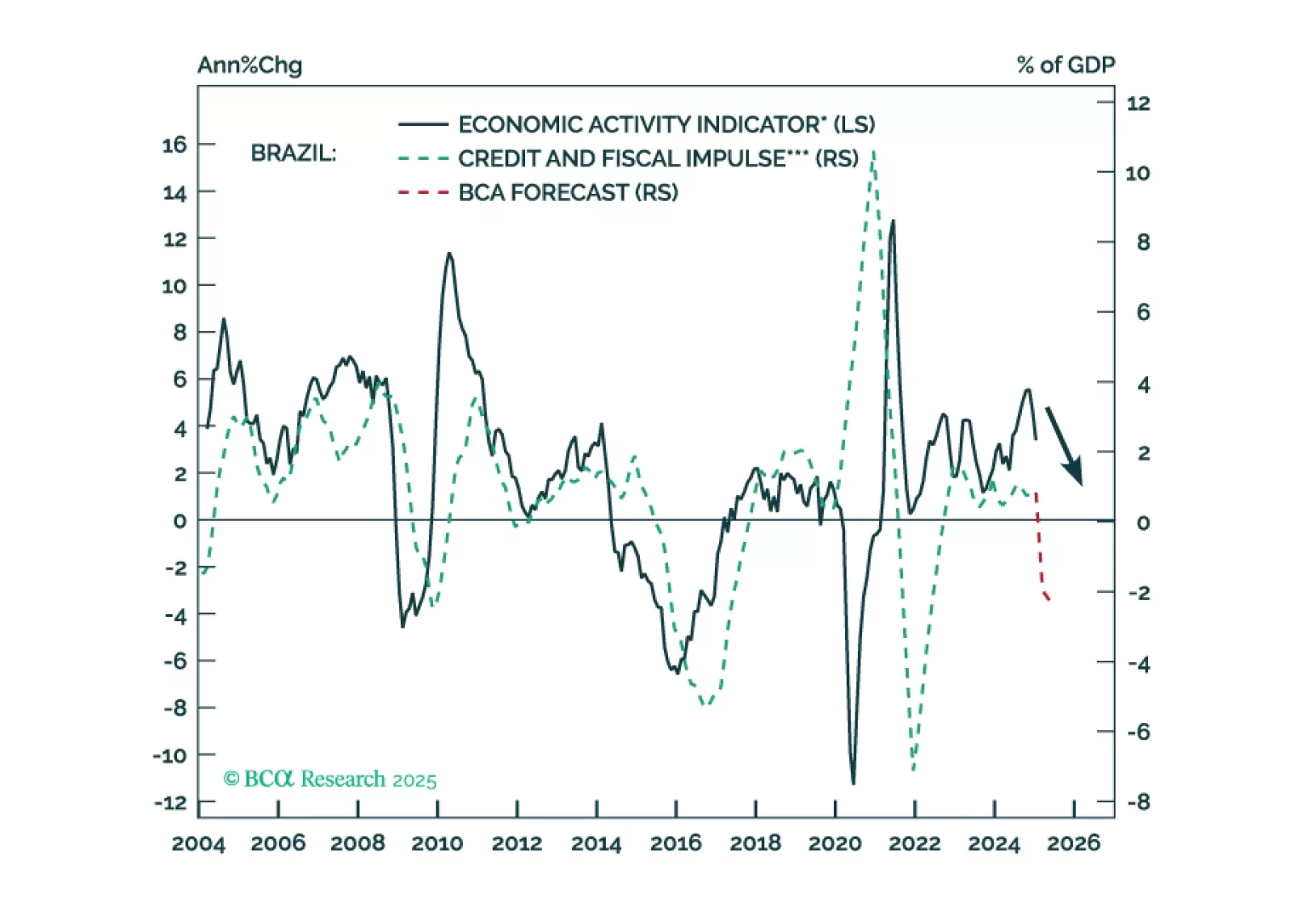

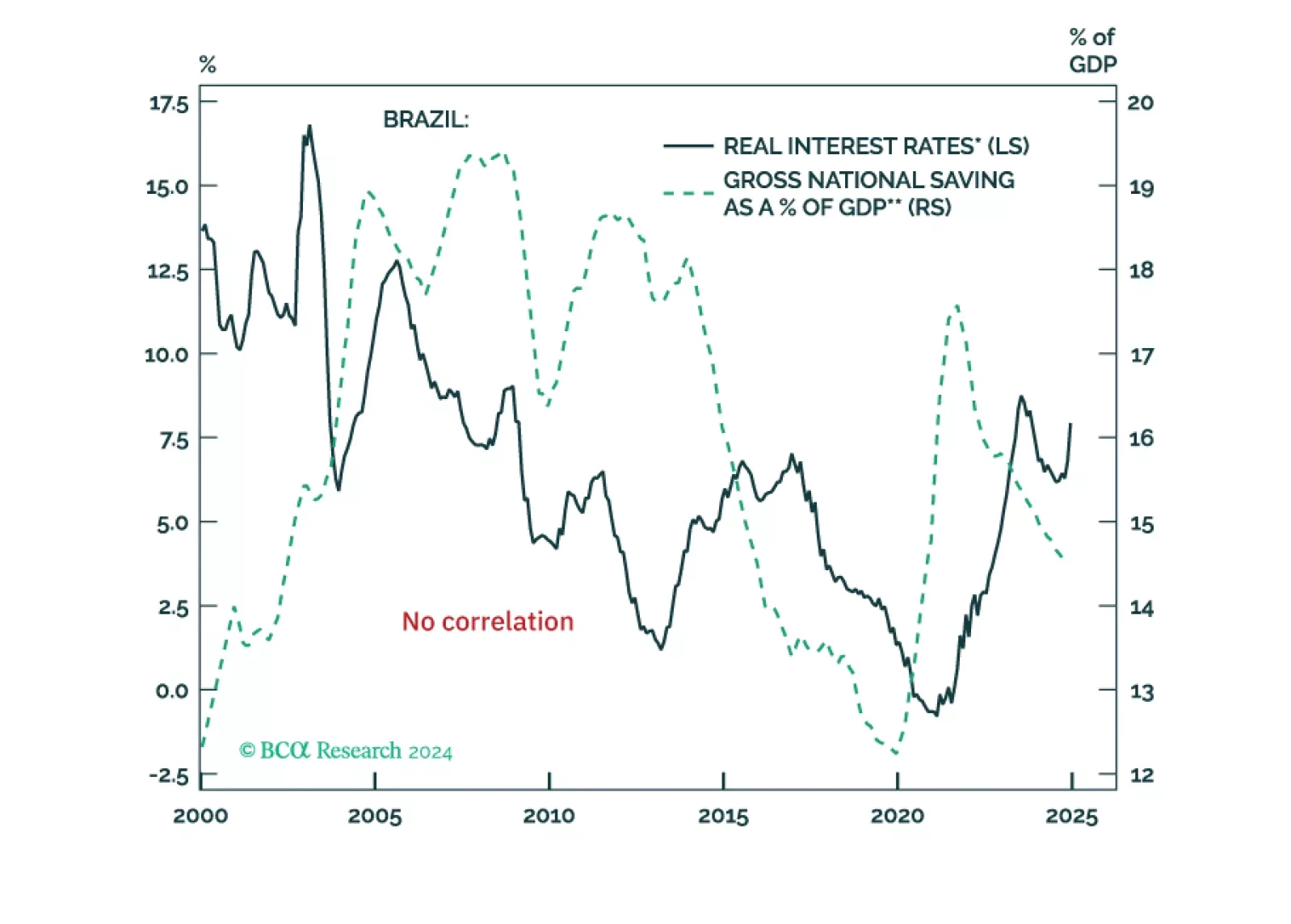

Brazil’s economy is like a patient who has been misdiagnosed and is receiving the wrong treatment. The odds of a complete recovery for this patient are not great. Presently, investors are scrutinizing the details of the announced fiscal adjustments and trying to assess how much the Central Bank of Brazil (BCB) has to hike interest rates to stabilize the exchange rate and inflation expectations. Yet, many miss the big picture: there is no politically feasible fiscal math that would stabilize Brazil’s public debt-to-GDP ratio. Plus, higher interest rates will worsen public debt dynamics by widening the gap between real interest rates and real GDP growth.Therefore, Brazil’s financial markets could rebound from time to time, but these rallies will not be sustainable. We are staying put on Brazilian markets.Simple Fiscal MathAs we have argued over the last several years, unless authorities implement bold and profound changes to fiscal and monetary policies and undertake structural reforms to boost productivity, Brazil’s public debt-to-GDP ratio will continue to rise in the years to come.In particular, we have maintained that neither orthodox macro policies of right-wing governments, the social security reform from 2019, nor President Luiz Inácio Lula da Silva’s fiscal responsibility act of 2023 would stabilize the nation’s public debt-to-GDP ratio. Chart 1 illustrates that the public debt-to-GDP ratio rose substantially between 2016 and 2022 under right-wing governments. The decline in the public debt burden in 2021-23 was due to one-off factors. Specifically, nominal GDP growth surged well above government borrowing costs due to Brazil’s pre-election fiscal stimulus and the spike in commodity prices in 2022 as a result of the Ukraine war . As soon as nominal GDP growth normalized and fell below borrowing costs, the public debt-to-GDP ratio began rising (Chart 1).BCA’s Global Investment Strategy service showed in a recent report that the required primary fiscal balance to stabilize the gross public debt-to-GDP ratio is calculated as follows:Primary Fiscal Balance = (Gross Public Debt / GDP) x (R –G) Where R is government borrowing costs in real terms, and G is the economy’s potential real GDP growth.This fiscal math holds true for any country in the world (including the US, Japan, Canada, Brazil, Korea, etc.) as far as local currency debt is concerned. Chart 2 shows that given the current level of real interest rates, a stable public debt-to-GDP ratio in Brazil can be achieved only if the primary fiscal balance is at a surplus of 4% of GDP (=79% x (7% - 1.8%)). This last data point is derived using these values:Gross public debt-to-GDP ratio (currently at 79%).R = 10-year inflation-linked bond yield (the current level is 7%).G = potential GDP growth (we estimate it at 1.8% = recurring productivity growth of 1.3% plus labor force growth of 0.5%).Even if we assume that R (inflation-indexed bond yields) average 5% over the long term, the required primary fiscal surplus to stabilize the public debt-to-GDP ratio would still be high at 2.5% of GDP (=79% x (5%-1.8%)). In a sense, as long as R > G, the nation needs to run primary surpluses to stabilize the public debt burden.Given that the government has been struggling to achieve a primary balance of 0%, running continuous primary surpluses equal to 2.5-4% of GDP is politically unfeasible.What is the level of real interest rates that would stabilize the public debt ratio with the primary fiscal balance at zero? For the primary fiscal balance to be at zero in the equation above, (R-G) should be zero. Thus, R should be equal to G, i.e., 1.8%.Bottom Line: There is no politically viable path through fiscal tightening that the government in Brazil could implement to stabilize its public debt-to-GDP ratio. The latter will continue rising for the foreseeable future.Drastic tightening of fiscal and monetary policies would also push the economy into recession and cap nominal GDP growth. The combination of high borrowing costs and low GDP growth will push the public debt ratio higher.What Are The Solutions?There is no easy way out to stabilize Brazil’s public debt-to-GDP ratio. Brazil's major macro imbalance is the enormous gap between its very high real interest rates and subdued productivity growth. Resolving this imbalance requires either bringing down real interest rates, lifting productivity growth, or a combination of the two (Chart 3). The most benign path is to meaningfully boost productivity growth via structural reforms. This would lift potential GDP growth and return on capital, attracting substantial foreign investment. The latter would strengthen the currency and tame inflation, allowing the central bank to bring down domestic interest rates. Lower nominal and real borrowing costs would unleash a capital spending boom, further accelerating productivity growth. The upshot would be a virtuous circle of robust productivity gains, currency appreciation, lower interest rates, and more capital expenditures. In short, real interest rates could be brought to or below the nation’s potential growth rate, which would stabilize the public debt-to-GDP ratio.However, there is no evidence to suggest that Brazil is about to embark on aggressive structural reforms to follow this benign adjustment path.Given that substantial structural reforms and running large and recurring primary fiscal surpluses are unlikely to occur, the only other solution for stabilizing public debt is to dramatically bring down real interest rates. The latter would lead to massive currency devaluation and, with it, rising inflation. In this scenario, the government should bring real interest rates down to below the country’s potential real GDP growth of 1.8% (Chart 3).Domestic demand would boom, widening the current account deficit. When nominal and real interest rates decline substantially, capital flight would escalate as residents shift from local currency to foreign currency deposits. The domestic bond market would riot. To bring down bond yields, the central bank might need to resort to bond purchases, which would heighten currency depreciation.While this scenario would unleash a period of major macro instability due to massive currency devaluation and inflation, it would also sow the seeds for a more sustainable macro environment in the future. Over the long term, low nominal and real interest rates would incentivize capital spending and, thereby, boost productivity. High productivity growth would lead to more exports and substantial import substitution, which would eventually steady the exchange rate and bring down inflation. On top of this, the public debt-to-GDP ratio would be stabilized as real borrowing costs drop below the rate of economic growth.Bottom Line: Running large and successive primary fiscal surpluses is politically unviable and aggressive structural reforms are unlikely for now. Therefore, the sole realistic choice Brazil has is to bring real interest rates below real potential GDP growth for its public debt-to-GDP ratio to stabilize. If it fails to do so, its public debt burden will continue rising for the foreseeable future. Does Brazil Have Enough Savings To Finance Investment?A common counter-argument from economists to the above analysis would be the following: If Brazil lowers real interest rates, (1) the national savings rate will plummet, and (2) banks will not have deposits to finance investment expenditures. Therefore, capital spending cannot be revived, and productivity growth will not increase despite very low real borrowing costs.We somewhat agree with the first point about a possible drop in national savings. However, we completely disagree with the second point about banks needing deposits or savings to finance investments. We discussed this issue in detail in our report titled "Is Investment Constrained By Savings? Tales Of China And Brazil." The key takeaways from that report pertinent to Brazil are as follows:Financing of investments is not constrained by national and foreign savings. In an economy where banks exist, "savings" and “financing” are very different things. Money supply and the national savings rate are not correlated in any economy in the world (Chart 4, top panel).Many investors use the term "savings" to refer to bank deposits. Yet, in macroeconomics, national and household "savings" are not related to deposits or money in the banking system at all. This is true for all countries, including Brazil (Chart 4, bottom panel).Brazil and other low "savings" rate nations do not need to raise interest rates to curtail consumption and boost savings in order to release funds for financing capital expenditures. Chart 5 demonstrates that there has been no positive relationship between real interest rates and the national savings rate in Brazil. Remarkably, even though real interest rates were often very elevated, that still did not lead to high "savings."Brazilian households do not need to save more for companies to obtain bank financing for their investments. In any country that has its own currency (excluding currency board systems), banks do not need deposits or "savings" to lend. Commercial banks simultaneously create money/deposits “out of thin air” when they originate loans or buy securities from non-banks. Given that the supply side of Brazil is very weak/undeveloped, the natural consequence of financing investments by creating money will be considerable currency depreciation. However, if continual capital expenditures lead to high productivity and enhance the supply side of the economy, the exchange rate would stabilize and inflation would subside over time.The key difference between Brazil and China is not their propensity to consume versus save. Rather, it is the ability to produce goods and services domestically. So long as a nation builds and maintains plentiful productive capacity, its banks can originate loans "out of thin air" and finance capital and consumer expenditures. China and the “Asian Tigers” (Hong Kong, Singapore, South Korea and Taiwan) have done exactly this. In fact, China’s unrelenting money creation “out of thin air” has led to deflation (Chart 6). The Middle Kingdom has overdone this by misallocating capital, i.e., creating redundant productive capacity and loss-making enterprises. Bottom Line: What Brazil needs is to build efficient and competitive productive capacity. To do this, their monetary authorities first need to bring down real interest rates, and banks need to expand their balance sheets to finance capital expenditures. The natural consequence of this will be considerable currency depreciation. Over time, however, currency depreciation and expanded productive capacity will boost exports and import substitution. In brief, an improving trade balance, stronger economic growth/higher return on capital, and ensuing foreign capital inflows will stabilize the exchange rate. Higher productivity and a stable currency will tame inflation, placing Brazil on a sustainable growth trajectory. Unfortunately, Brazil is not close to achieving this.Investment RecommendationsWe reiterate our short/underweight positions in Brazilian markets: Stay short BRL / long MXN (Chart 7, top panel).Maintain the short Brazilian banks / long Mexican banks strategy (Chart 7, bottom panel). Underweight Brazilian local currency and sovereign credit and neutral on stocks within their respective EM portfolios (Chart 8). We will delve deeper into the cyclical economic outlook and discuss markets in more detail in Part 2 of this report, to be published tomorrow.Arthur BudaghyanChief EM/China Strategistarthurb@bcaresearch.comPlease follow me on LinkedIn