Mega Themes

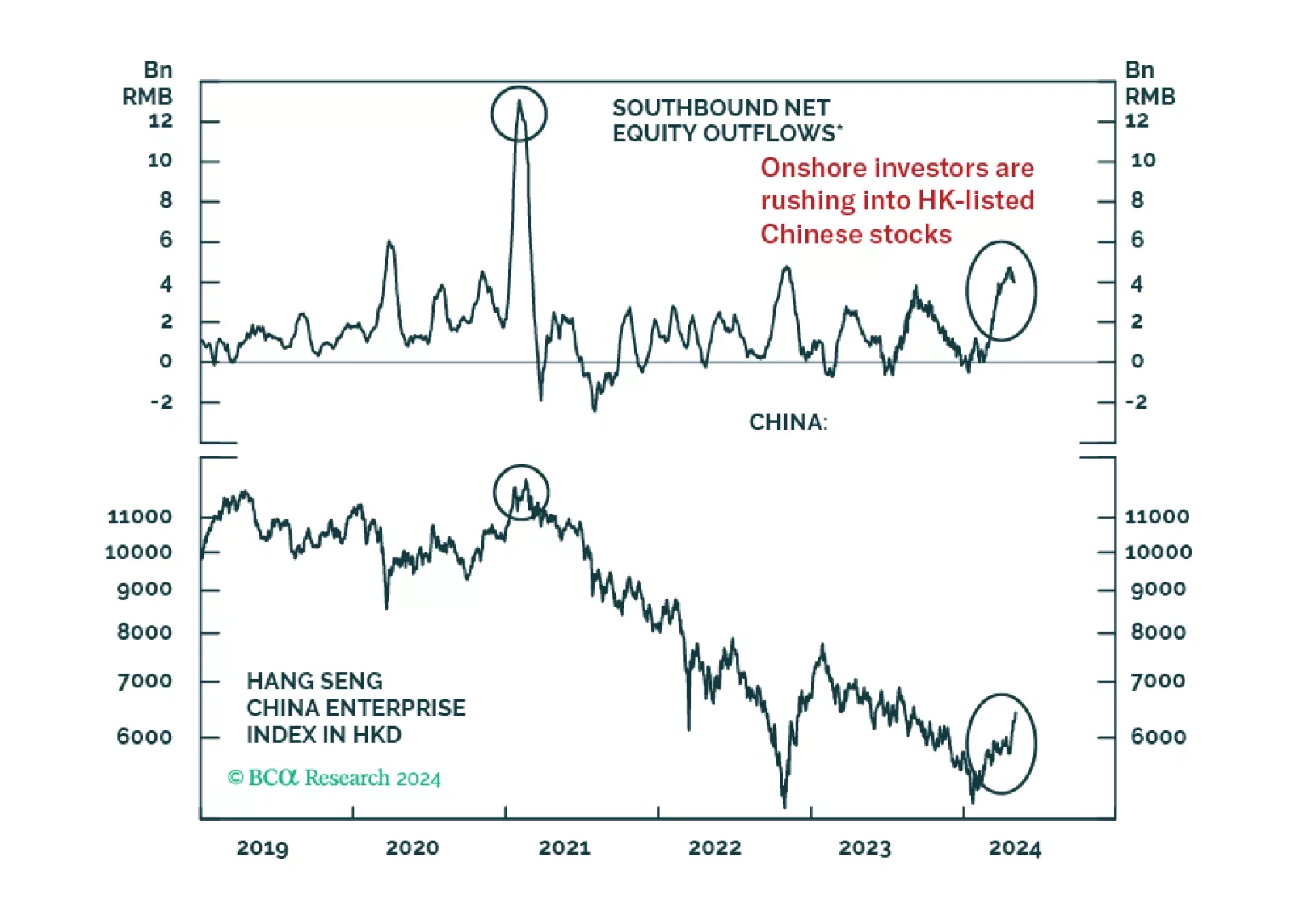

Mainland residents’ investments in gold, other metals, and Hong Kong-traded stocks are a form of capital outflow. Chinese authorities will counter any excessive capital flight with stricter administrative controls. Thus, markets benefiting from these flows will likely be hurt.

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

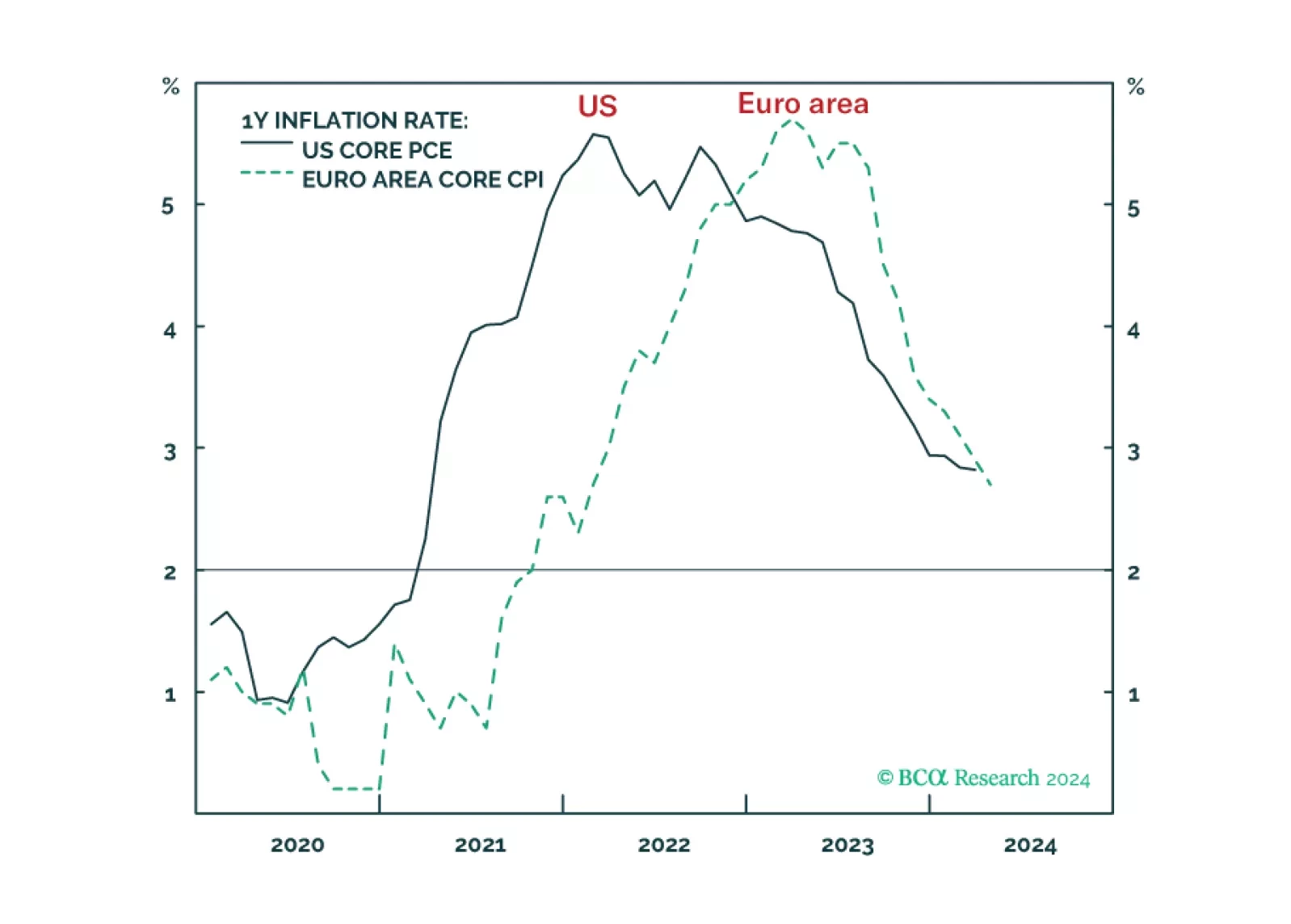

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.

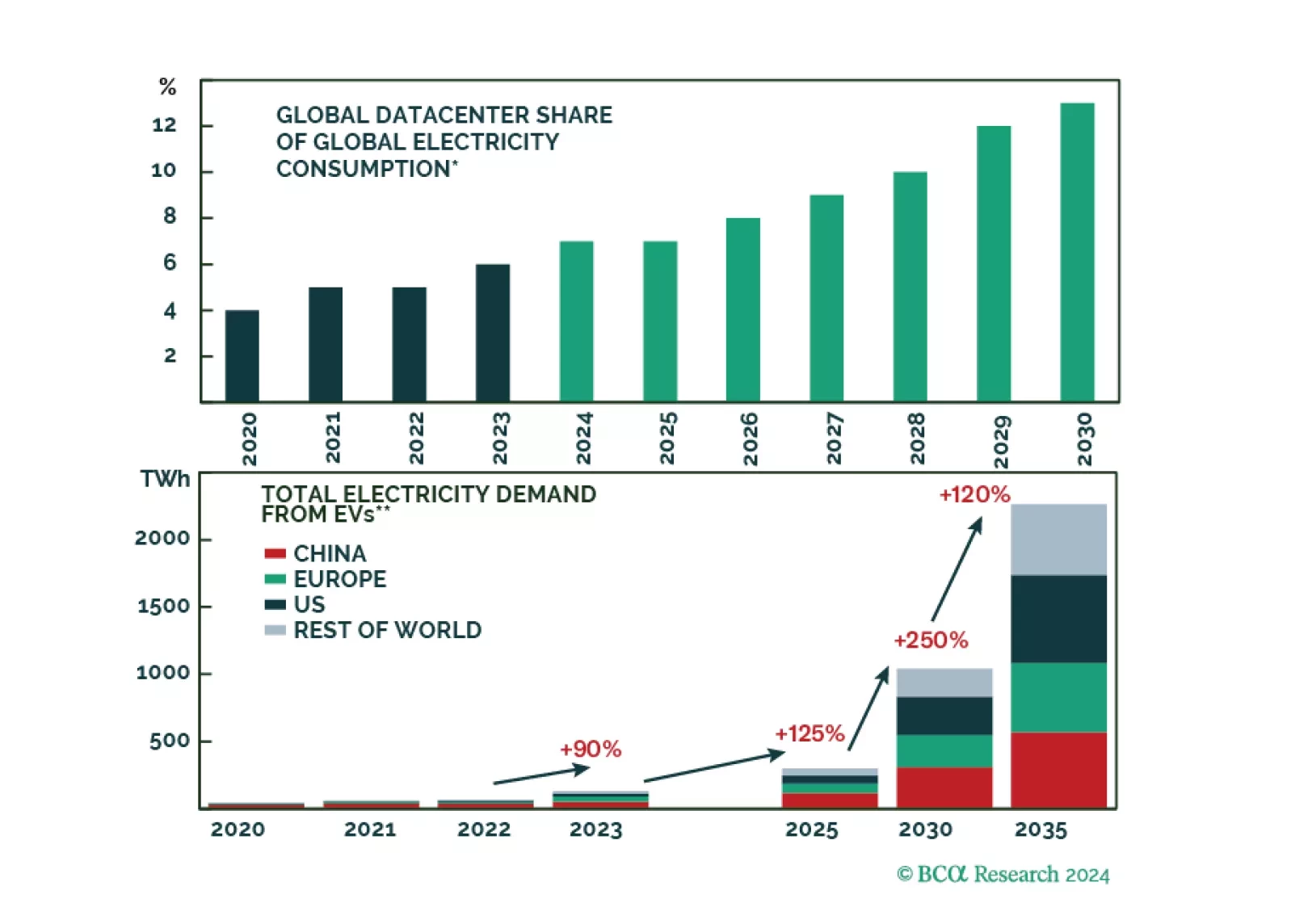

AI, EVs, and reshoring will lead to a massive surge in demand for electricity. Carbon-free, cheap, baseload nuclear energy stands to greatly benefit from these megatrends going forward.

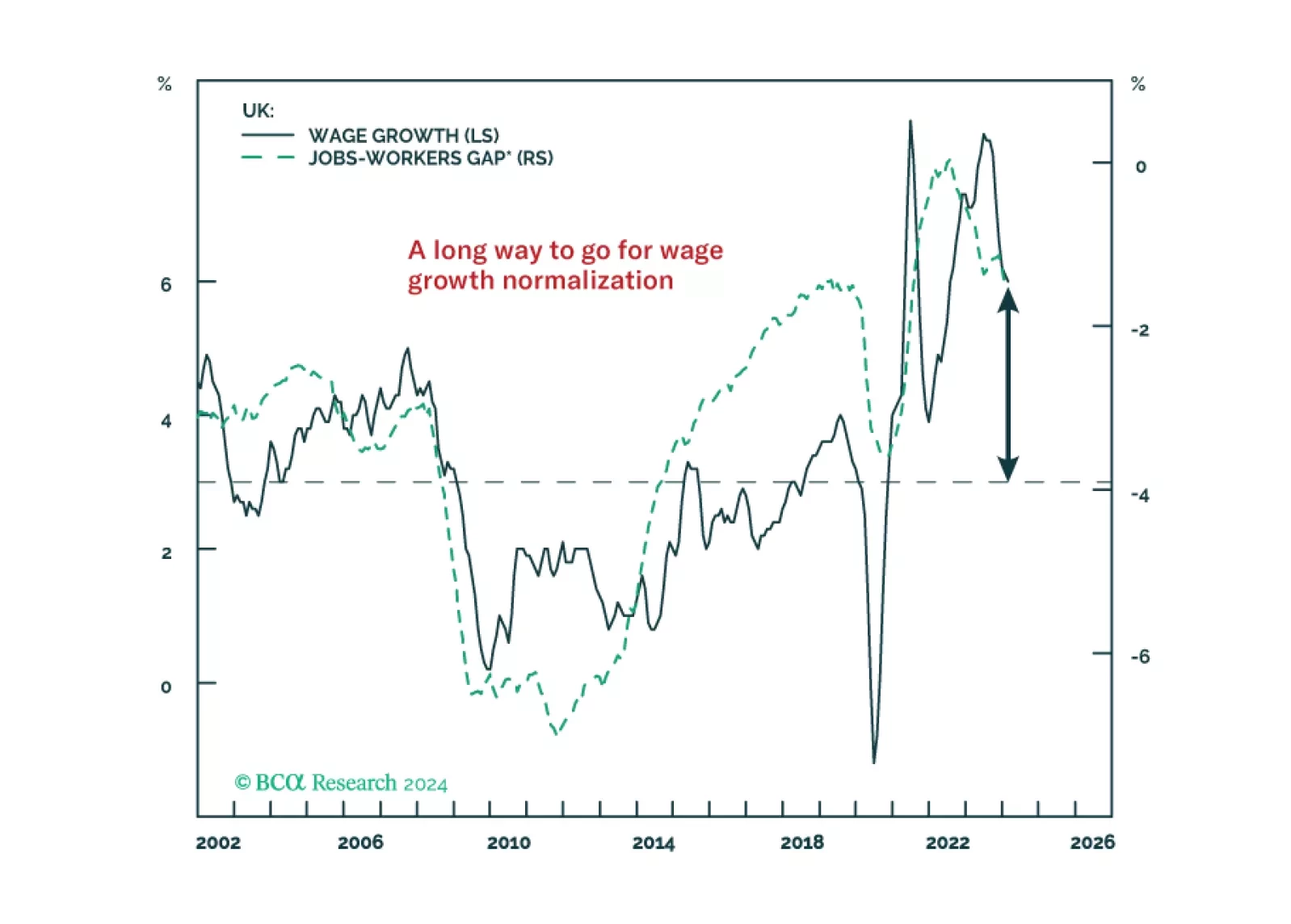

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

China’s economy is cruising at a very low altitude. The odds are that China’s equity rebound is running out of time. The RMB will continue to depreciate versus the US dollar in the coming months, albeit the pace may be modest.

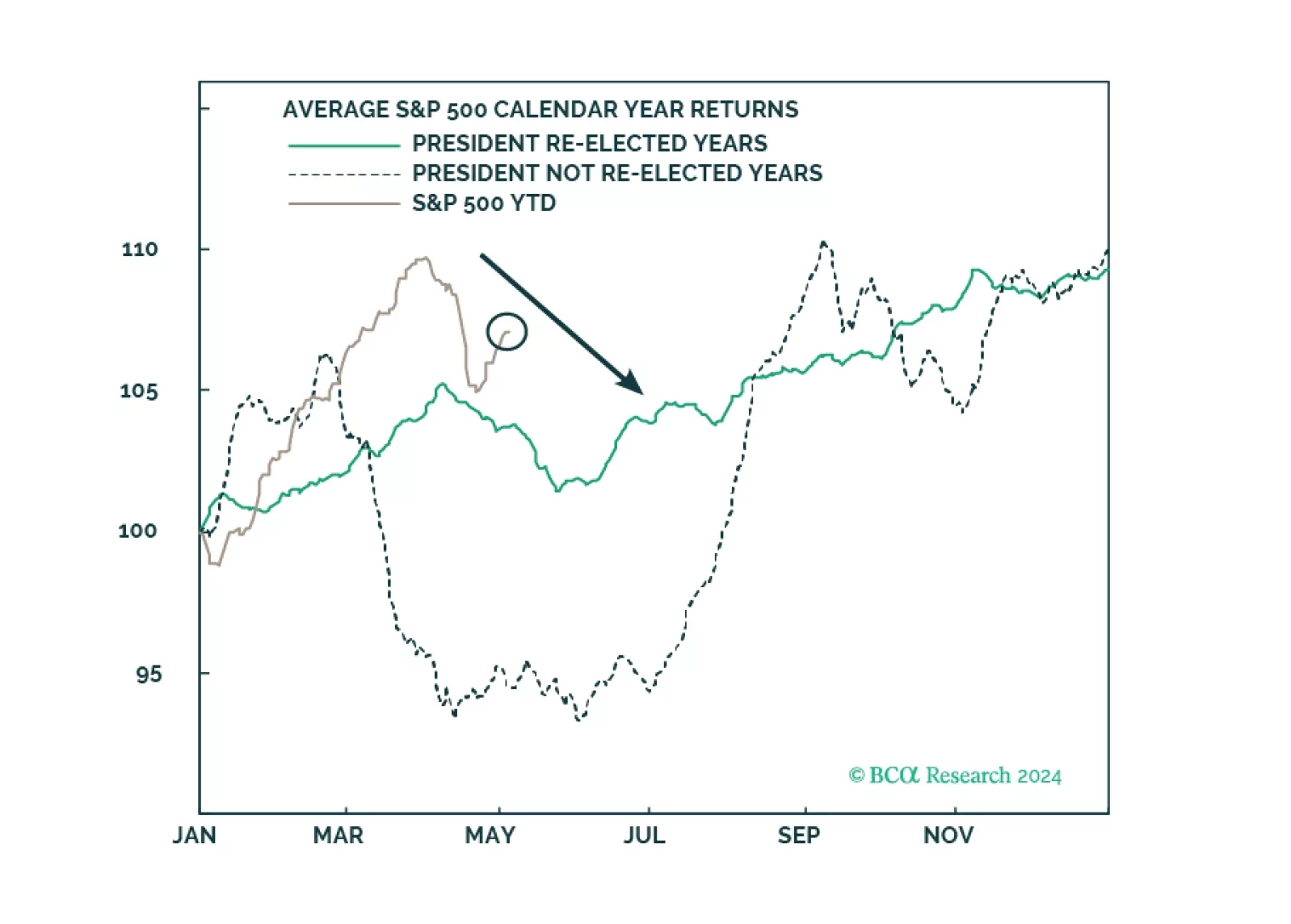

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.

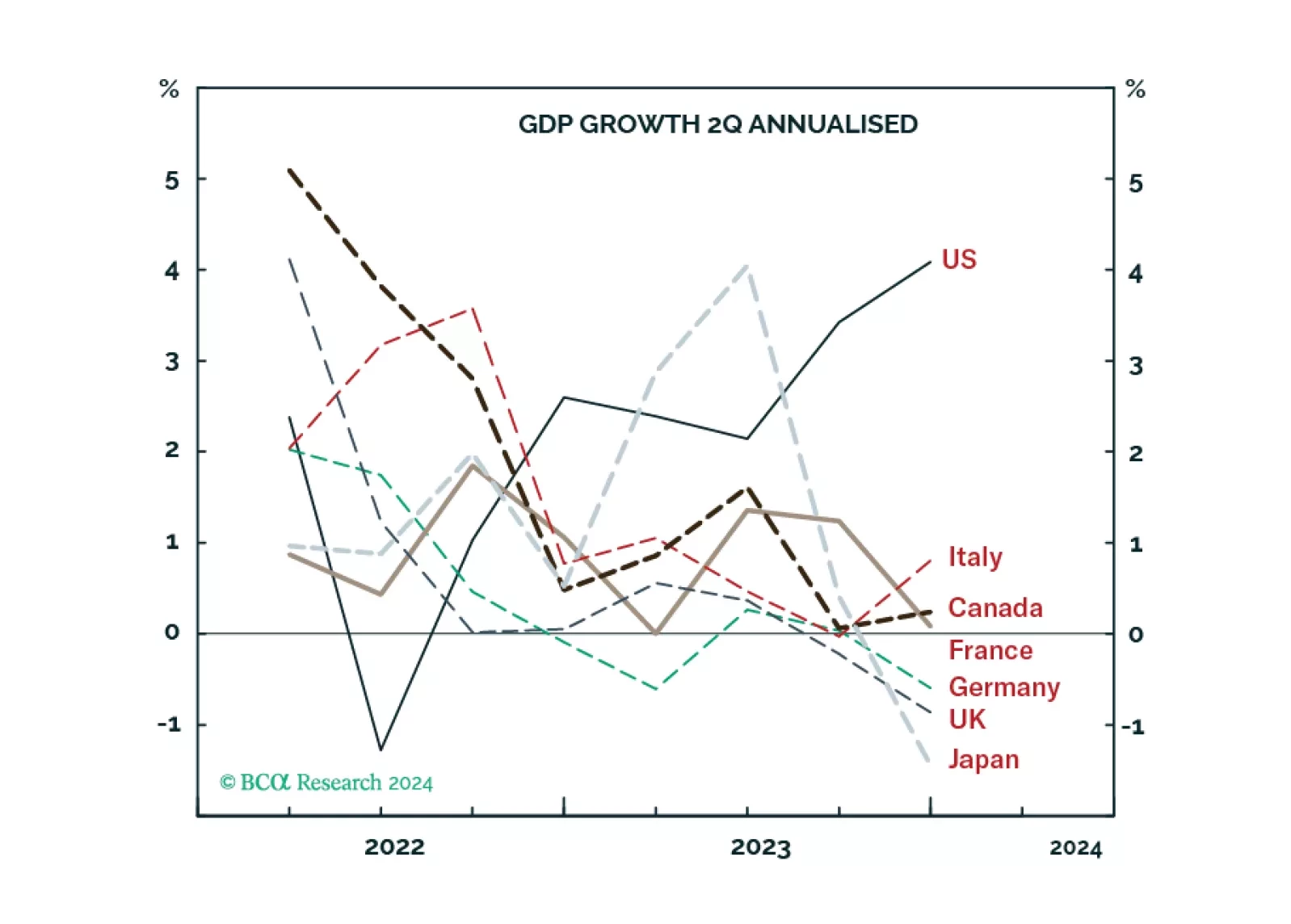

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

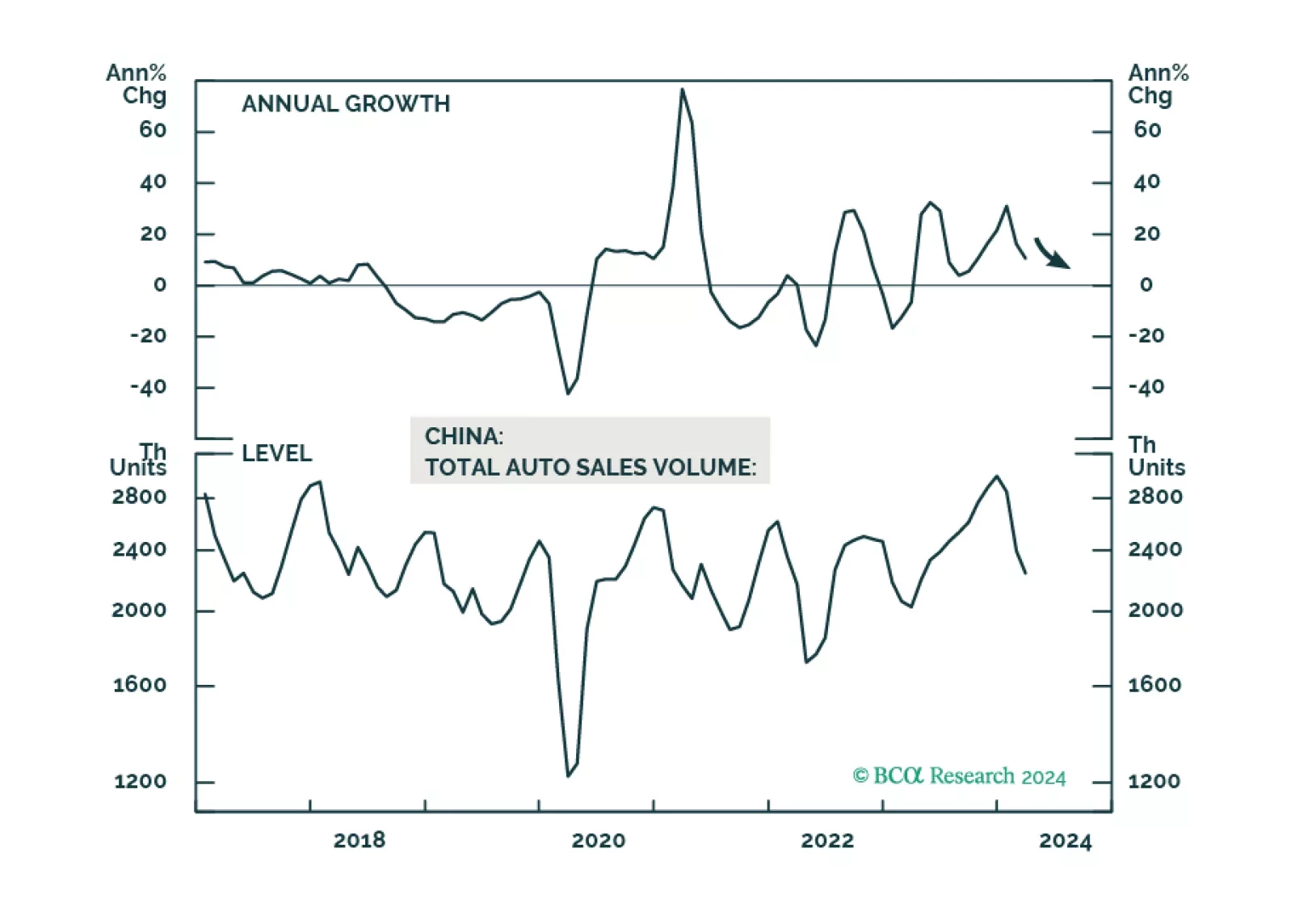

This year’s cash for clunkers program will have only a mildly positive impact on domestic demand for automobiles and home appliances in China. In the meantime, the equipment renewal program will prop up domestic manufacturing moderately as well as help the country reduce its reliance on high-end equipment imports. We recommend continuing to overweight onshore auto stocks relative to the A-Share Index.

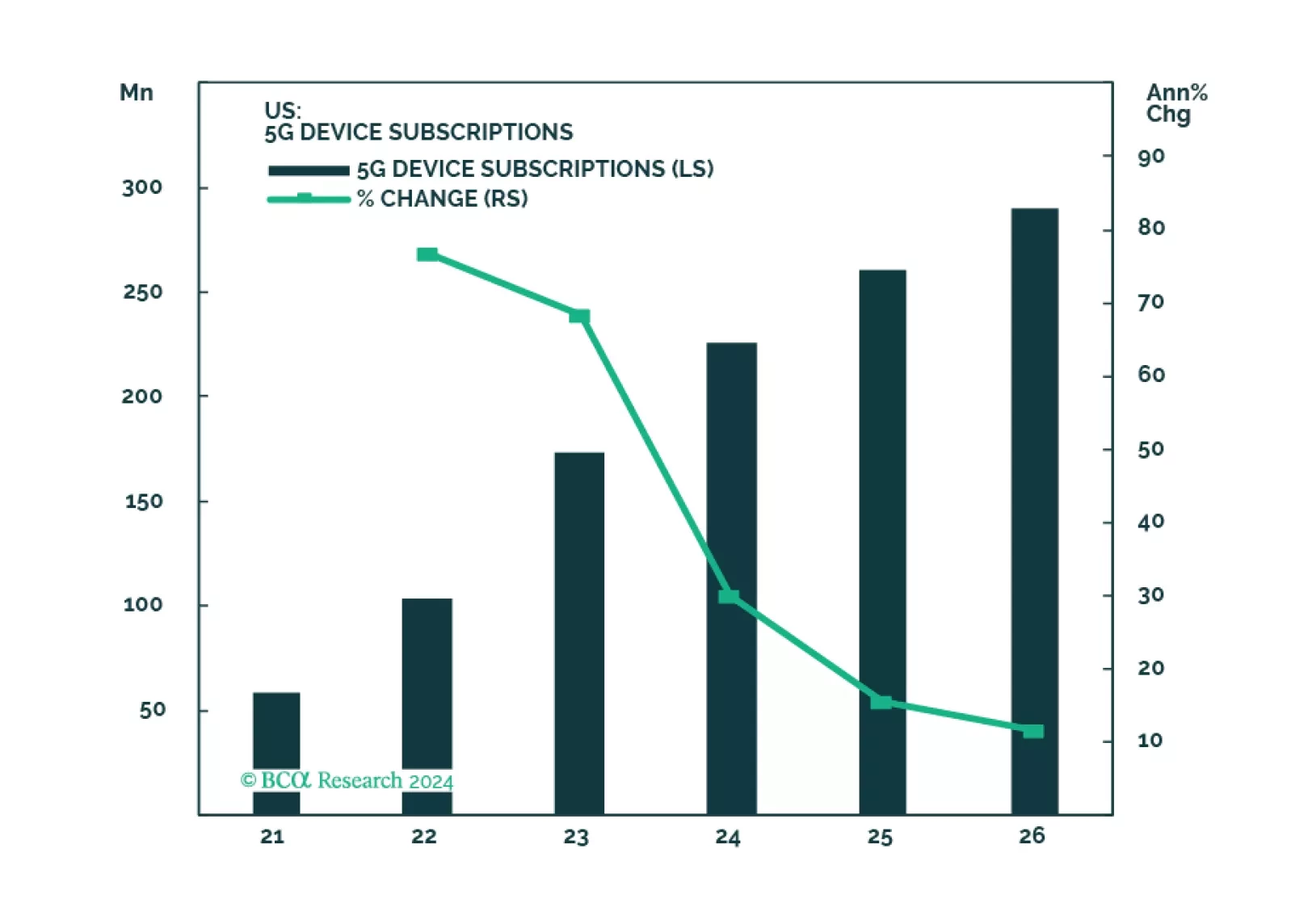

The Telecoms industry is highly concentrated, and carriers compete on price and quality of service in a slow growing market. Demand for capex is relentless. The roll out of 5G has disappointed. Recently, capex outlays have slowed, and operating cash flow has rebounded. Further, Telecoms is a quintessential defensive industry that will outperform during a market pullback.