Mega Themes

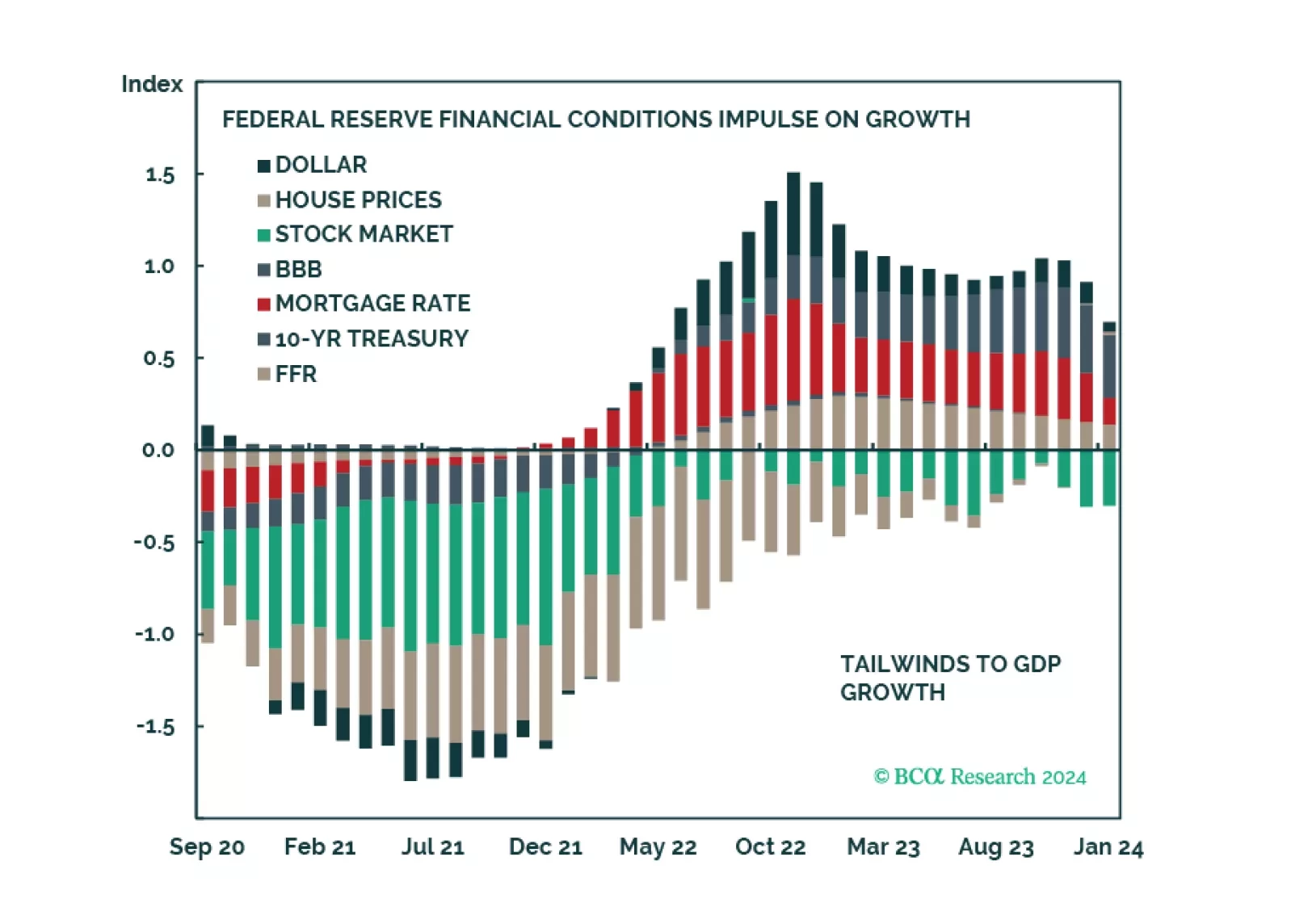

Clients are increasingly more positive about the US economy, but there are no signs of exuberance. The rally could continue as the majority is not fully invested. Financial conditions have already eased, and the Fed is unlikely to surprise on the upside but will deliver a promised cut this summer. CRE is a still pain point of the US economy. We are not bearish, but after a fast and furious rally, markets are fragile.

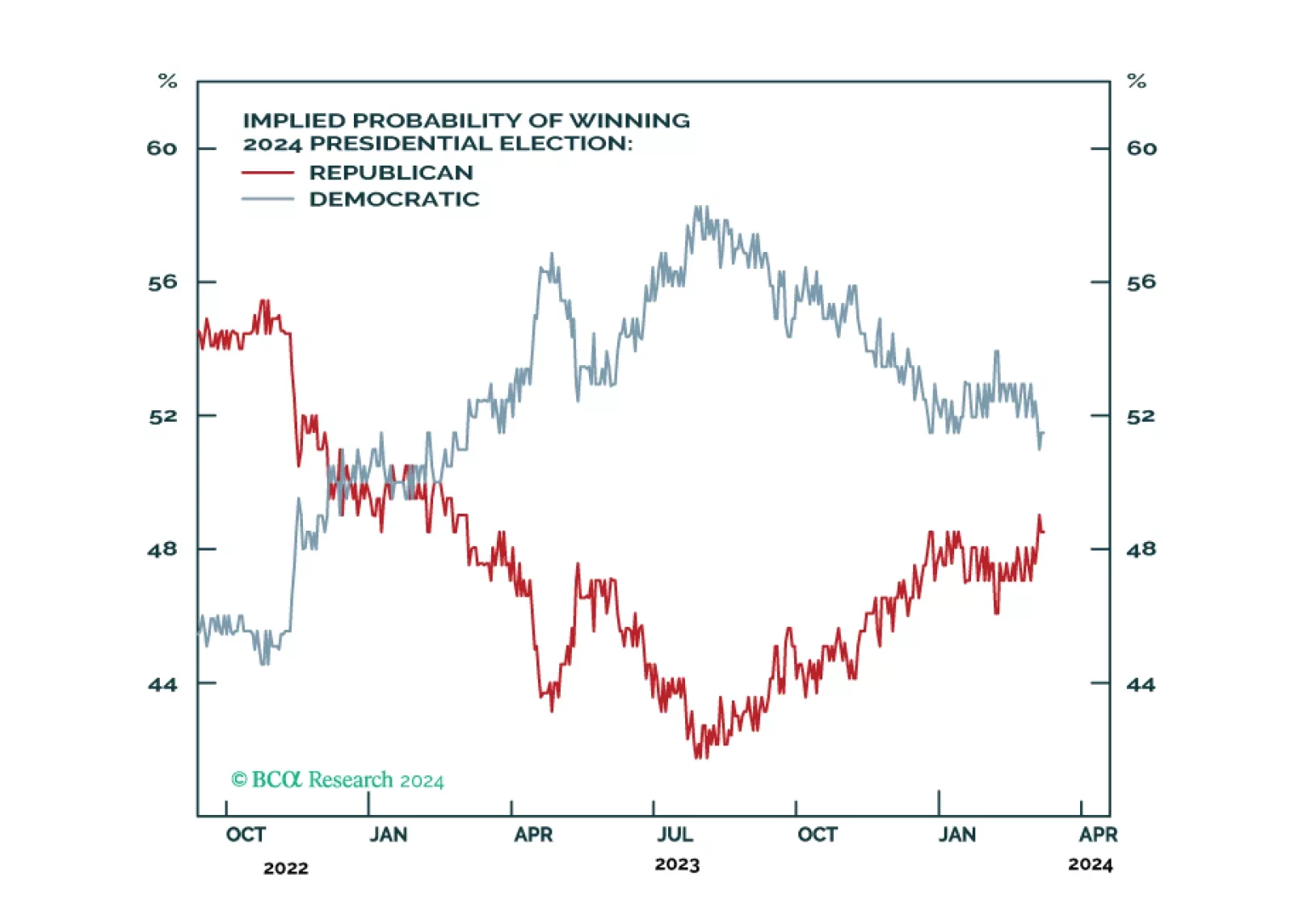

Democrats are still slightly favored for reelection as the incumbent party is presiding over a growing economy. However, Biden’s strong showing in the primary election is not lifting his popular approval yet, and that is a worrying sign. Policy uncertainty should rise sharply, which is marginally negative for the stock market.

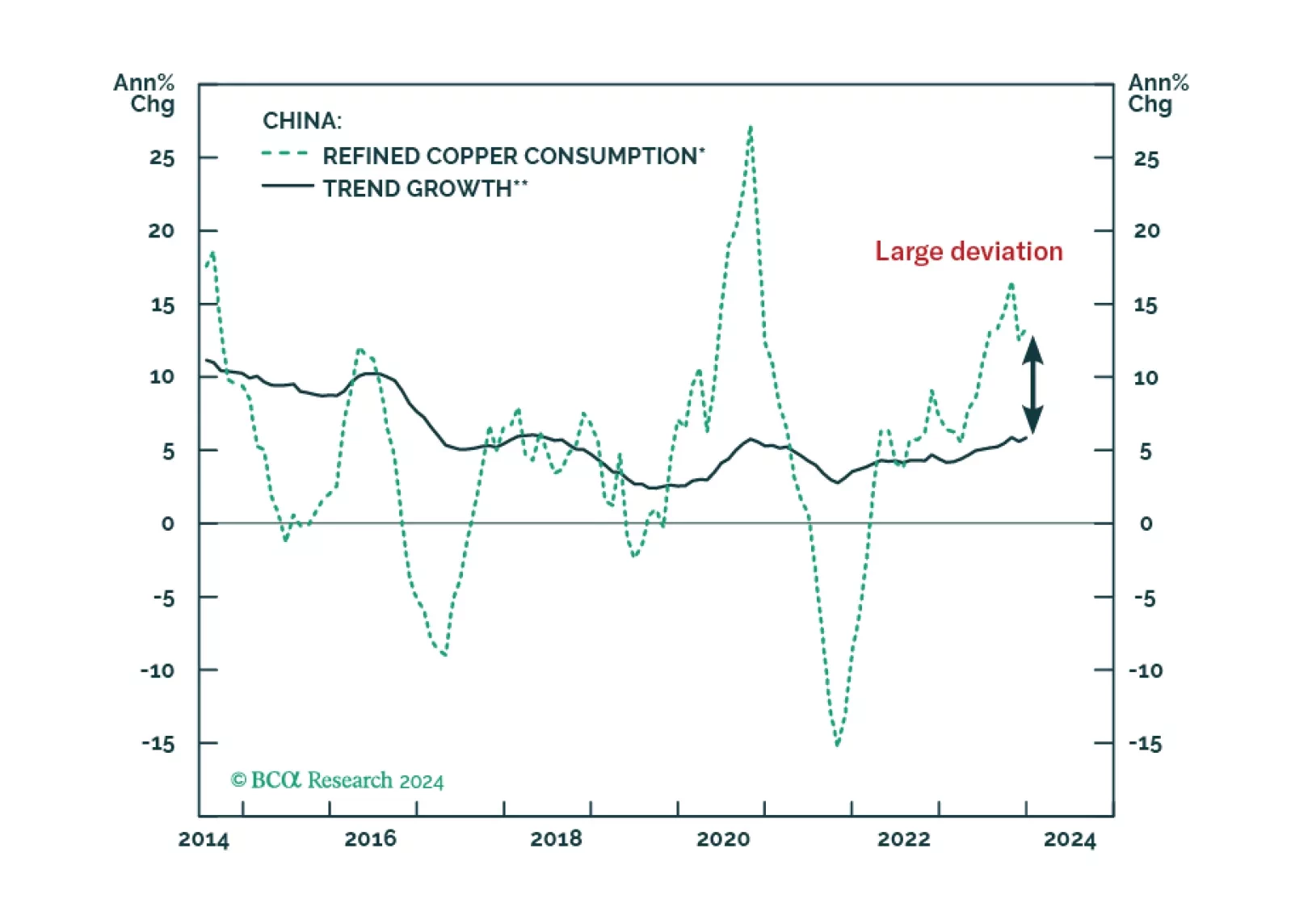

On the one hand, China’s copper intake boomed last year despite the travails of the mainland economy and shrinking property construction. On the other hand, global copper supply mushroomed despite persistent worries about supply shortages. This report uncovers this puzzle and elaborates on the outlook for copper prices. The conclusion is that red metal prices are still vulnerable.

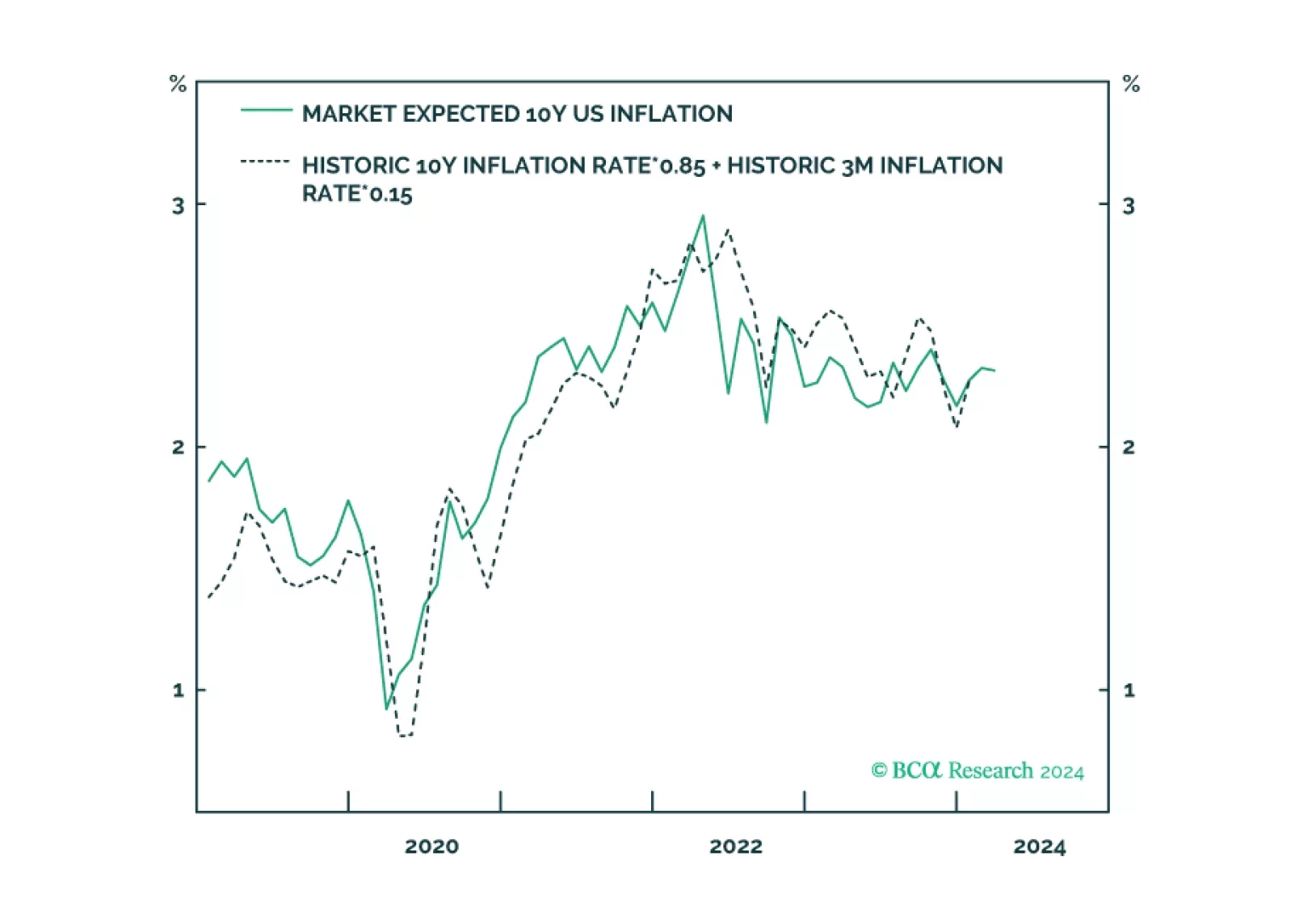

Expected inflation has surged to its highest level in a year. This has surprised many people, but expected inflation is behaving just as expected. Expected inflation is not a prophecy, it is just a mathematical function of delivered inflation. We discuss what this means for central banks in the US, UK, euro area, and Japan. Plus: bitcoin’s structural uptrend to $100,000+ is still intact.

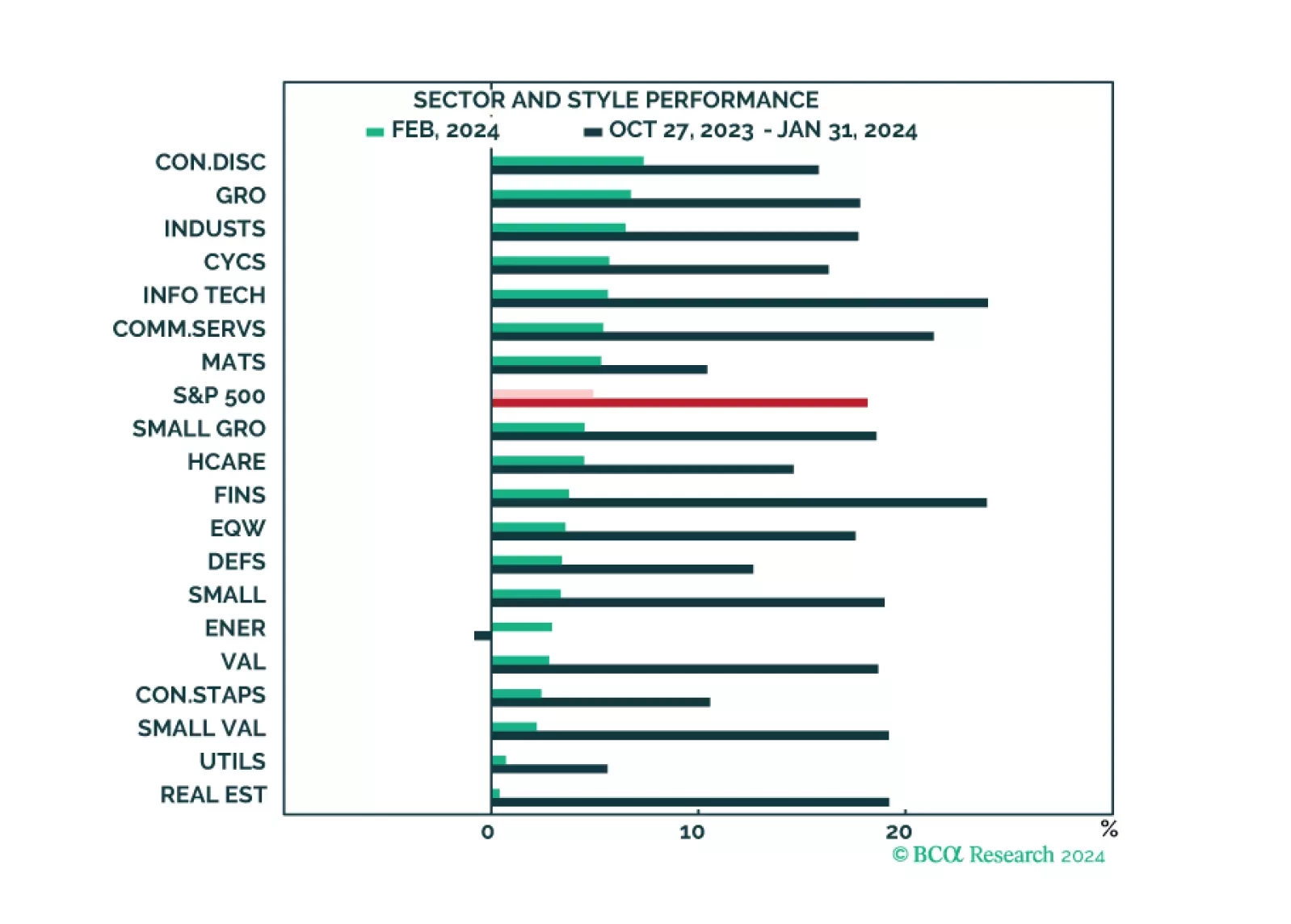

The market narrative continues to be dominated by the Magnificent Six, which drove both market performance and strong Q4 earnings results. While all sectors and styles have recently turned green, the rally is still mostly narrow. Earnings growth appears to be strong, but outside of the Magnificent Six, many companies are struggling. The market appears expensive and overbought, but that is mostly down to the high valuations and the popularity of the Magnificent Six.

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.

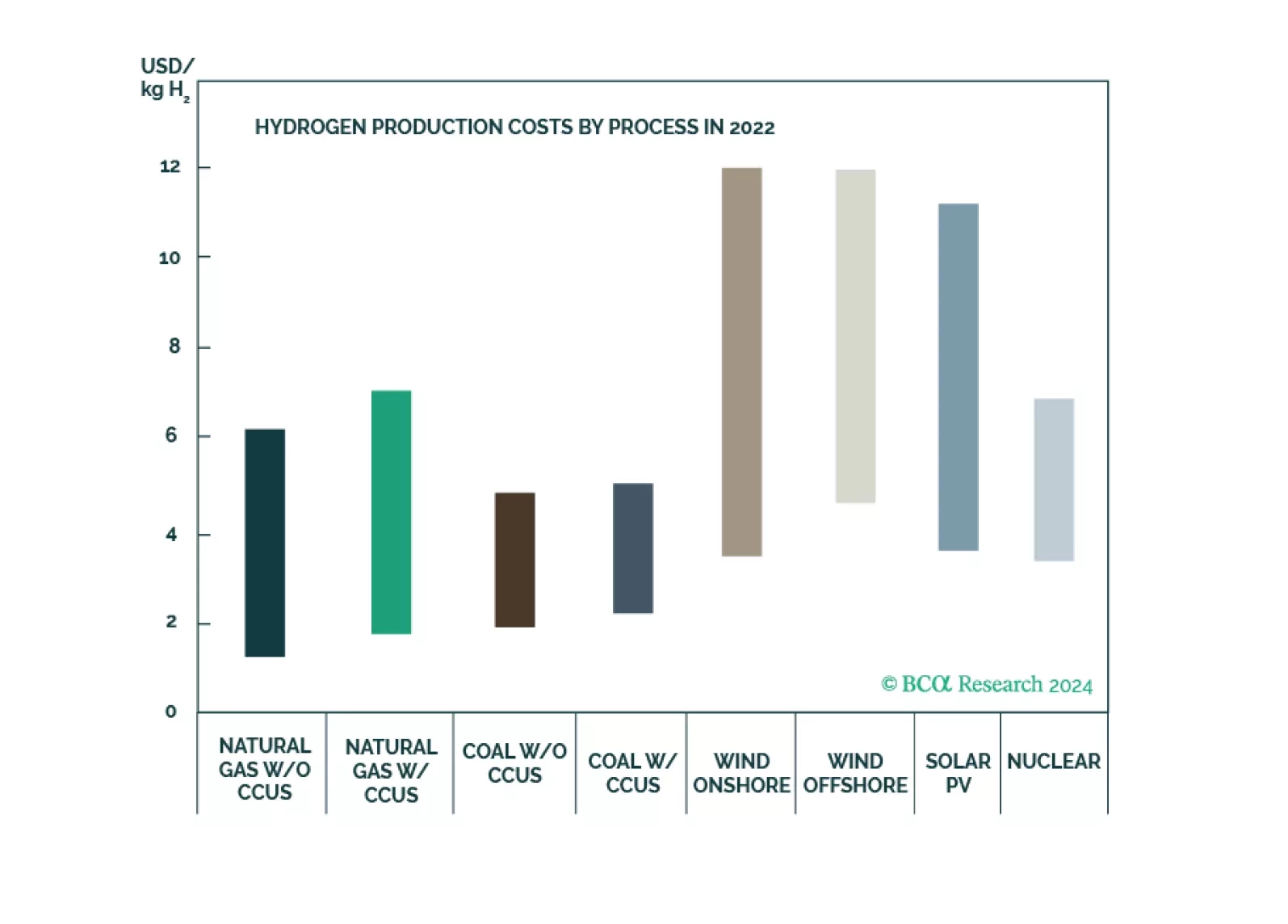

Naturally occurring hydrogen as a clean-energy source has the potential to satisfy significant energy demand growth at low cost. Oil and gas E+P companies and pipelines are ideally positioned to take a leading role in this clean-energy evolution, given their core competencies include large-scale resource extraction, storing and transporting gaseous commodities. Blending gold hydrogen with natural gas in pipeline systems could accelerate the industry’s learning curve in finding and delivering clean-energy fuels.

The US ‘immaculate disinflation’ has run its course, given that labour force participation is topping out. This leaves the Fed with a dilemma. Settle for price inflation stabilising at 3 percent, and cut rates early to avoid higher unemployment. Or, not cut rates early and go the final mile to 2 percent price inflation, at the risk of higher unemployment. We discuss which way the Fed is likely to tilt, and the investment implications. Plus: China is oversold while Japan is overbought.

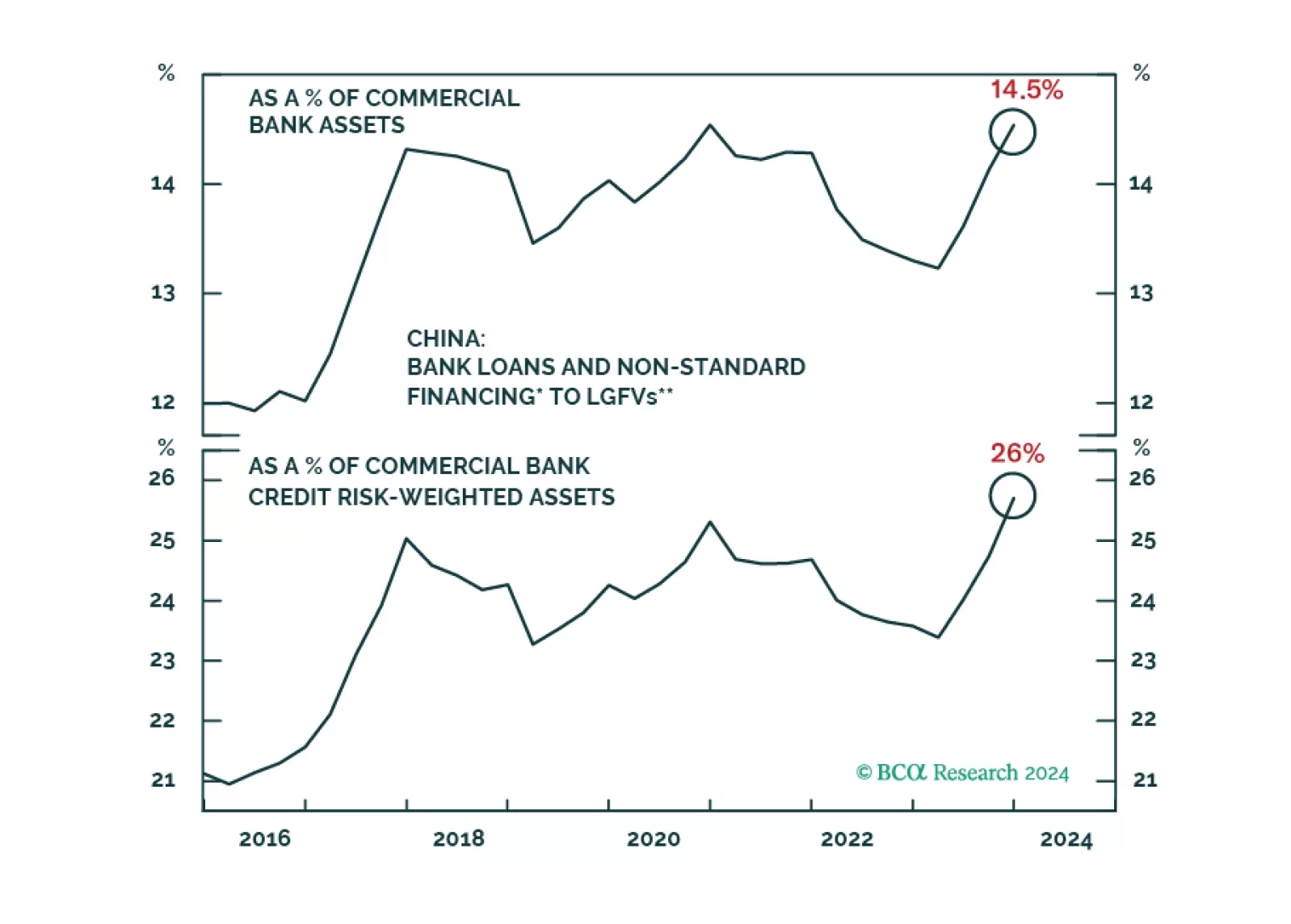

The odds of a “Minsky Moment” for the Chinese banking sector are low. They, however, will continue facing cyclical and structural headwinds, including a dismal asset quality and profit outlook. Bank stocks remain a value trap. Absolute-return investors should sell rebounds in Chinese bank stocks.

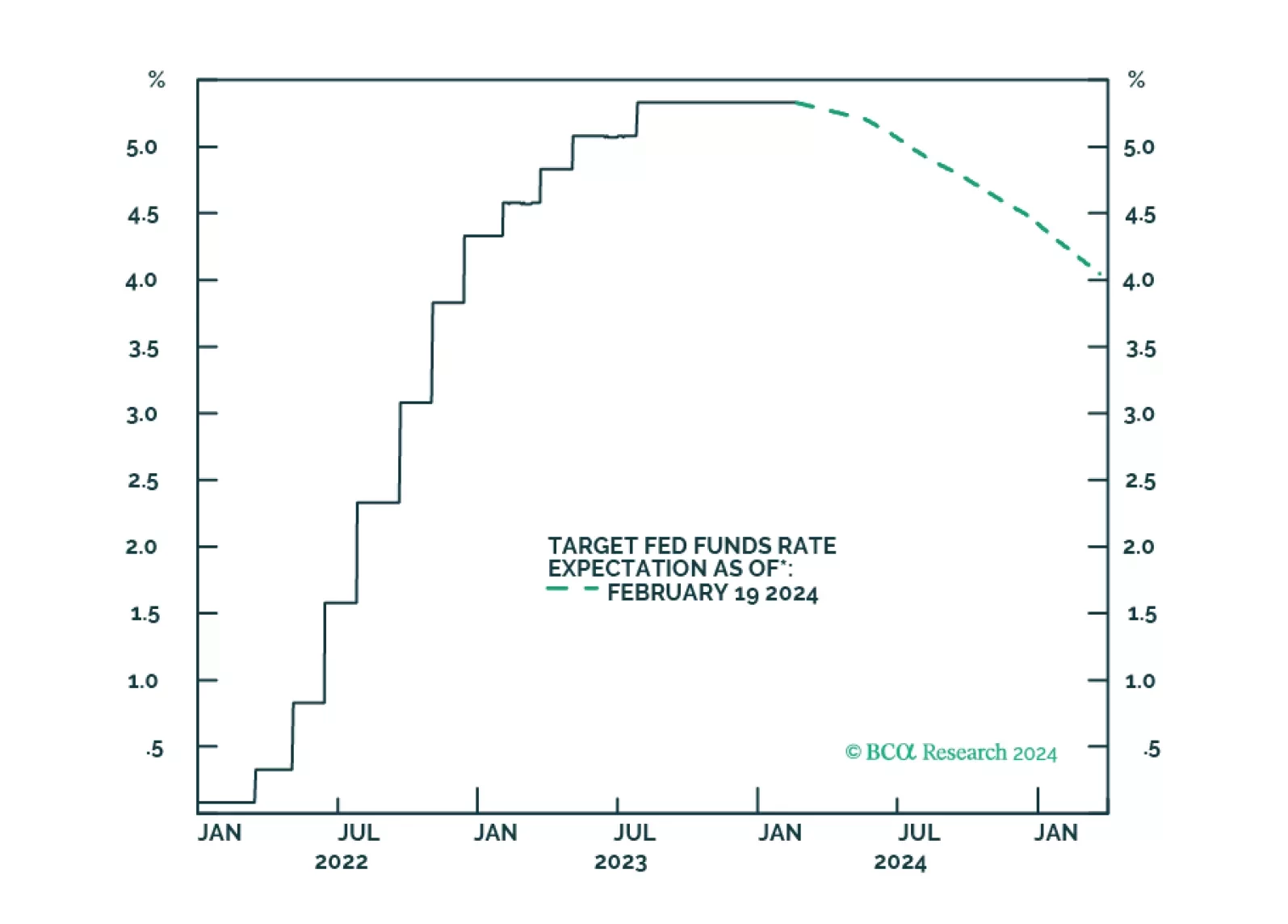

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.