Middle East & North Africa

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

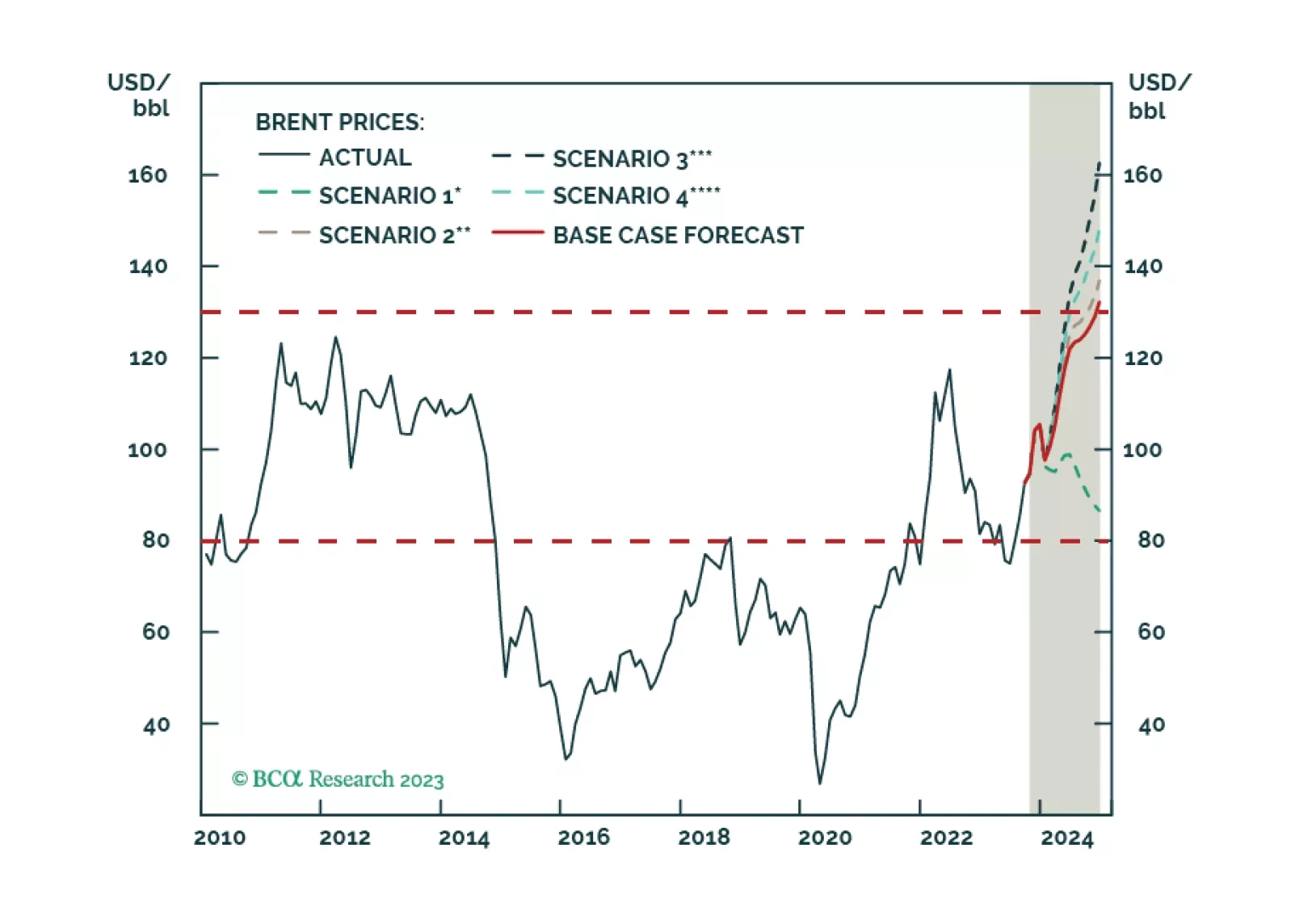

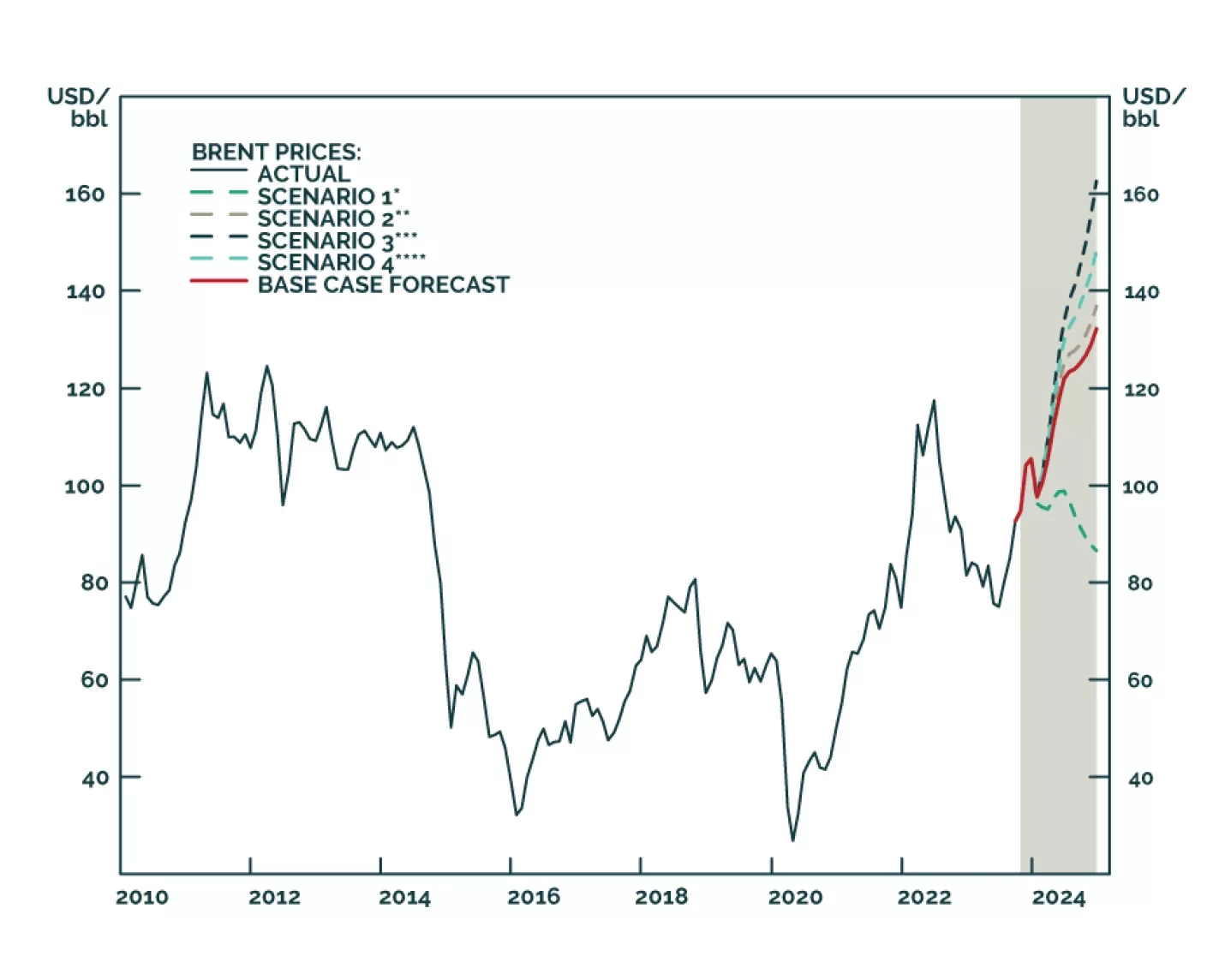

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

The Israeli-Arab crisis is more likely to expand and cause oil disruptions than market consensus holds. Close long dollar trades and go long energy and defense stocks relative to cyclicals.

Hamas’s attack on Israel raises the odds of a wider conflict in the Gulf, which would lead to higher oil prices. Given the response of oil prices Monday, markets appear to be relatively restrained in their assessment of a sharp escalation in prices. However, this is early days in a strategy that is just revealing itself.

Volatility will remain the key dynamic in oil markets in the aftermath of the surprise Hamas attacks against Israel on October 7. The risk of a major oil supply shock has gone up, but meanwhile supply constraints will remain at variance with global growth problems stemming from restrictive monetary policy over the next 12 months. Favor bonds over stocks, large caps over small caps, defense and energy stocks over other cyclicals, and US equities relative to global equities.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

Investors should underweight global equities and risk assets; overweight US stocks relative to global; and overweight defensive sectors versus cyclicals.

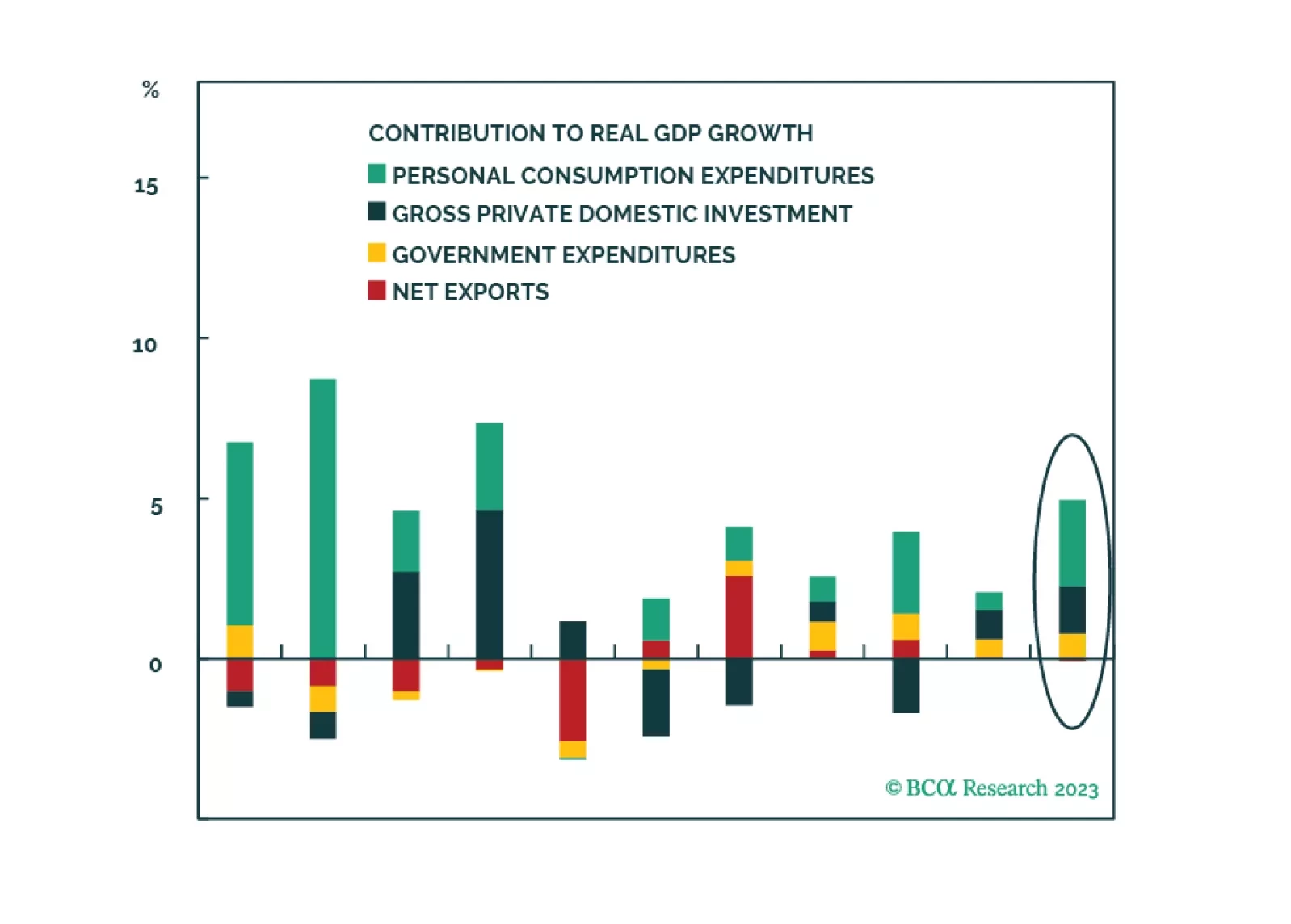

In Section I, we audit the market’s “soft landing” narrative in response to a meaningful challenge to our cautious stance from recent financial market developments. We acknowledge that US economic growth was stronger in the first half of the year than many investors expected, but we are unmoved by the recent uptick in “soft landing” hopes. A “soft landing” outcome very likely necessitates interest rate cuts before recessionary dynamics emerge, and it is far from clear that rate cuts or (especially) an easy monetary policy stance are likely to materialize over the coming year. As such, we continue to believe that conservative portfolio positioning is appropriate. In Section II, we discuss some simple approaches that we use when valuing the major asset classes that we cover. We conclude that global ex-US equities and ex-US developed market currencies are the main assets that can be considered “cheap” today.