Monetary Policy

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

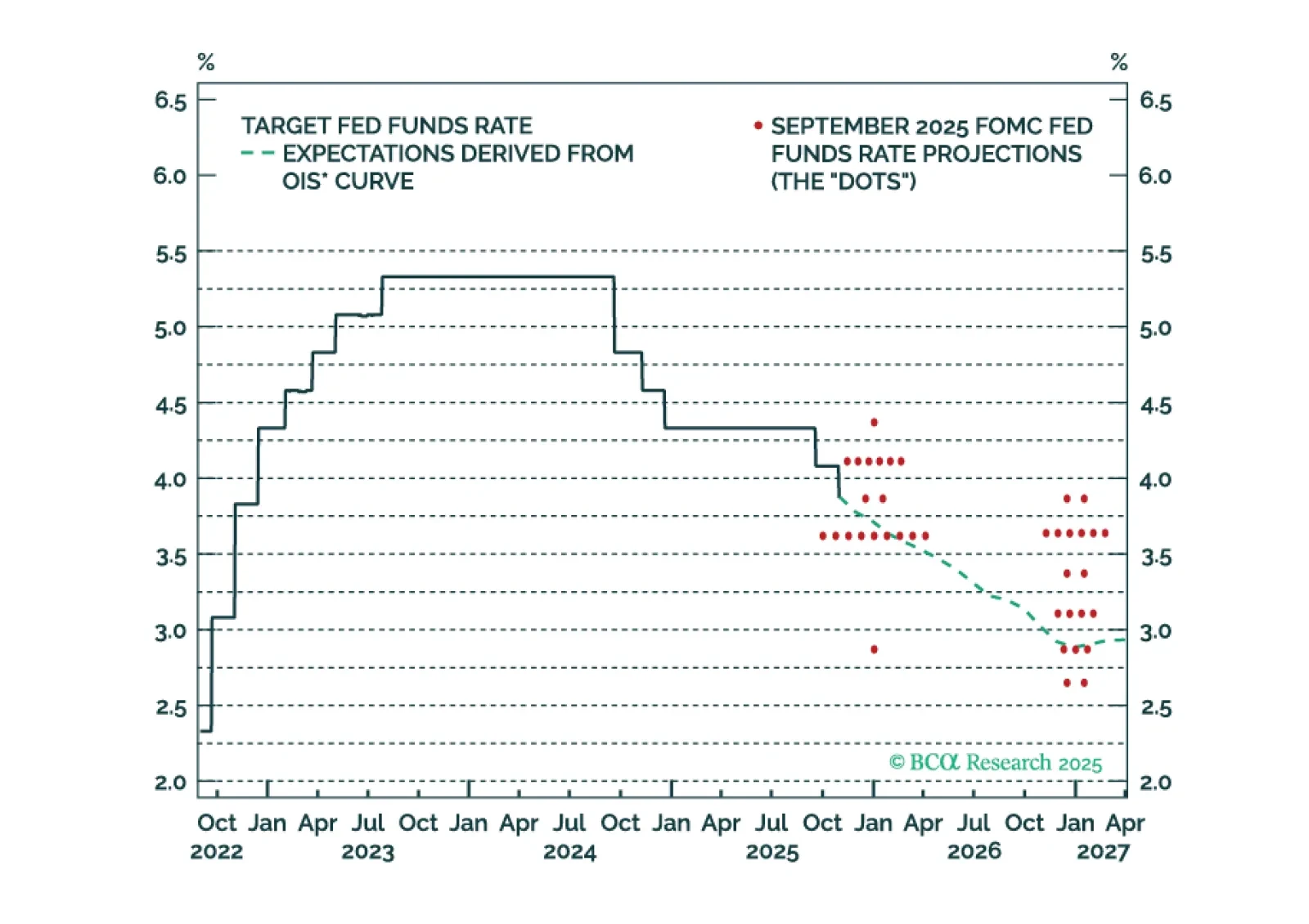

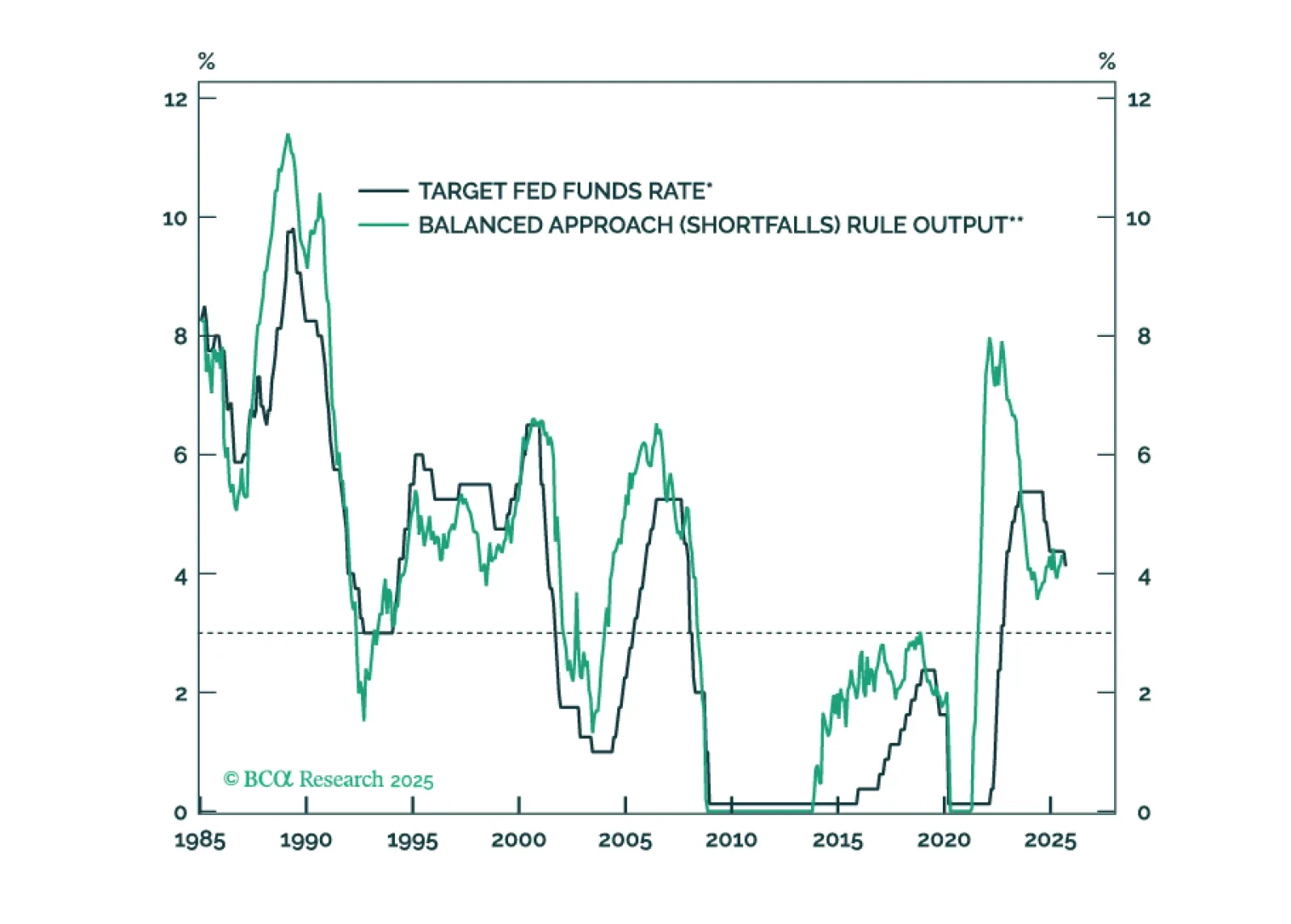

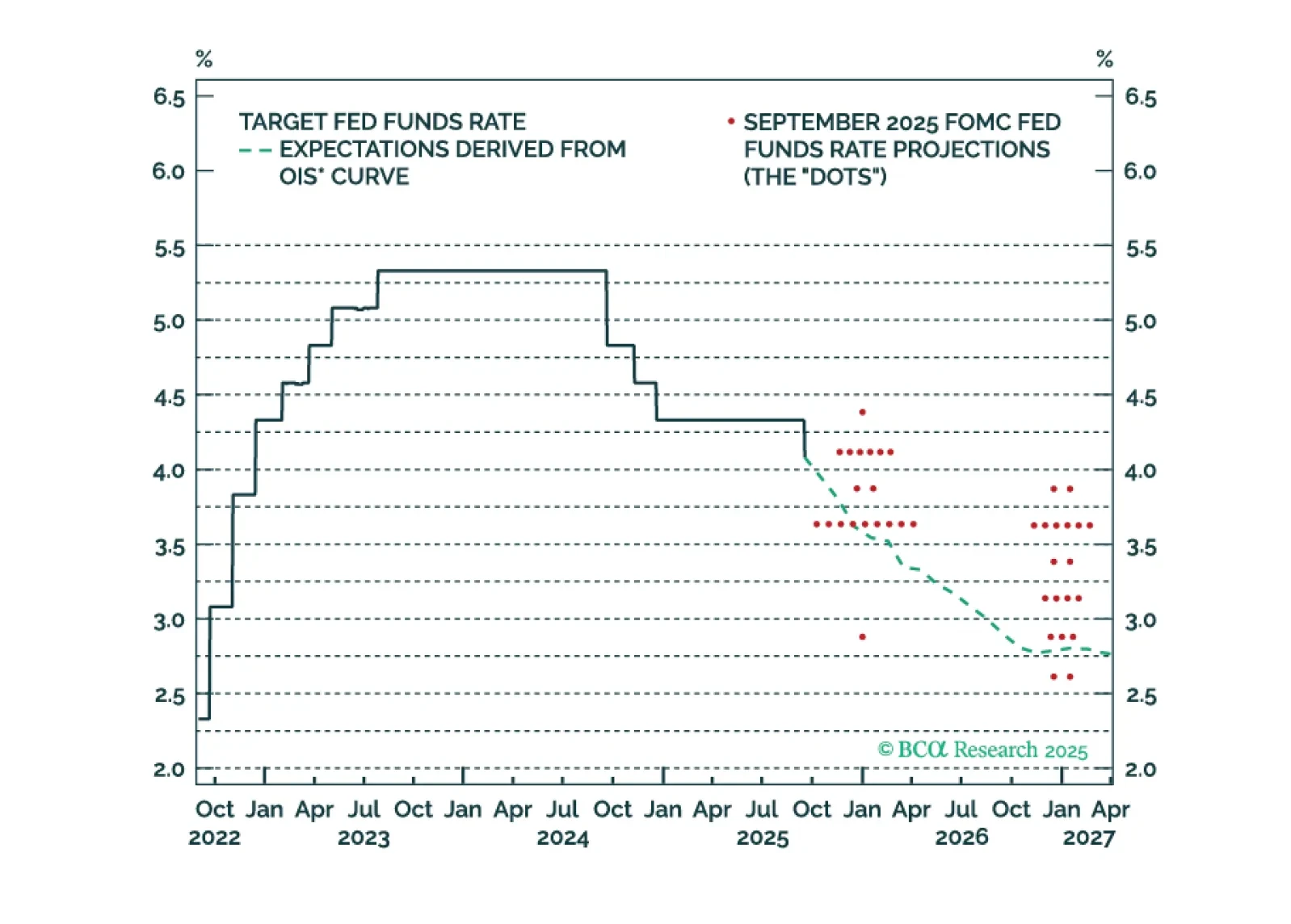

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

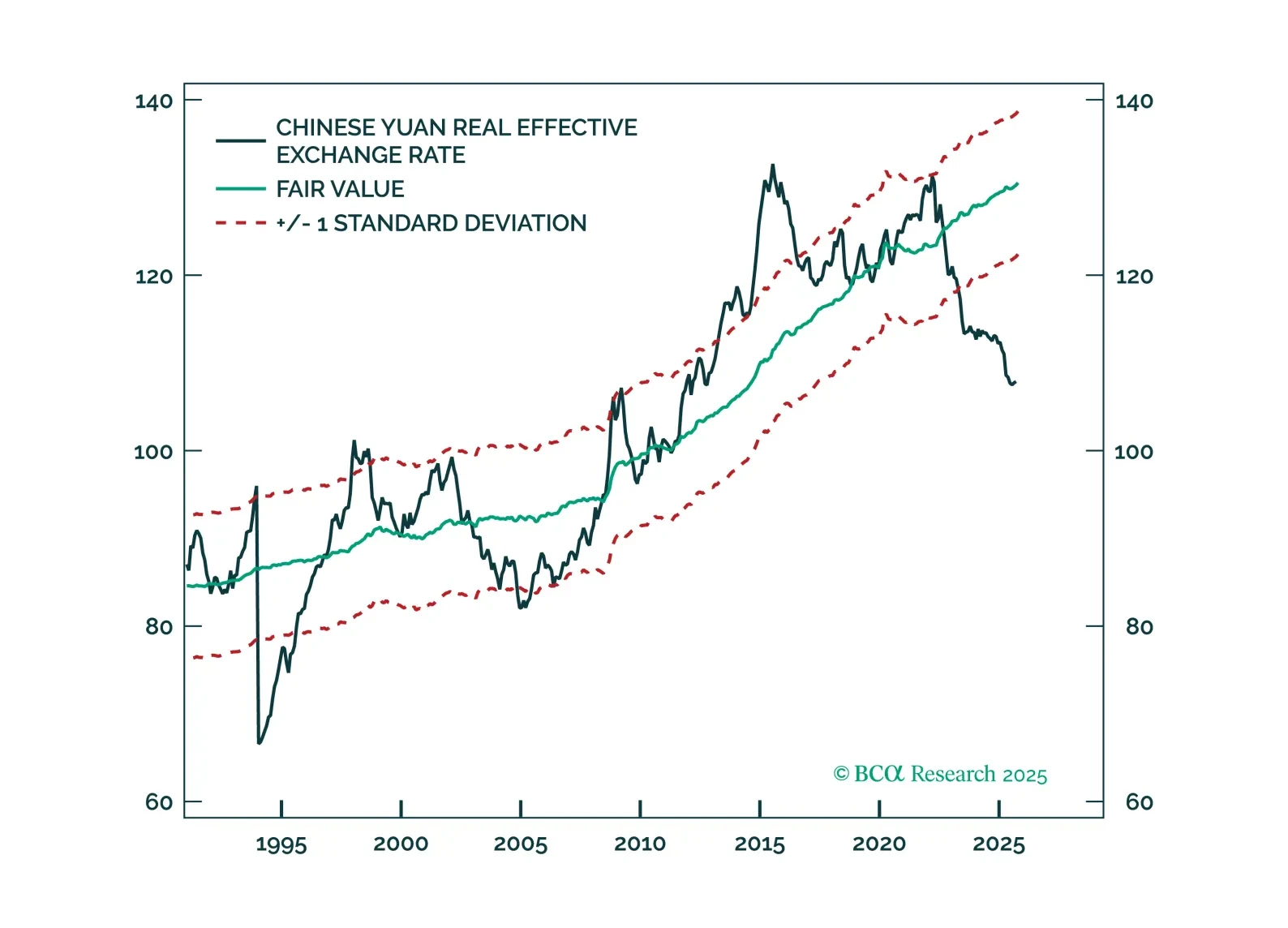

Beijing’s quiet pivot toward RMB strength and a deep valuation discount set the stage for a multi-year appreciation. Our latest FX Insight explores why we see the CNY rising to 6.5–6.8 versus the USD over the next year.

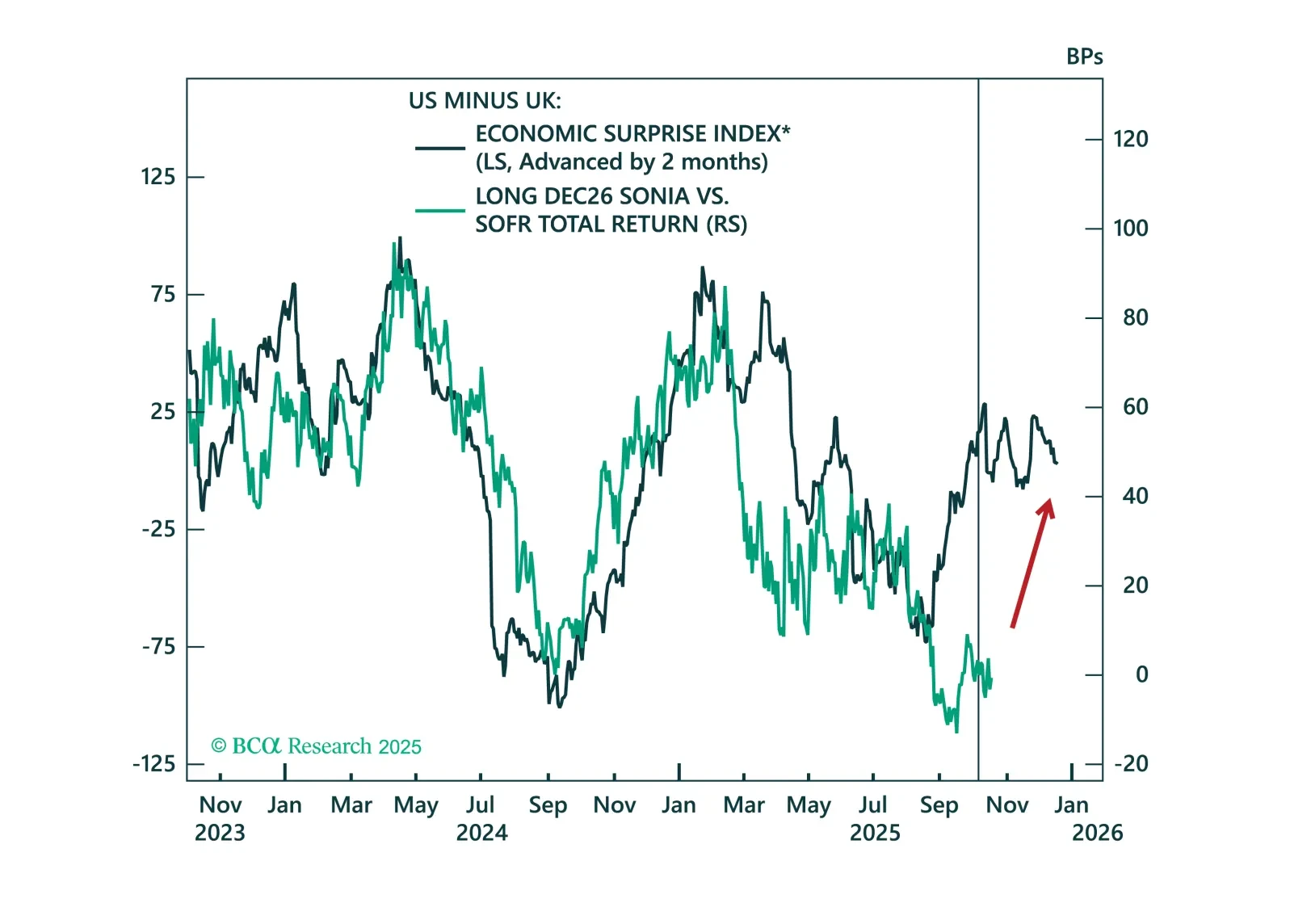

Same policy rate, very different expectations. We break down why policy convergence between the Fed and BoE is THE fixed income trade for year-end.

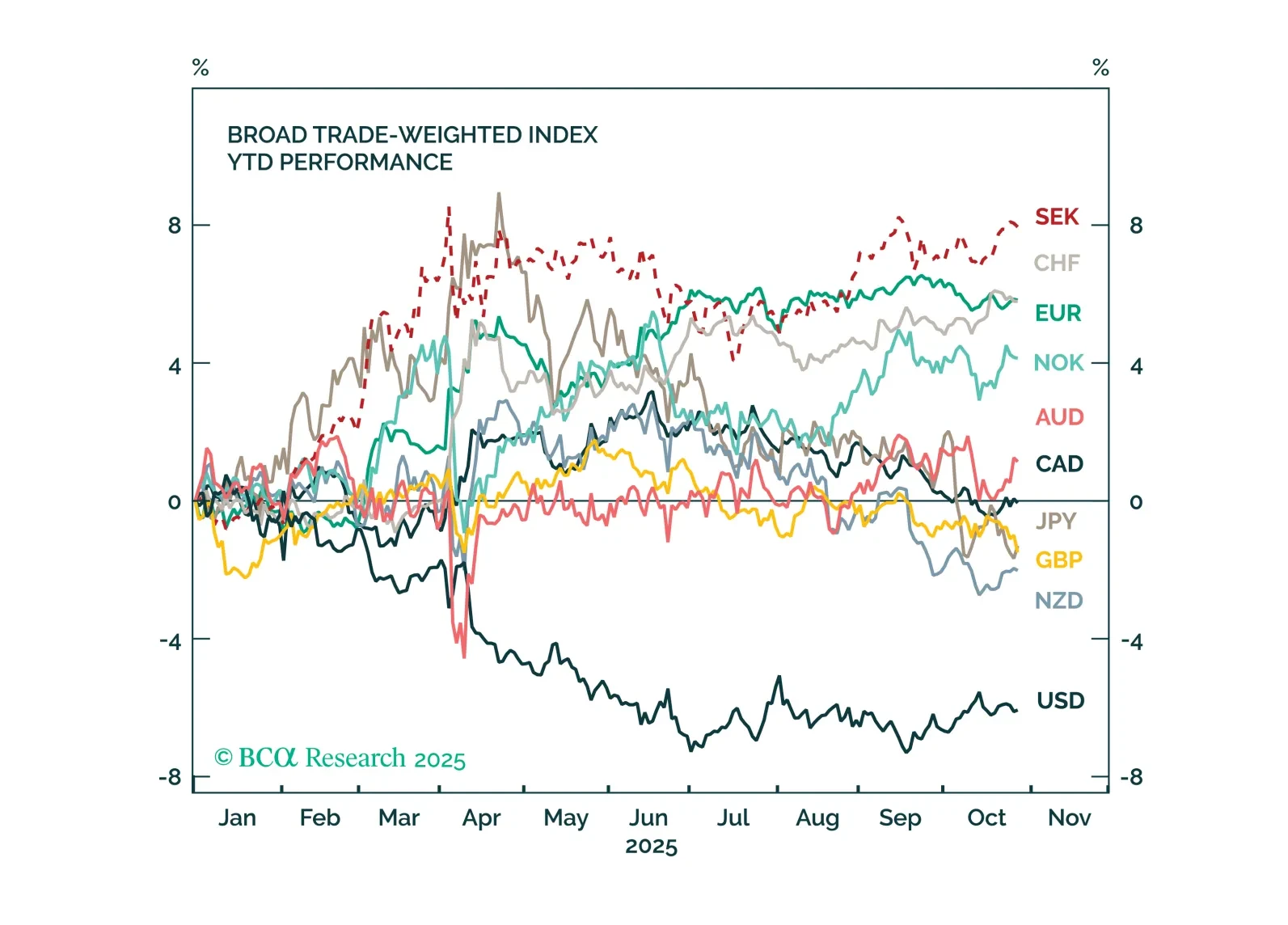

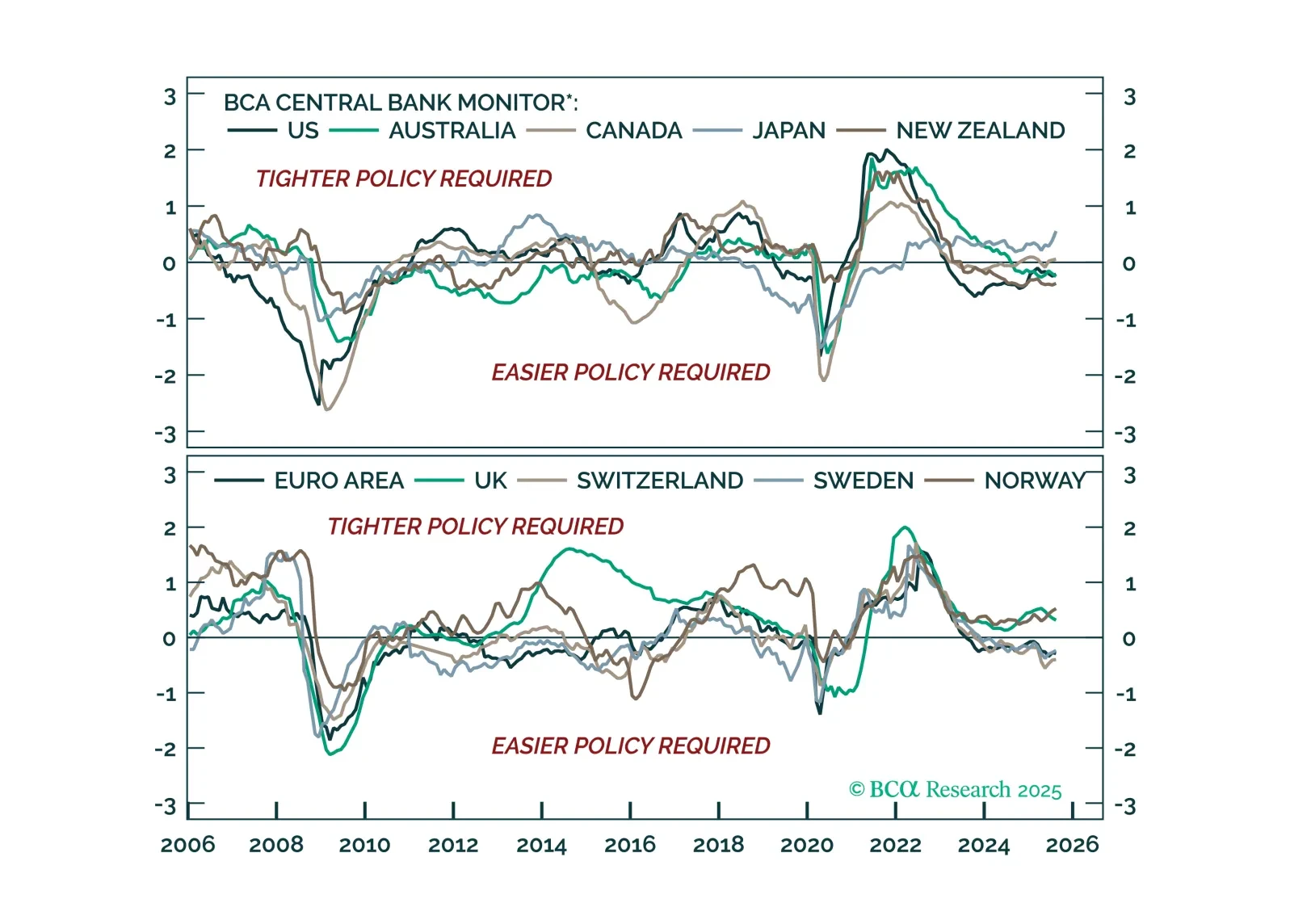

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

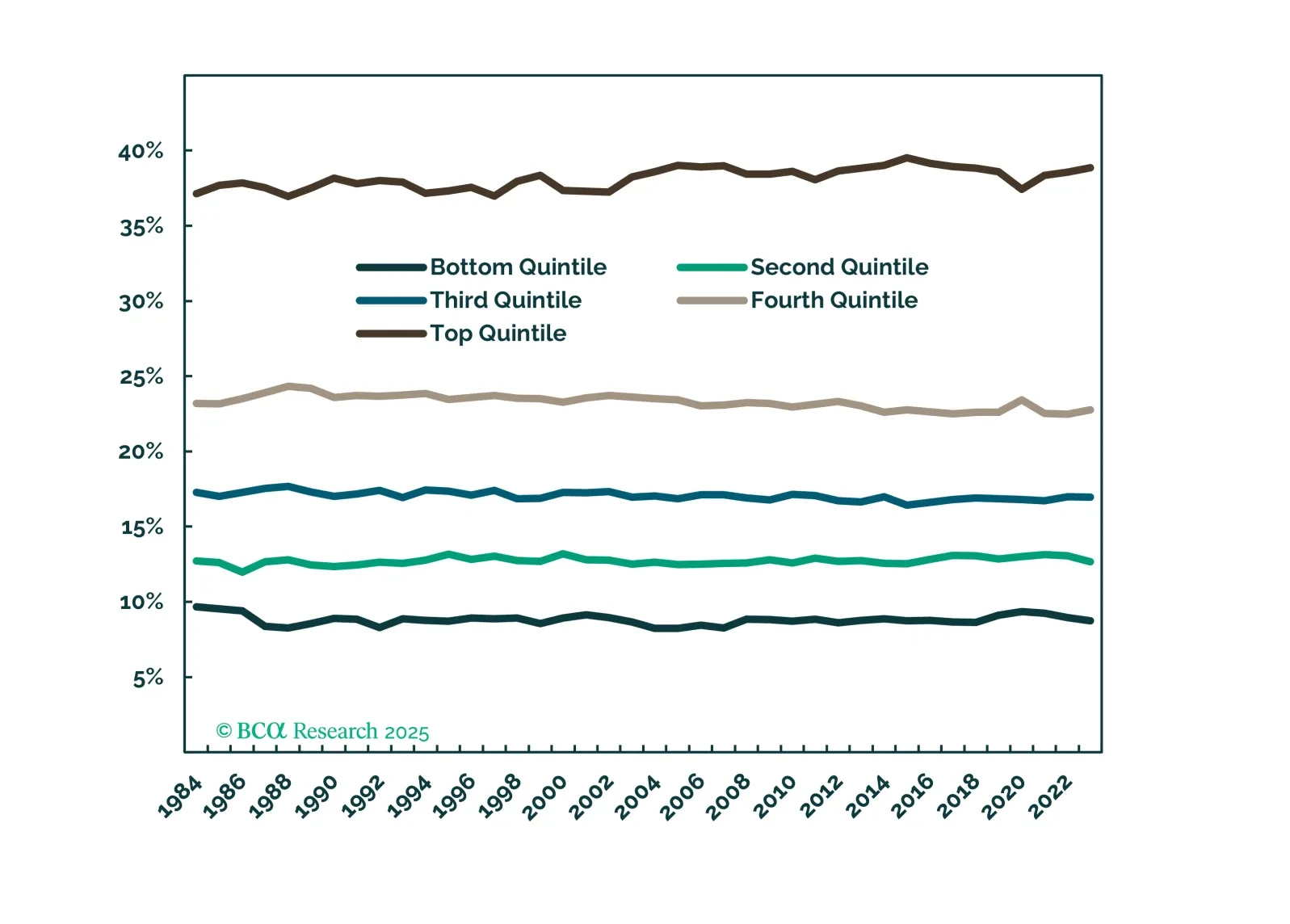

While it is not yet time to bet against risk assets, we push back on the increasingly popular ideas that the wealthiest households and/or AI-related capex can keep the expansion going despite the wobbling labor market.

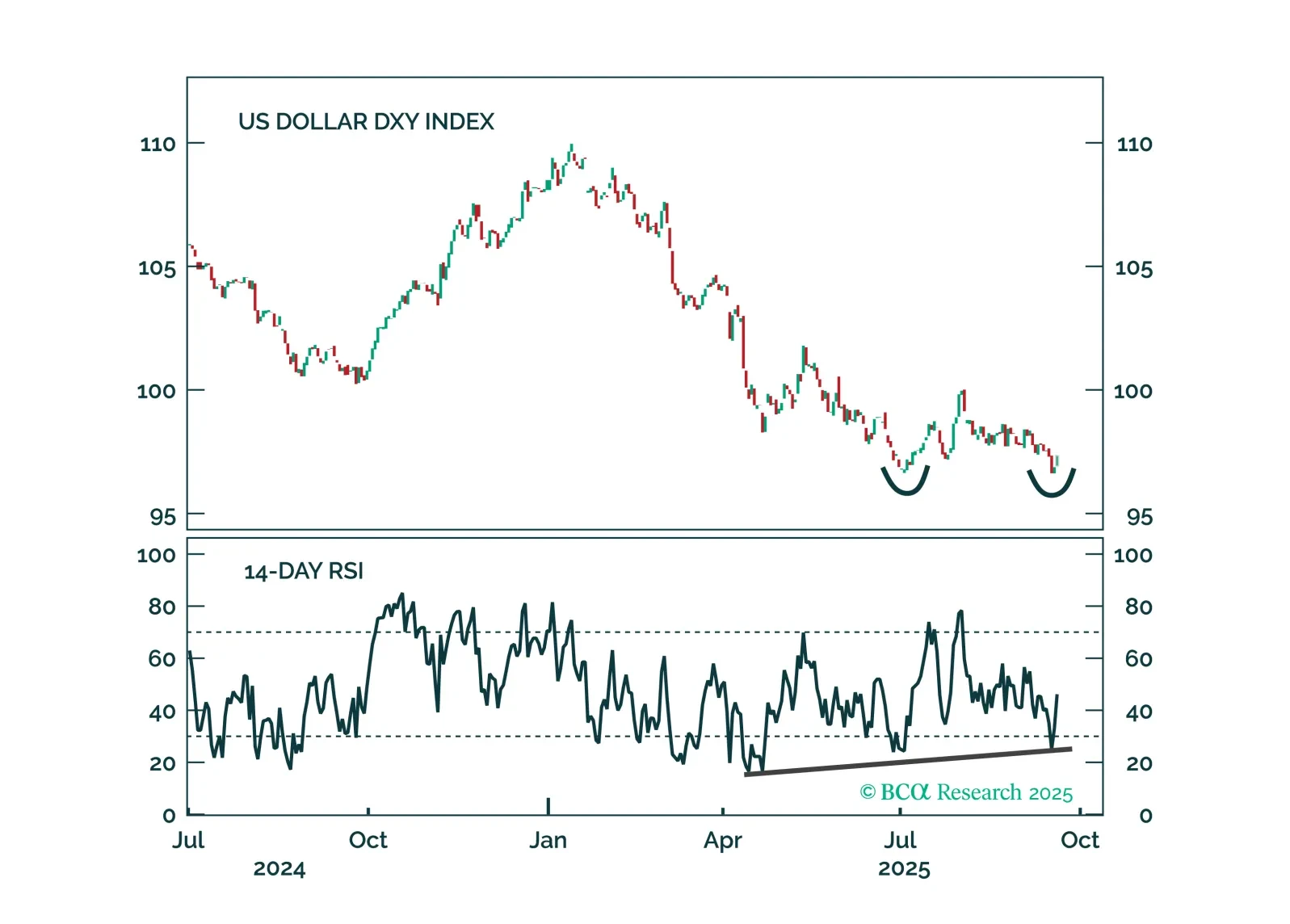

The Fed is mispriced for the rest of 2025. We explain why the dollar is poised to rebound and the trades to position for it.

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

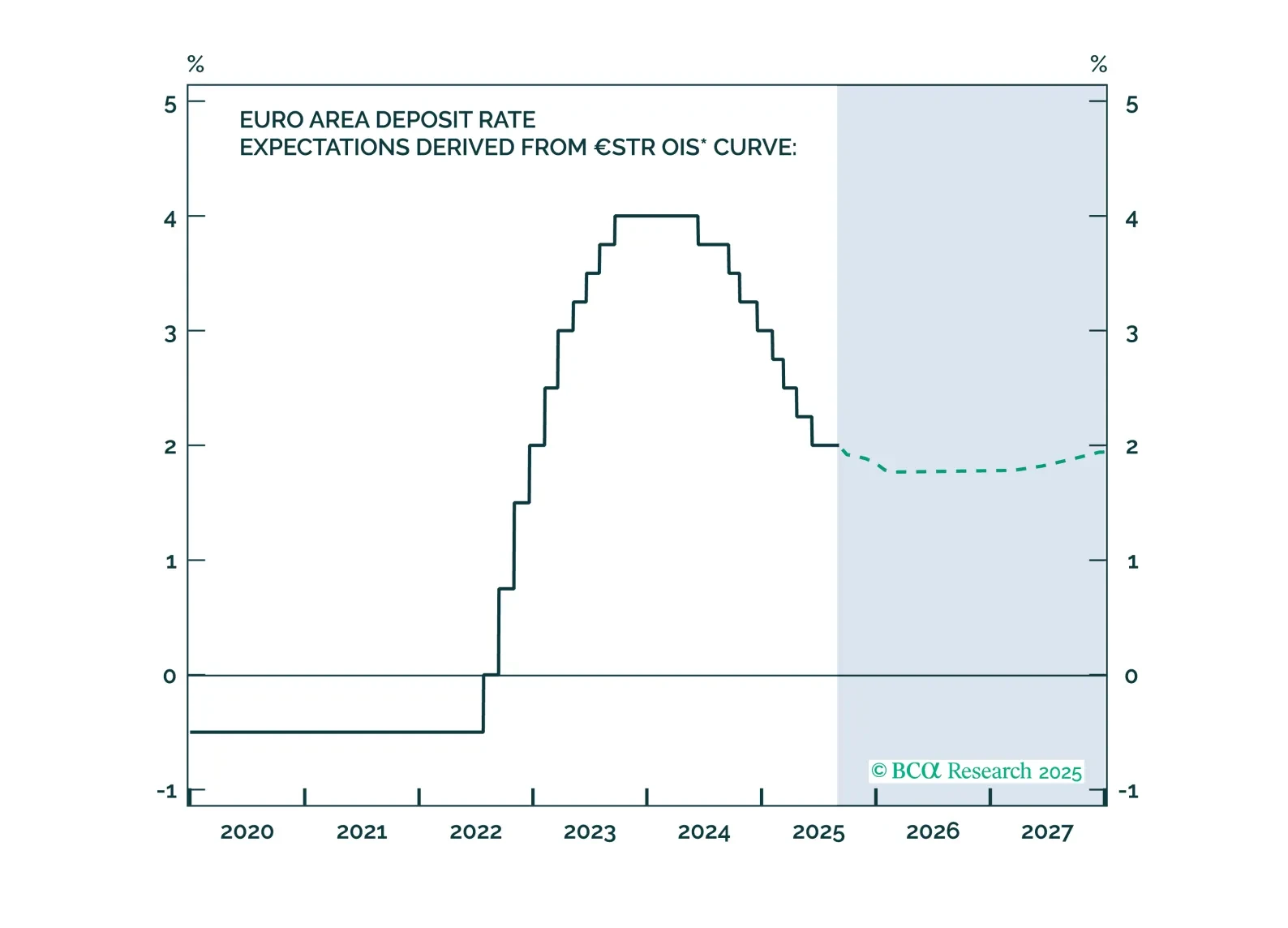

The European Central Bank has achieved a soft landing. Inflation is back to target, with well-anchored inflation expectations. The unemployment rate is historically low, and real economic growth is stable, albeit weak. Given that little to no additional easing will come from the ECB, investors should underweight government bonds relative to equities.