Latin America

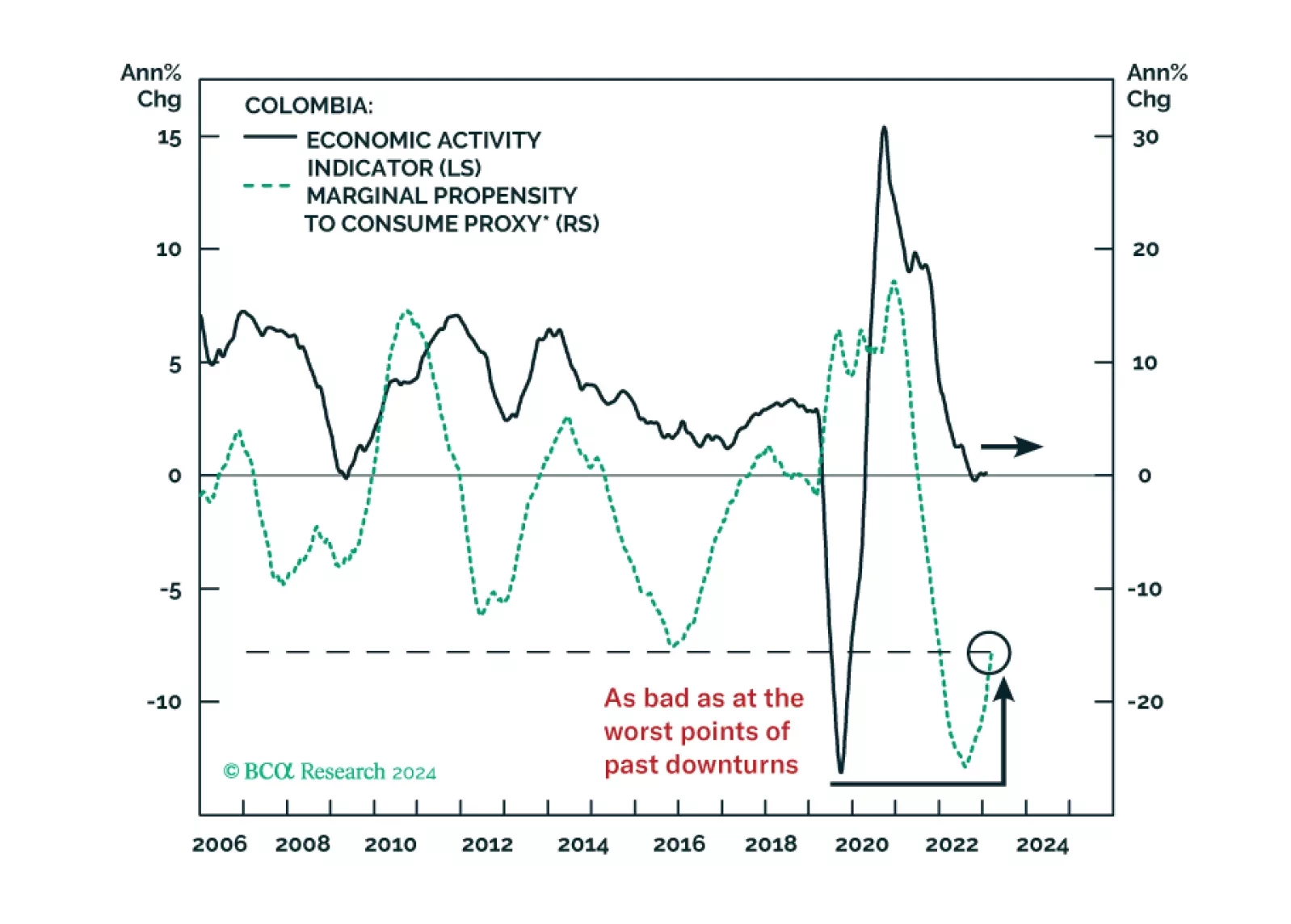

Colombia has fallen from grace in terms of its healthy macroeconomic fundamentals, business-friendly government policies, and conservative fiscal stances. The economy is experiencing stagflation, public finances are deteriorating rapidly, and political uncertainty will persist. Underweight Colombia across all financial markets relative to their EM benchmarks, and short Colombian bank stocks and the currency versus their Chilean counterparts.

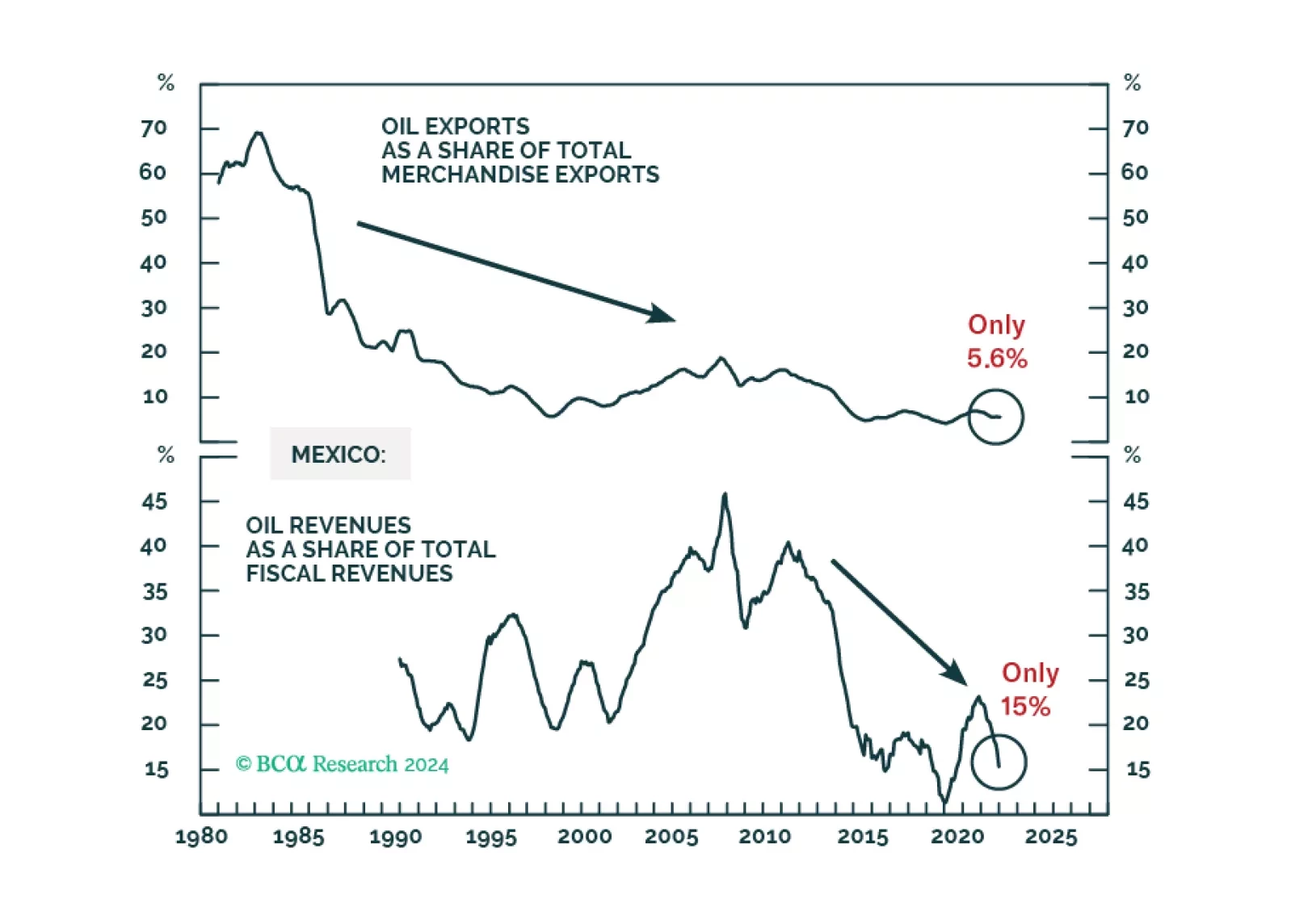

Continue overweighting Mexican stocks, sovereign credit, and local bonds relative to their respective EM benchmarks. That said, the peso is overbought and will correct versus the US dollar. Therefore, we recommend that investors hedge the currency risk for their outright long positions in Mexican equity and local bond markets for the next few months.

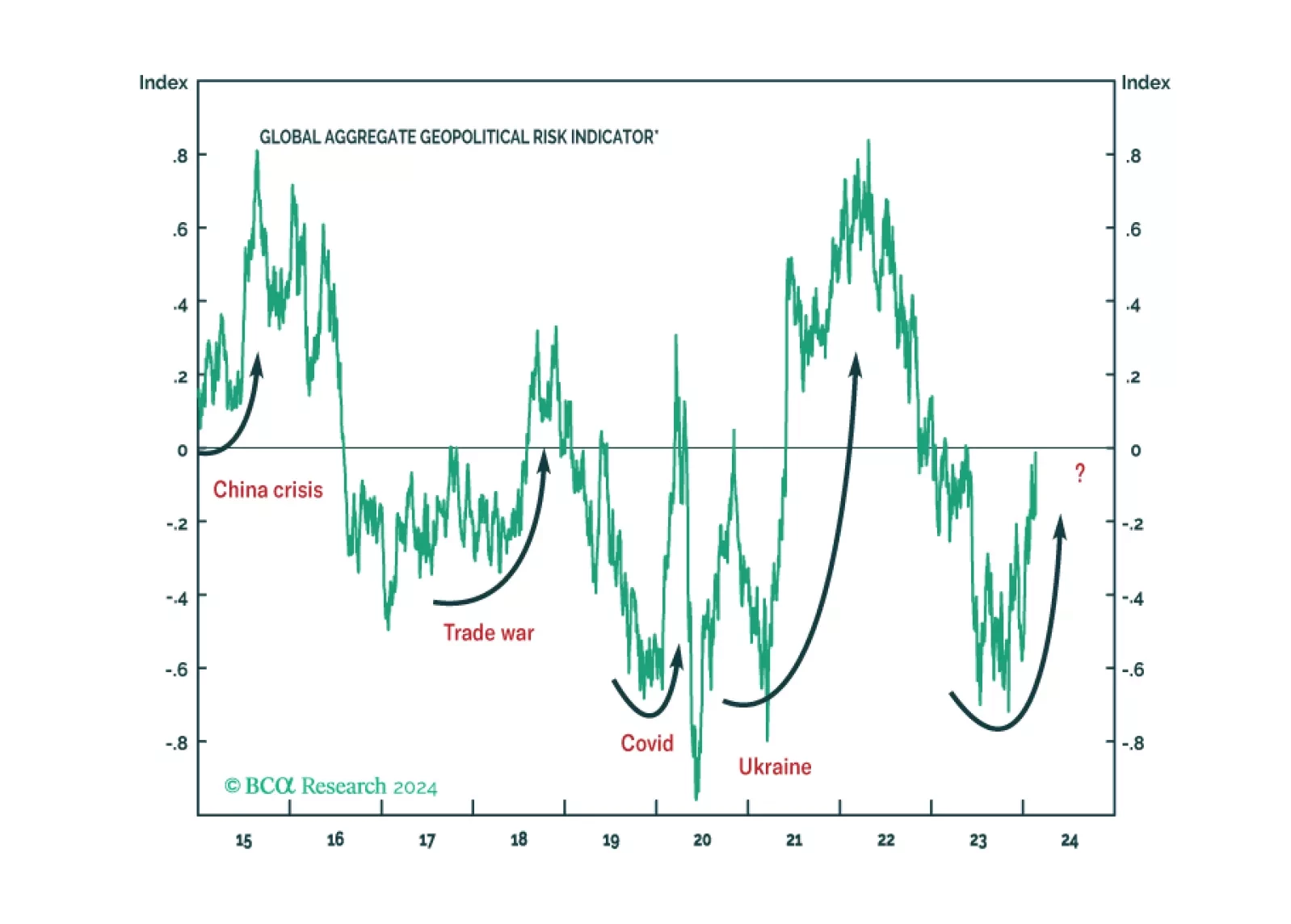

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

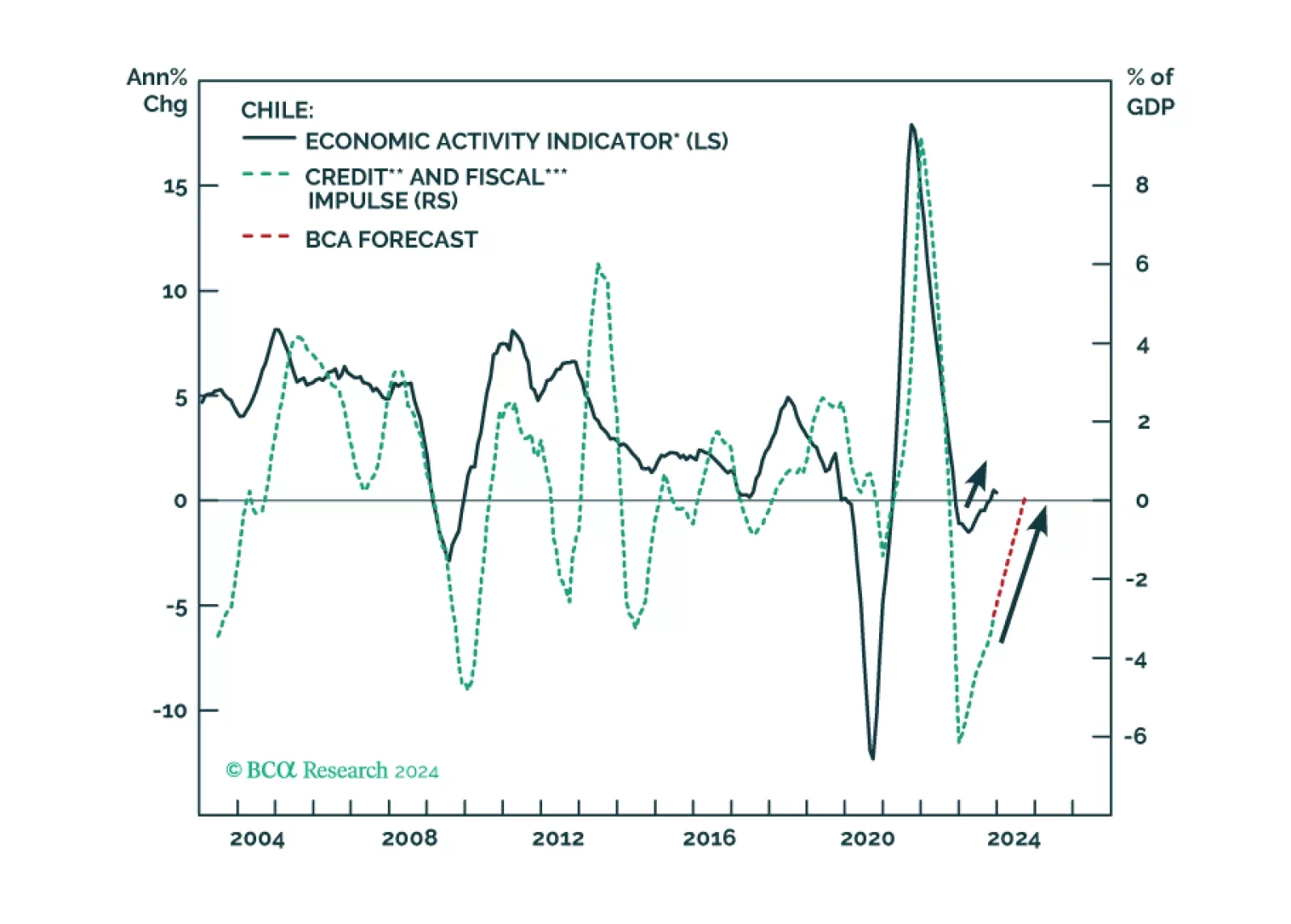

The stars have aligned for a major outperformance of Chilean stocks versus the EM equity benchmark. Plummeting inflation in Chile will push monetary authorities to continue their aggressive rate cuts, engineering a quick economic recovery this year. We maintain our overweight stance on Chilean stocks and fixed income, and recommend investors go long Chilean banks / short the overall EM index, buy 10-year government bonds, and go long CLP / short COP.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

The Brazilian government and the central bank will be prioritizing growth over curbing the fiscal deficit and inflation. The outcome of an easy policy mix is that growth and inflation will be higher relative to market expectations, and real interest rates will drop considerably. We recommend that investors go long mid- and small-cap stocks on a pullback and inflation-linked bonds. However, foreign investors should hedge the currency risk.