Mega Themes

Stay cautious on Chinese stocks. Equity investors should use any rebound in onshore stock prices to downgrade A-shares from overweight to neutral within global and EM equity portfolios. Remain underweight Chinese investable/offshore stocks. Onshore bond yields will drop to all-time lows. Continue receiving 10-year swap rates. The currency will continue depreciating versus the US dollar in the coming months.

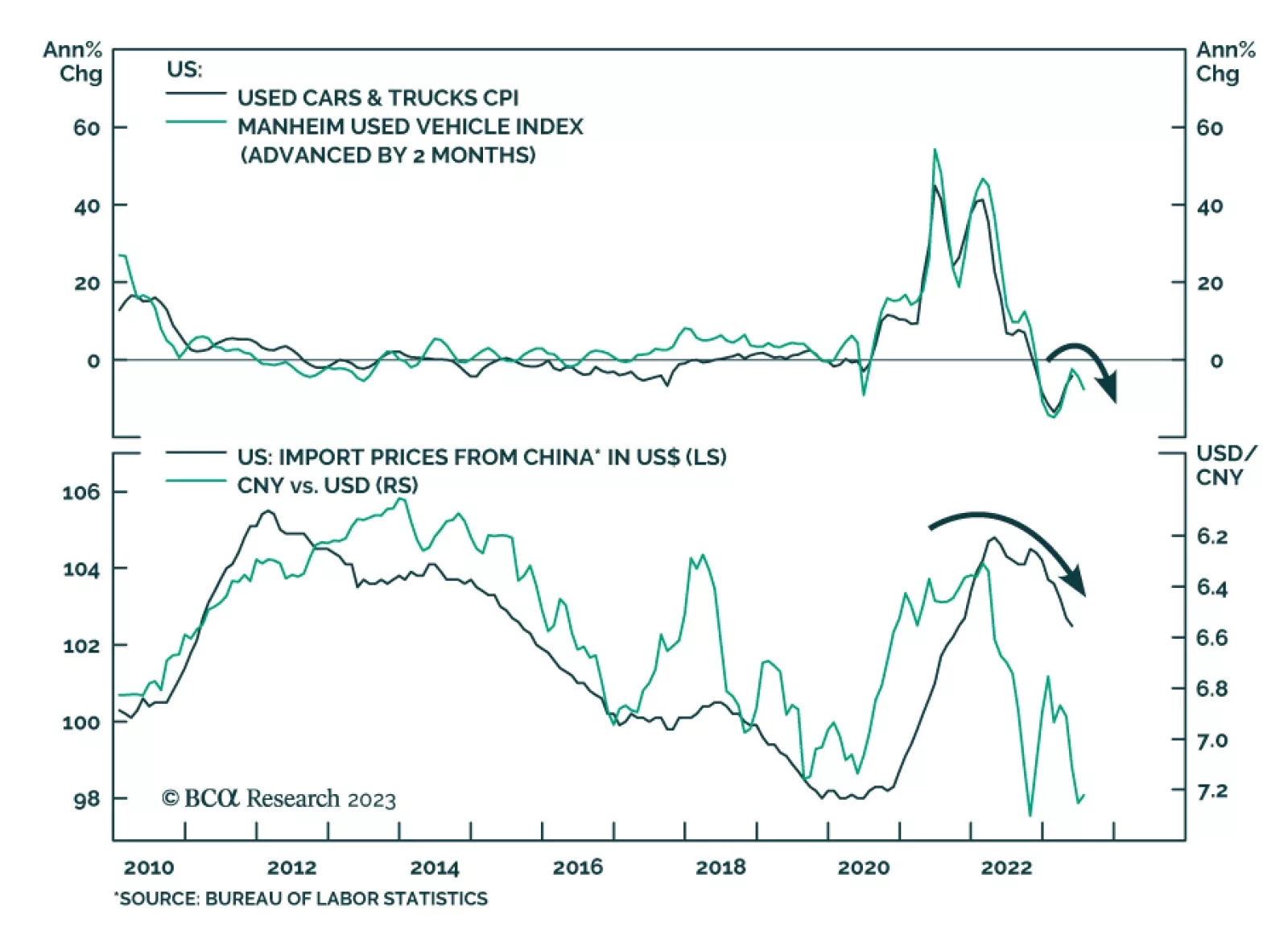

China’s economy is cruising at a very low altitude where gravity forces are intense. Downbeat consumer and business sentiment will reduce the effectiveness of stimulus. Anything short of “irrigation-style” stimulus will be insufficient to boost growth. We remain cautious on Chinese stocks. Onshore bond yields will drop to an all-time low. The RMB is still vulnerable against the USD in the next few months.

In this report, we present our performance review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for the Q2/2023, and the outlook and scenario analysis for the next six months. The portfolio return exactly matched that of the benchmark index during the quarter, as modest gains on government bond allocations in the US, UK and core Europe completely offset losses on spread product underweights. Looking ahead, the portfolio is positioned to capitalize on an expected slowing of global growth over the rest of the year through an overweight stance on government bonds versus spread product and above-benchmark duration tilts in the US and core Europe.

In this report, we dissect which markets have broken out and which ones have not, and reflect what this entails for our global macro view. Also, we analyze how the S&P 500 has been taking its cues from a change in the inflation trend. Yet, inflation dynamics are complex, and a falling inflation rate does not mean that the inflation menace has been eliminated.

Both EV and Green Energy themes still hold strategic promise for investors, posing large upside, despite prevailing macro headwinds. While both themes have yet to claw back their pandemic peaks, a broadening of the rally supports a run for both, even in the face of high valuations.

Global oil demand growth is tracking with our estimate of ~ 1.8mm b/d for this year. Supply discipline is being maintained by OPEC 2.0, where the core (KSA and the UAE) and Russia have reduced production by ~ 240k b/d yoy in 1H23. In addition, KSA extended its unilateral production cut of 1mm b/d from July into August. We expect inventory draws in 2H23 as supply stays below demand. Our Brent forecast remains unchanged at $92/bbl this year, and $120/bbl next year. We remain long the COMT and XOP ETFs.

An outlook for inflation and Fed policy following this morning’s CPI report.

The stratospheric valuation of this year’s AI mania is likely to deflate, just as it did after the Web 1.0 mania of the late 90s. We go through some long-term and short-term investment implications.

The Politburo meeting in late July will set the course for economic policy for 2H23. We think China will only resort to "irrigation-style" stimulus if something breaks in the economy and/or financial markets. Furthermore, the gradual and targeted rounds of stimulus are unlikely to boost economic activity considerably. The reasons are the diminished efficacy of the monetary transmission mechanism and the unique features and constraints of the nation’s fiscal system.