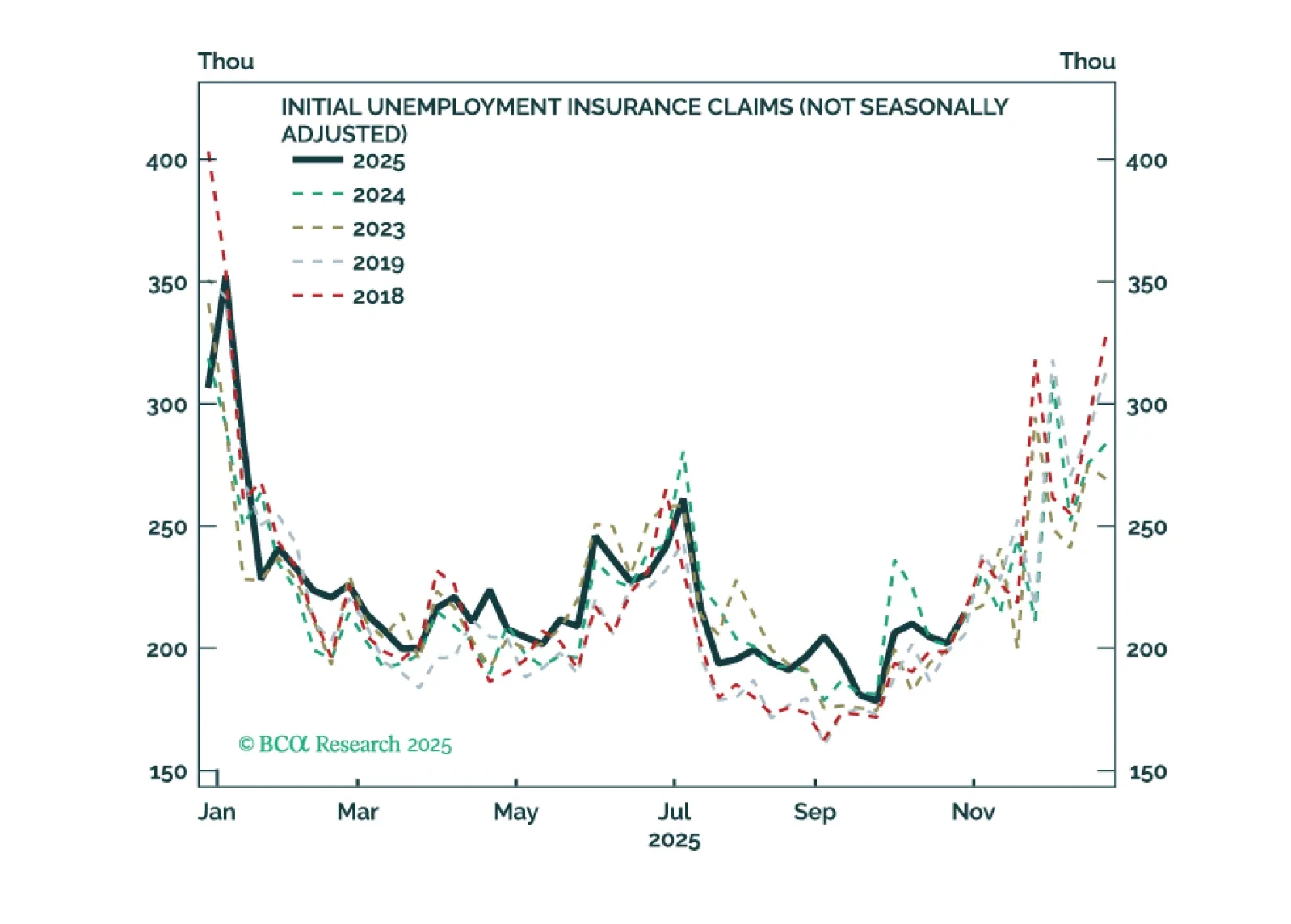

Labor Market

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

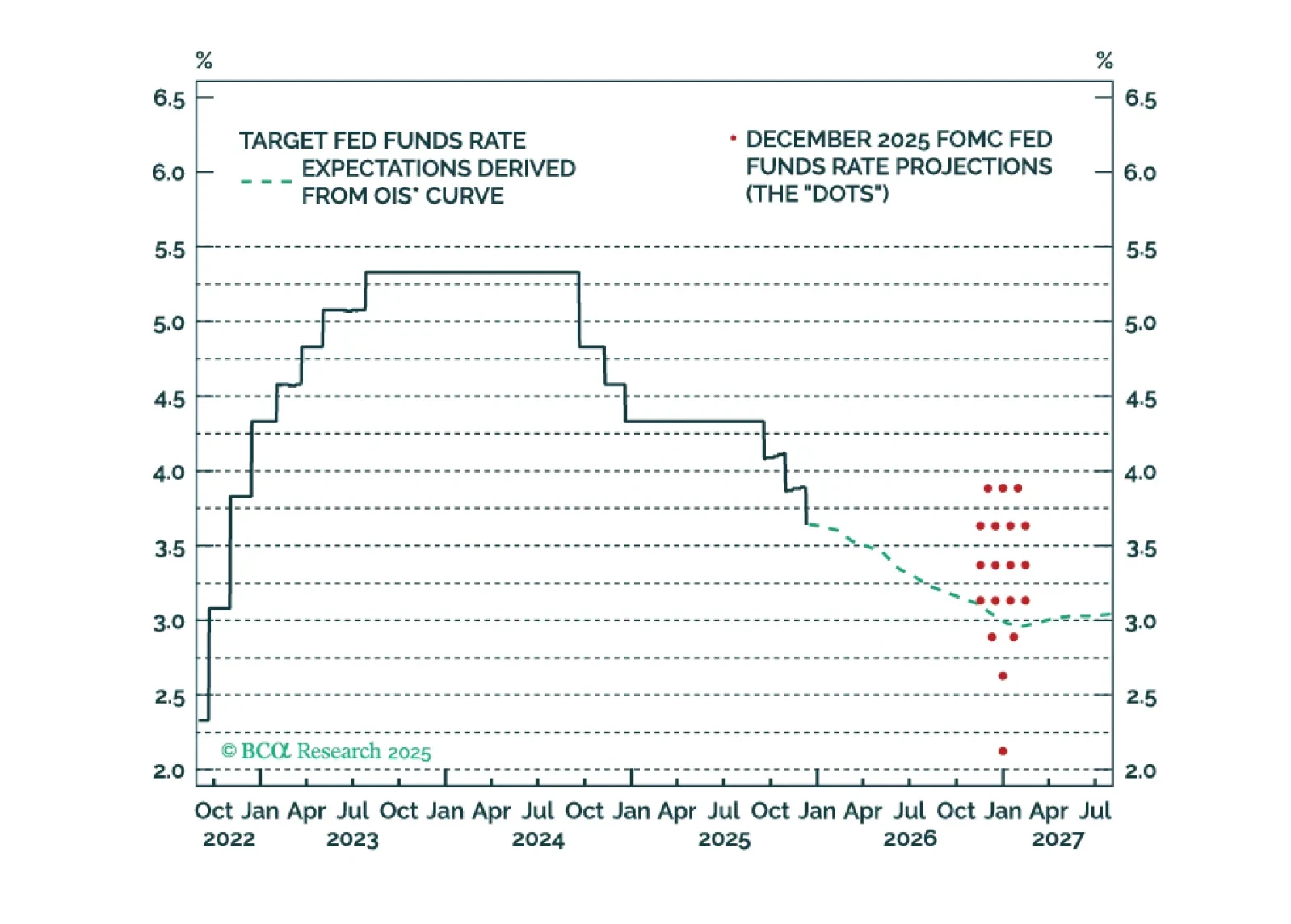

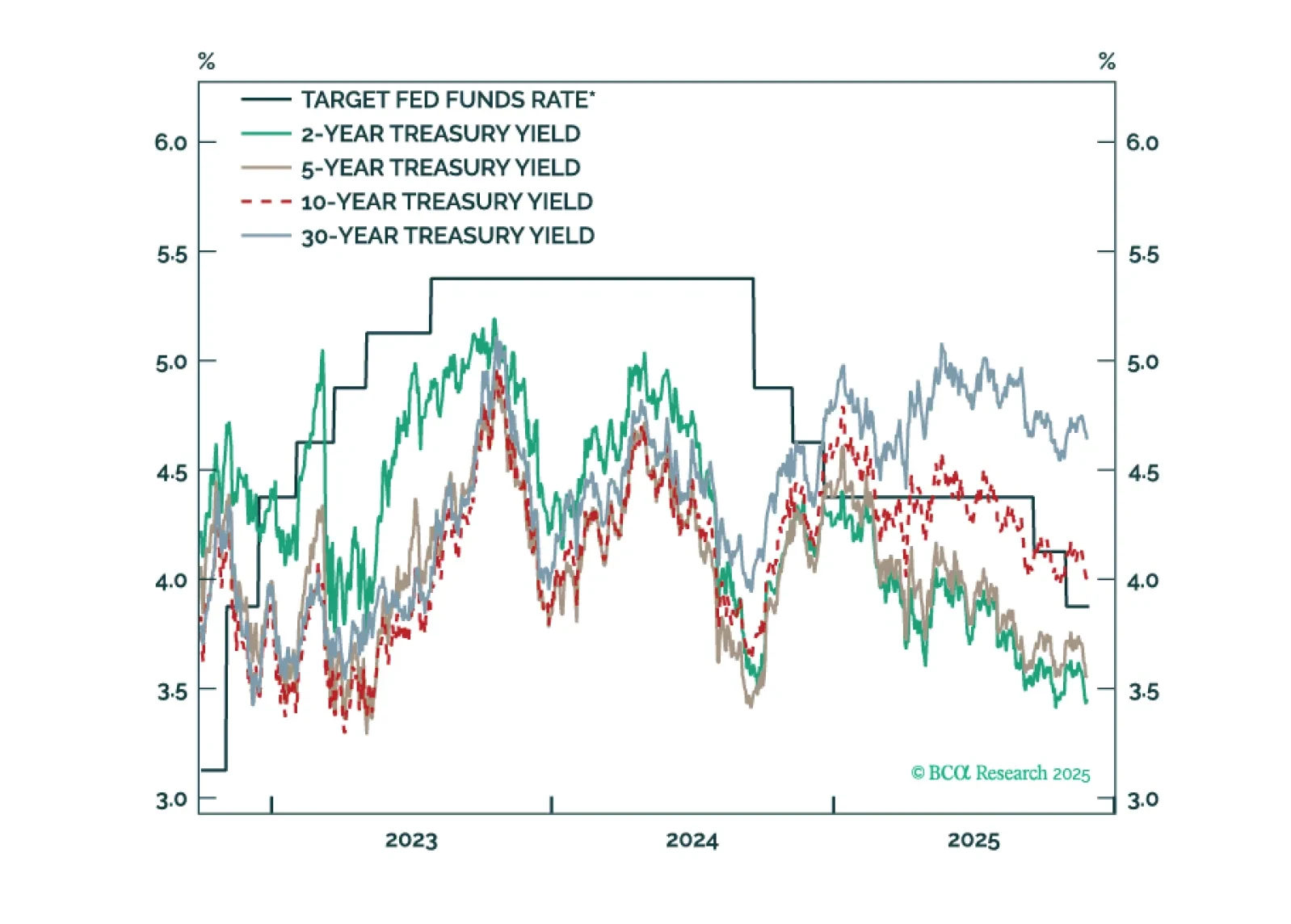

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

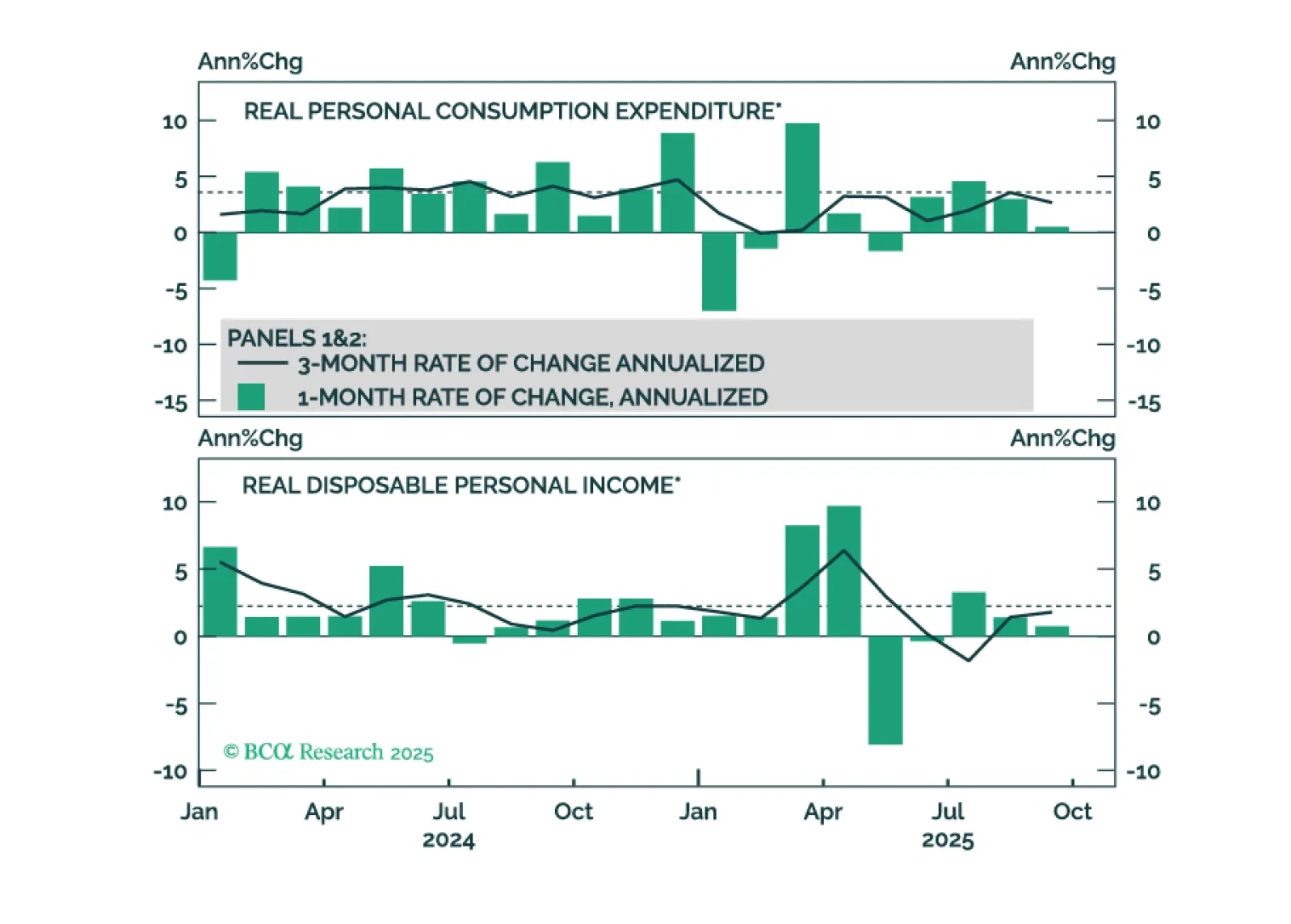

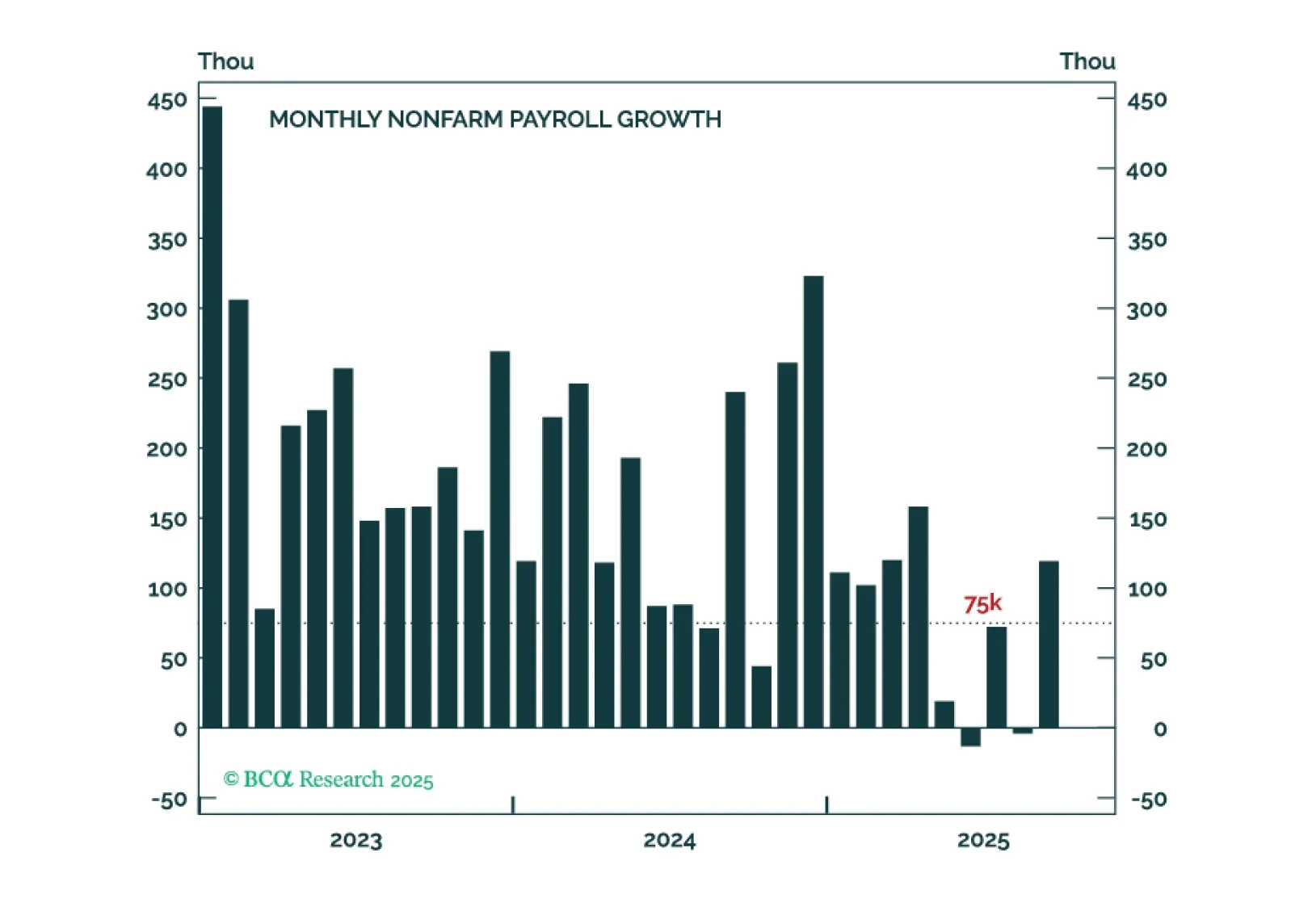

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

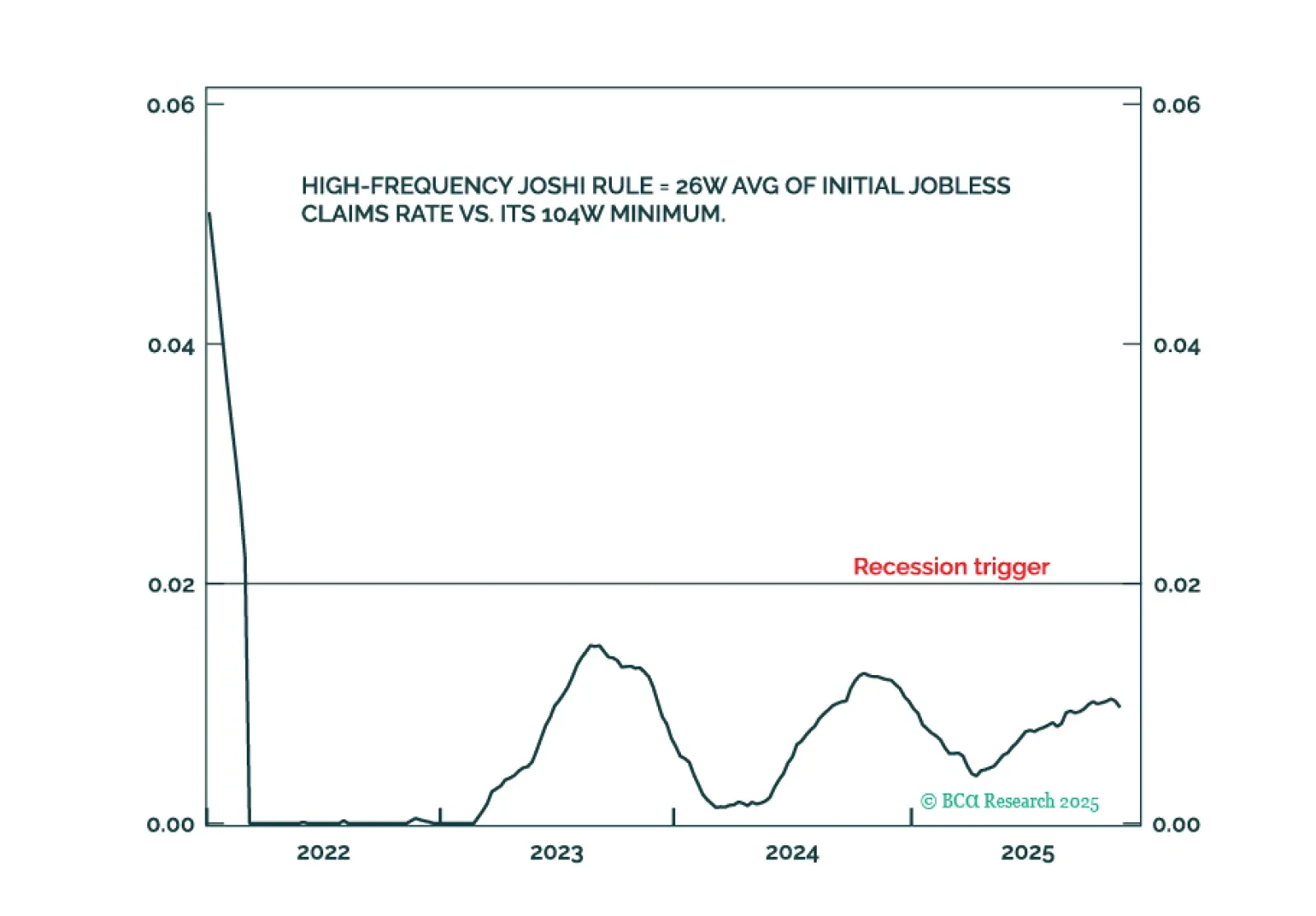

The high-frequency Joshi Rule confirms that the US labour market is holding up. Equity investors should regard 5-10 percent selloffs as tactical buying opportunities. Bond investors should stay underweight US duration. Plus, a new high-conviction trade is to go overweight the 30-year German bund versus the 30-year US T-bond.

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

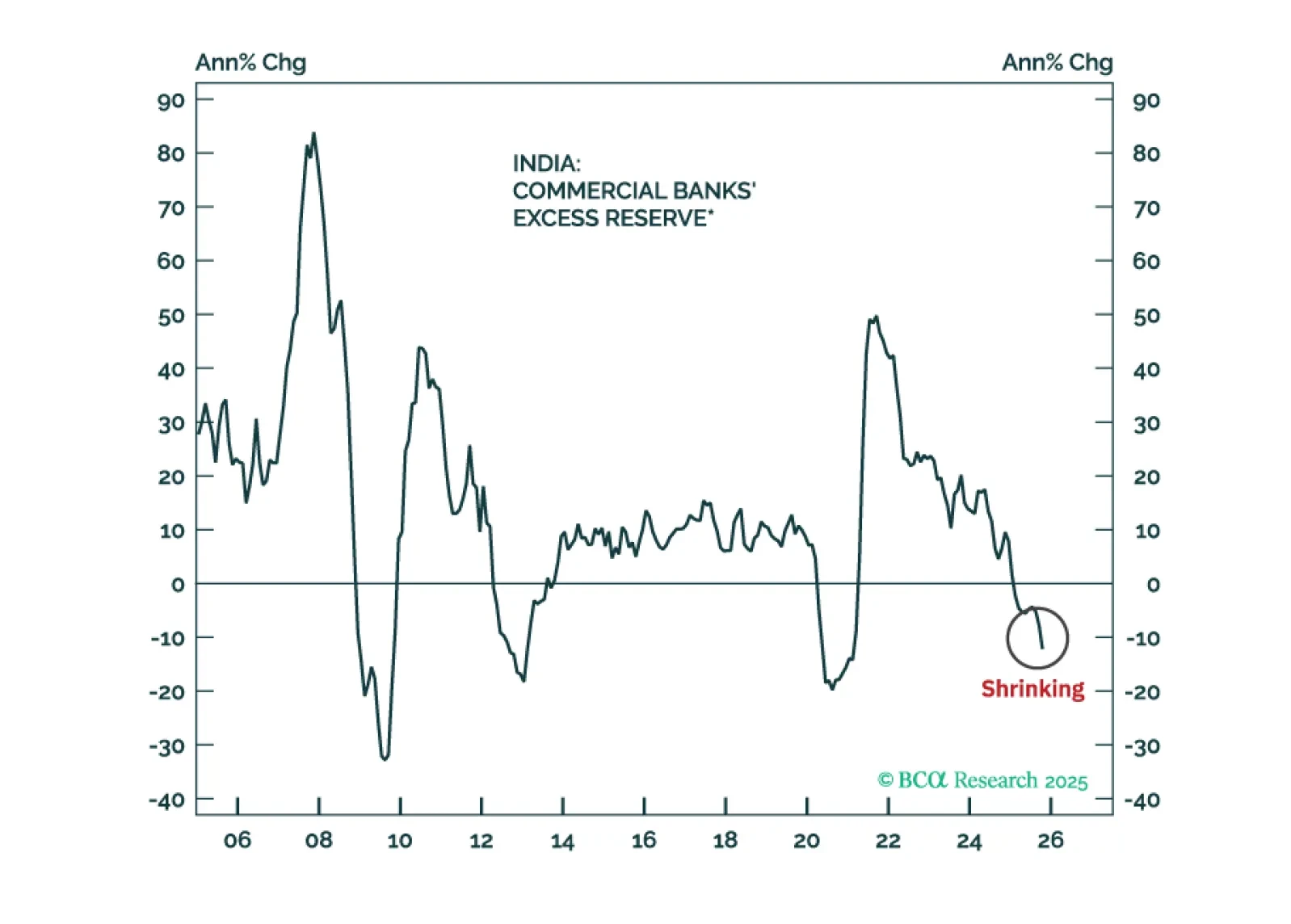

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

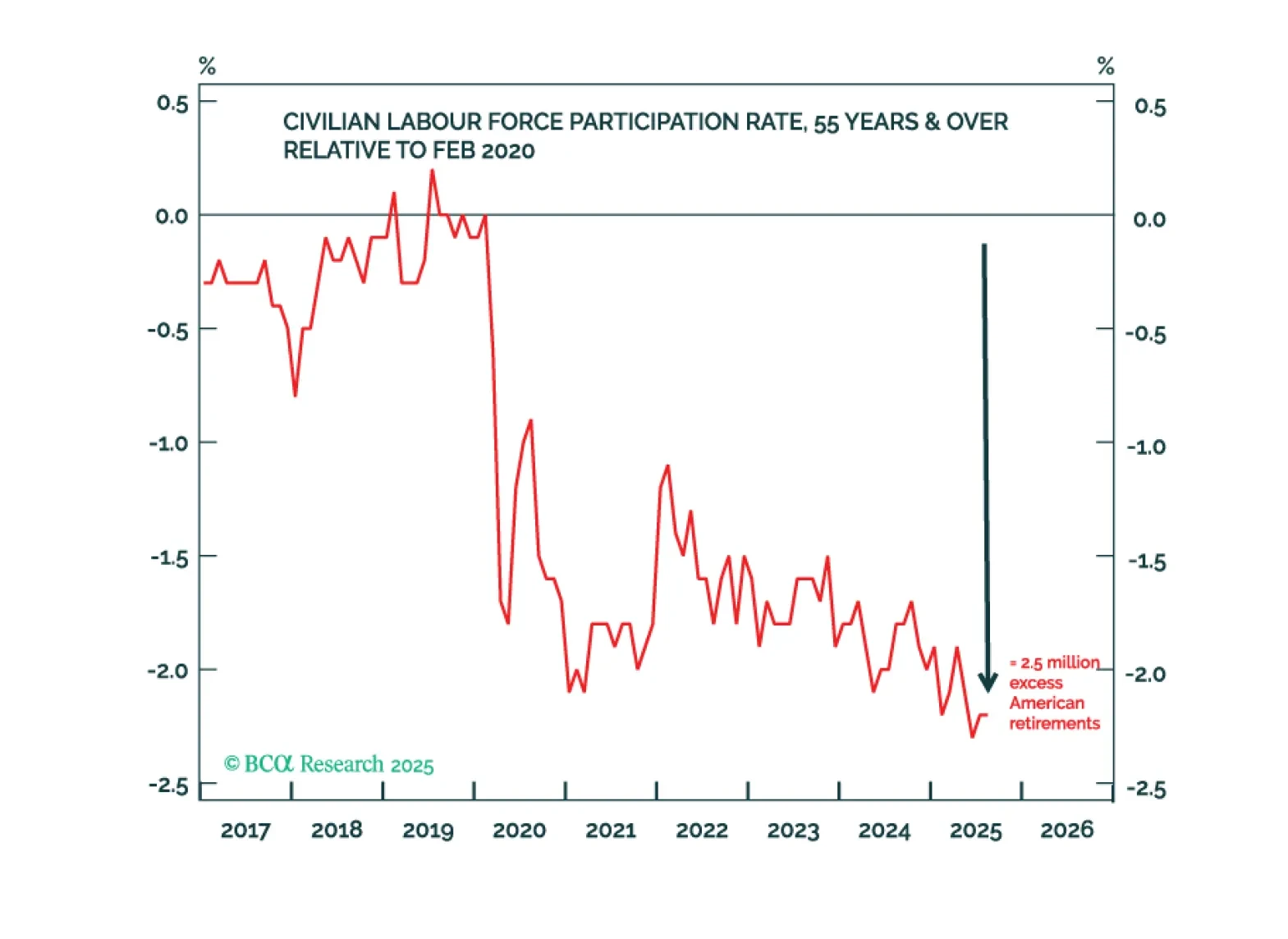

The greater risk to the world economy in 2026-27 is not that a recession triggers a market crash, but that a market crash triggers a recession. This is because a market crash will destroy the wealth that is funding the crucial marginal spending of 2.5 million excess American retirees. Plus, a new tactical trade is: Overweight Switzerland (SMI) versus UK (FTSE 100).