Monetary Policy

With central banks largely on hold, the return of a lower volatility environment is bringing carry trades back into focus. We outline the most attractive carry opportunities across global fixed income markets.

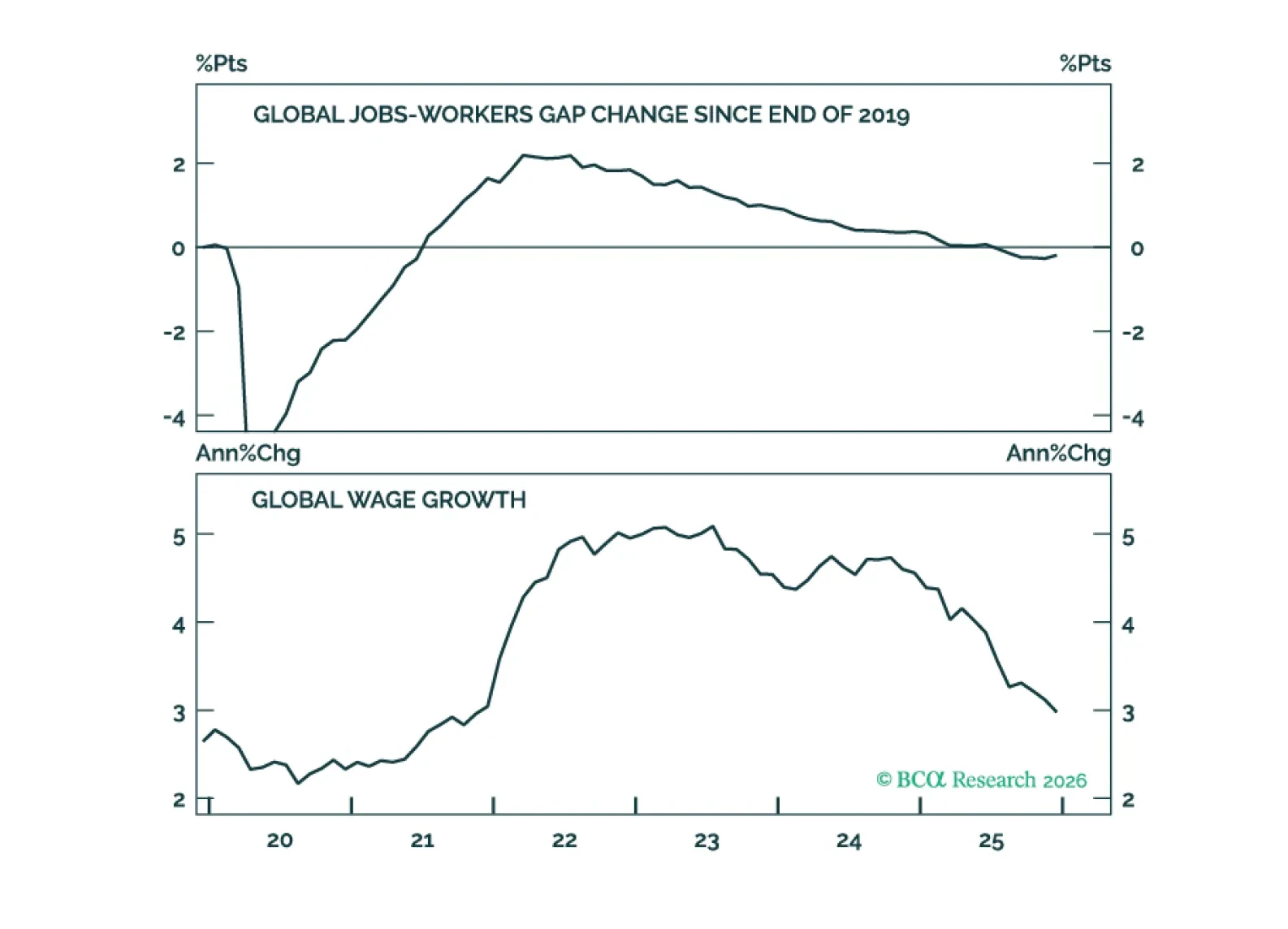

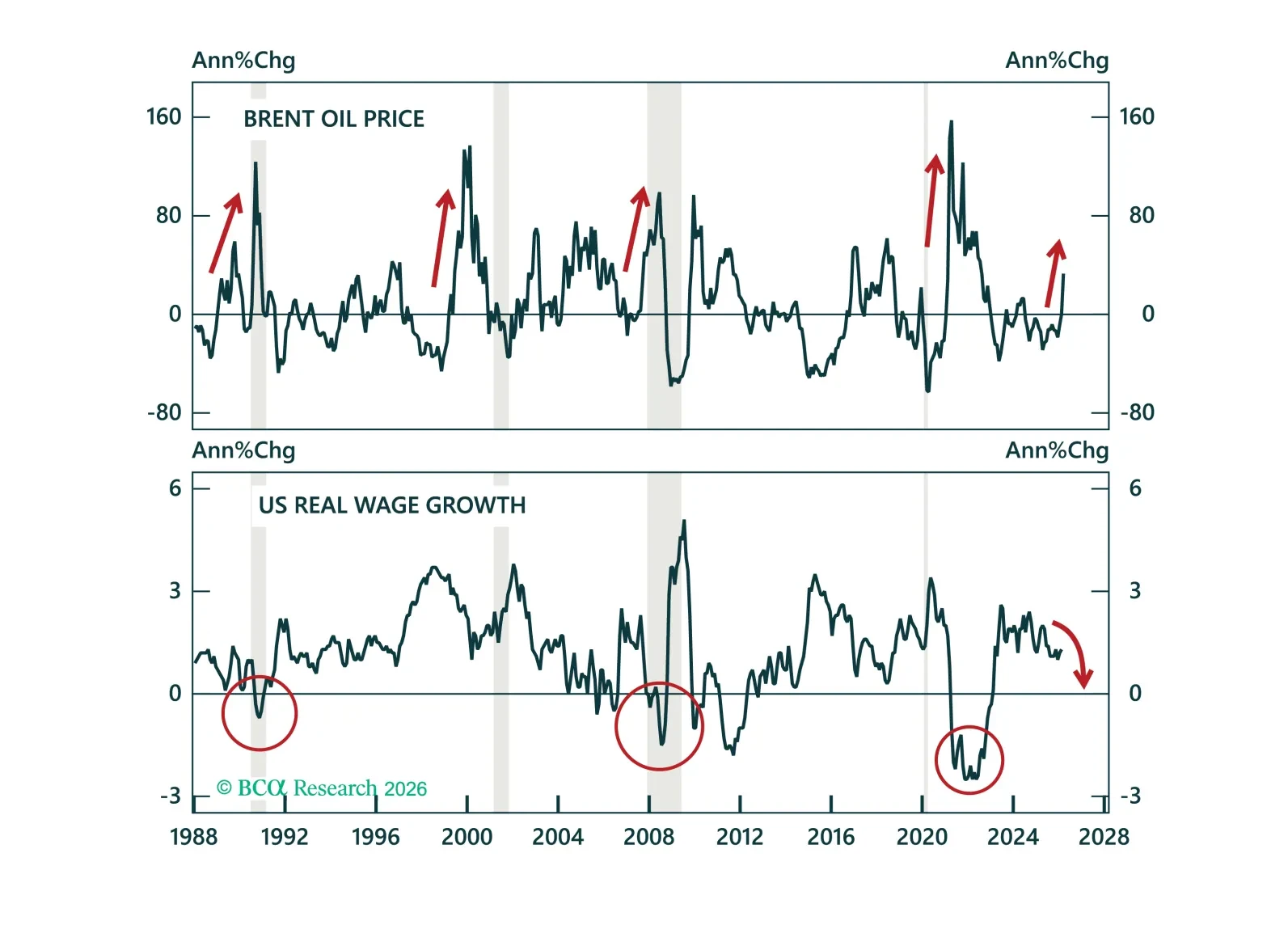

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.

In today’s Strategy Insight, we show why both a quick resolution and a prolonged crisis ultimately point to lower yields.

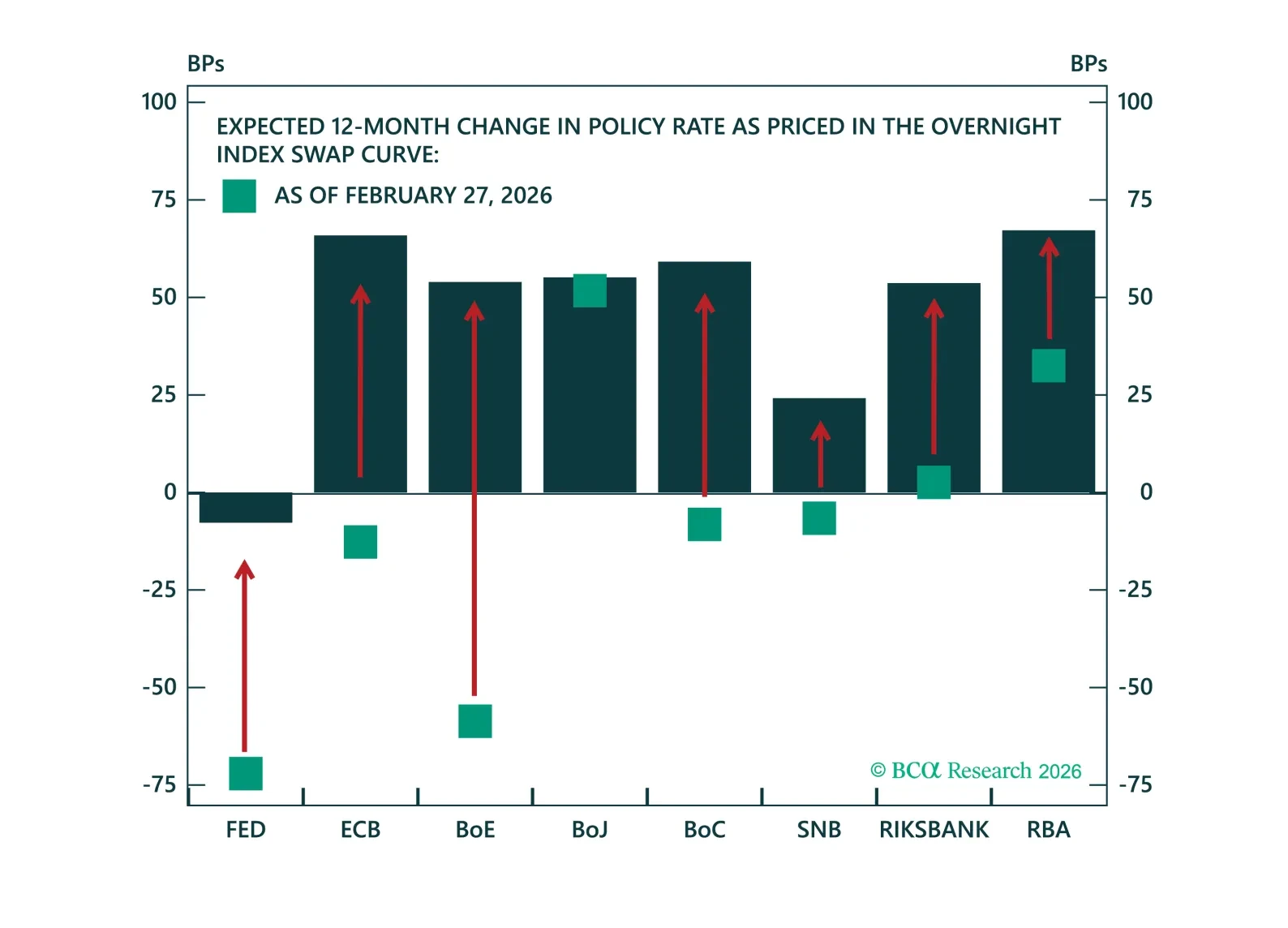

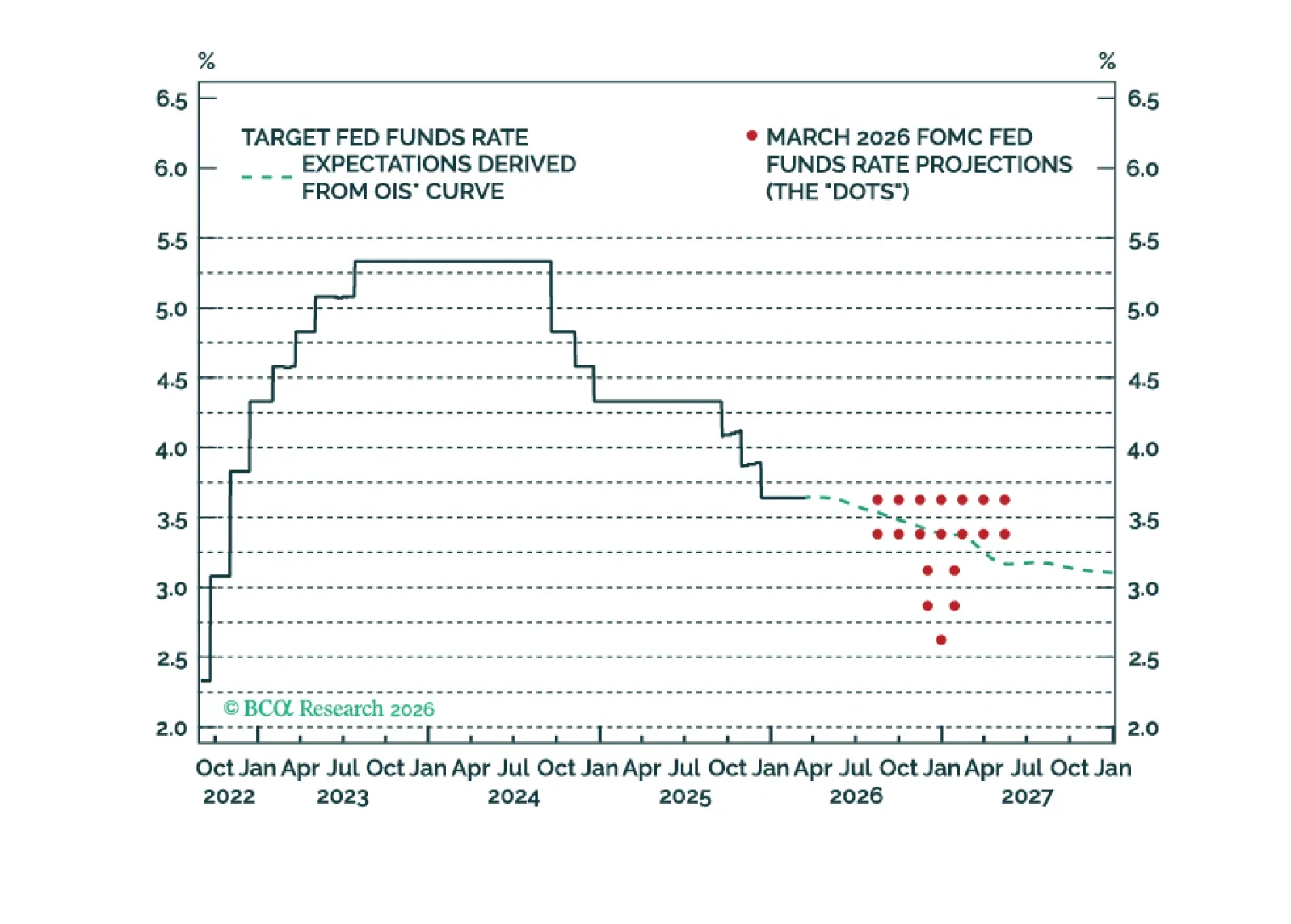

We discuss the takeaways from this week’s central bank meetings amidst the unfolding energy price shock.

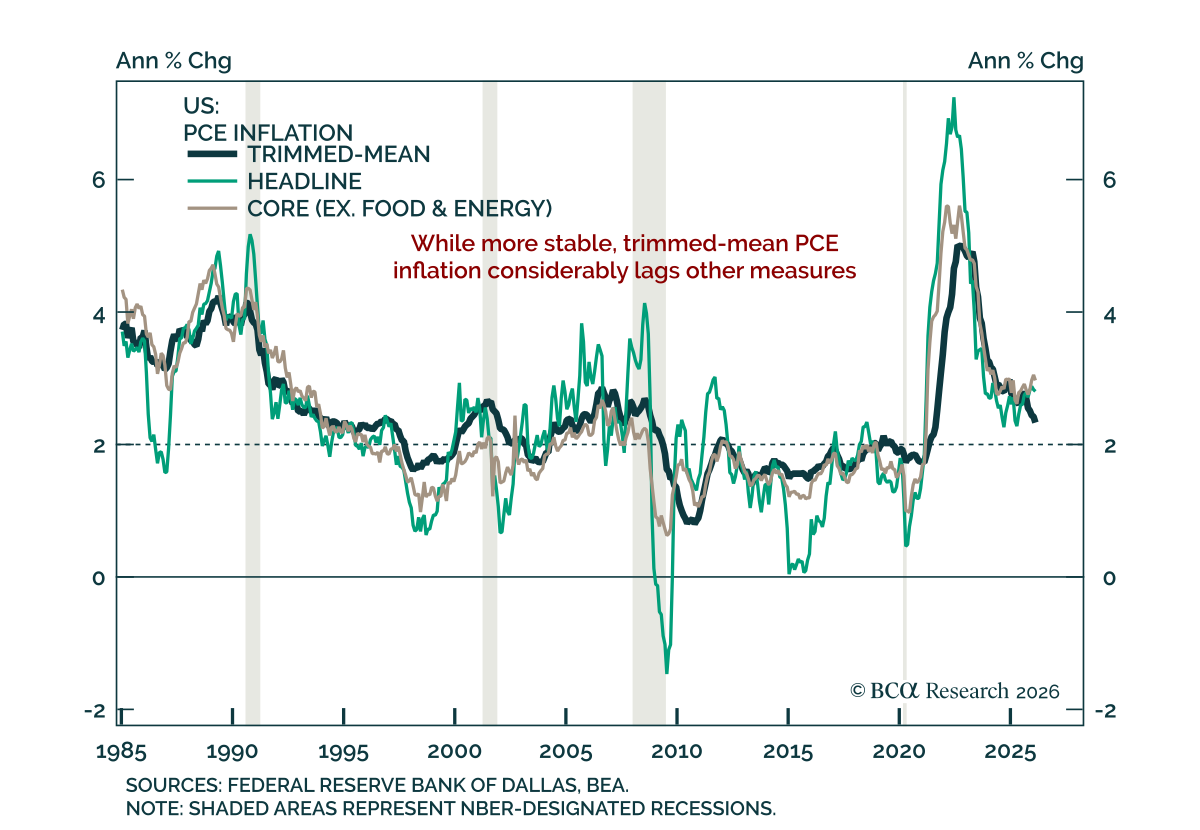

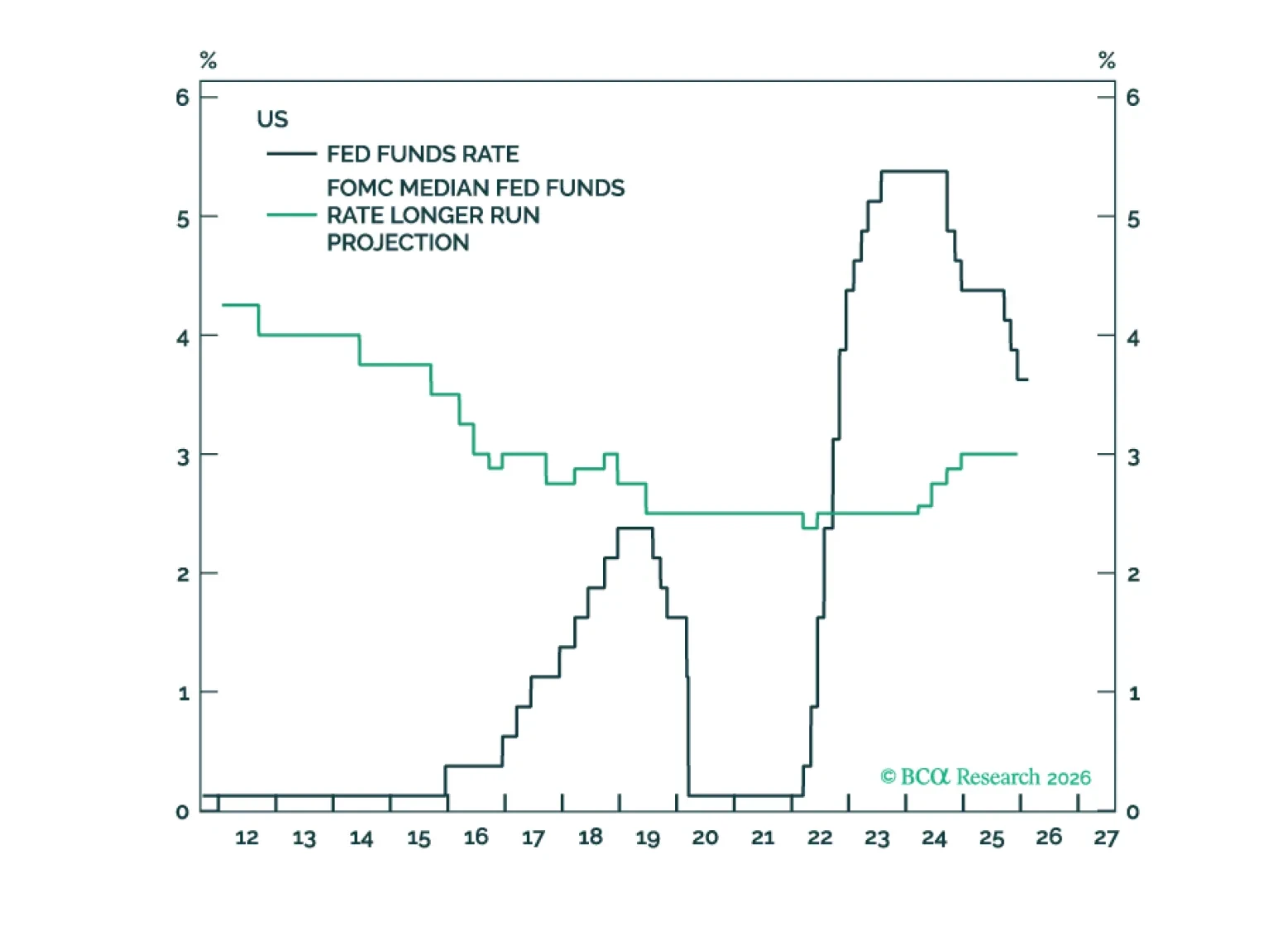

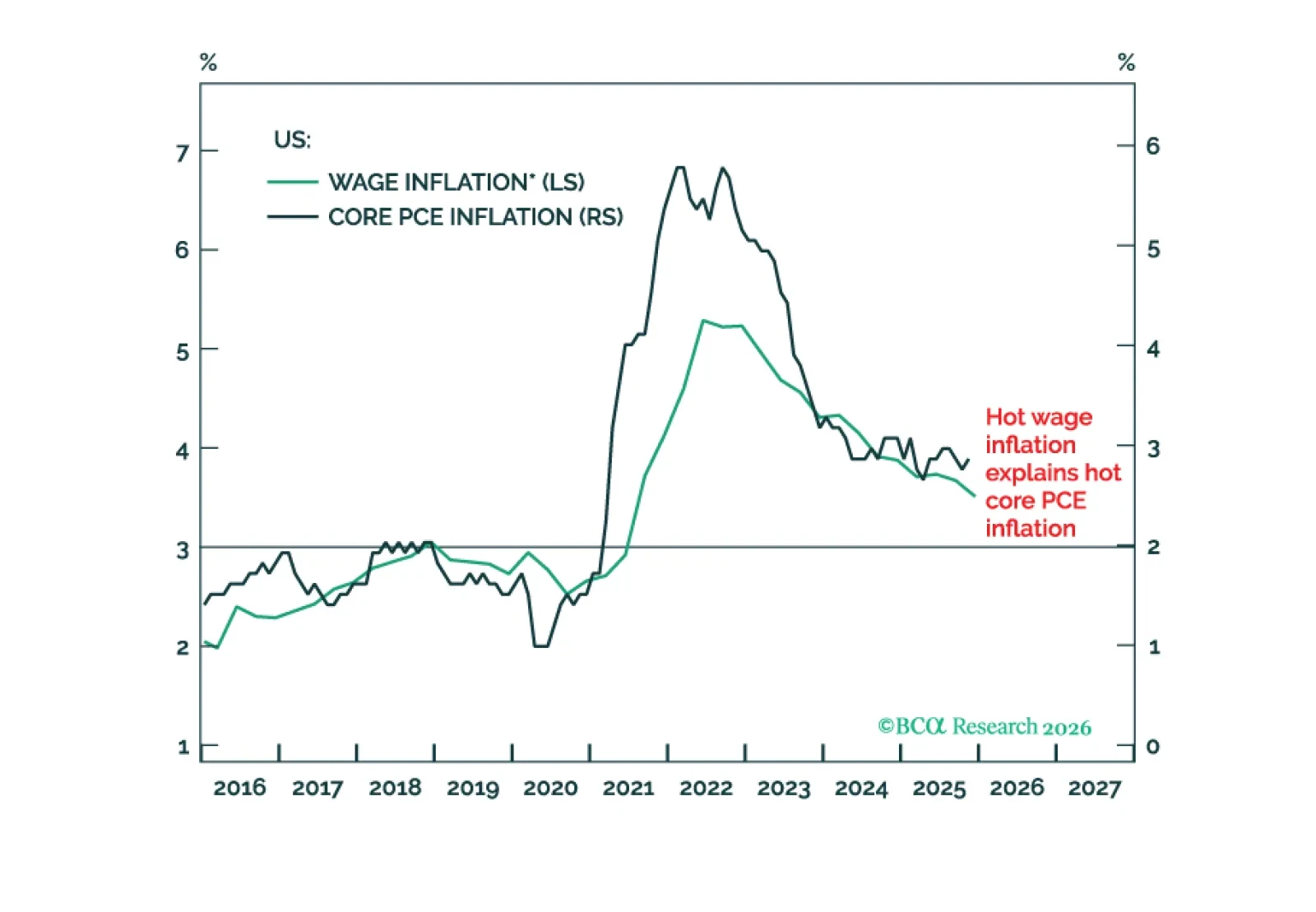

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

The Warsh Fed will run the US economy hot. This is bad for T-bonds and the dollar, but good for stocks. Plus, a new tactical trade is overweight Consumer Discretionary (RXI) versus Industrials (EXI).