Mega Themes

The Q1-2023 earnings season has surprised as companies’ results point to the end of the earnings recession. However, the good news is already priced in – the market has barely budged over the past six weeks. Earnings rebound may continue as long as the economy avoids a recession. However, inevitably, tighter monetary policy will weigh on demand, and recovery will come to a halt.

The outlook is downbeat for the share prices of both onshore and offshore Chinese property developers in absolute terms, and relative to China’s overall equity benchmark. A marginal increase in housing construction activities in the rest of this year implies that there will be not a meaningful recovery in the demand for commodities, such as iron ore, steel, cement and glass.

In this *Special Report*, we analyze the dollar’s reserve status within the context of geopolitical crosscurrents. In our view, there is more than meets the eye when betting on the end of the dollar’s reserve status.

Financial commentators, politicians and policymakers have increasingly been blaming stubbornly high inflation on companies pursuing aggressive pricing strategies to boost earnings and margins. In this Special Report, we investigate the concept of “greedflation” – companies persistently raising prices faster than costs are increasing to pad profit margins - and see if the associated conclusions about corporate pricing power and inflation are borne out by the data in the US, euro area and UK.

Global growth will weaken in the coming months, yet monetary authorities worldwide will be reluctant to ease policy. This state of affairs foreshadows a clash between markets and policymakers in the months ahead. China’s recovery is losing steam. The latest divergence between Emerging Asian and LATAM currencies will not last.

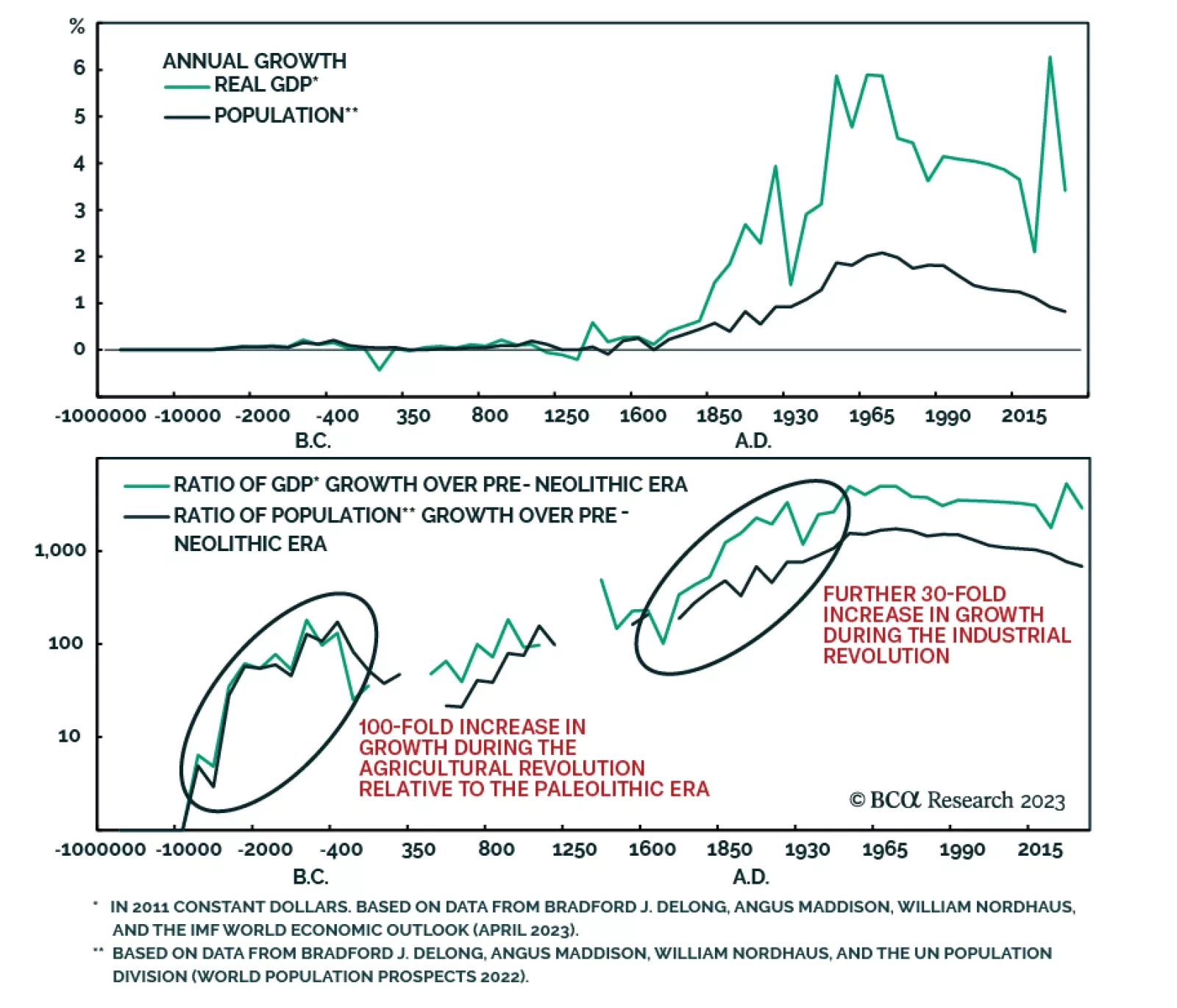

The conventional economic thinking about the likely impact of AI is misguided because it extrapolates linearly from what AI can do today to what it can do tomorrow. Just as the investment community and the broader public were blindsided by the exponential rise in Covid cases during the early days of the pandemic, they will be blindsided by how quickly AI transforms society and the economy.

The conventional economic thinking about the likely impact of AI is misguided because it extrapolates linearly from what AI can do today to what it can do tomorrow. Just as the investment community and the broader public were blindsided by the exponential rise in Covid cases during the early days of the pandemic, they will be blindsided by how quickly AI transforms society and the economy.

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.