Mega Themes

On one hand, China will be exporting deflation to the rest of the world. On the other hand, core inflation is sticky in the US, making the Fed err on the hawkish side. Altogether, these crosscurrents are creating a toxic mix for risk asset prices.

Markets continue to be tossed to and fro by central-bank policy, and risks of higher commodity prices. These are due to fiscal stimulus and exogenous weather and war-related risk, which could send food and energy prices higher this winter. We remain long gold outright, energy and metals producers via the XOP, XME and PICK ETFs, direct commodity exposure via the COMT ETF, and futures exposure to backwardation in copper (long 4Q23 copper futures vs. short 4Q24 copper futures).

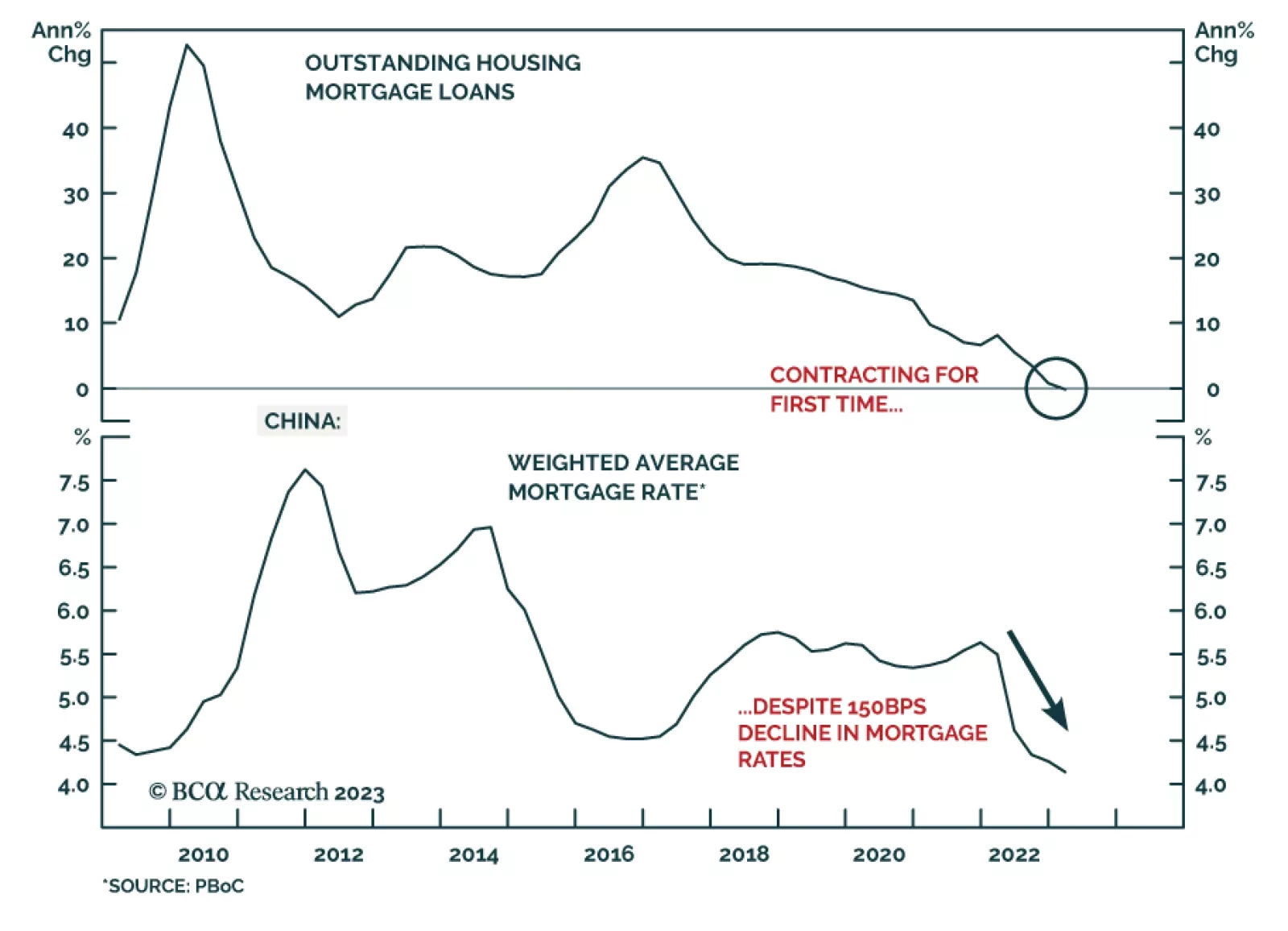

The recovery of China’s industrial profits is set to disappoint in 2H 2023. Corporate profits are more sensitive to changes in prices than volumes. Given producers’ selling prices will keep deflating through 2023, industrial profits will only stabilize at a very depressed level even with a mild improvement in volume. A disappointing recovery in industrial profits entails more downward risks for A-share prices in absolute terms. Chinese 10-year bond yields are set to drop to a record low.

The world economy is likely already in recession, defined as world growth dipping to sub-2 percent. So far, the world recession has been China-led, but in the coming months it will change to being developed economy-led. Hence, while metals and industrial commodities may get some brief respite, high yield credit and stocks will underperform government bonds. New tactical recommendations are to overweight French luxury goods versus US tech, and to overweight USD/COP.