Mega Themes

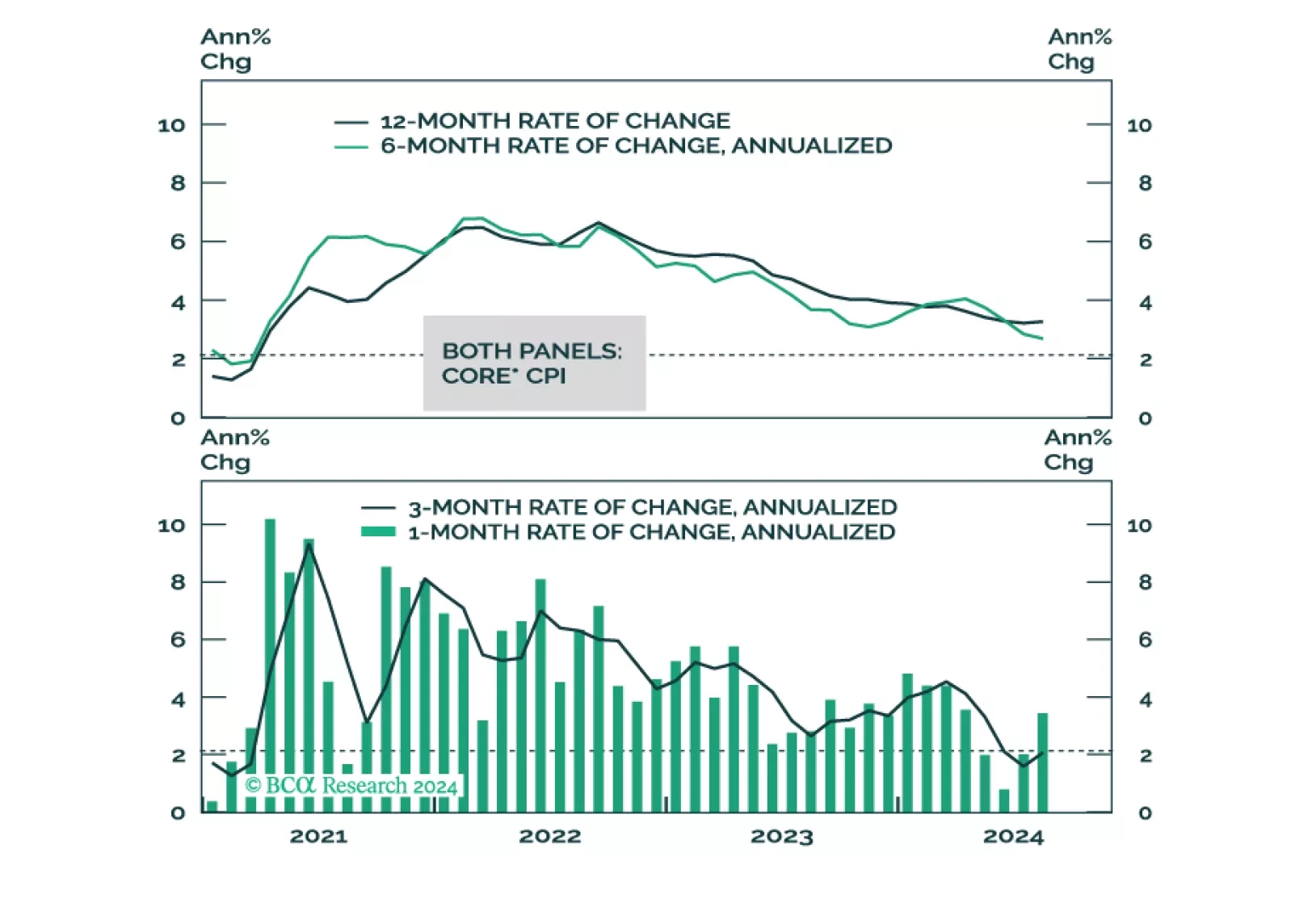

Our reaction to this morning’s CPI report and what it means for Fed policy.

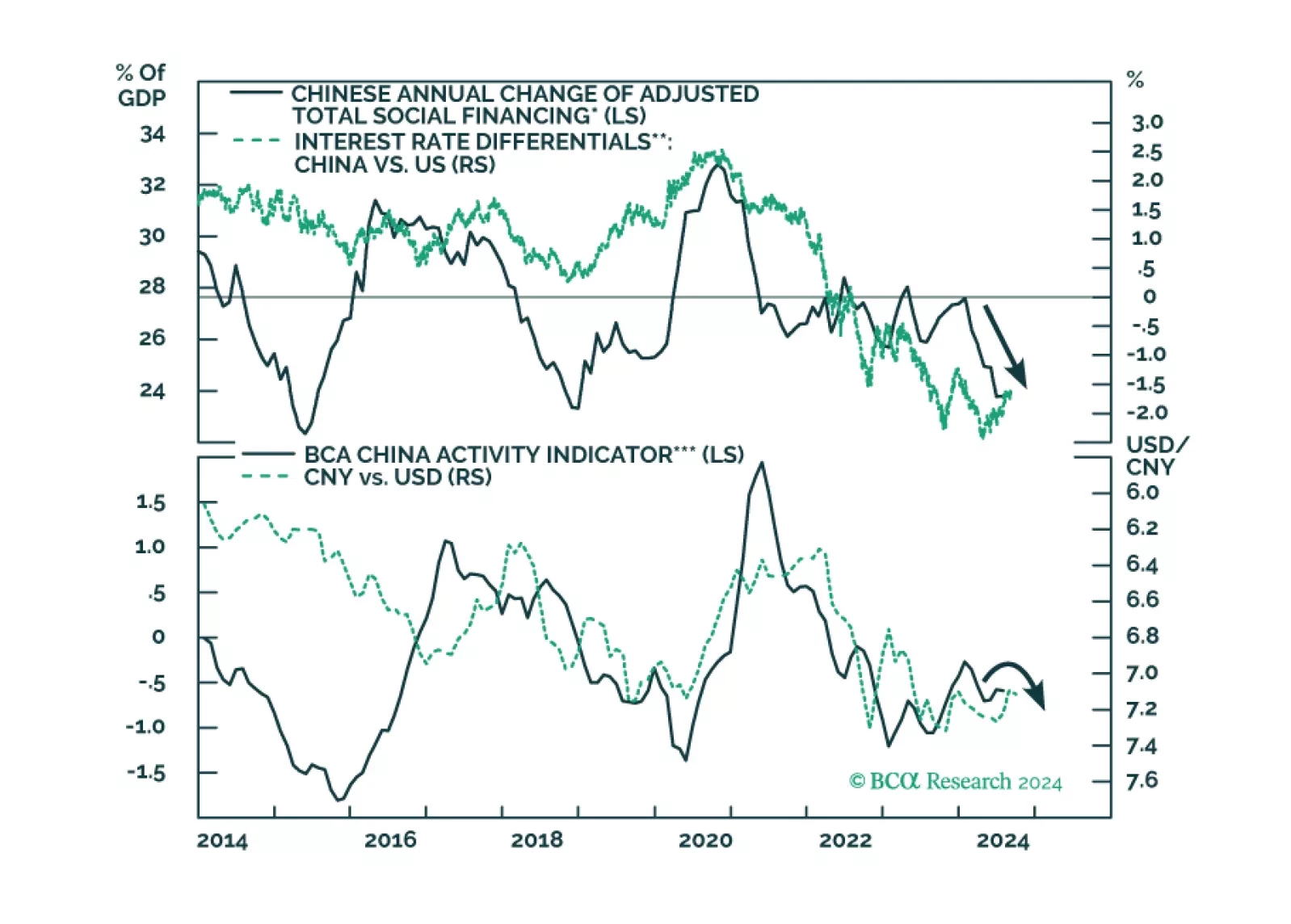

Both the Chinese and US central banks will likely take policy actions in the coming weeks. What is the potential impact of a mortgage rate cut on China’s household consumption and the broader economy? Will the anticipated Fed easing cycle further lift the RMB exchange rate versus the US dollar?

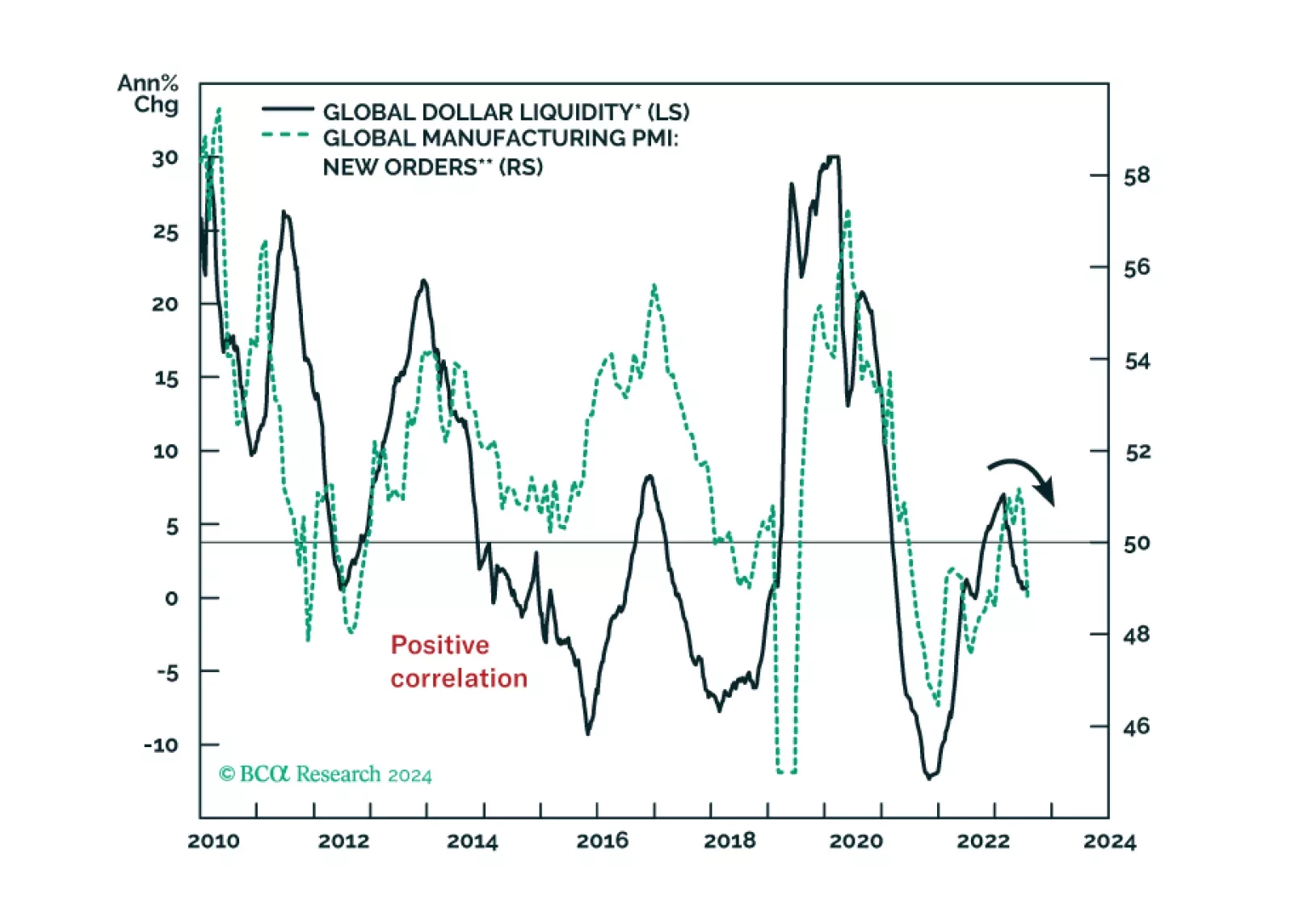

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

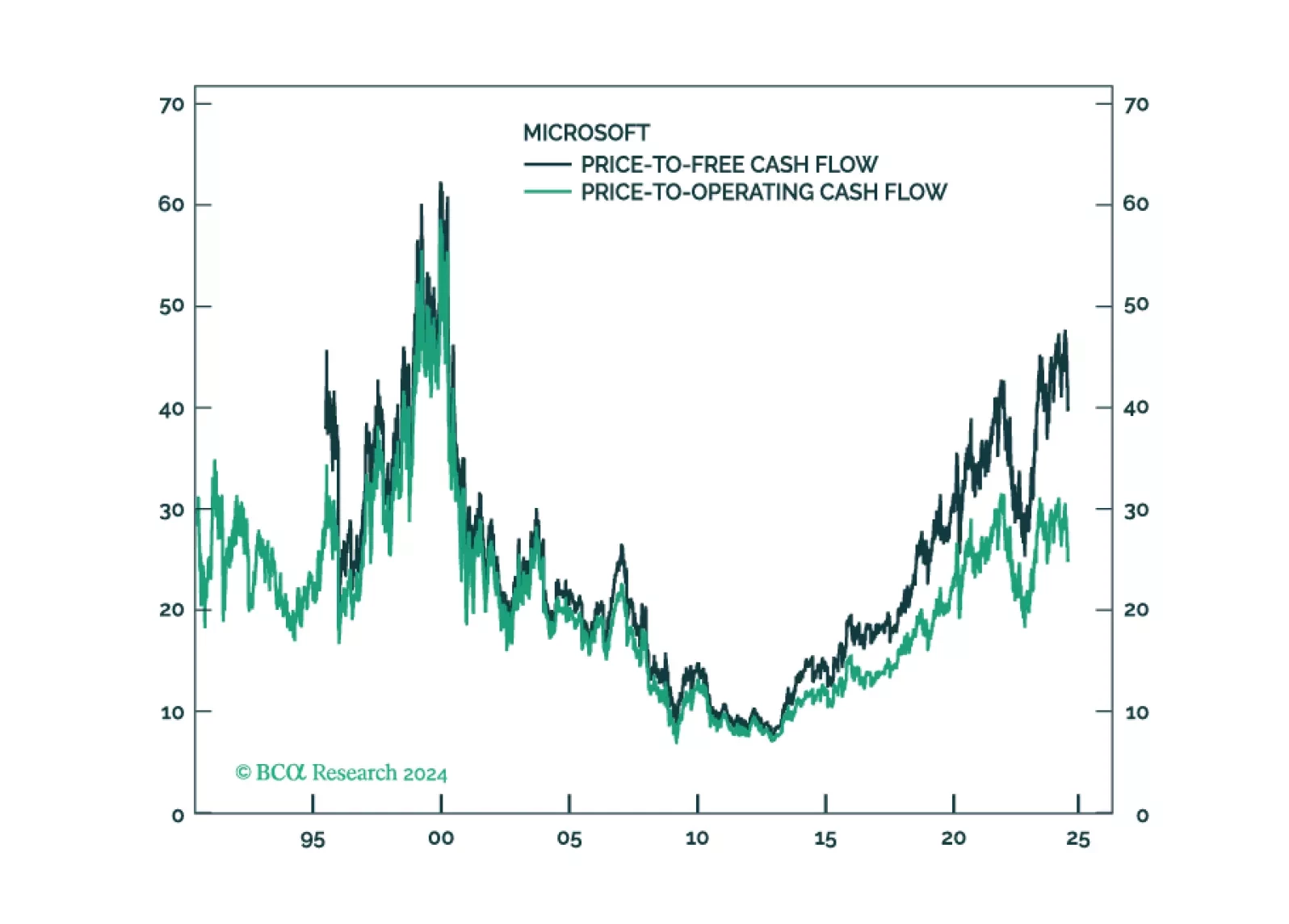

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

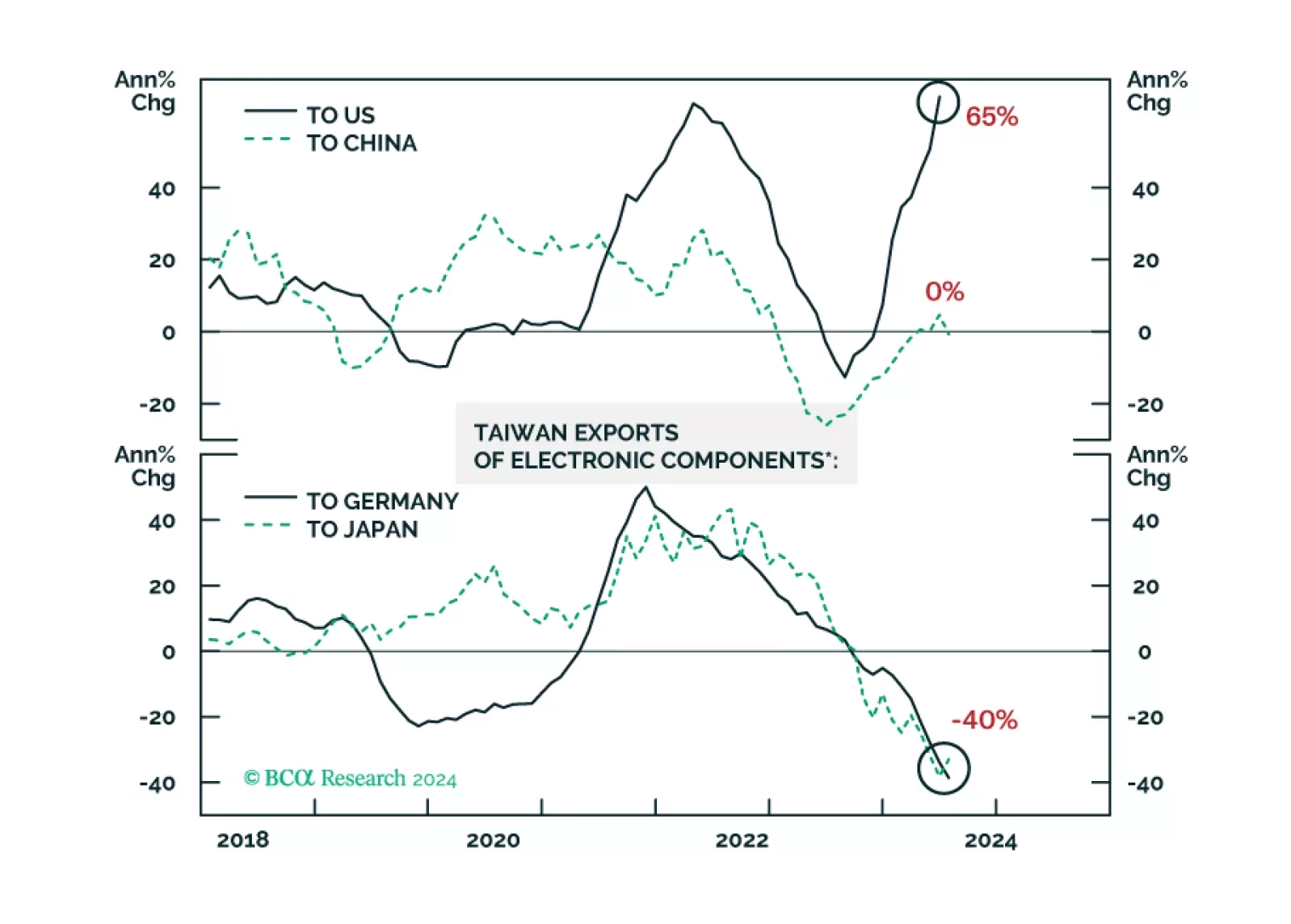

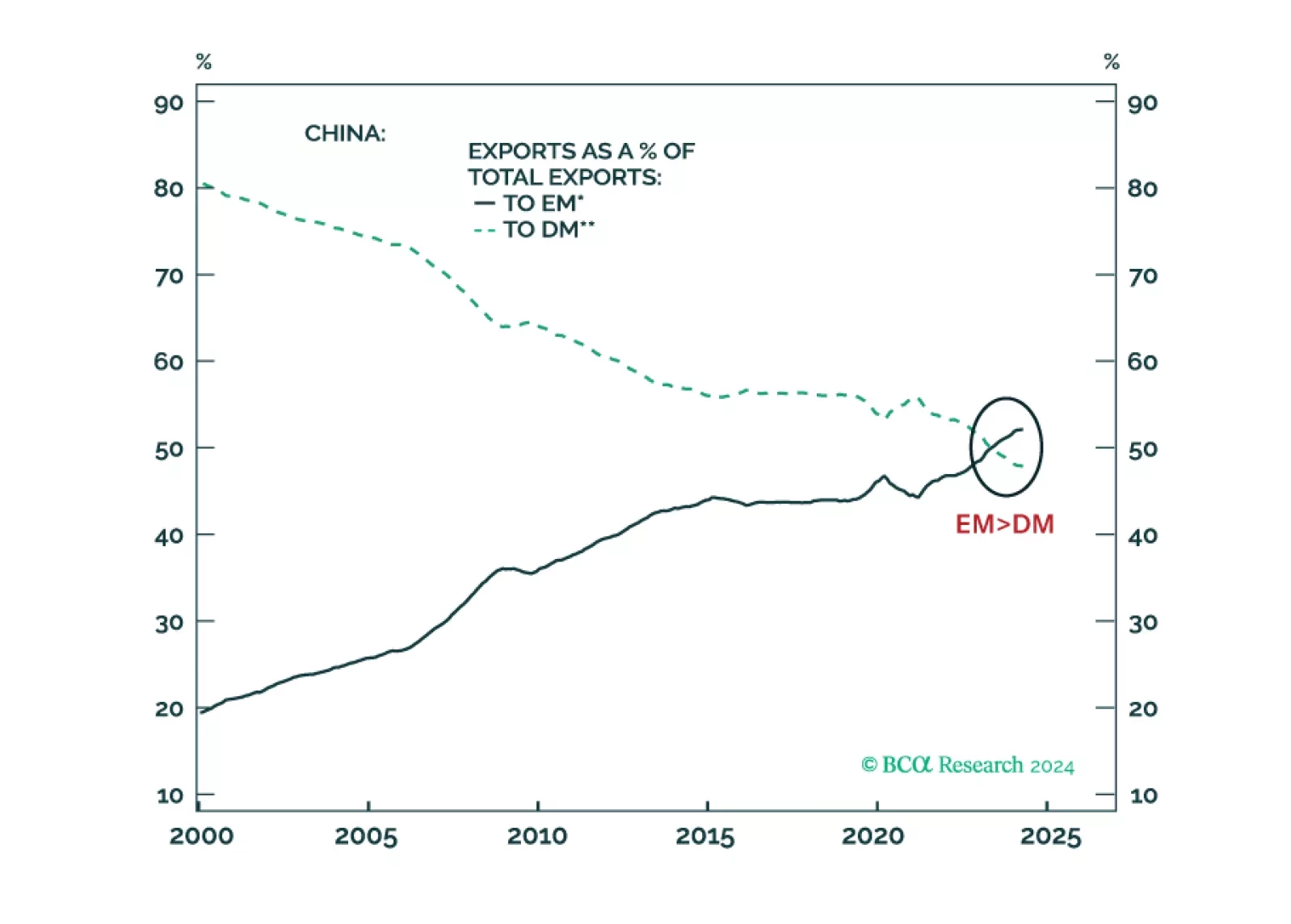

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

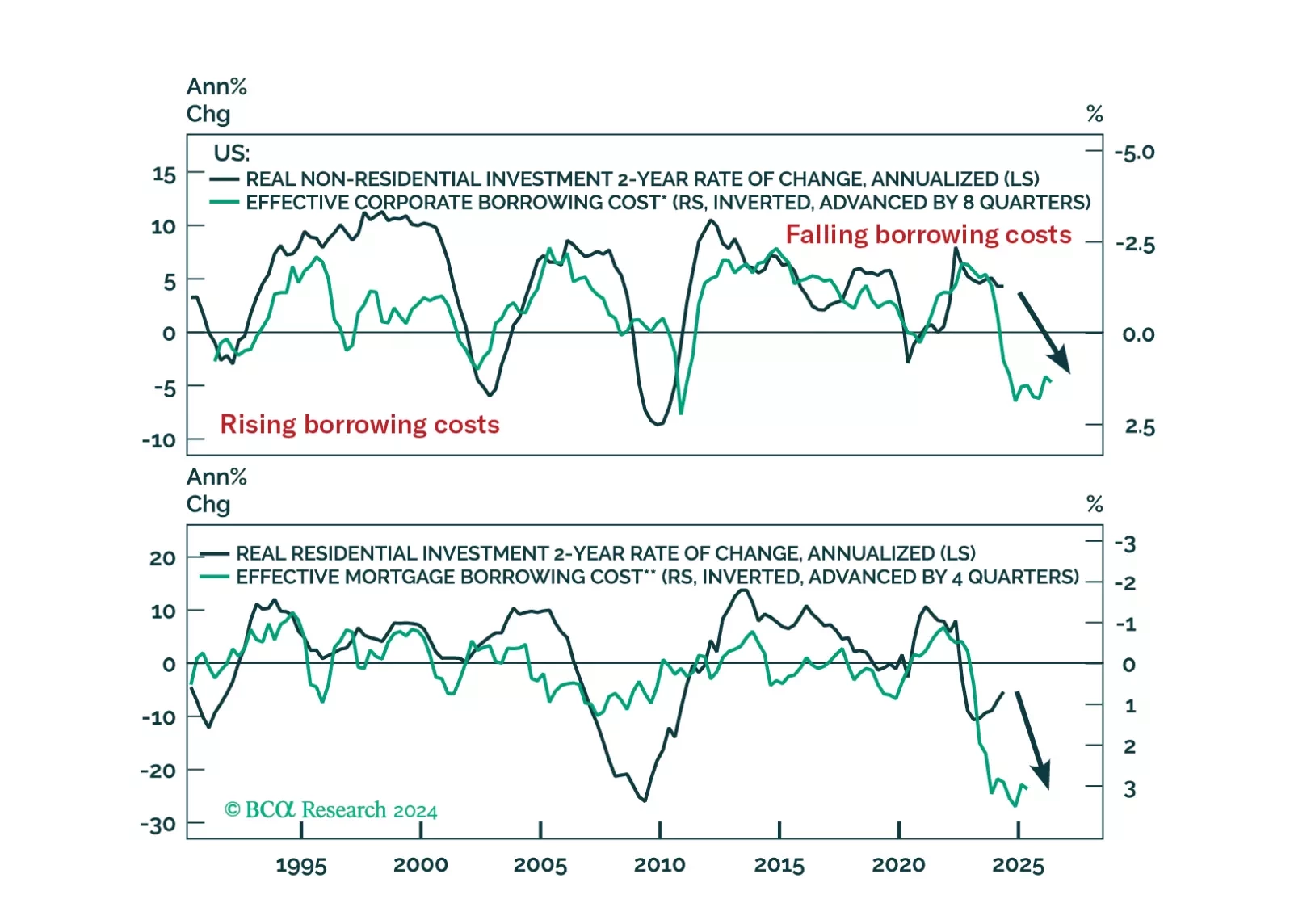

In this Special Report, we assess the impact of monetary policy tightening on major economies. Interest rate sensitive GDP already slowed significantly in response to the aggressive rate hiking cycle. Despite the beginning of policy easing, our forward-looking indicators suggest monetary policy will continue to weigh on the economy.

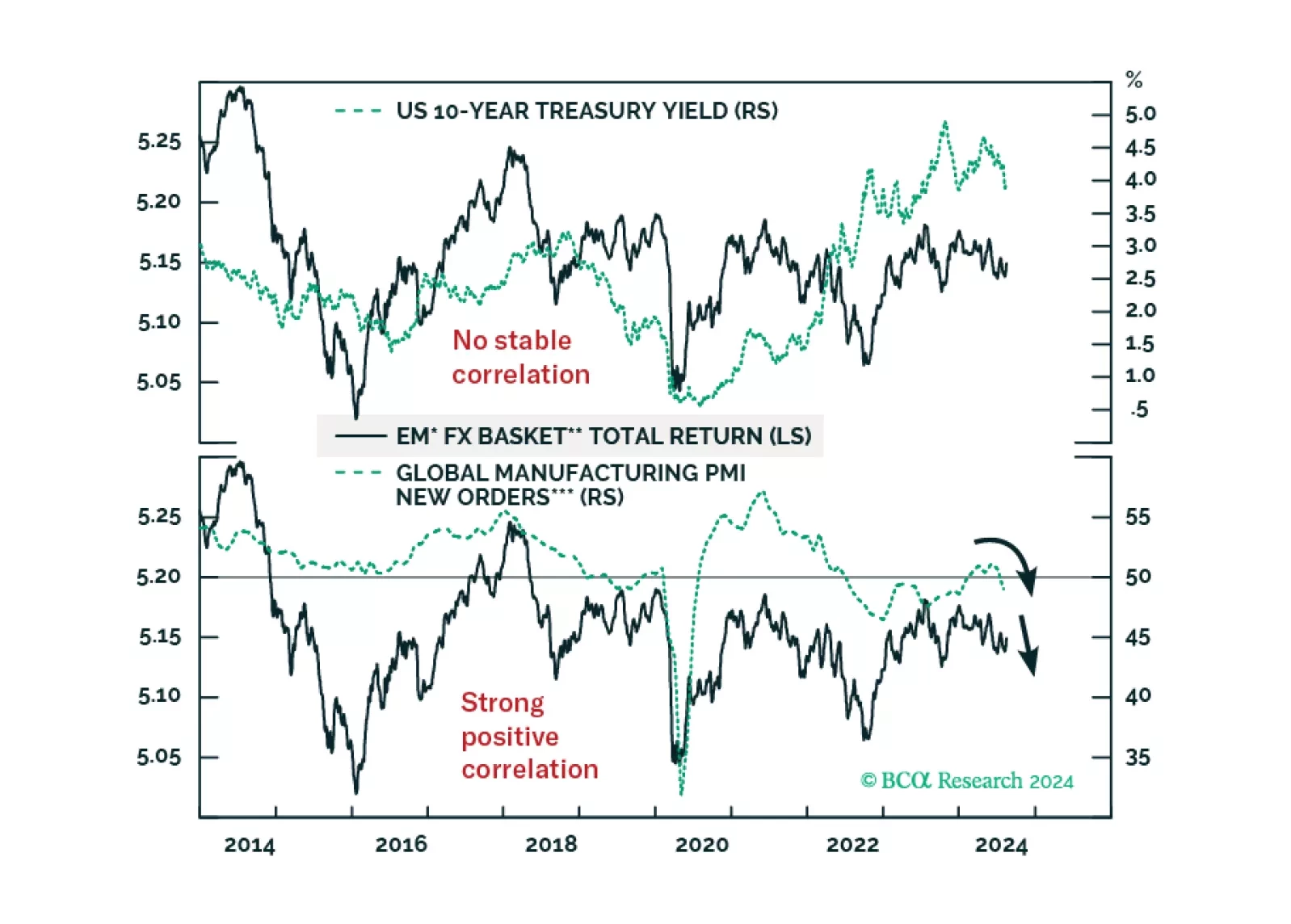

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

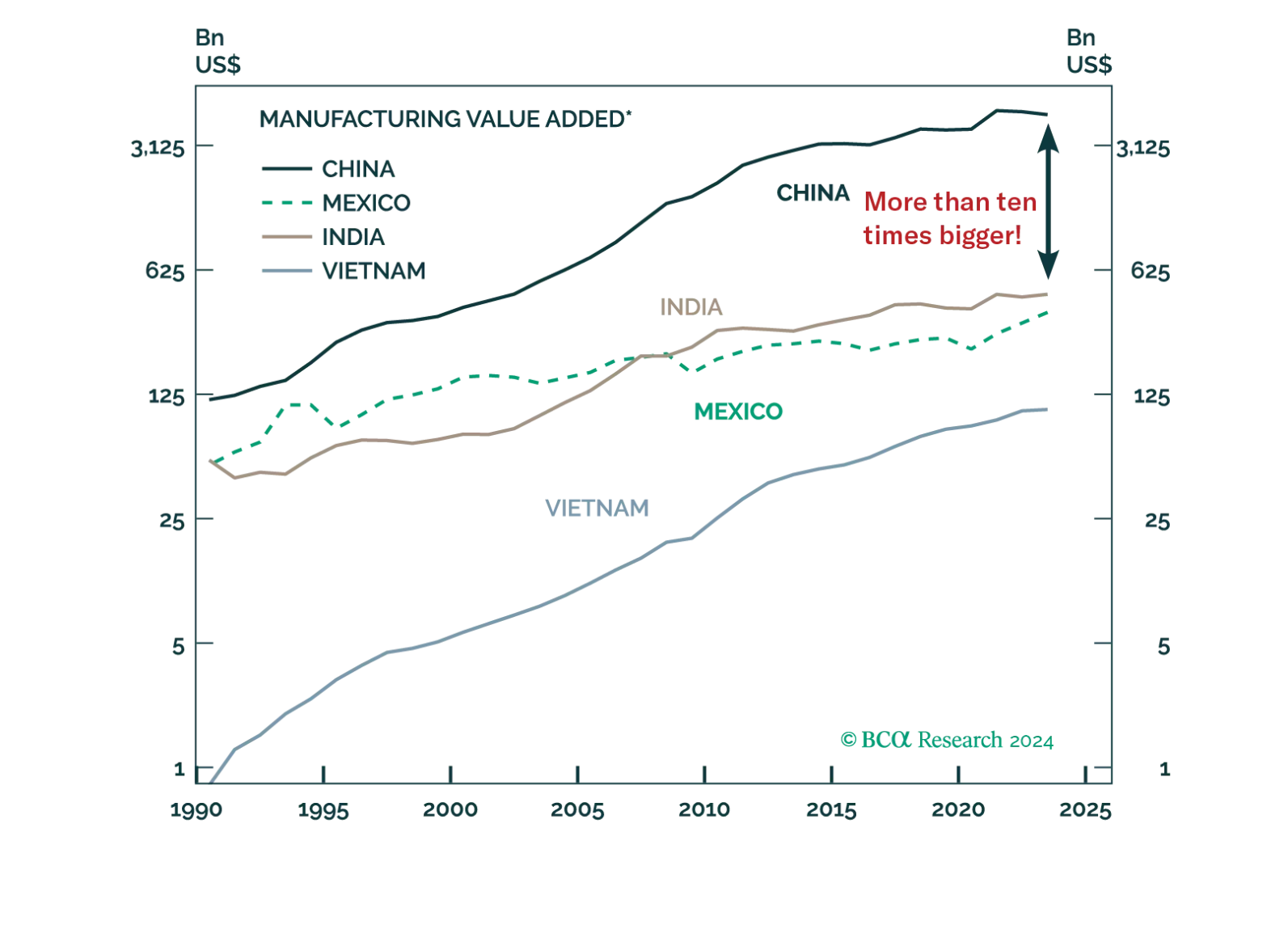

Multinationals are attempting to expand their supply chains beyond China, but the relocation process has been slower than expected. In the coming years, however, geopolitical tensions, changes in China’s business environment, and rising competition from Chinese producers could accelerate multinationals' departure from China.

Over the past few weeks, global equities have been hit by rising scepticism over the bullish AI narrative and increasing concerns over global growth. Stocks should stabilize in the near term, but the medium-term direction is to the downside. We expect the S&P 500 to drop to 3750 in 2025 and the 10-year Treasury yield to fall to 3%.