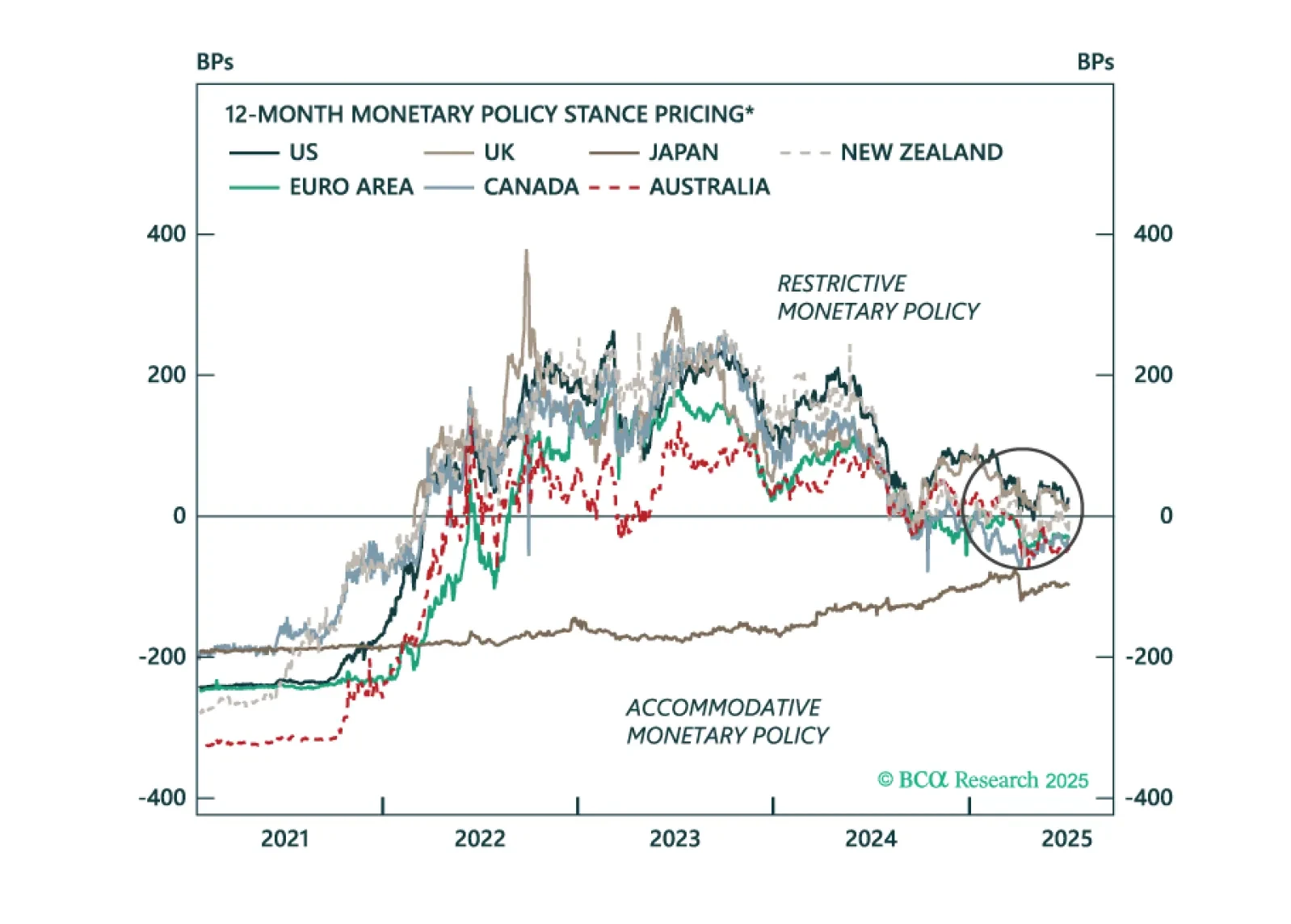

Markets are pricing a return to a neutral policy stance for the major central banks within the next 12 months. However, recession risks still loom amid slowing growth. We unpack where recession risks are underappreciated and what it means for bond positioning.