Market Returns

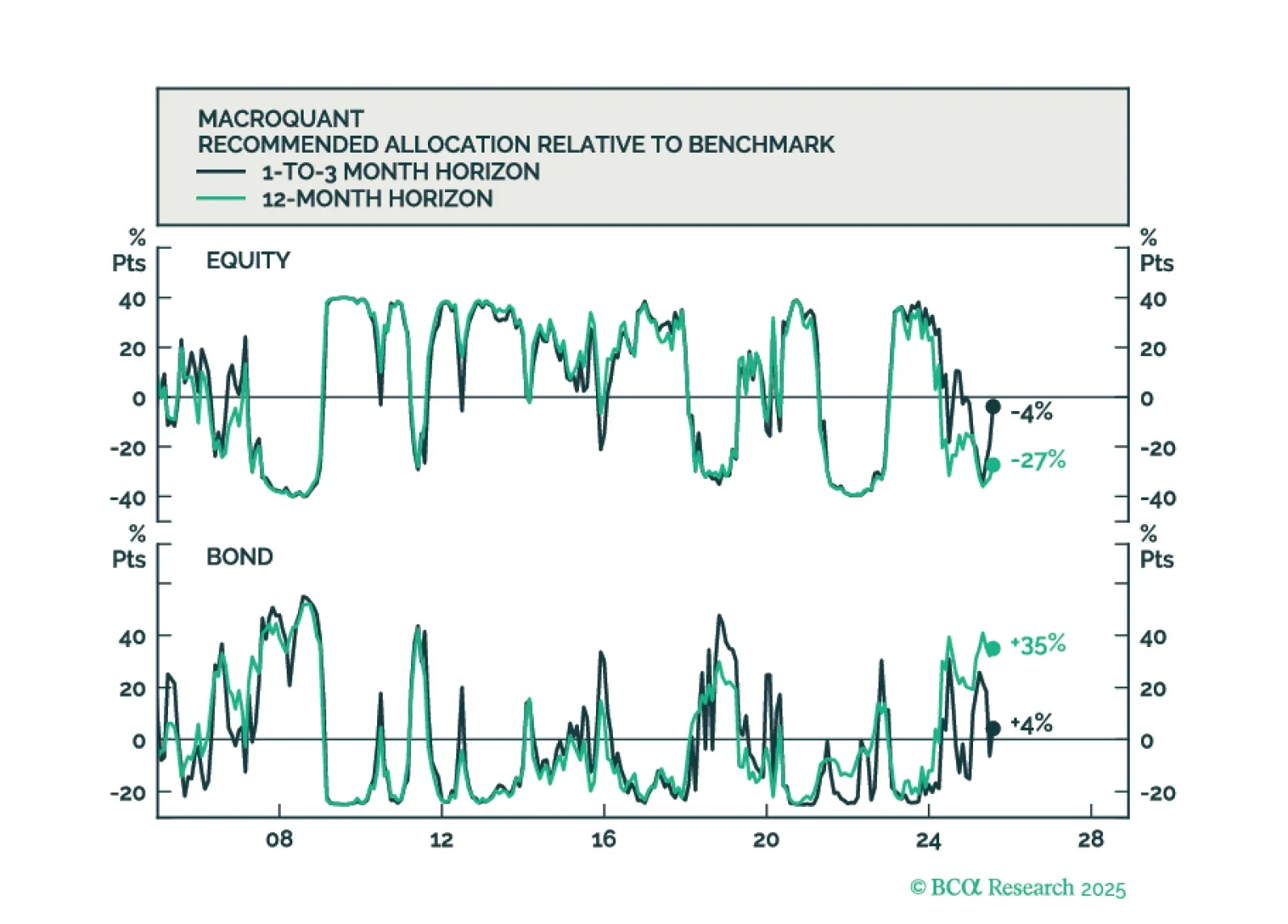

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

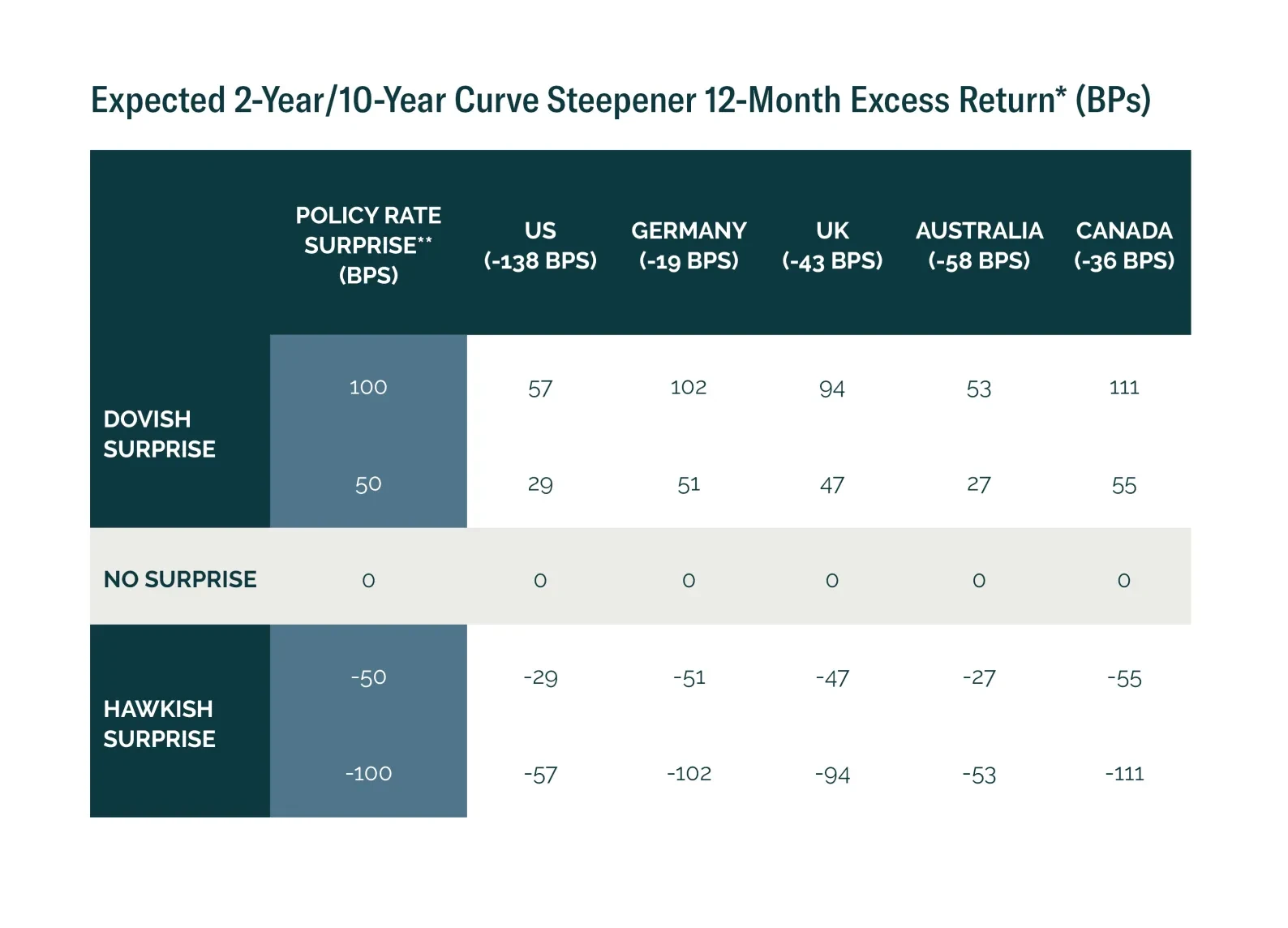

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.

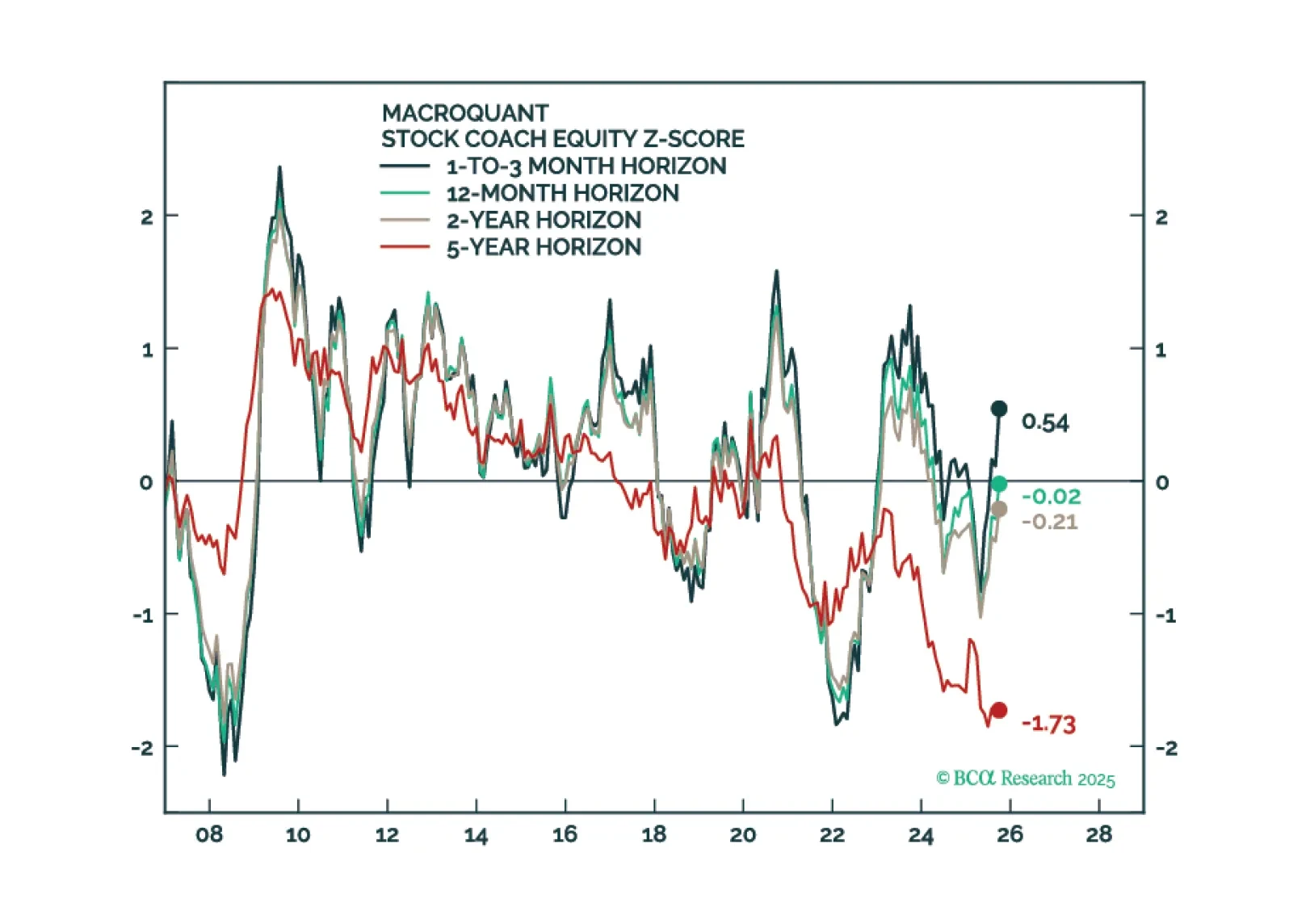

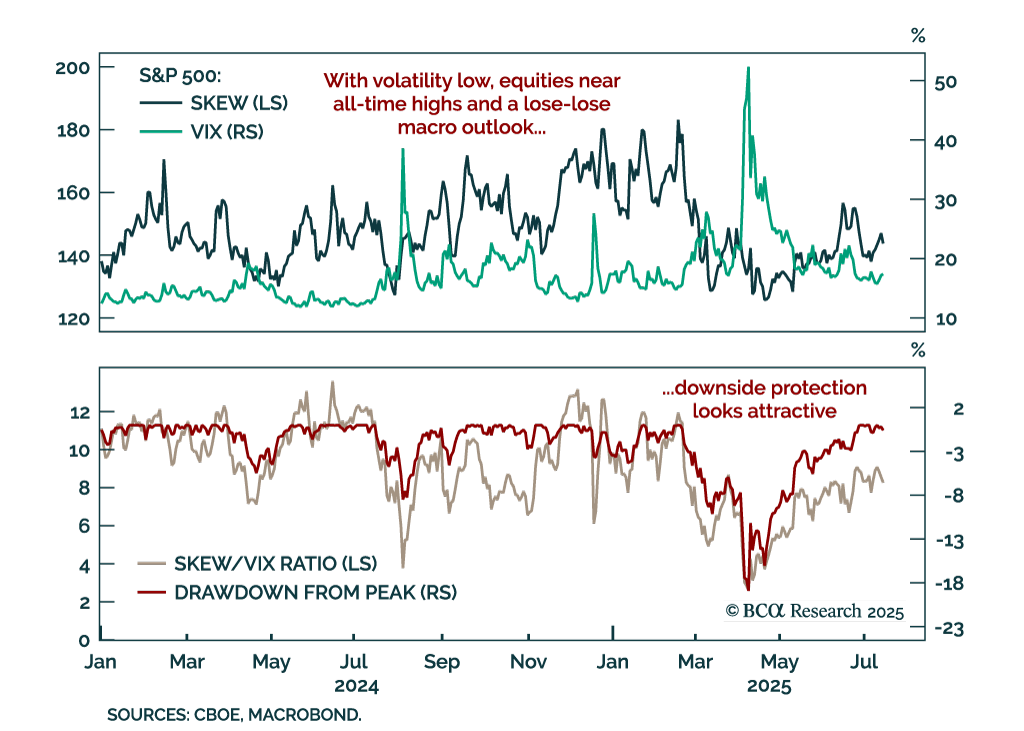

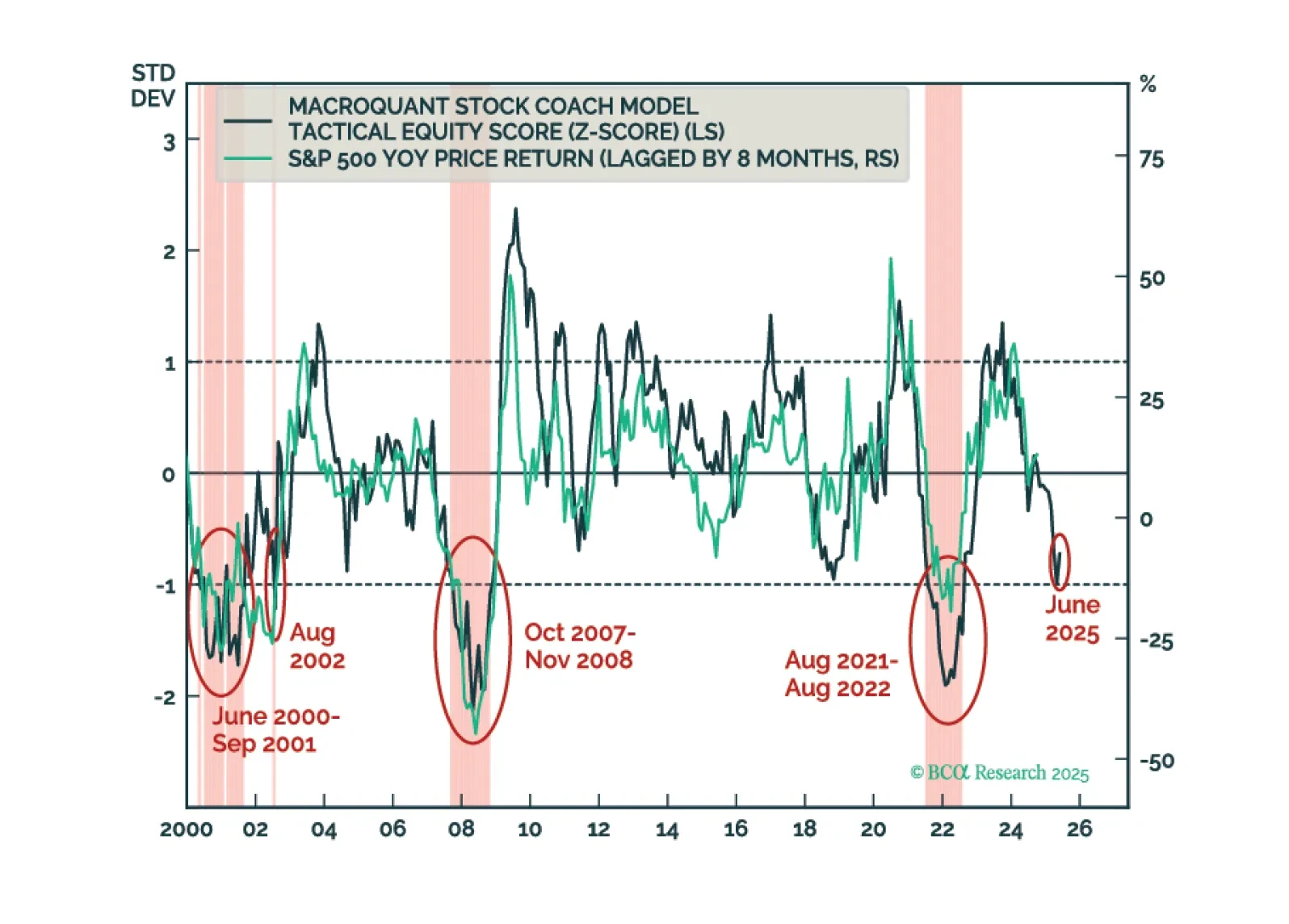

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

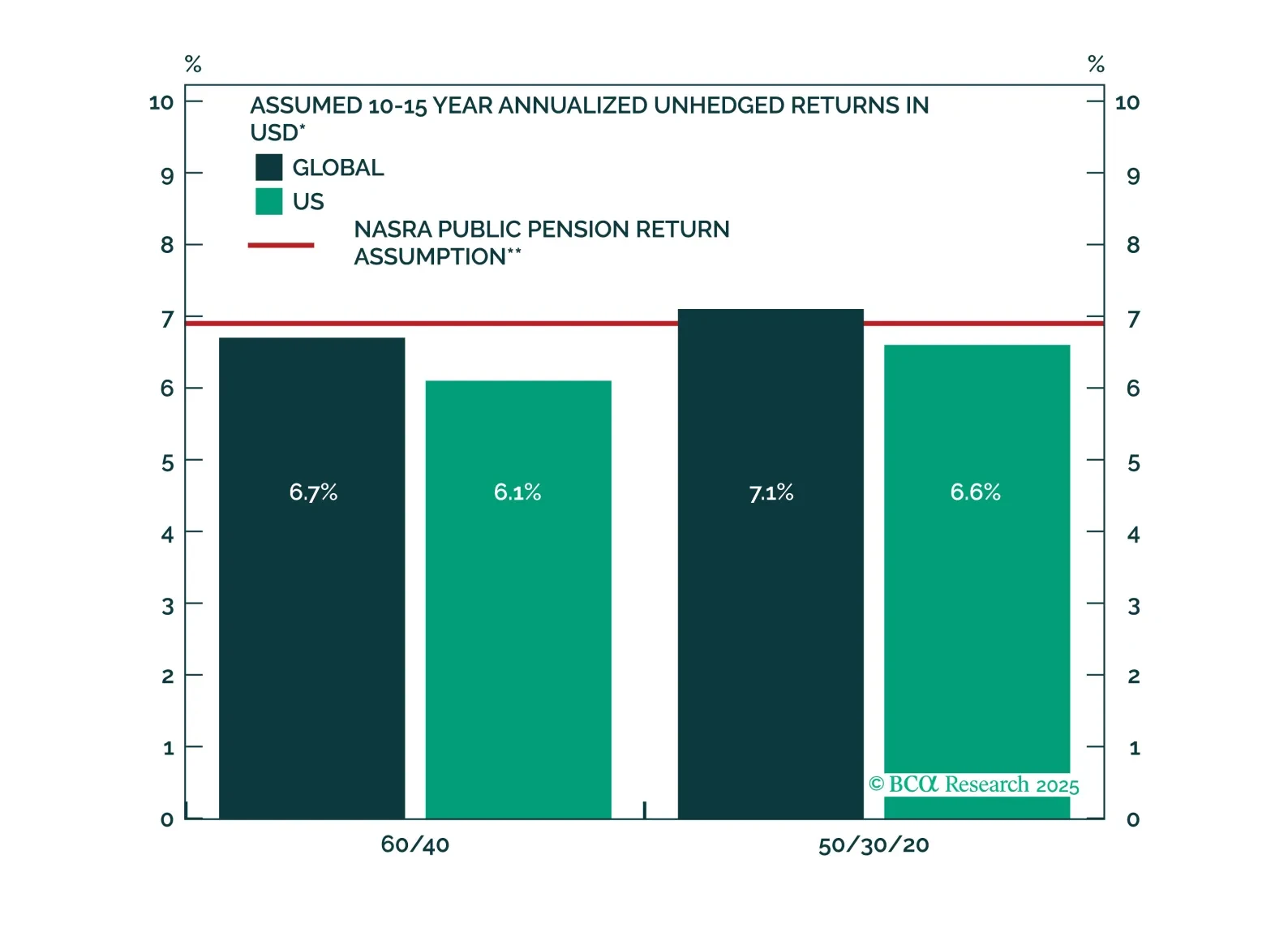

We revamp several of our methodologies in this edition of our return assumptions. We estimate that a US 60/40 portfolio will return 6.1% over the next 10 years. This is slightly below the return assumptions for US pension funds. Investors can obtain better returns by diversifying internationally and to alternative assets.

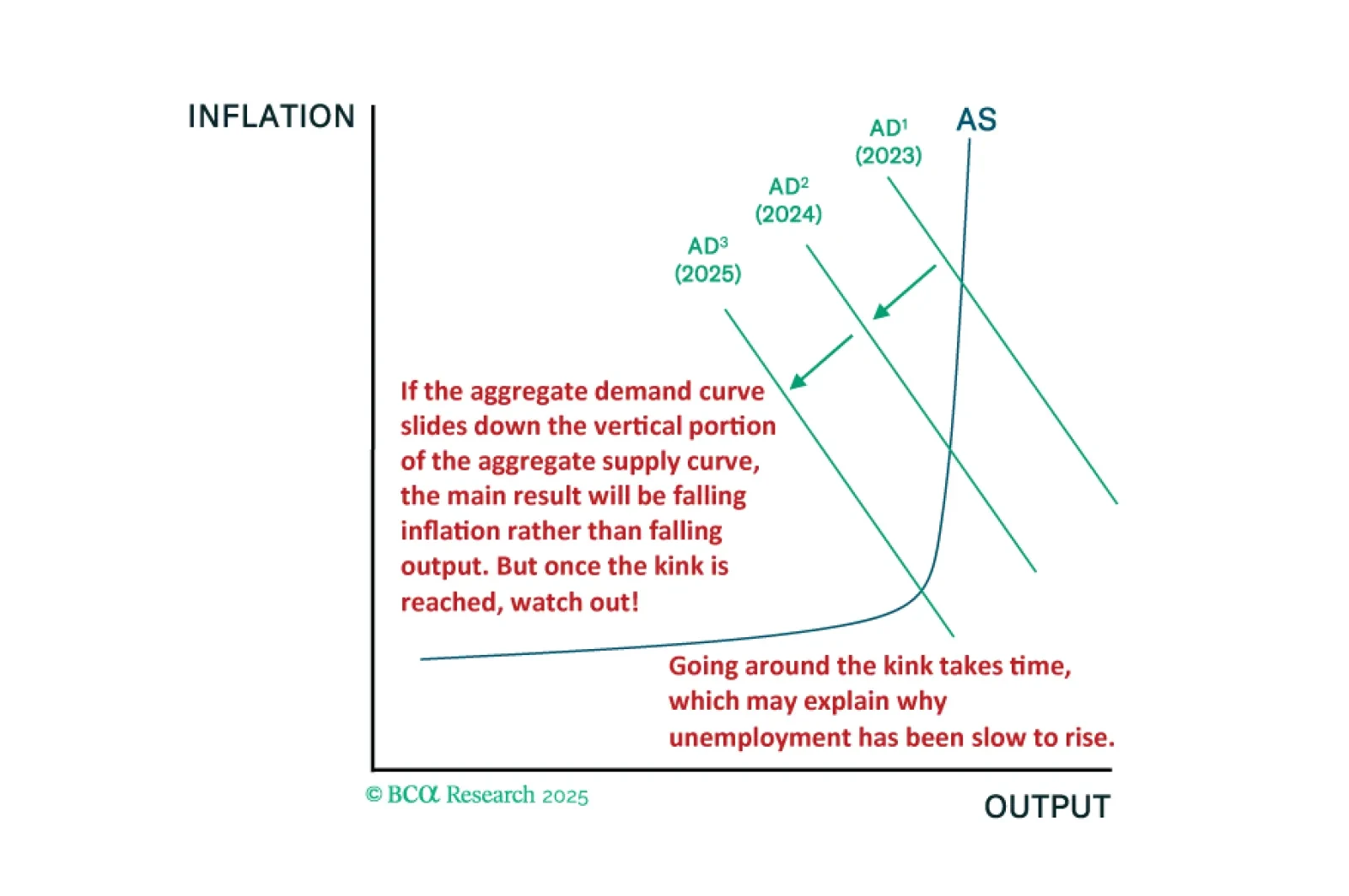

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.