Monetary Policy

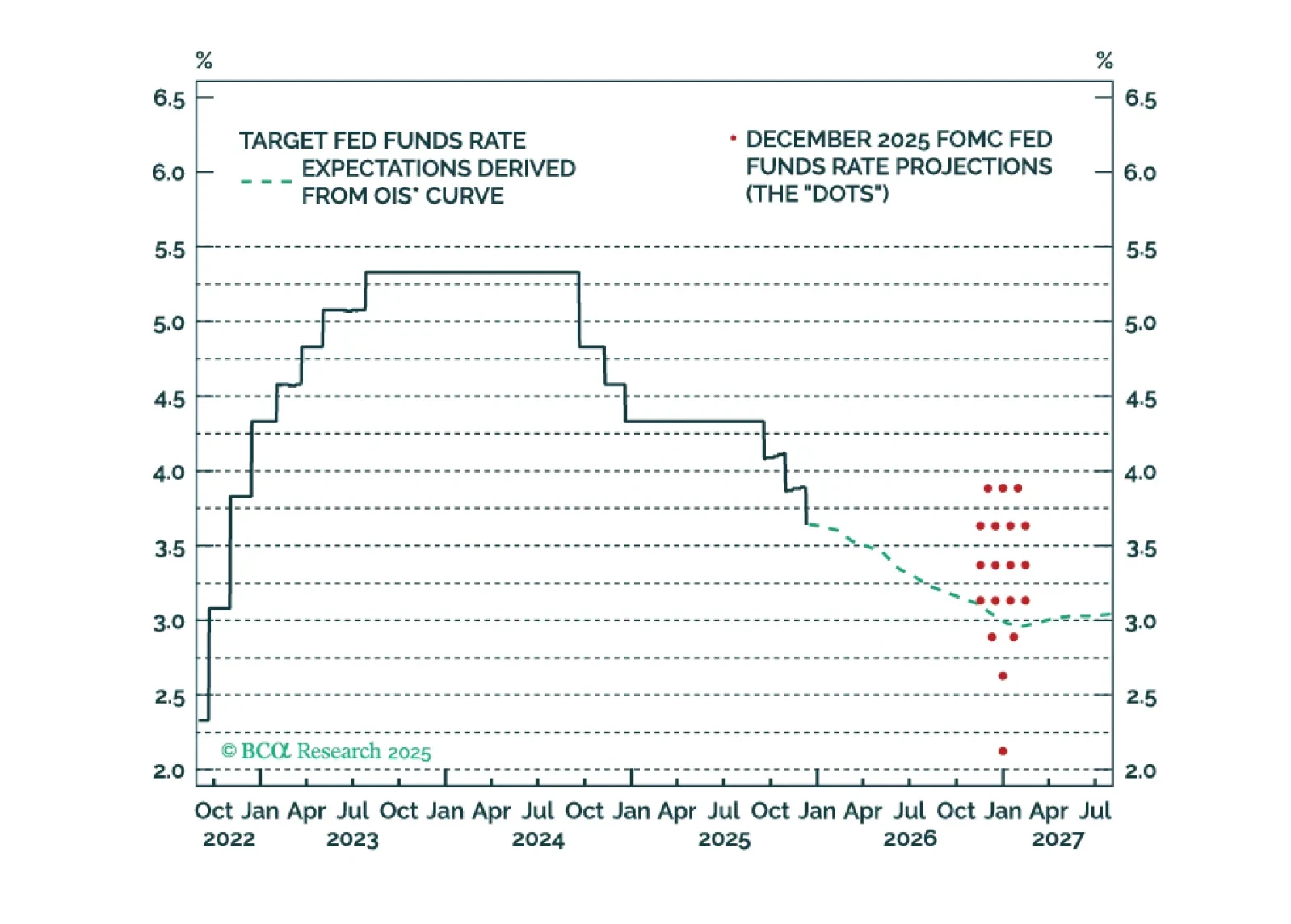

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.

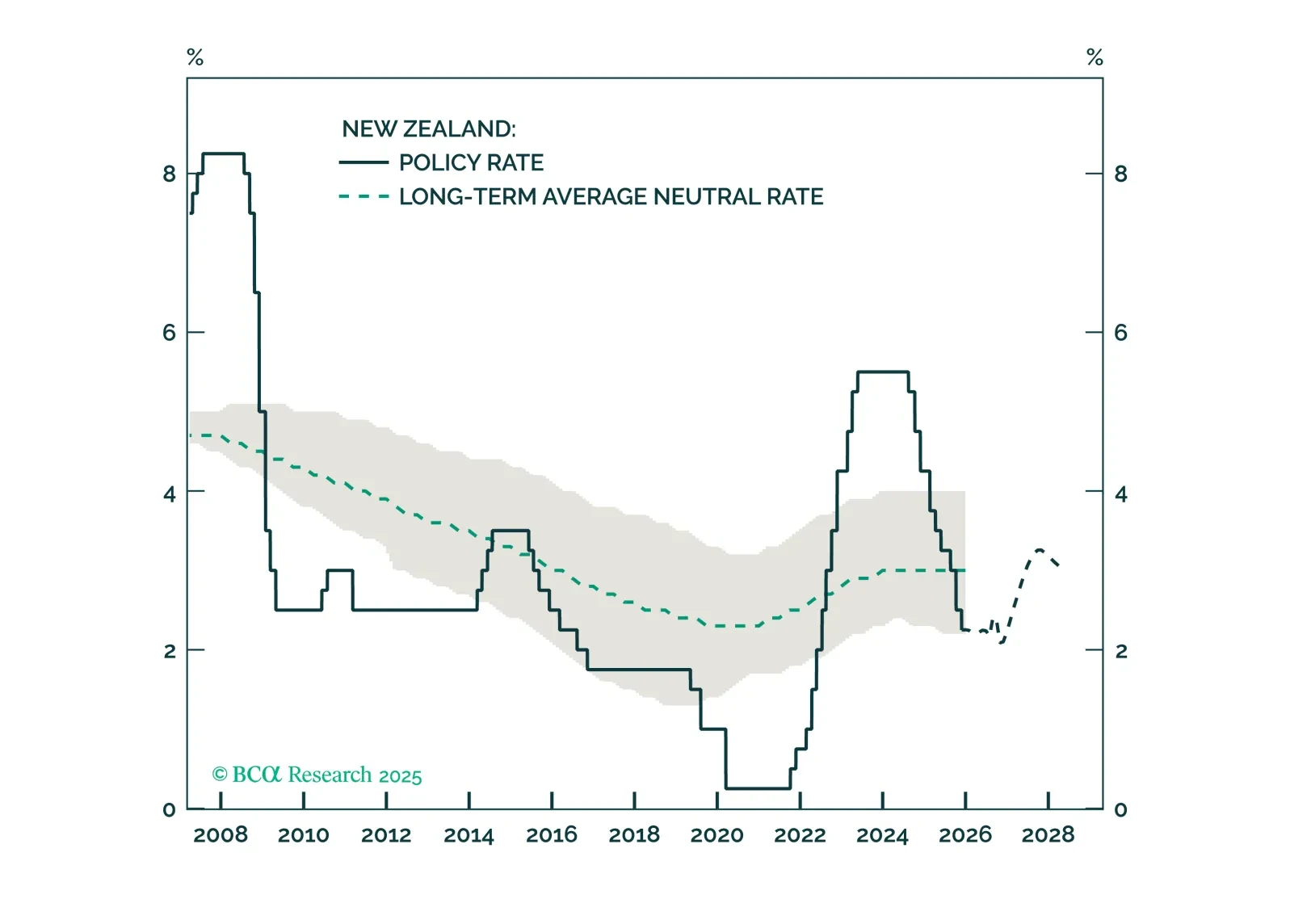

The RBNZ has concluded its aggressive easing blitz. With New Zealand economy finally showing signs of life, both the kiwi and local rates now look ripe for a reversal.

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

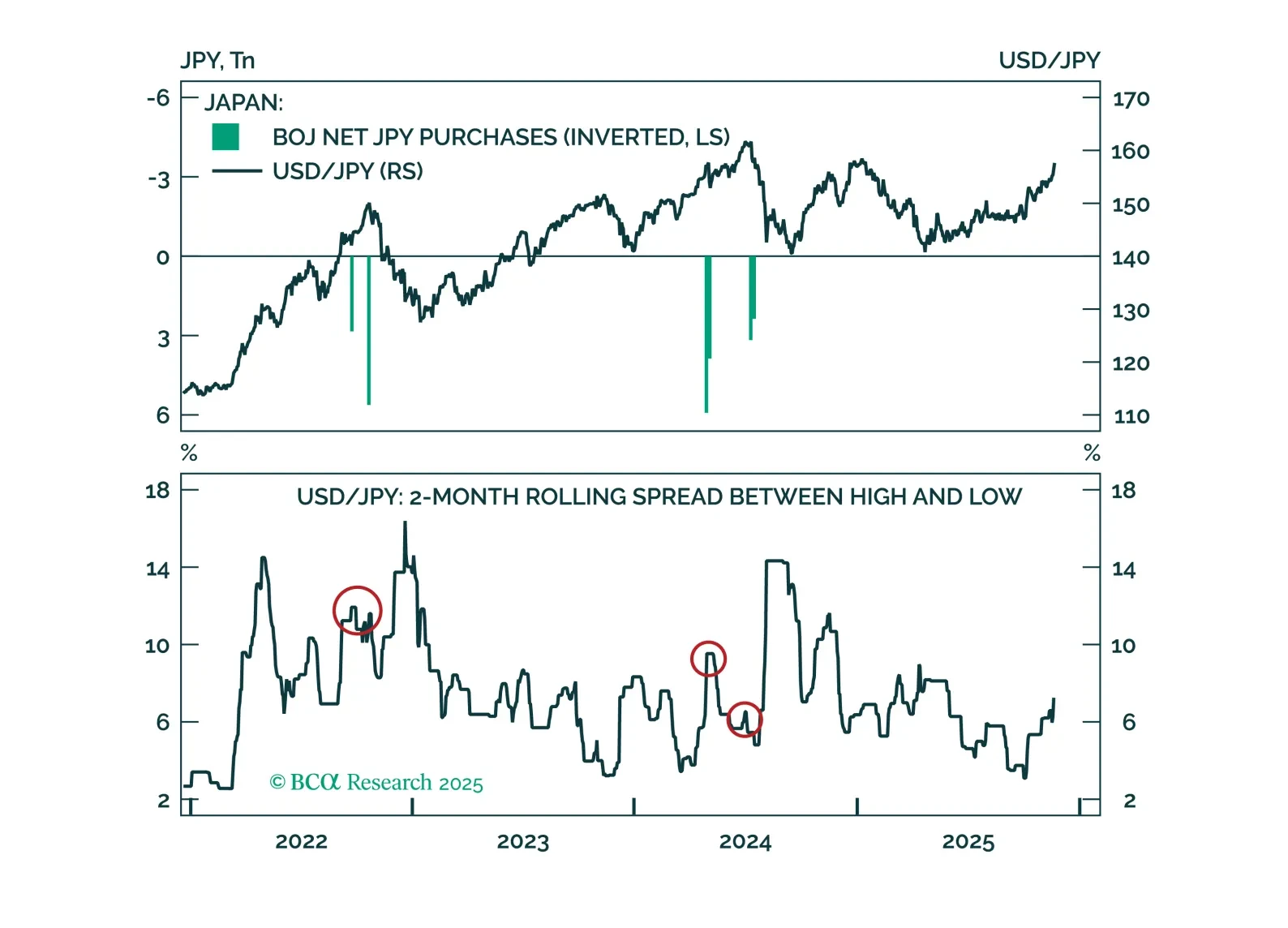

Markets are misreading Japan’s fiscal headlines. Our latest Insight examines what will shape BoJ policy next, when intervention might come, and the timing of a yen reversal.

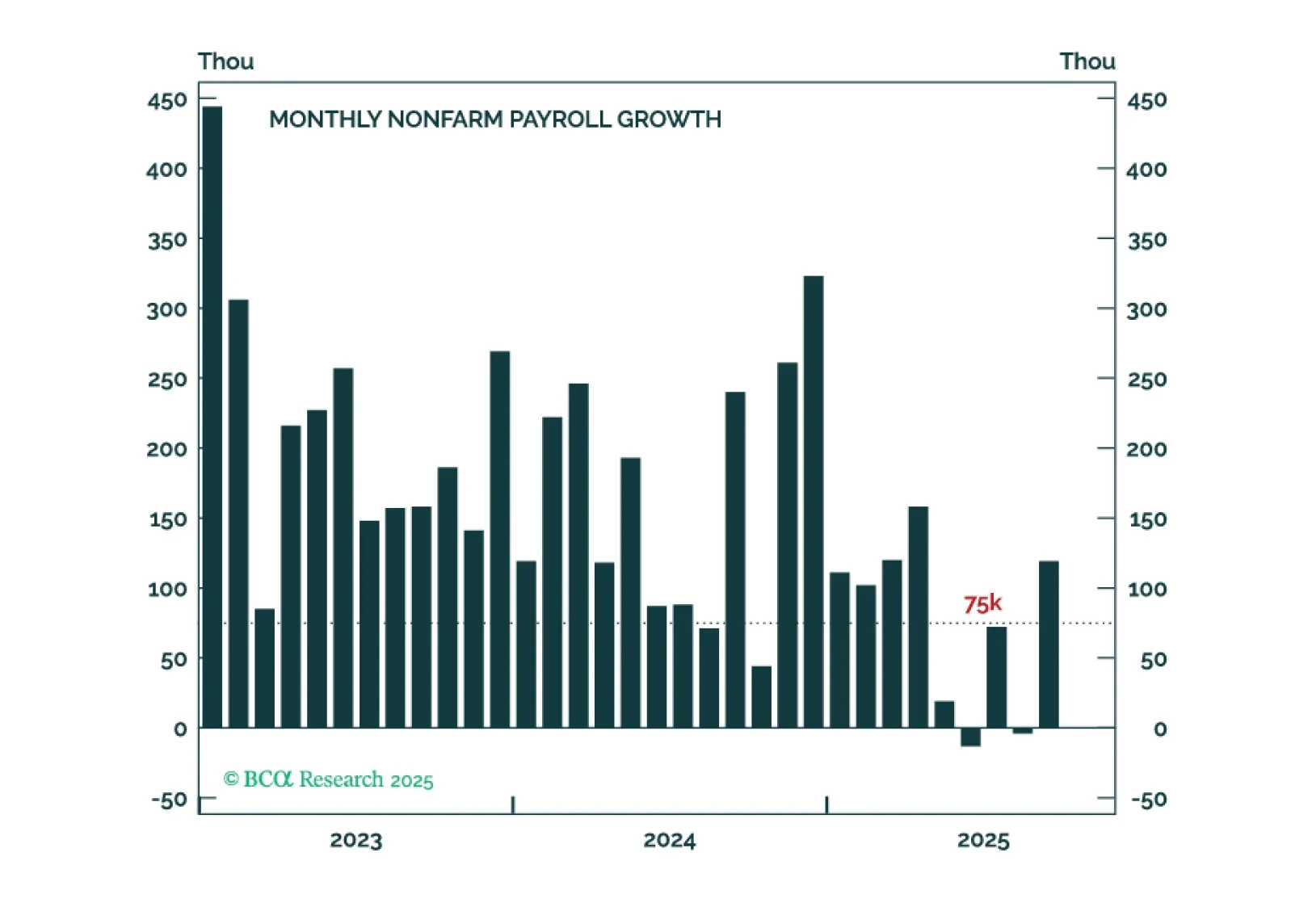

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

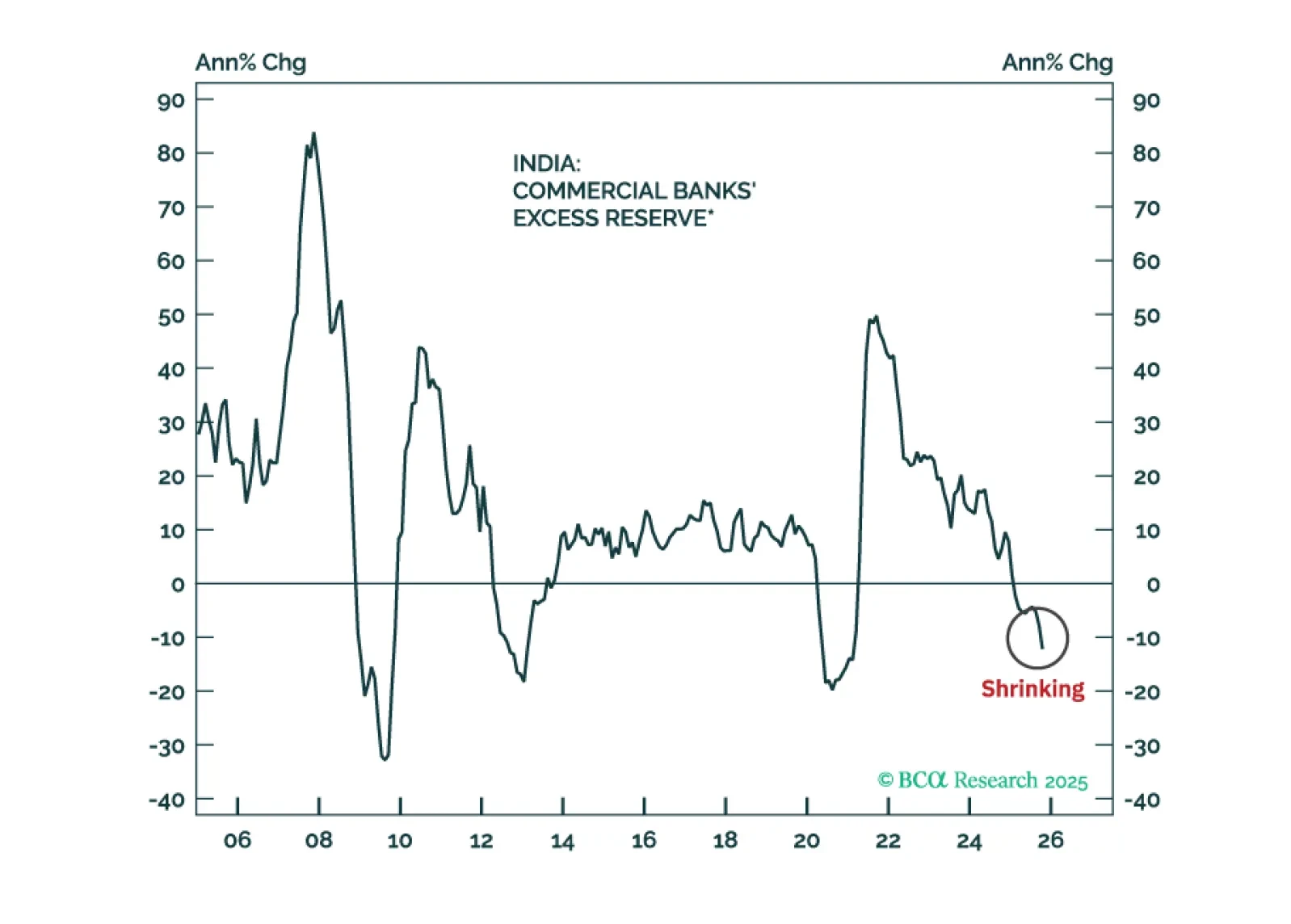

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

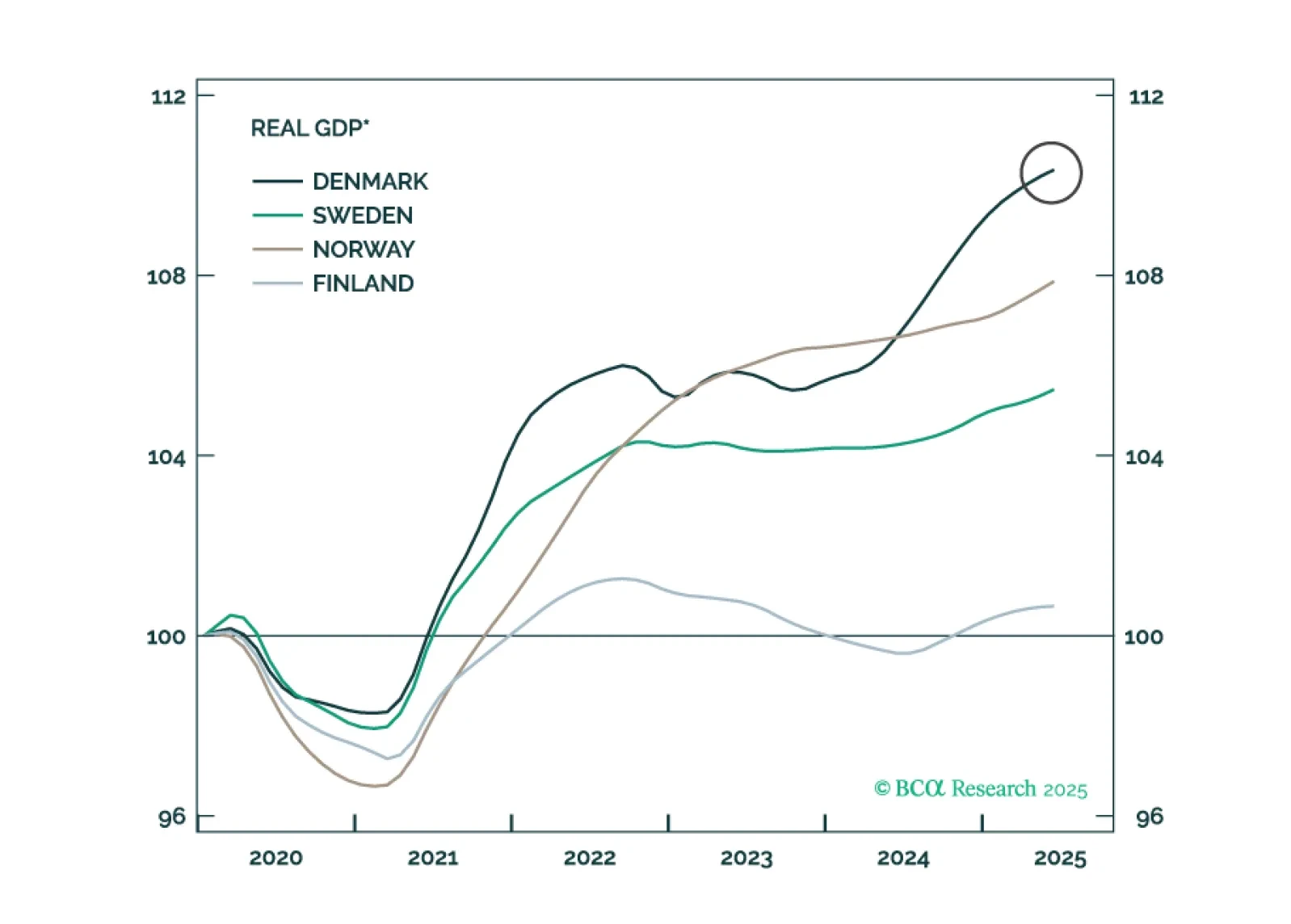

The Nordic central banks are now aligned in pause mode, but their economies are diverging. With Swedish prospects improving and Norwegian headwinds mounting, we are turning overweight on Swedish equities and shorting NOK/SEK.

The Bank of England will resume rate cuts in December after the autumn budget is passed. Today’s Strategy Insight discusses what this means for UK gilts and the pound.

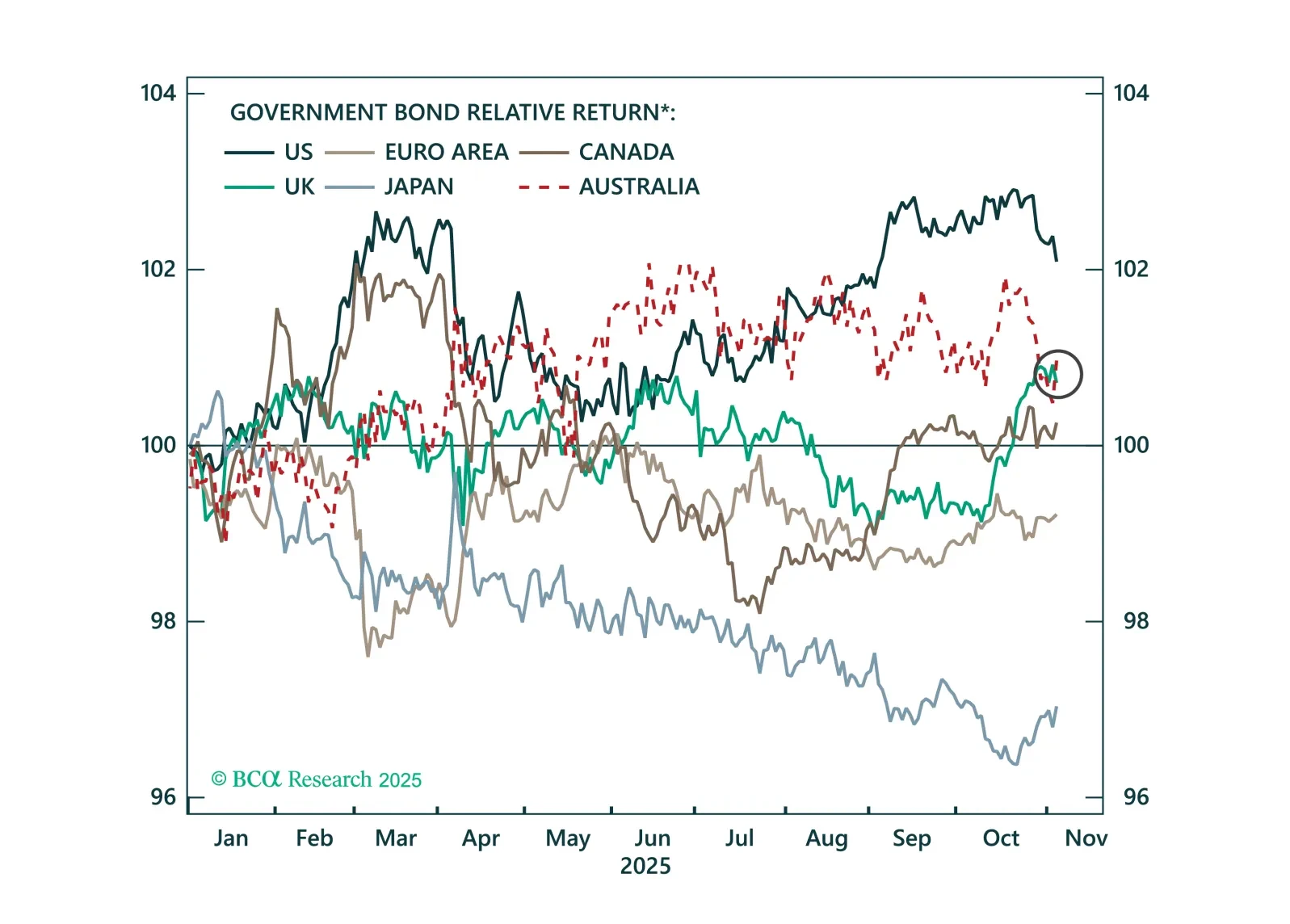

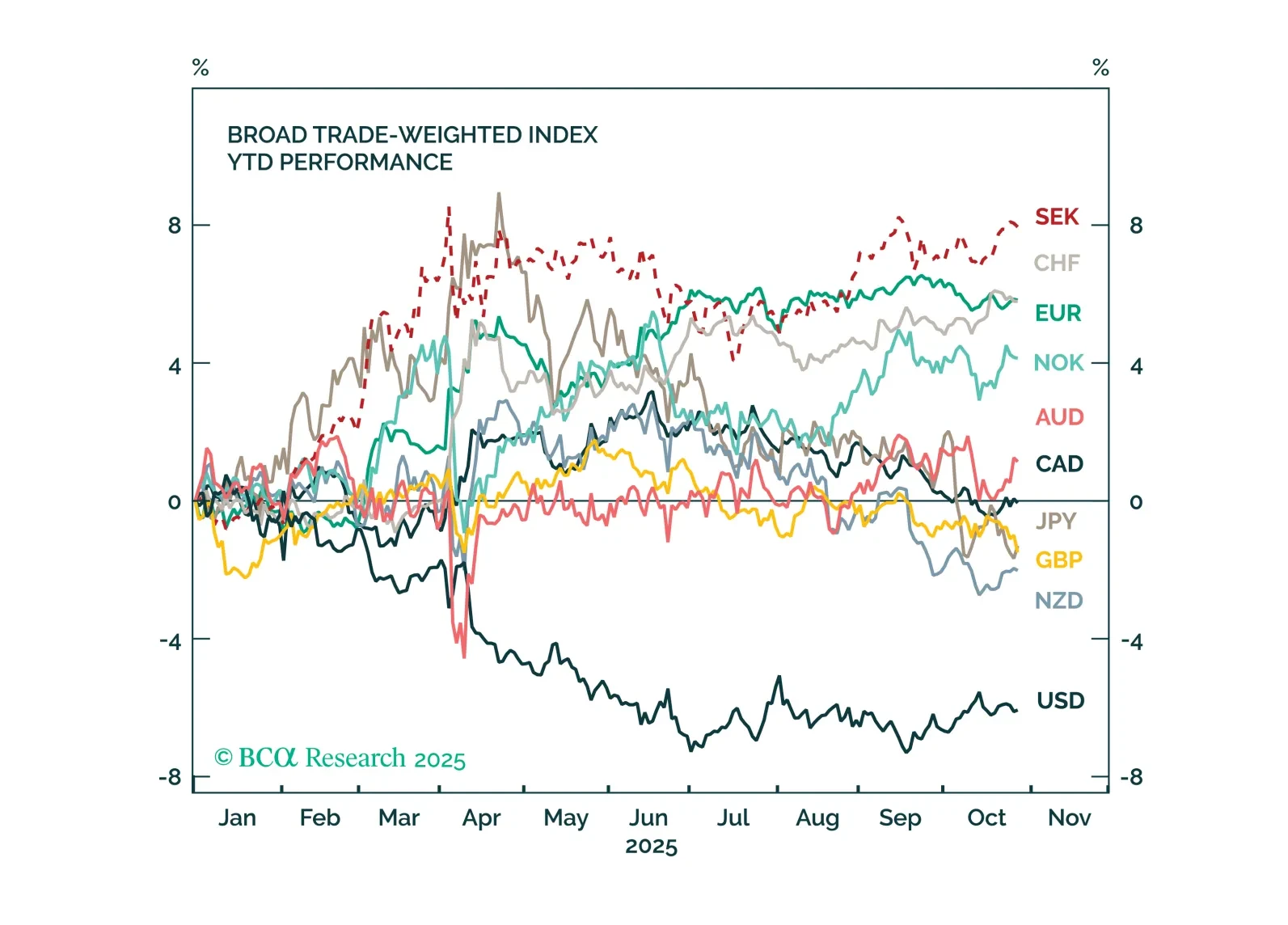

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.