Latin America

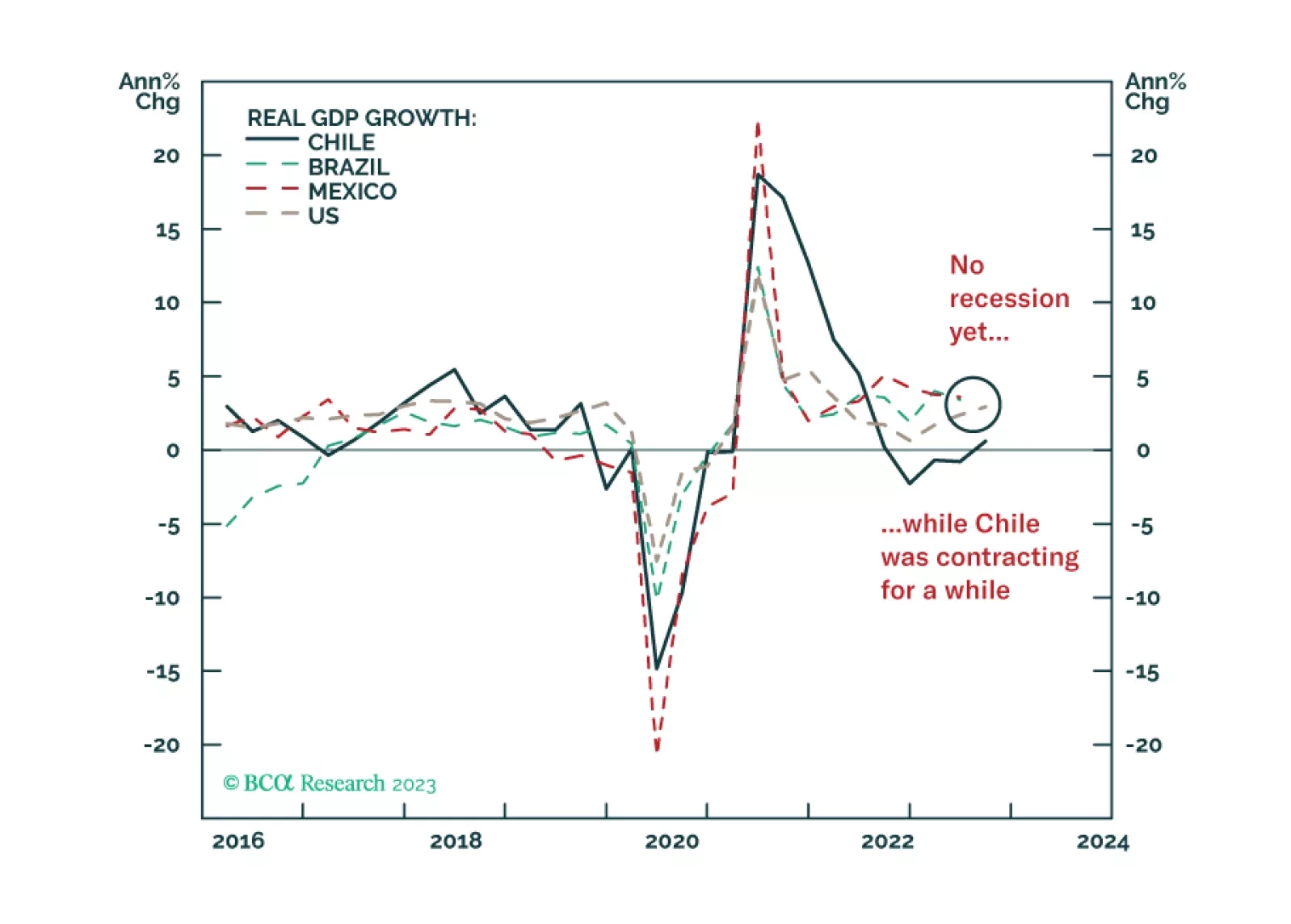

The Chilean economy is in a unique position worldwide: as it is the first to enter a recession, it will be the first to recover. Together with historically cheap valuations, this will lead to a sustained outperformance of Chilean stocks relative to their EM peers.

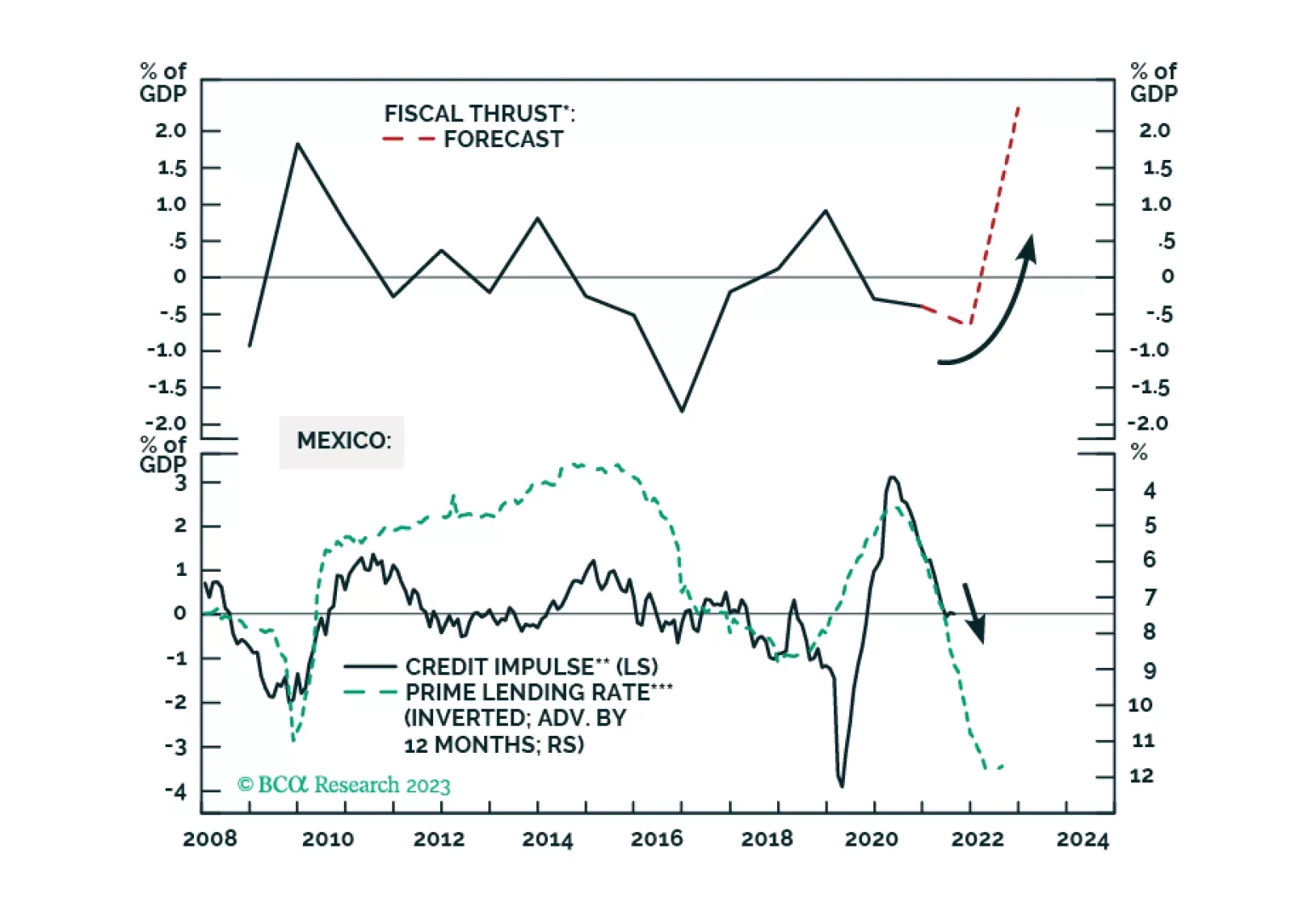

While Mexican markets will continue selling off in absolute terms, their recent underperformance versus their EM peers is a temporary setback in a cyclical and structural bull market. Domestic politics are evolving from stable to bullish: the new president will rule in a technocratic manner, respecting private sector interests. The Mexican economy will achieve a soft landing even if the US enters a recession.

Despite higher oil prices, Colombian risk assets will underperform their EM peers in the months ahead. The domestic economy is evolving from stagflation into recession, and fiscal and political risks will raise the risk premium of Colombian assets. Take profits on the yield curve inversion trade and stay short COP vs. USD.

While it may be tempting to bottom fish, we advise that investors maintain a cautious stance on Argentinian sovereign credit. Even though the election of a right-wing candidate in the coming months may boost investor sentiment, the country still faces major headwinds: more currency devaluation, and another possible default/debt restructuring.