Mega Themes

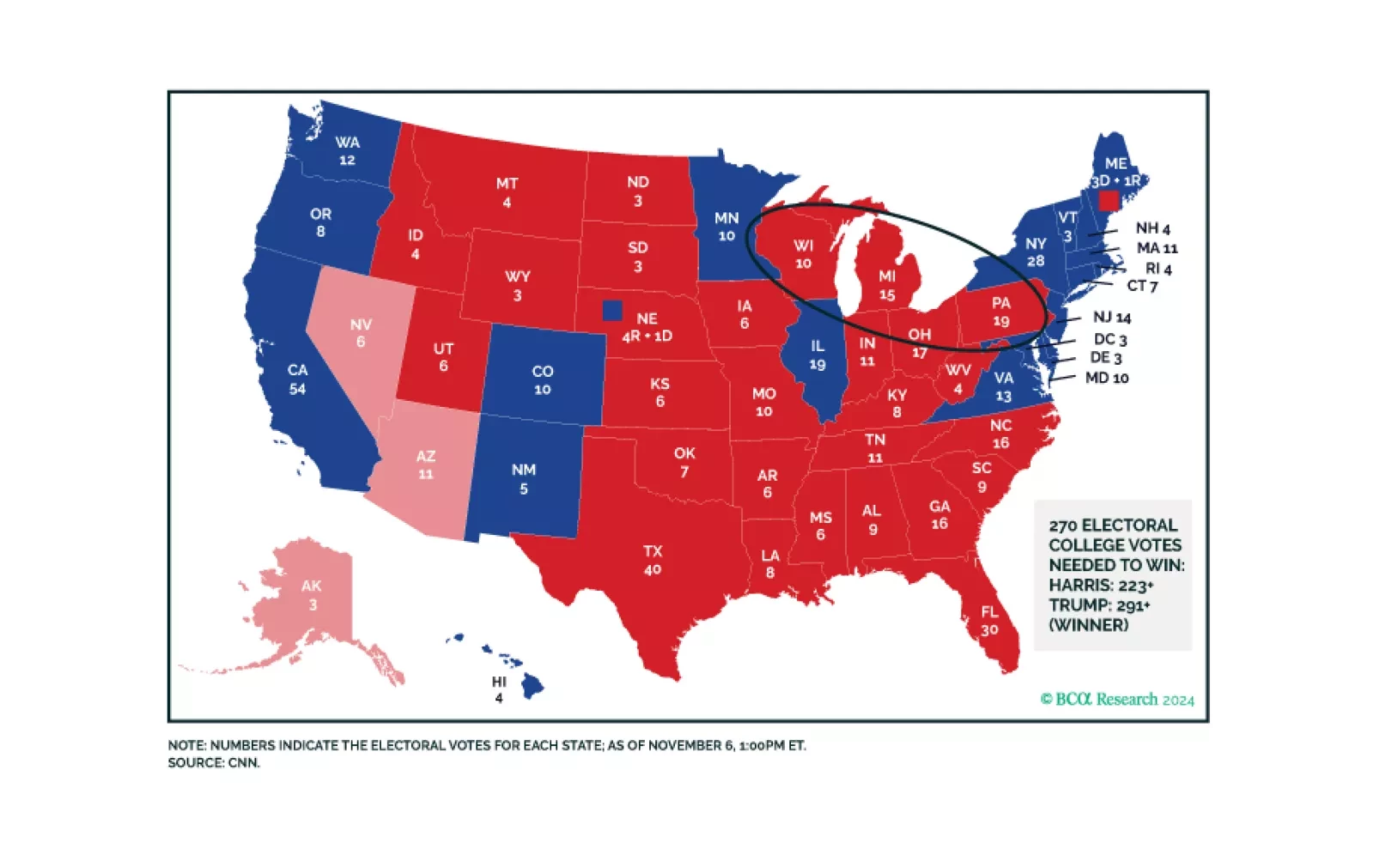

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

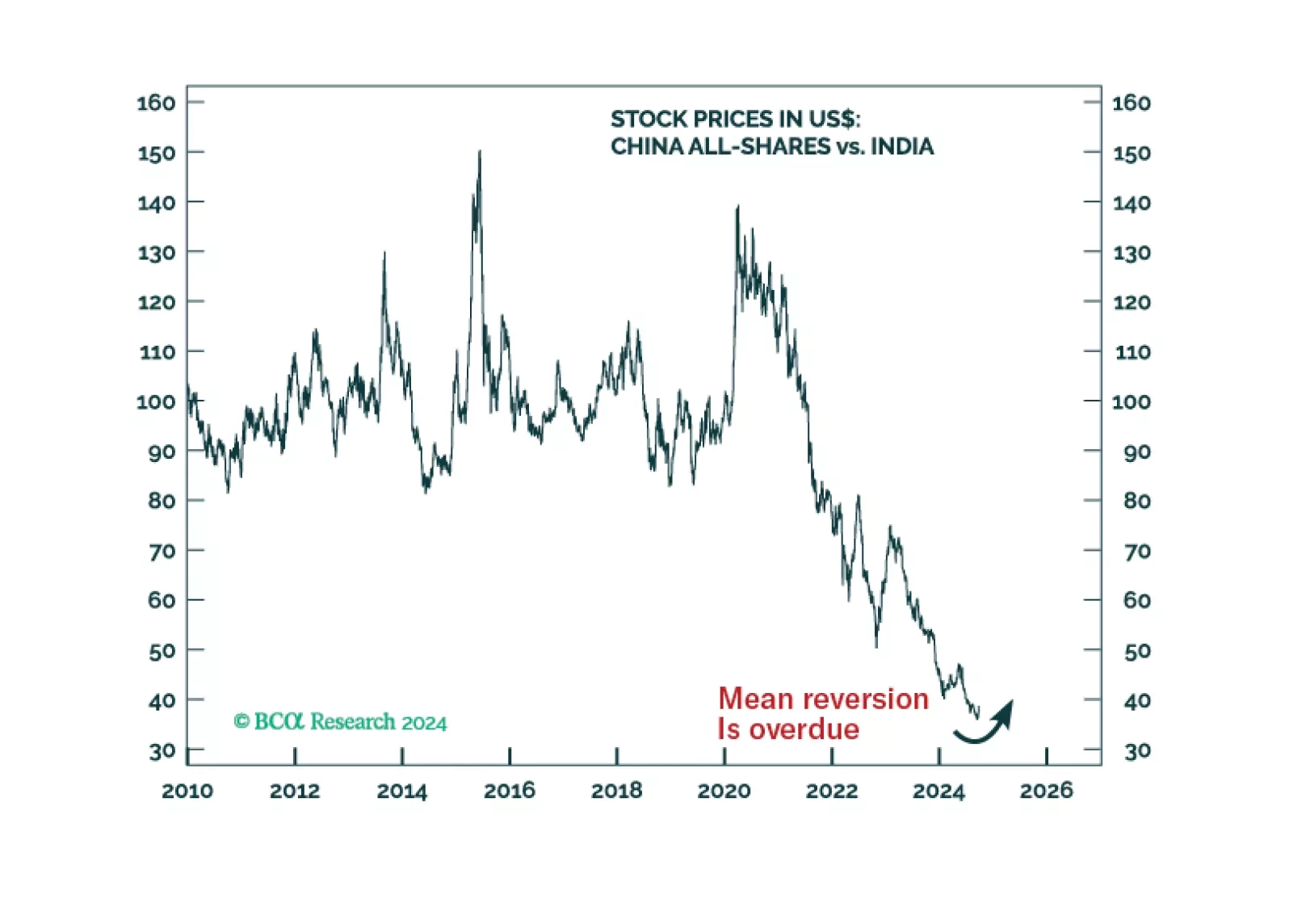

To produce a moderate economic recovery, at least RMB 3 trillion in additional government expenditures is needed in H1 2025. Our bias is that Beijing is not yet ready to launch such a massive fiscal support measure. Hence, volatility-adjusted equity returns in China will be poor.

We give our thoughts on this morning’s CPI release and (lack of) market reaction. We also close our short position in January 2025 fed funds futures.

Western policymakers are pursuing three capital “T” Truths: China is evil, climate change is a major risk, and Russia is… also evil. Pursuing all three priorities at the same time presents a version of the classic “impossible trinity.”

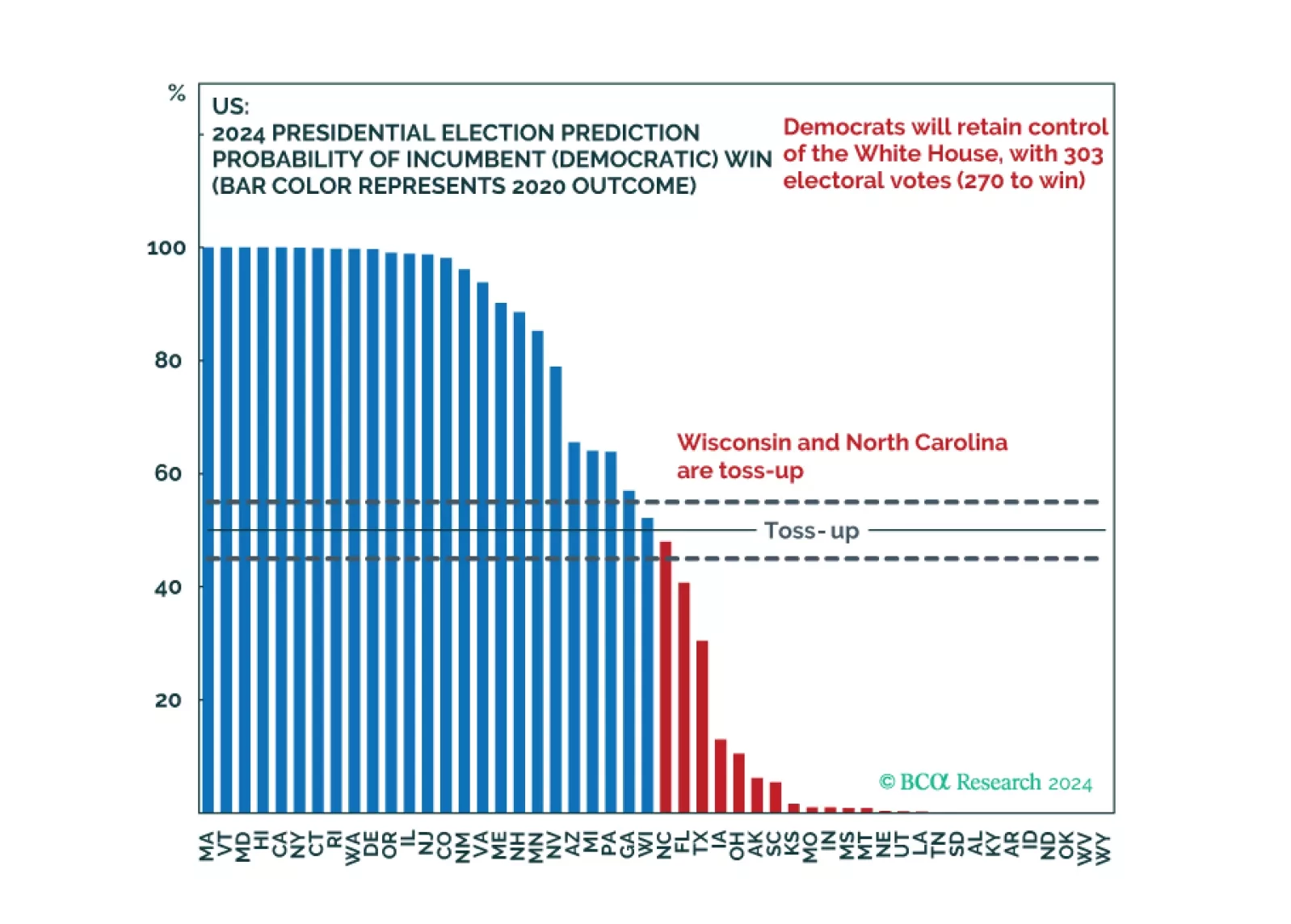

Our quant model shows Democrats winning the election at a 56% probability, with 303 electoral college votes. But swing state economies are slowing and Democrats’ odds in Michigan fell. Trump can win with Georgia, Michigan, plus one other state. Neither the Fed nor China’s stimulus should reduce one’s odds of a Republican upset.

The adrenaline from the recent policy stimulus might be sufficient to produce a window of outperformance for Chinese equities and China-plays in financial markets. However, this adrenaline will not extend to China's real economy. Net-net, we are upgrading the allocation to EM in a global equity portfolio from underweight to neutral.