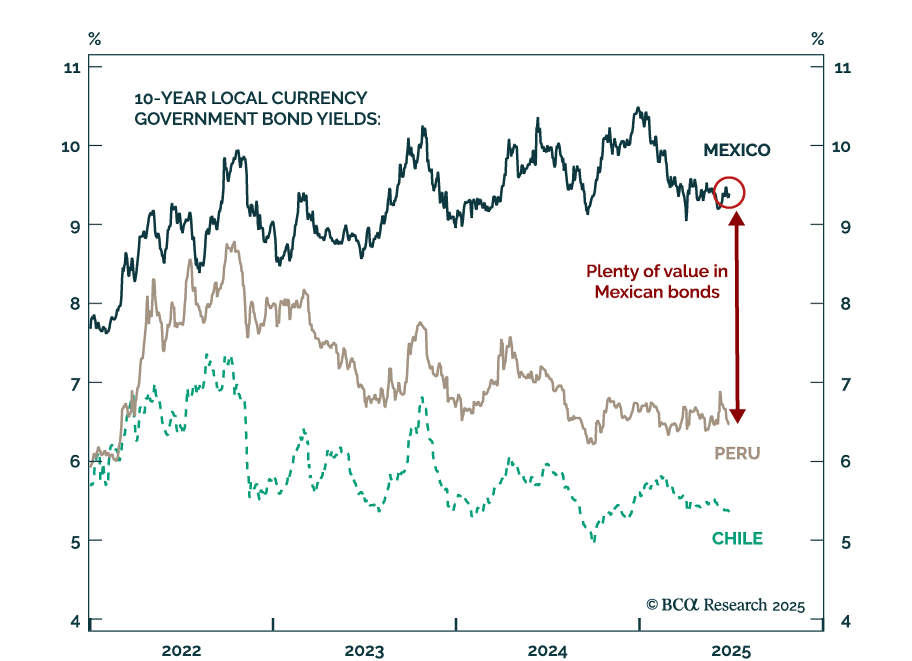

Latin America

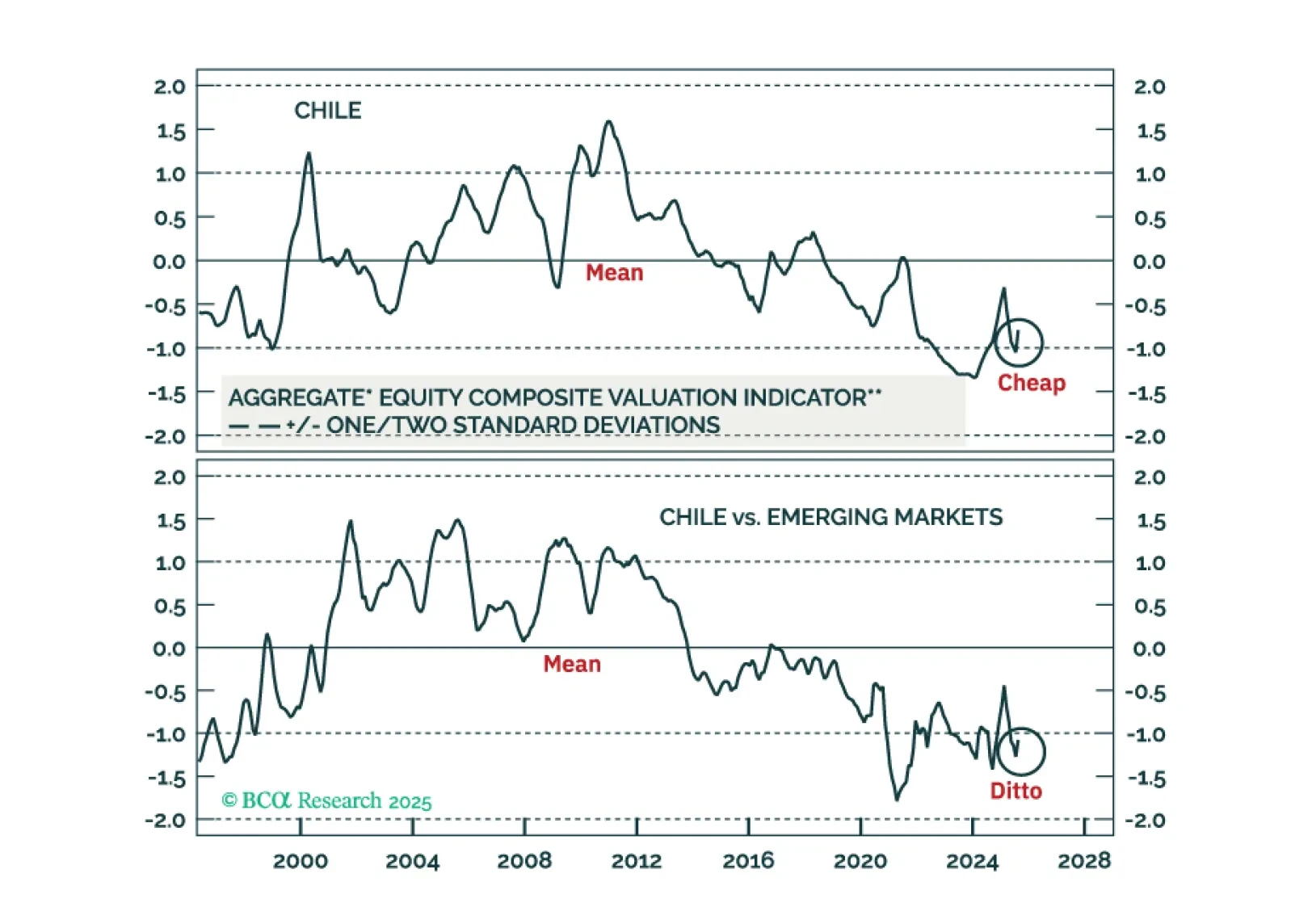

Chilean equities are undergoing a structural re-rating. A political swing back to a pro-business administration, a benign macro backdrop, and a resilient exchange rate will drive Chilean markets’ outperformance versus EM peers.

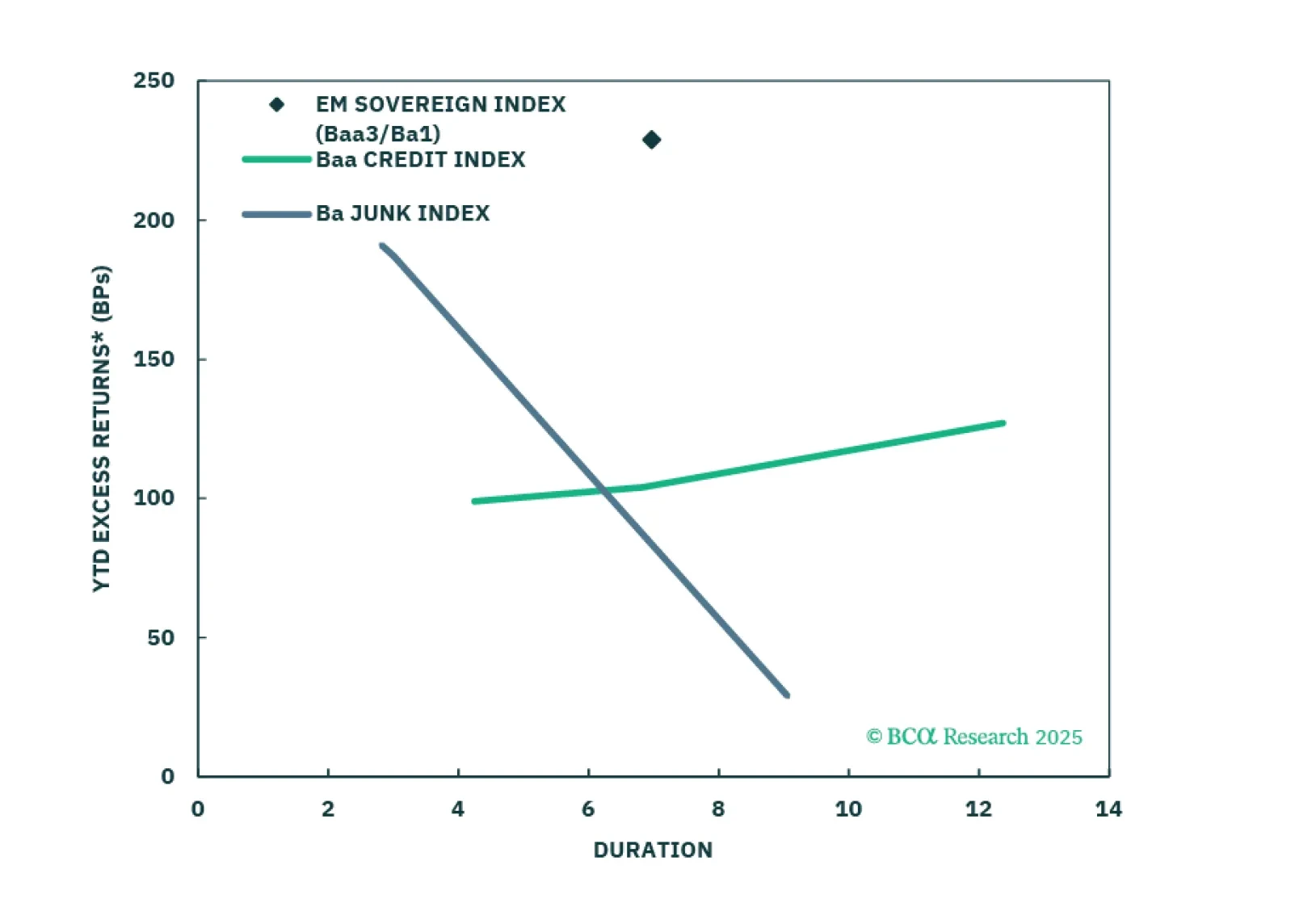

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

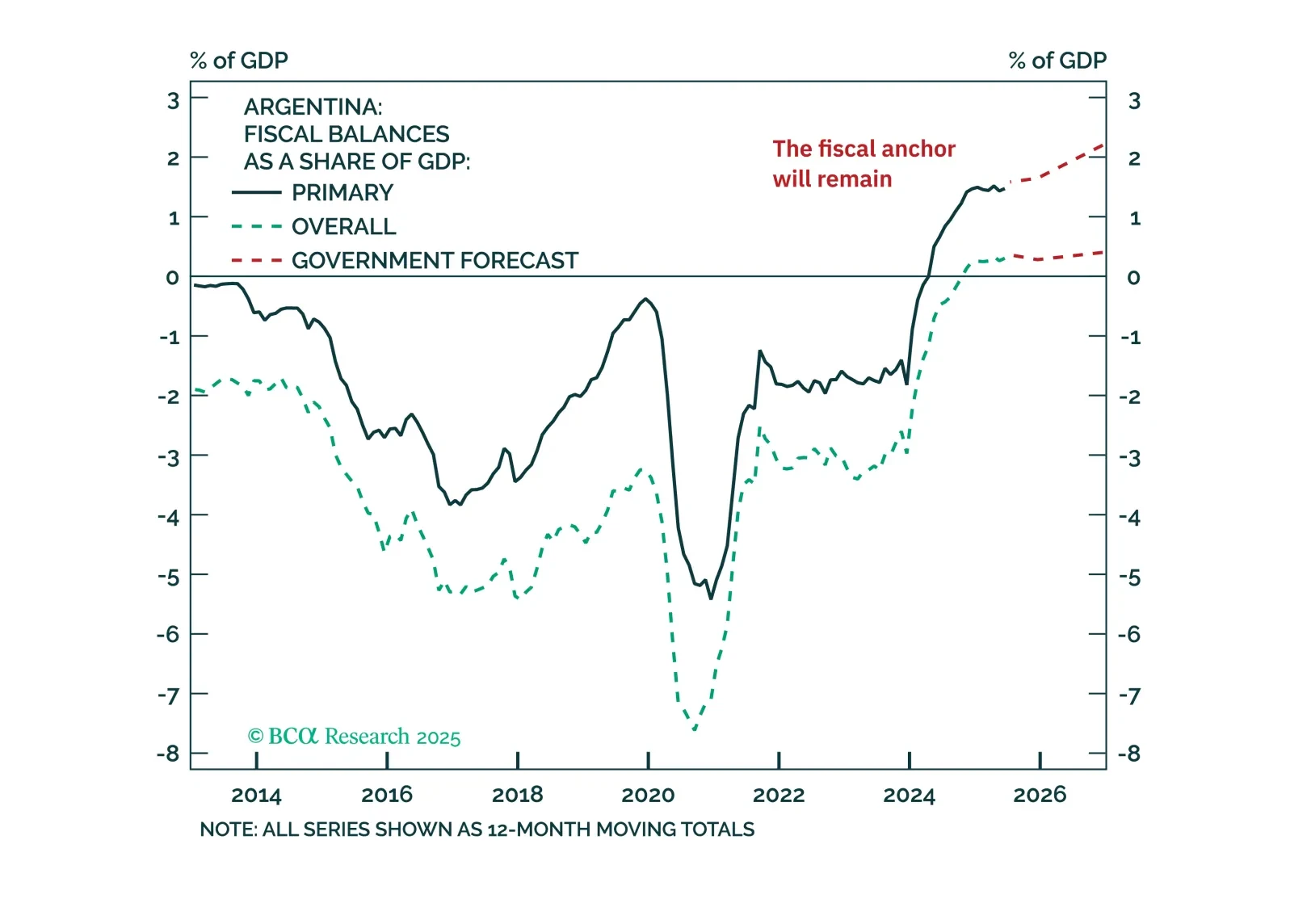

The Buenos Aires election results are a setback for the government's political momentum, but not the endgame. Our long-term bullish view remains in place, but short-term investors should stay on the sidelines in the near run.

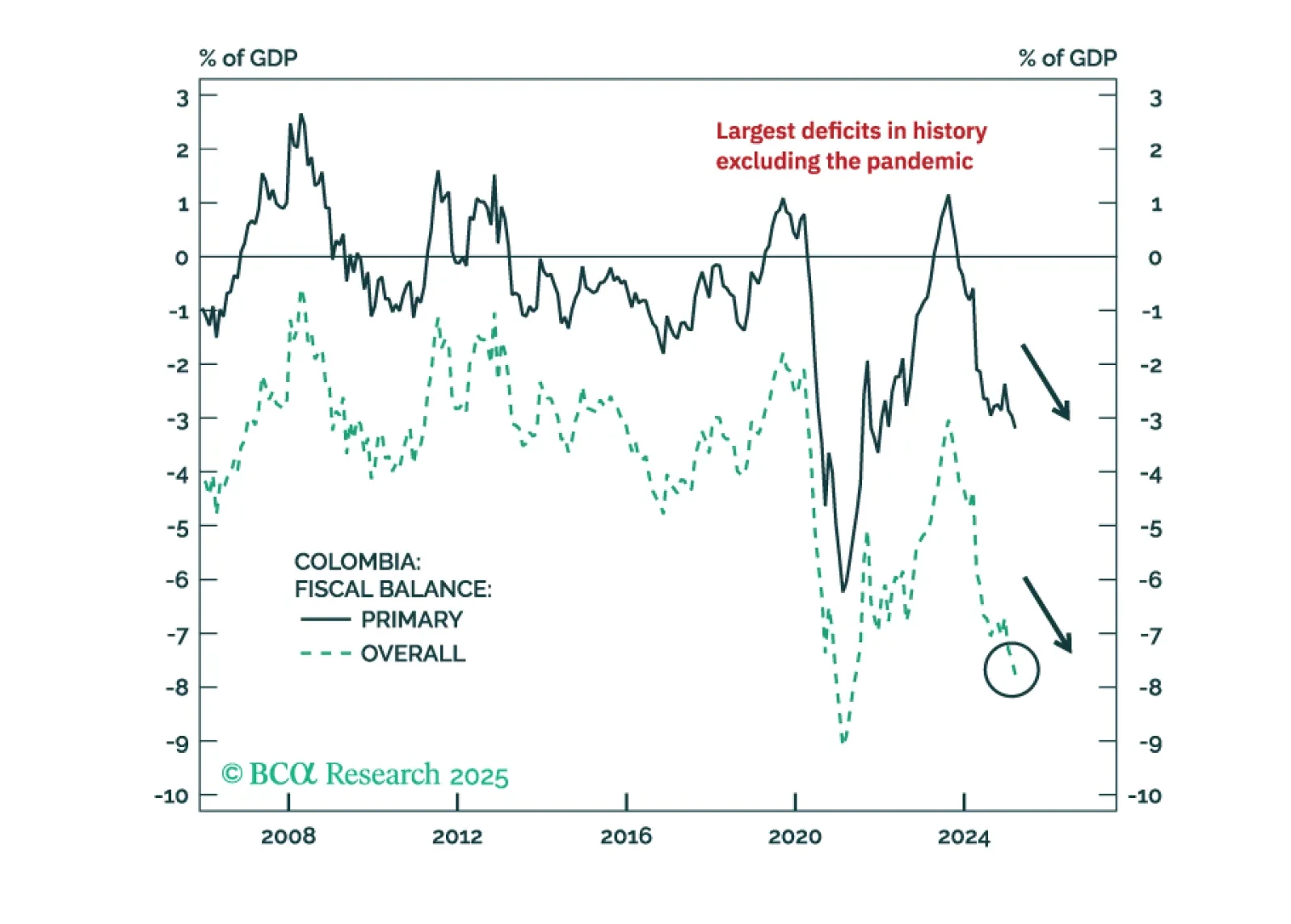

Colombian markets will be torn between expectations of future orthodox policies and the reality of a worsening macro backdrop in the next 12 months. To balance risks, we are upgrading Colombian equities, local bonds, and sovereign credit from underweight to neutral versus their respective EM benchmarks.

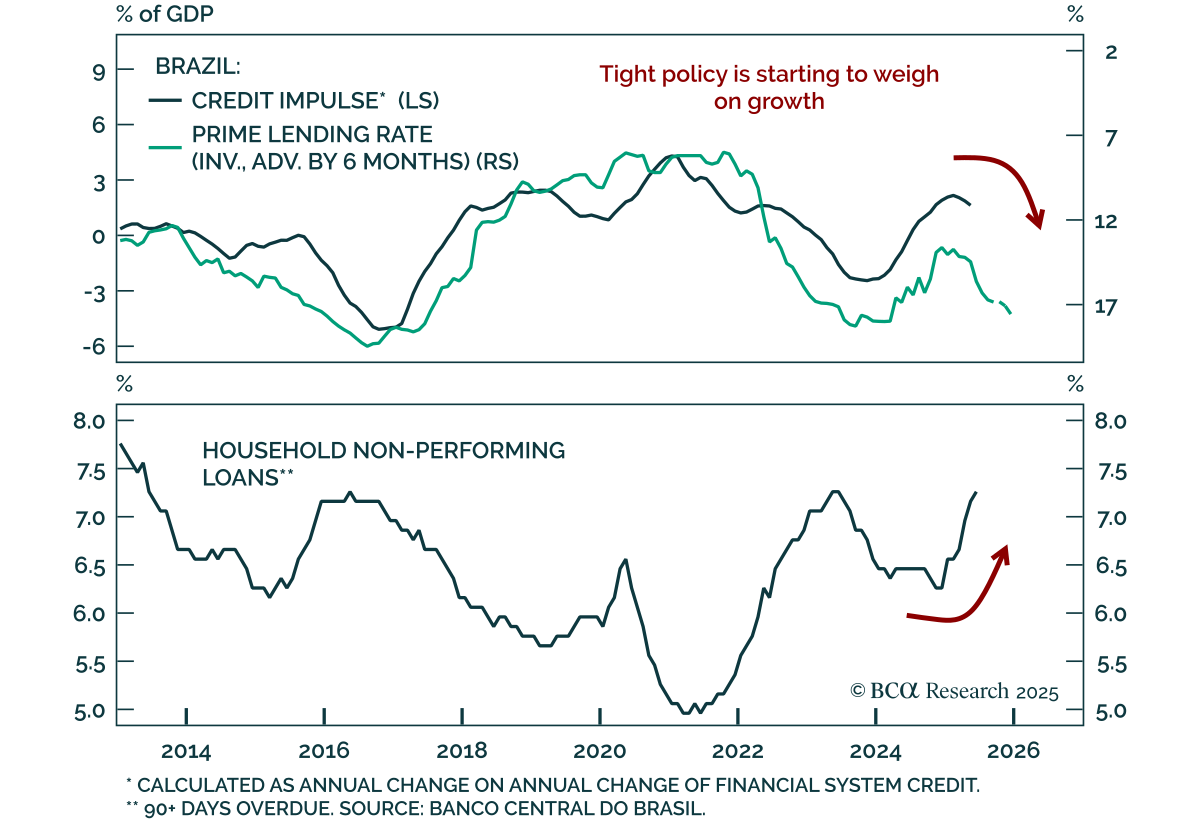

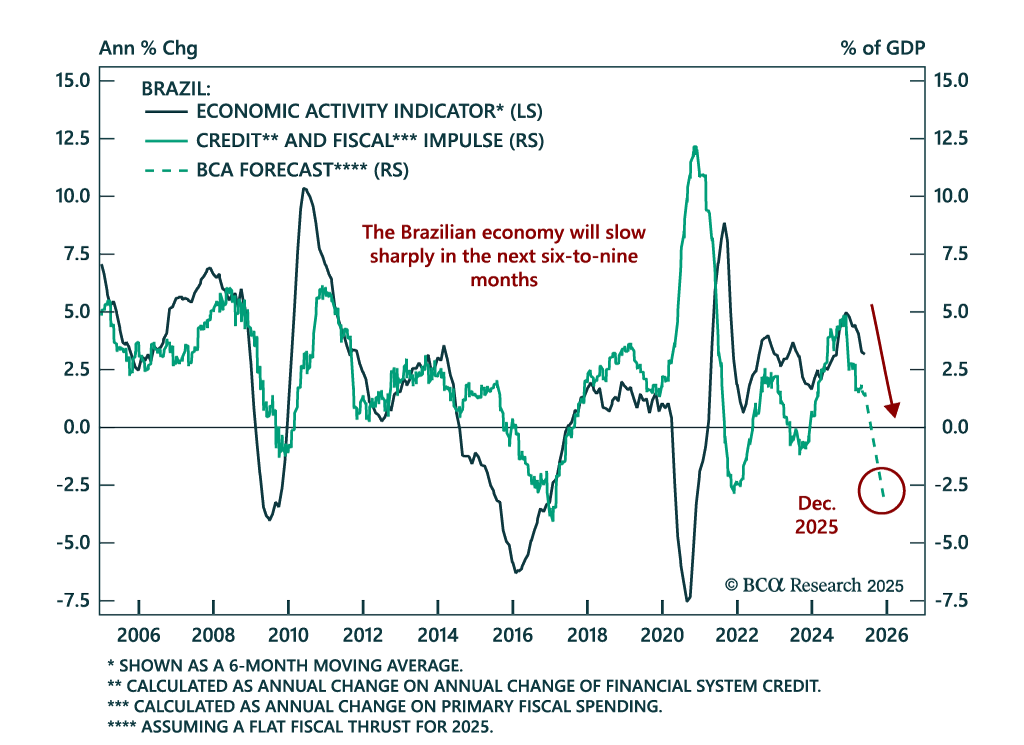

Despite widespread investor optimism Brazil’s currency outlook is challenged by a toxic mix of poor external, fiscal, and macro fundamentals. Expect BRL to underperform most EM peers.

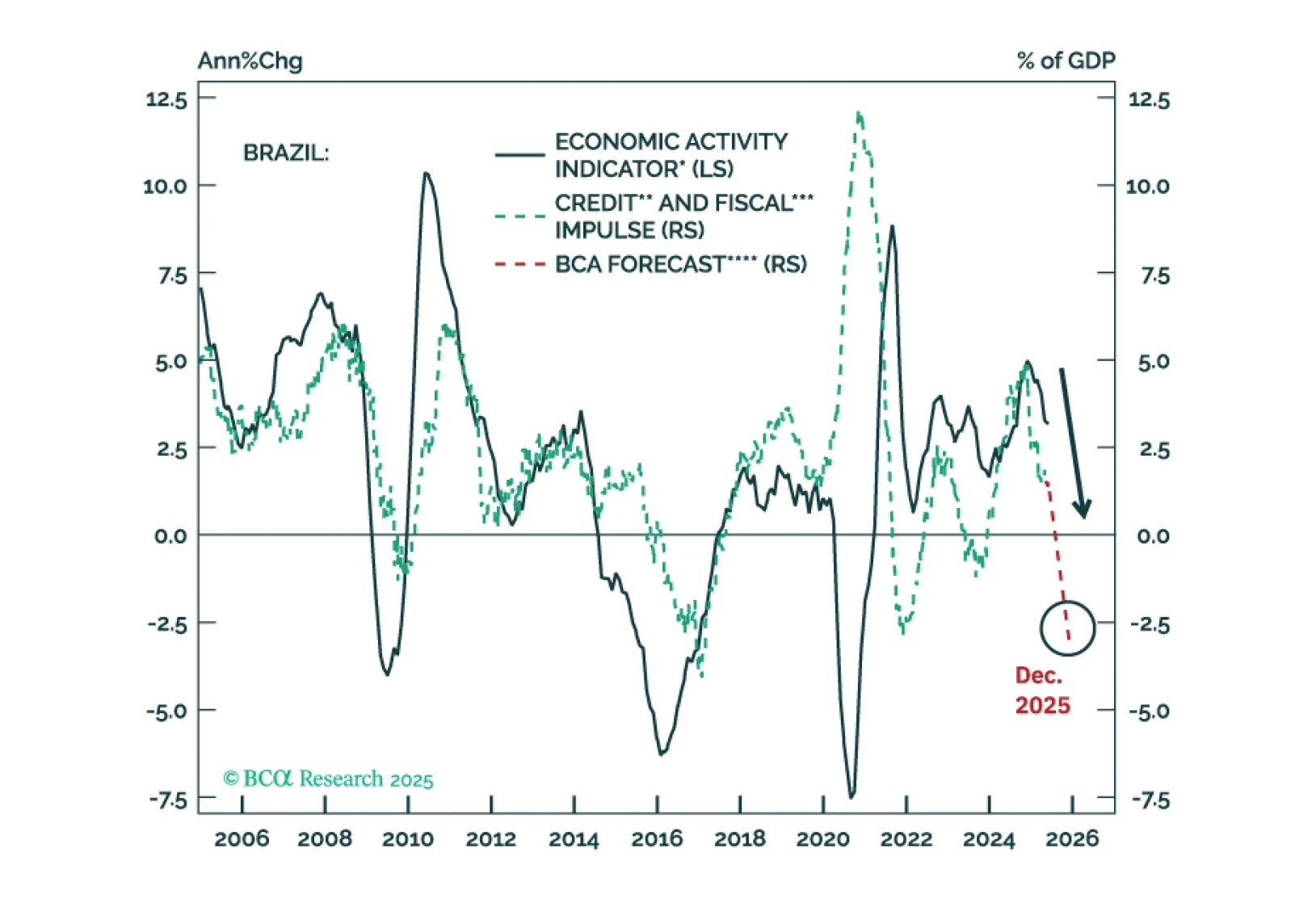

A potential right-wing government in 2027 will not stabilize the trajectory of the public debt-to-GDP ratio. Unsustainable public debt, a large current account deficit, and a sharp growth slowdown will lead Brazilian markets to underperform EM. Yet, to benefit from a quickly decelerating economy, we recommend receiving 2-year swap rates.

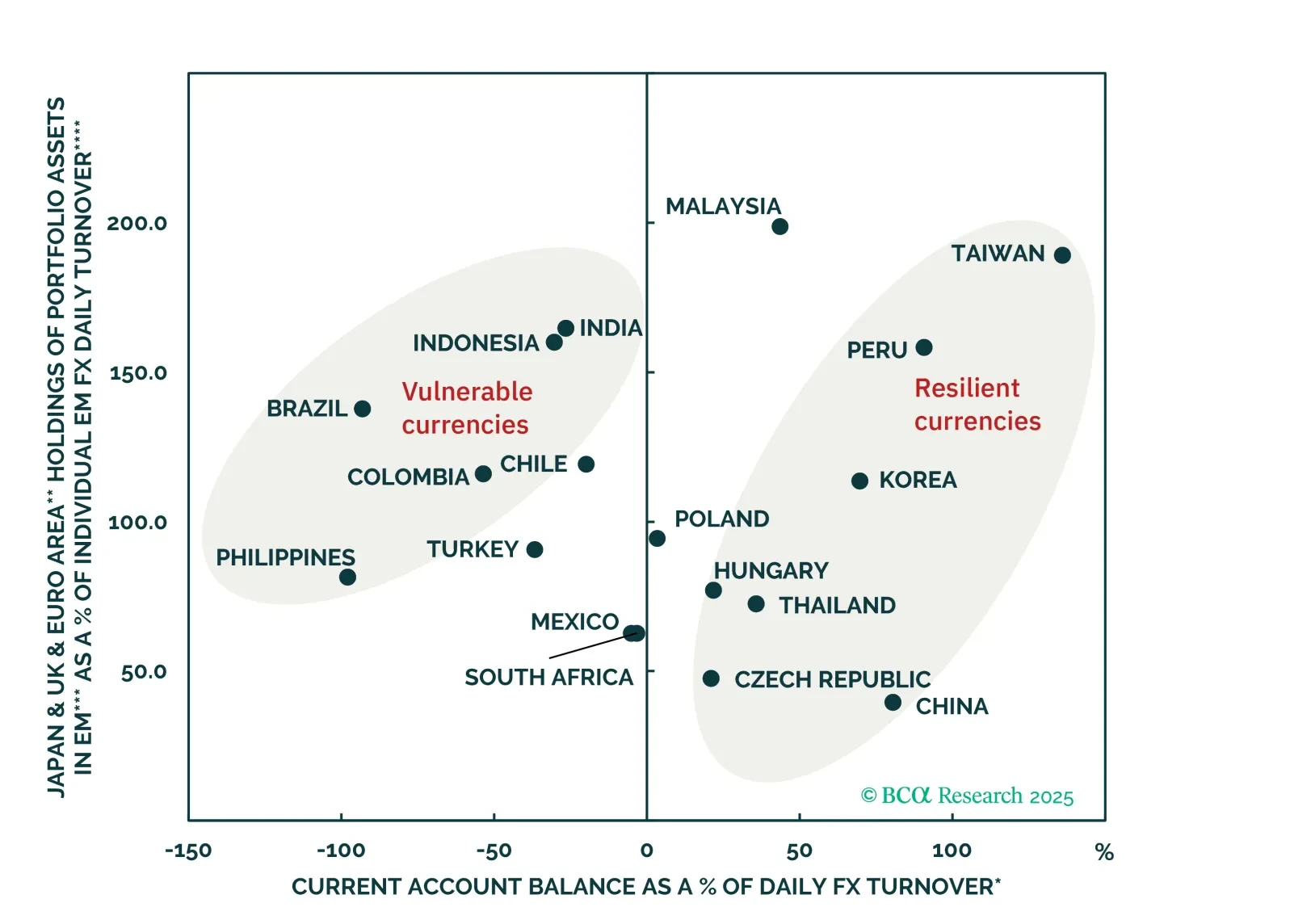

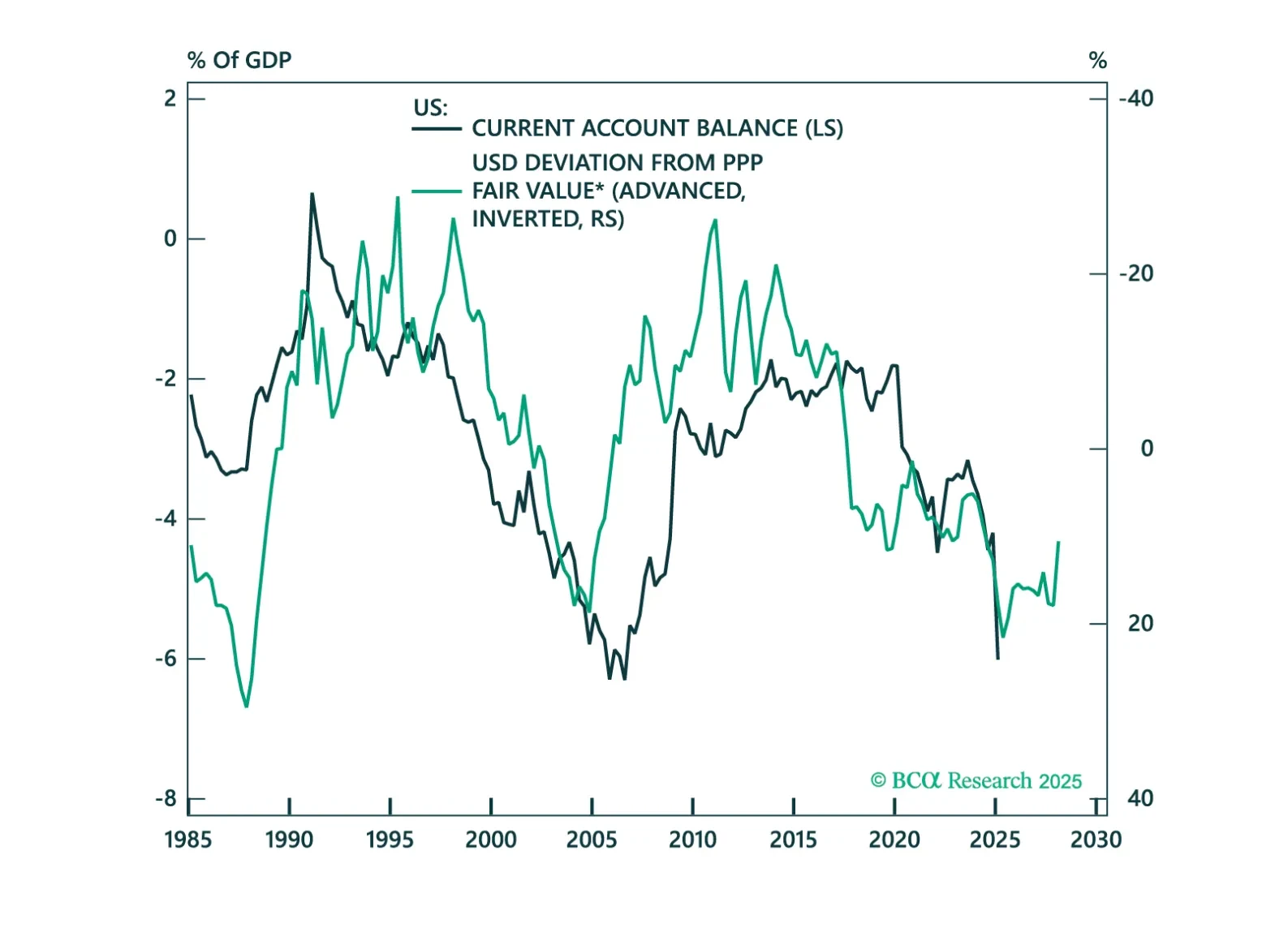

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.