Monetary Policy

Fed Chair Jay Powell’s remarks yesterday were in-line with our base case expectation that the Fed will not cut rates proactively in the face of rising tariff-driven inflation.

Today, we publish our Quarterly Model Bond Portfolio report. We discuss how the trade war has further increased the global recession risk, but US Treasuries could underperform their global peers in the near term. We cover the fixed income investment implications in the short run and which bond markets are poised to outperform in a severe economic downturn.

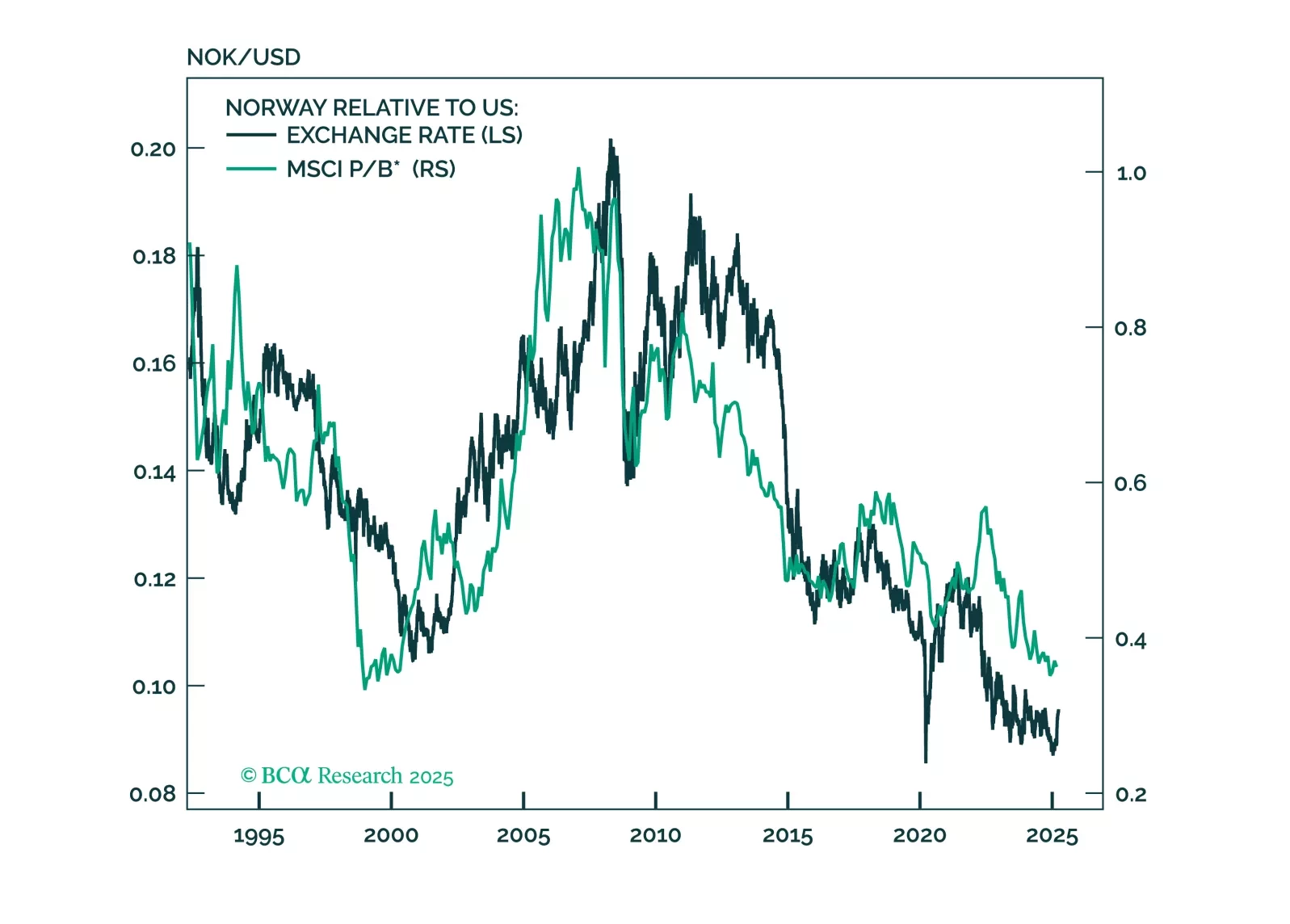

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.

This report is a quick take on our views on UK bonds and FX, given the recent budget.

Given the meetings between the Bank of Japan, the Bank of England, and the Swiss National Bank, our highest convictions views are:

Overweight UK Gilts. It is also time to sell sterling. We are short sterling, as of 1.30.

Underweight JGBs. Correspondingly, be long the yen.

A short CHF/JPY position remains a core holding. Selling GBP/JPY is also a great trade.

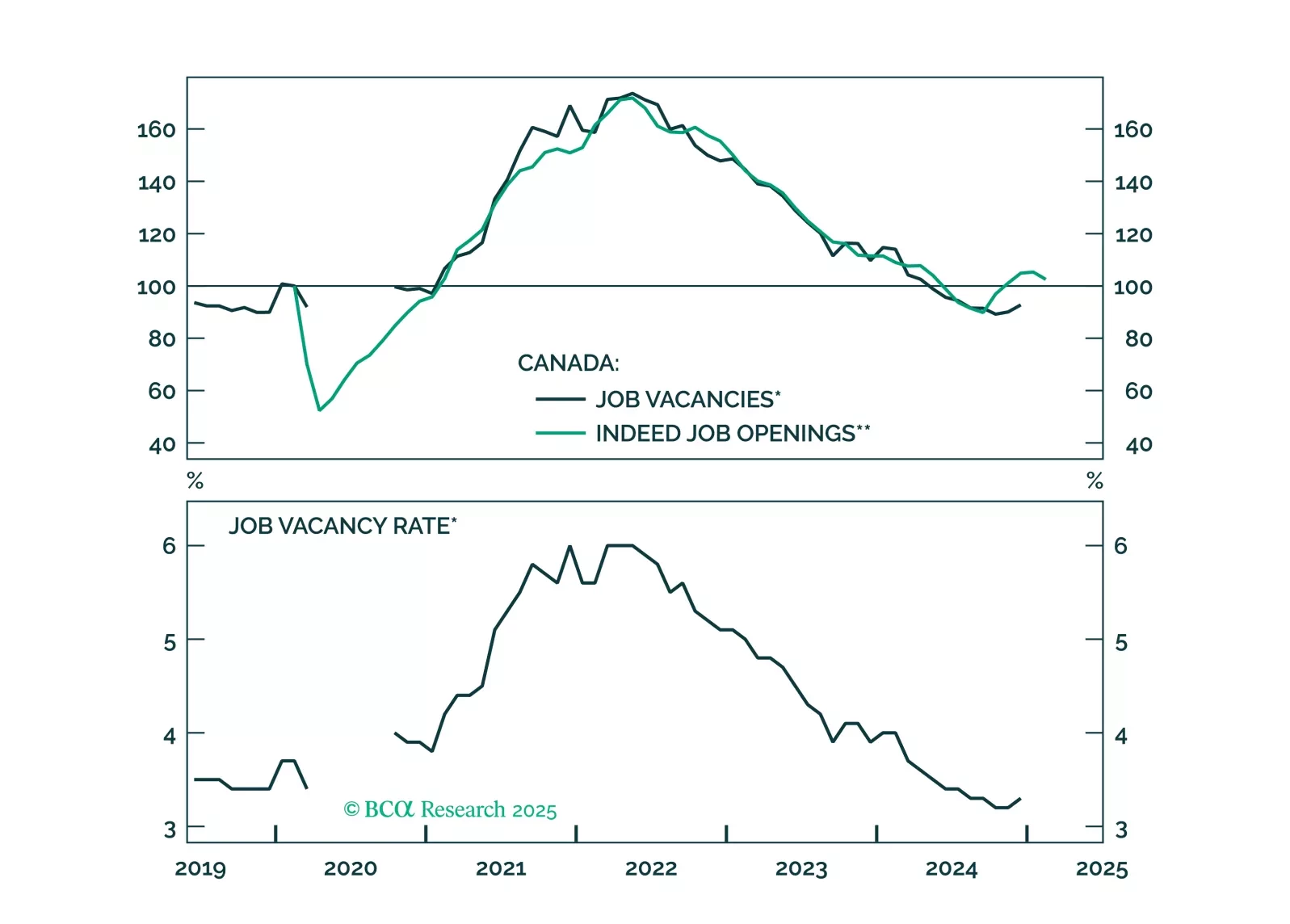

The trade war complicates the Bank of Canada’s task to achieve stable inflation. But the bottom line is that rising uncertainty, which will dampen business sentiment, will cause the BoC to cut rates by at least what is priced in the CORRA curve, and likely to 2%. The CAD, which is very oversold, might not depreciate much. The big trade is a bet on a spread widening for Canadian provincial bonds.

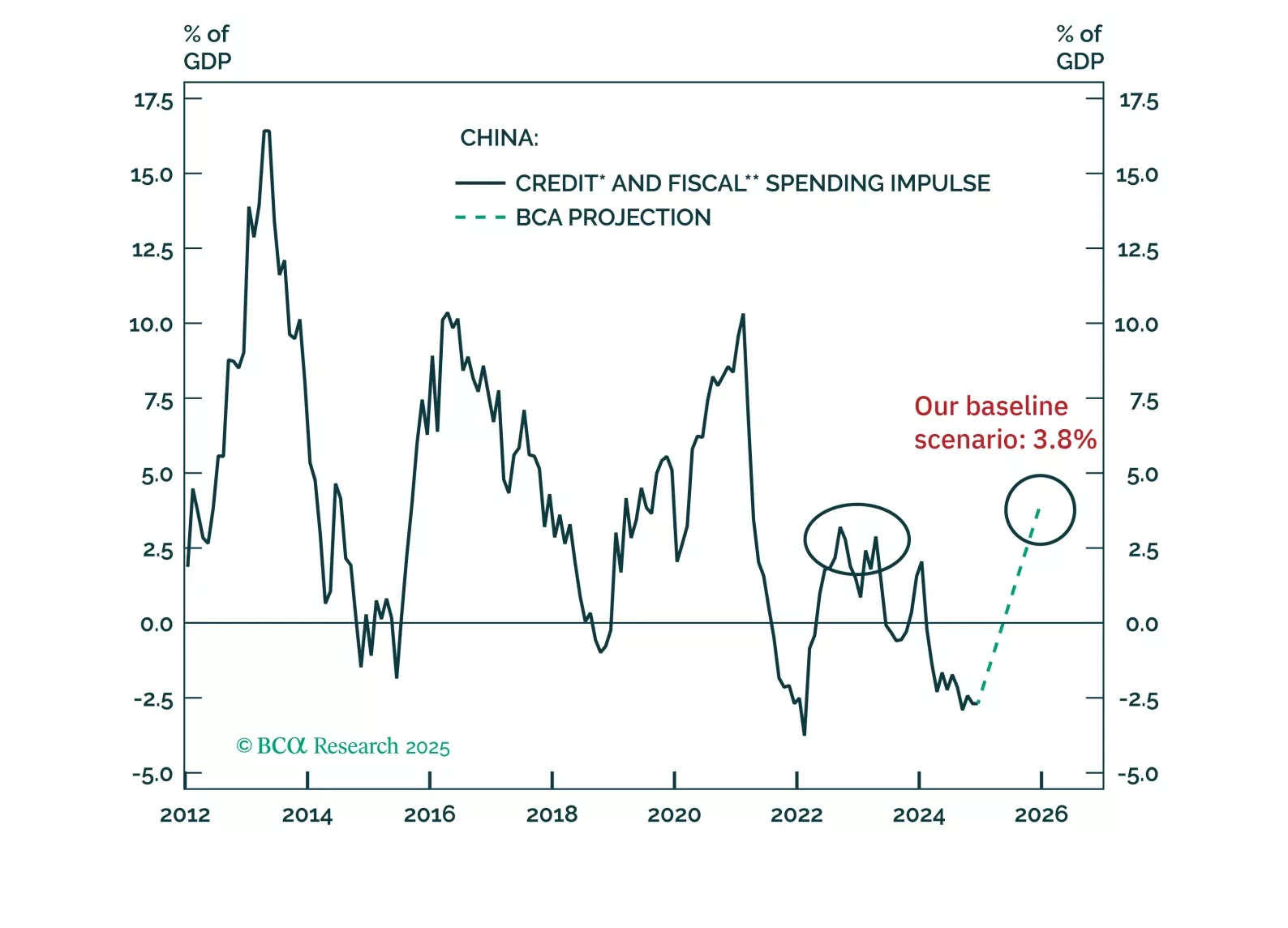

The fiscal stimulus announced at this year’s National People’s Congress is only slightly larger than last year’s. Notably, the details of the measures suggest that it will be challenging for fiscal stimulus to effectively counterbalance the country’s economic difficulties this year.