Latin America

Our Portfolio Allocation Summary for July 2024.

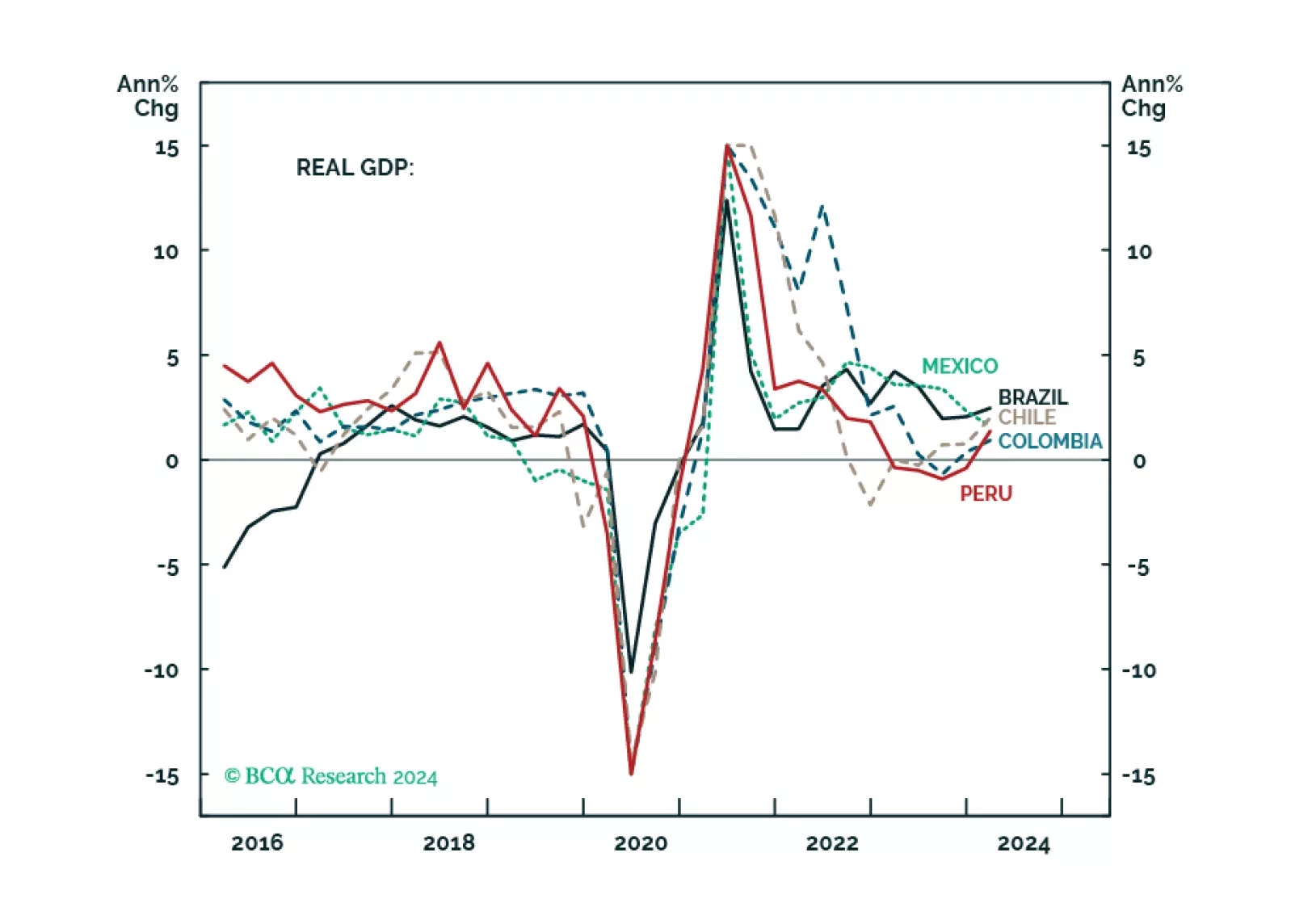

Non-trivial macro divergences have emerged between mainstream LATAM economies. This report compares and ranks Brazil, Mexico, Colombia, Chile, and Peru based on their business cycle outlook, macro policy stance, external accounts, and structural fundamentals. All in all, LATAM risk assets will fall in absolute terms given a strengthening US dollar and a global risk-off move in the coming months. Within LATAM, we favor Mexico, Chile and Peru, are neutral on Brazil, and bearish on Colombia.

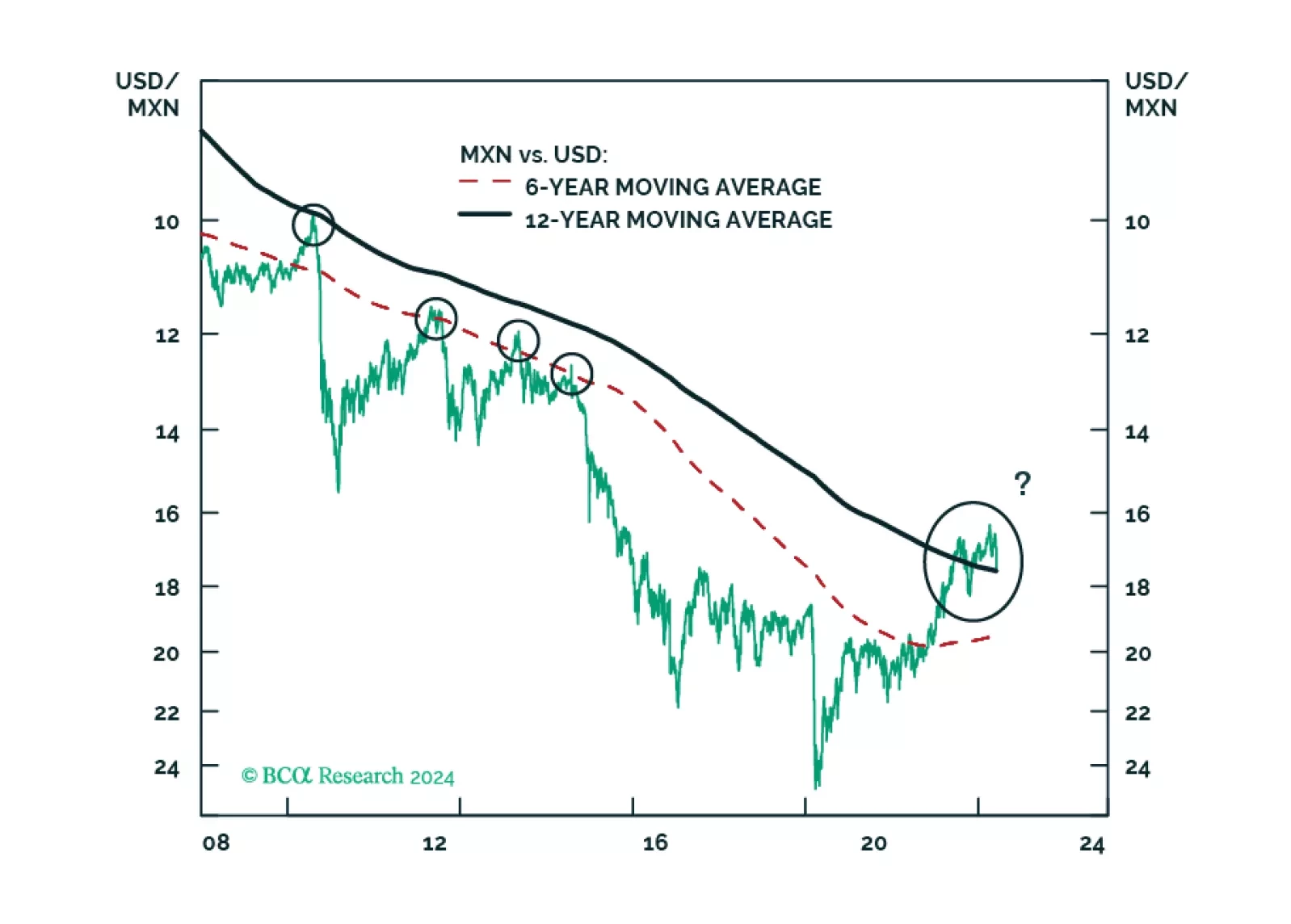

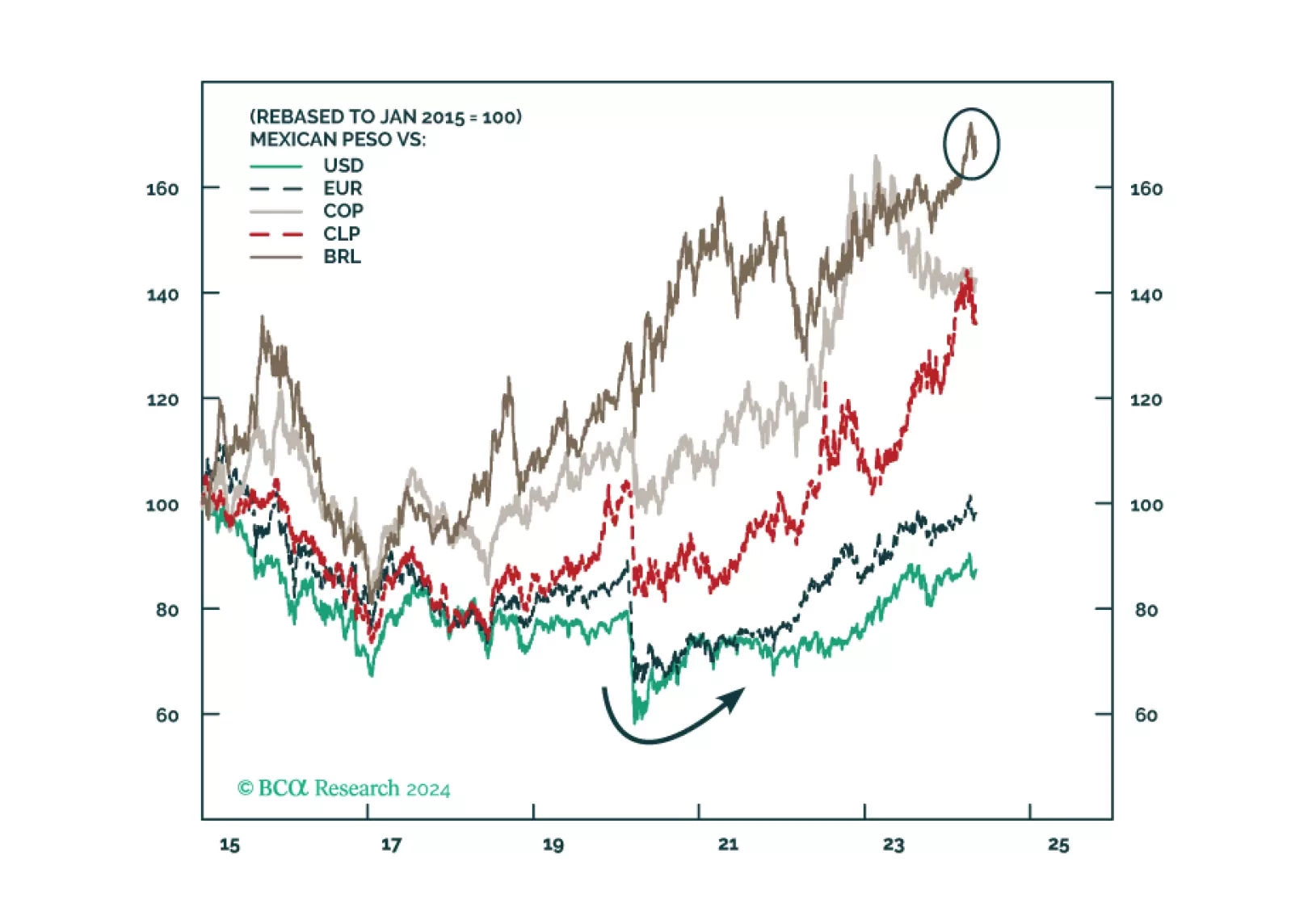

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

Our Portfolio Allocation Summary for June 2024.

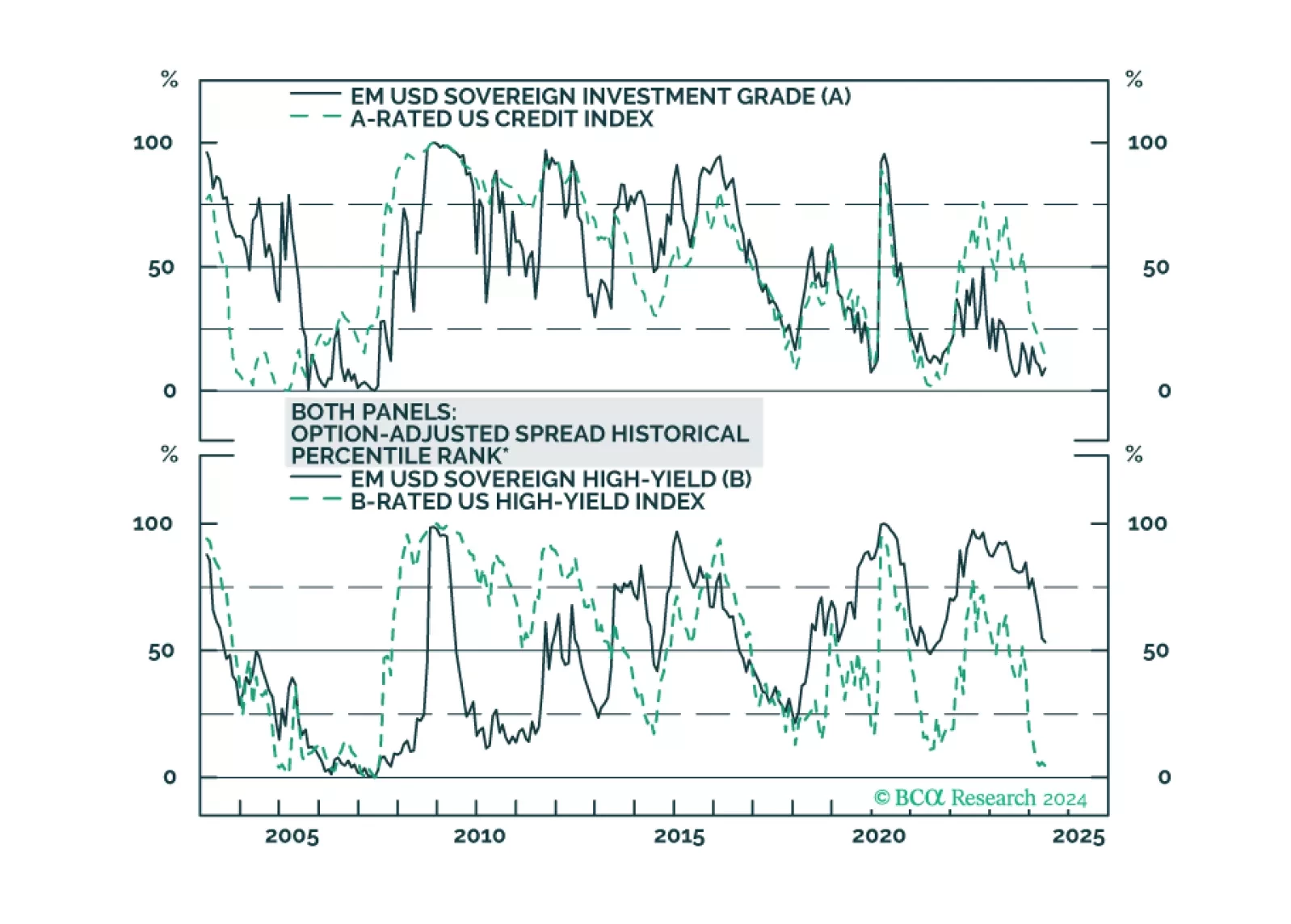

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

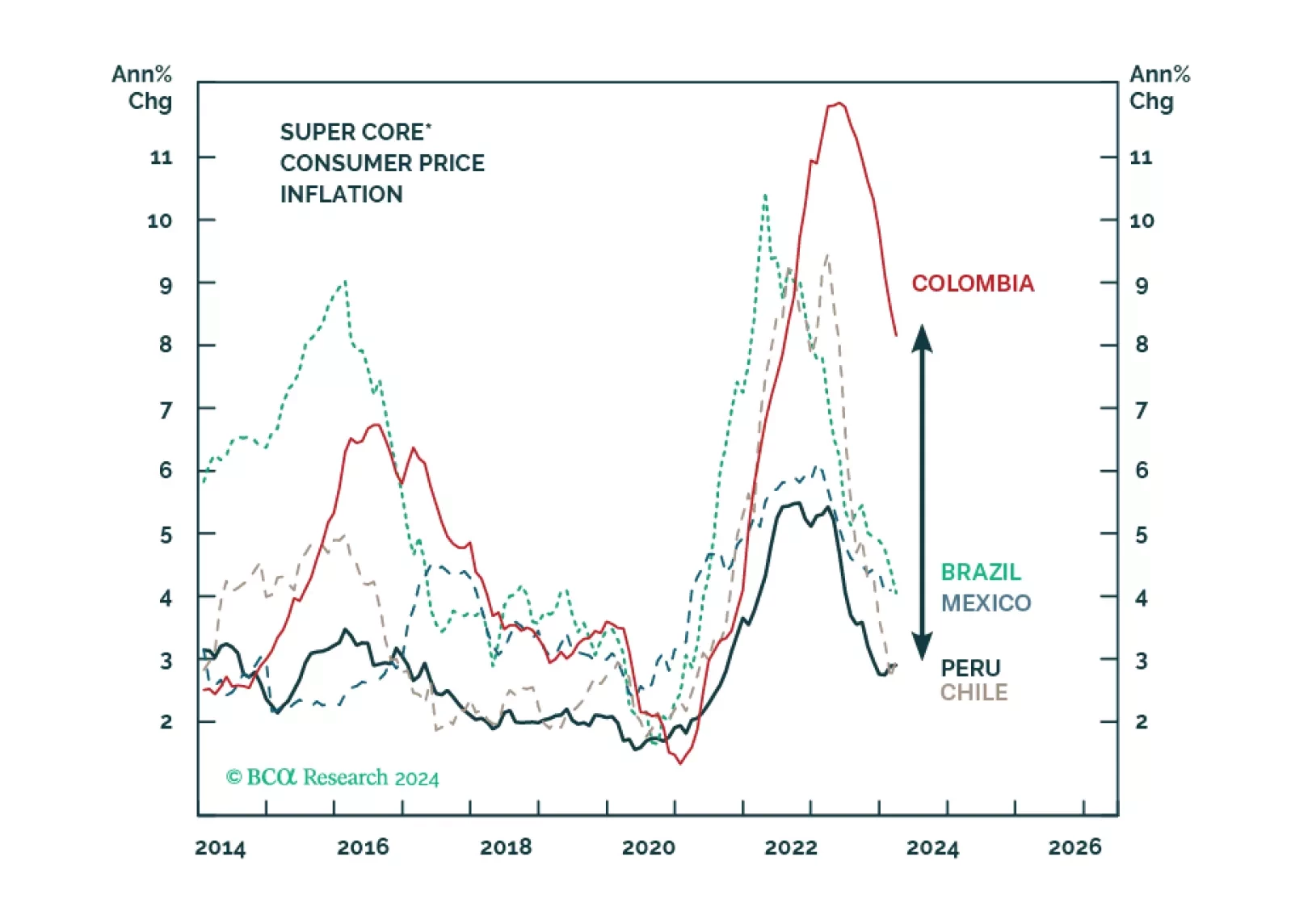

Peru is entering a benign macro environment: low and falling inflation amid a solid economic recovery. The country’s balance of payments position is robust, which will help the PEN depreciate by less than other EM currencies. The political situation is on shaky ground, but a regime shift will have to wait until 2026. We remain overweight on Peruvian equities, domestic bonds, and sovereign credit relative to the EM benchmarks.