Monetary Policy

This week’s central bank meetings are a good reminder that monetary policy can still surprise. The Bank of England sounded more dovish, and the European Central Bank sounded complacent about the inflation undershoot. Meanwhile, the Reserve Bank of Australia hiked rates earlier this week. Investors should remain overweight UK Gilts, position for more ECB easing by going long the September 2026 3-month Euribor futures, and fade further rate hikes priced in Australia.

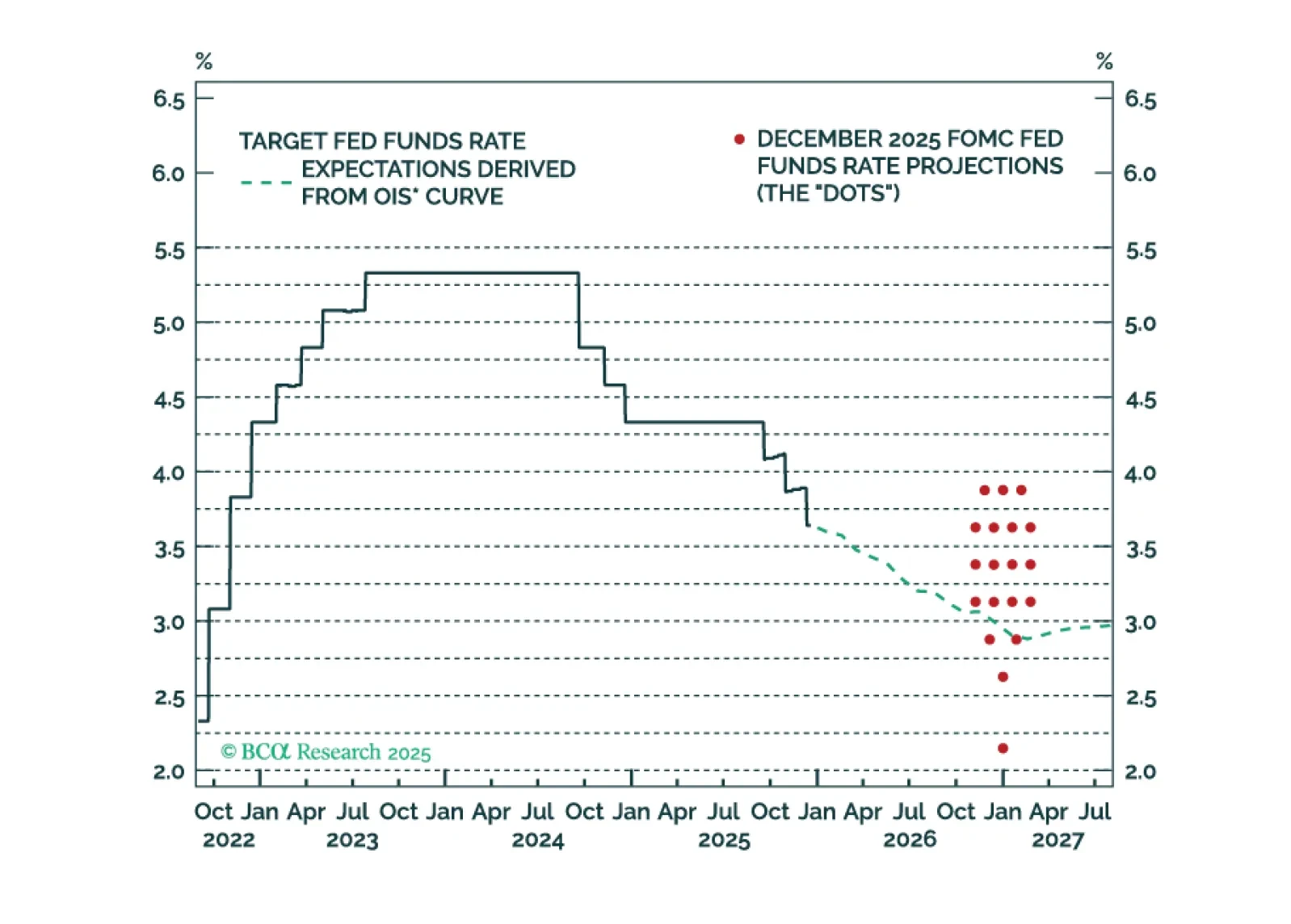

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

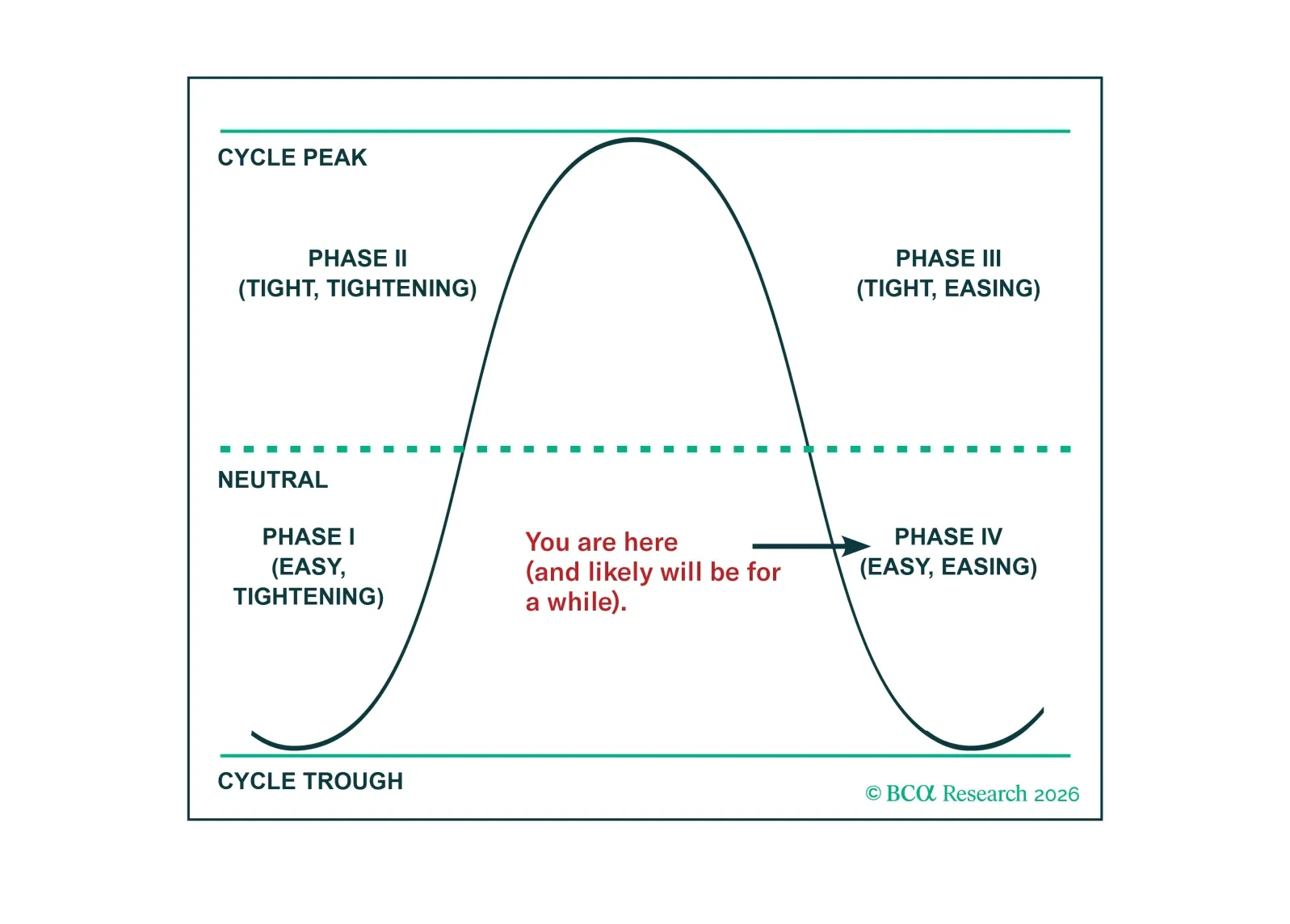

With the Fed looming larger on investors’ radar screens, we revisit our fed funds rate cycle analysis. We expect that the current easing-while-already-easy phase will be less rewarding than normal for the S&P 500 because multiples have already expanded to very elevated levels.

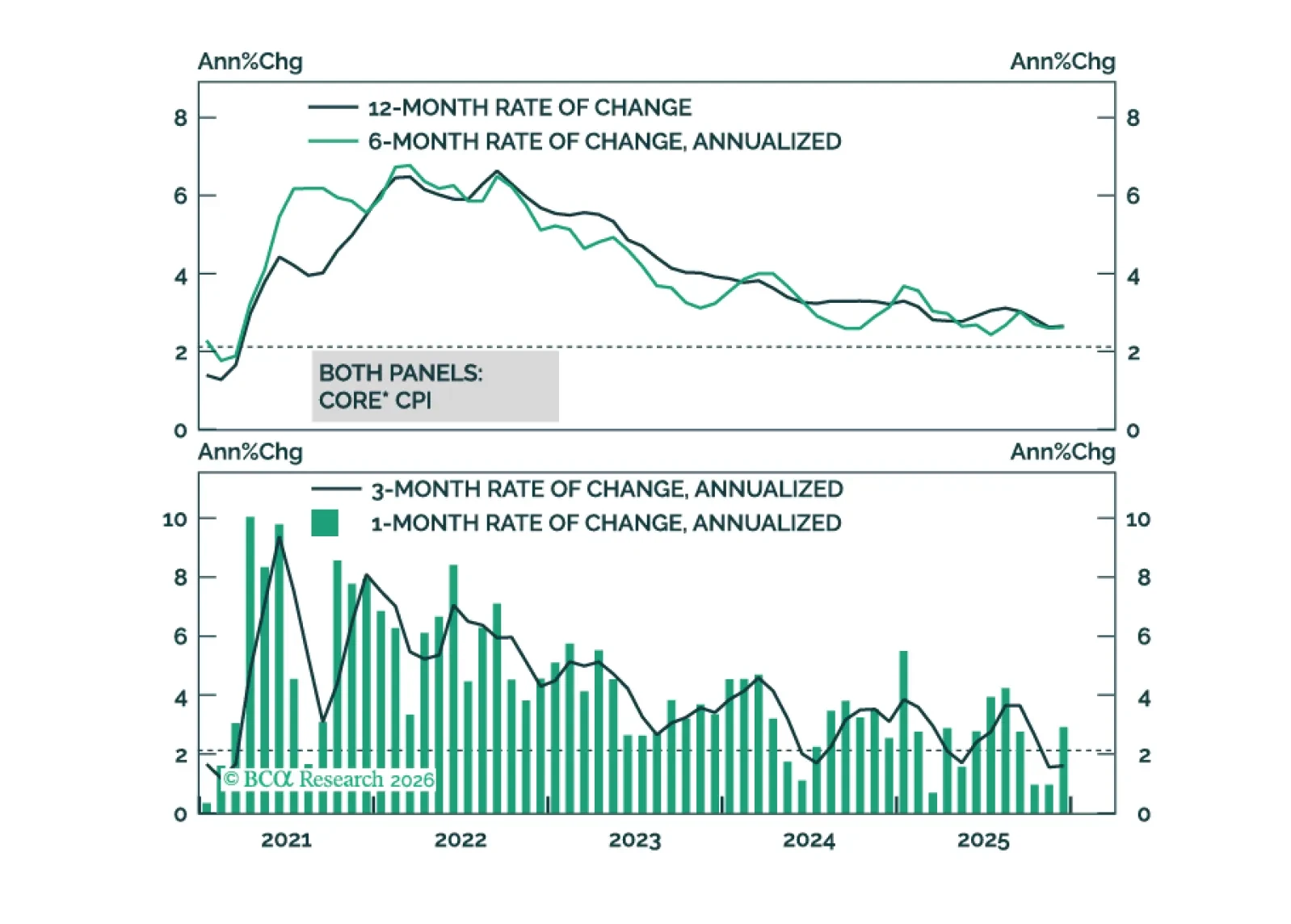

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

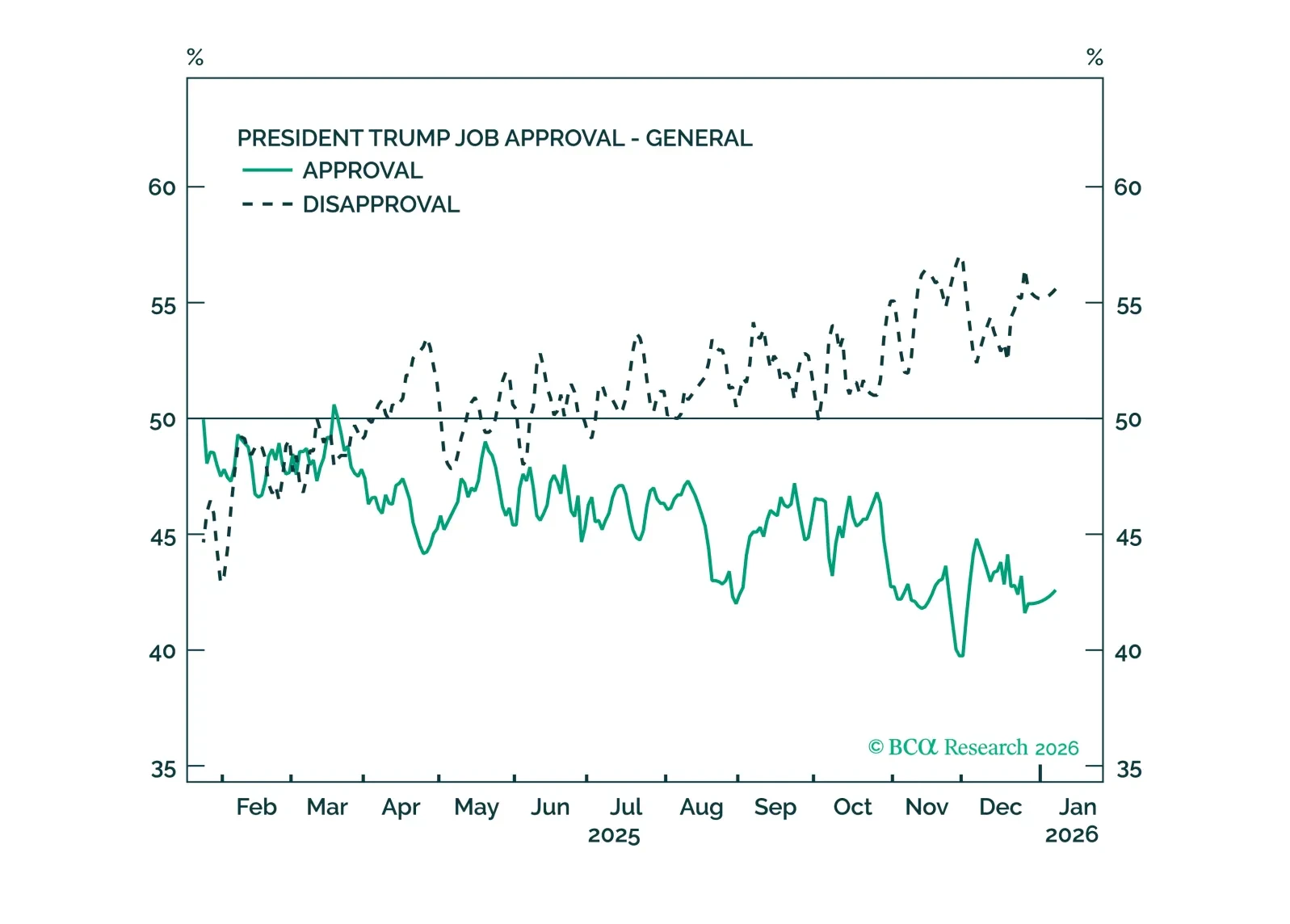

Congress will ultimately limit Trump from acting on his worst impulses, but his efforts to bypass those limits will cause market volatility.

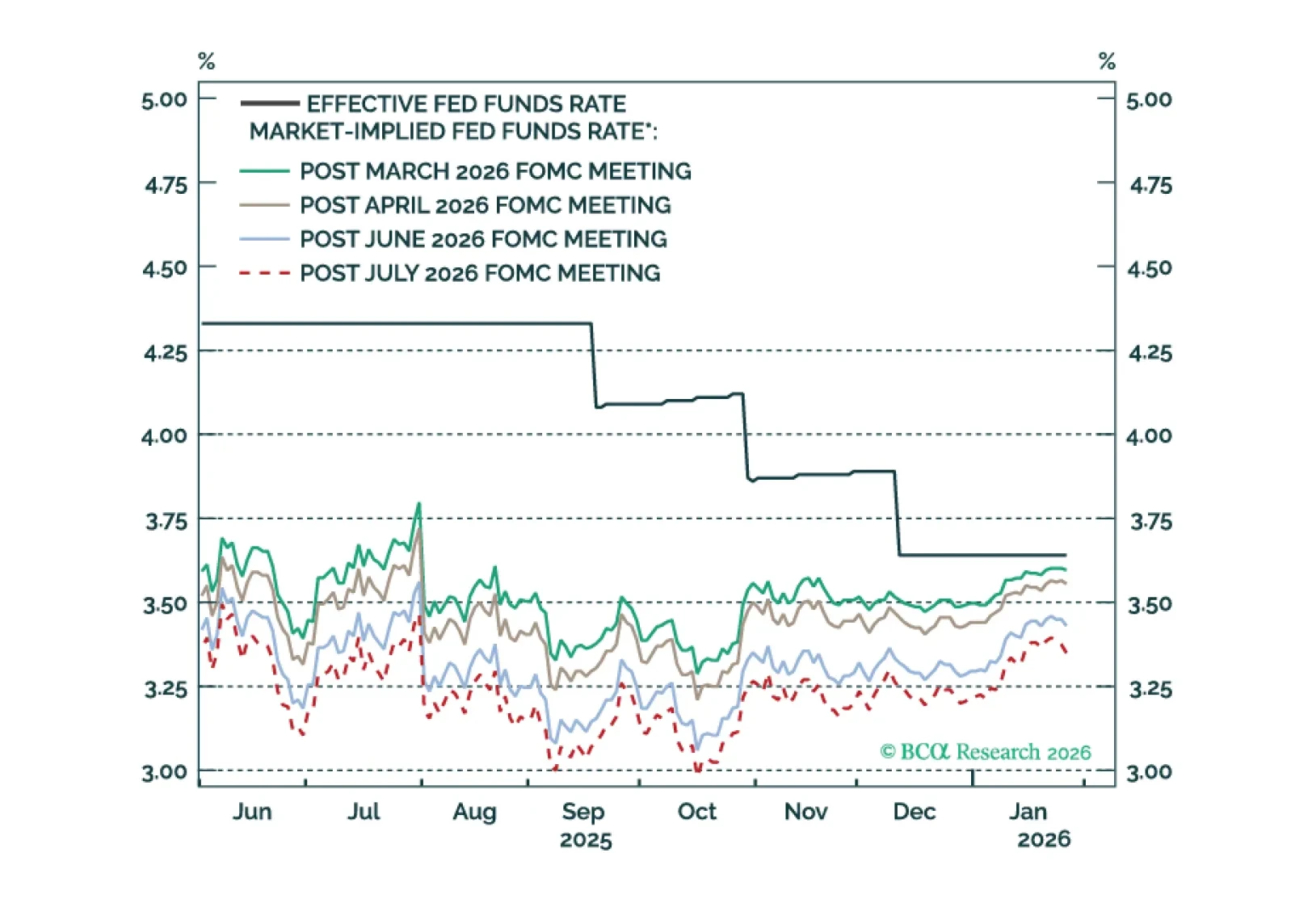

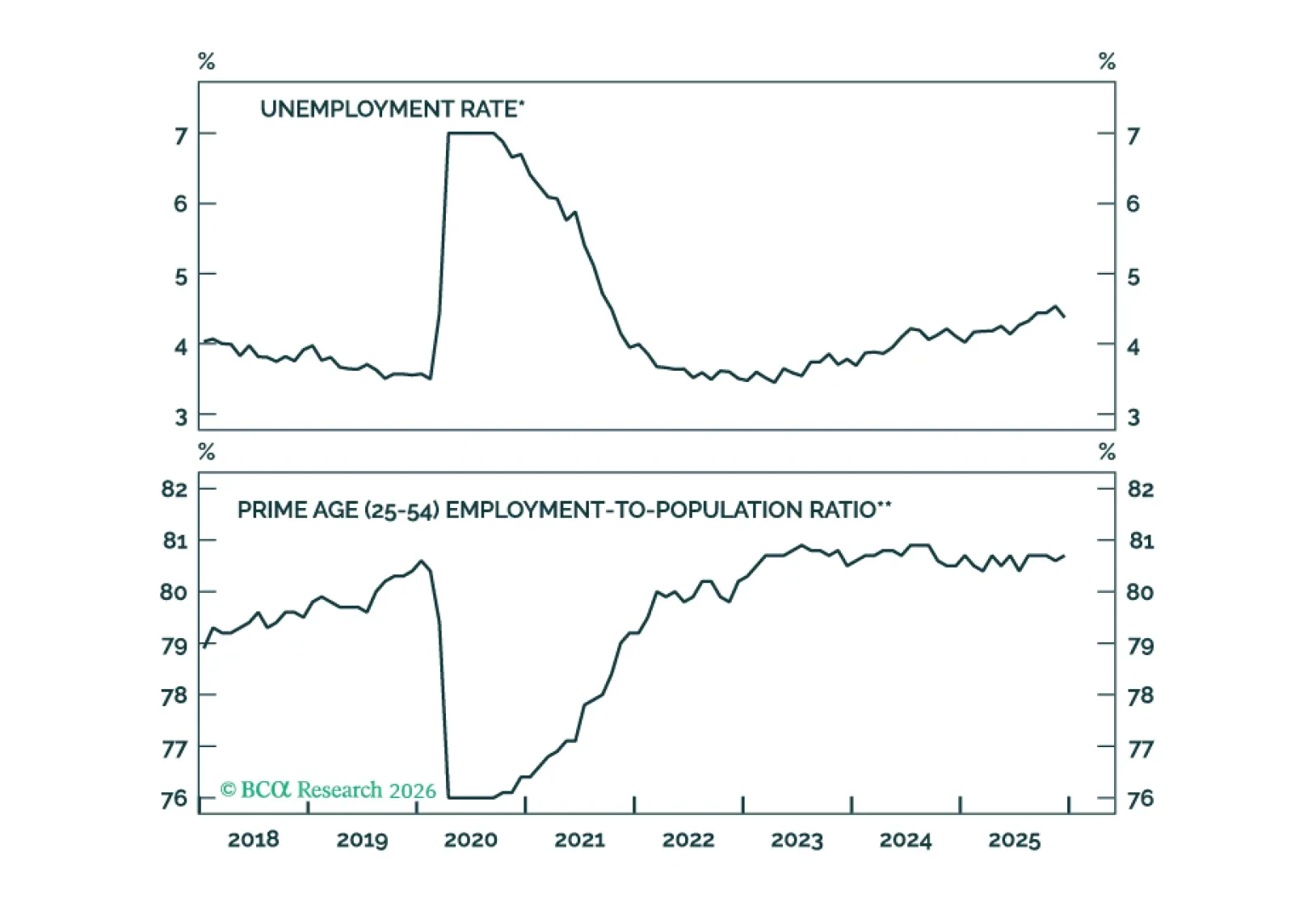

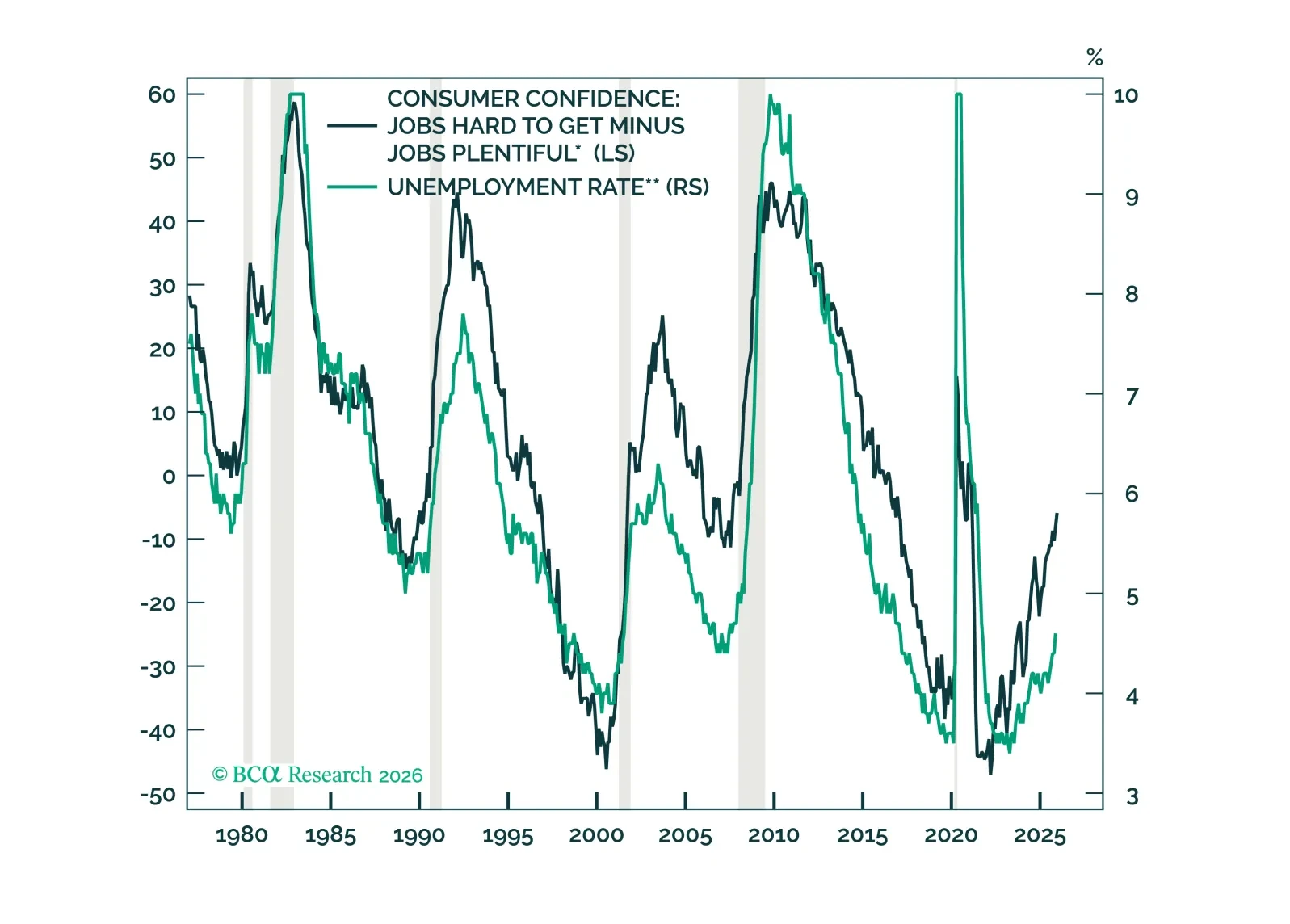

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

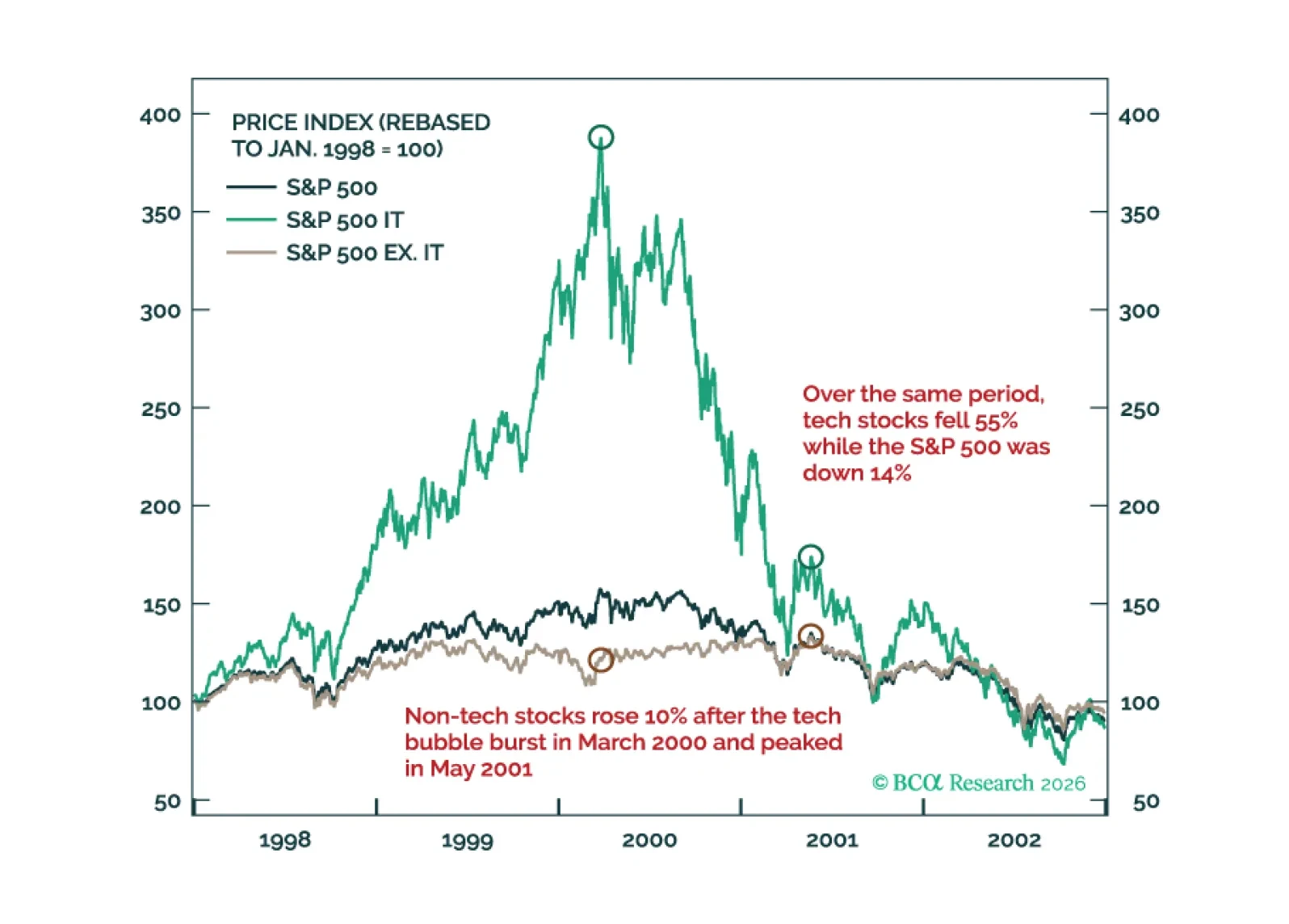

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

We have been surprised that consumption has held up well despite anemic payrolls growth. This brief considers ways that consumption might continue to beat our base-case expectations.