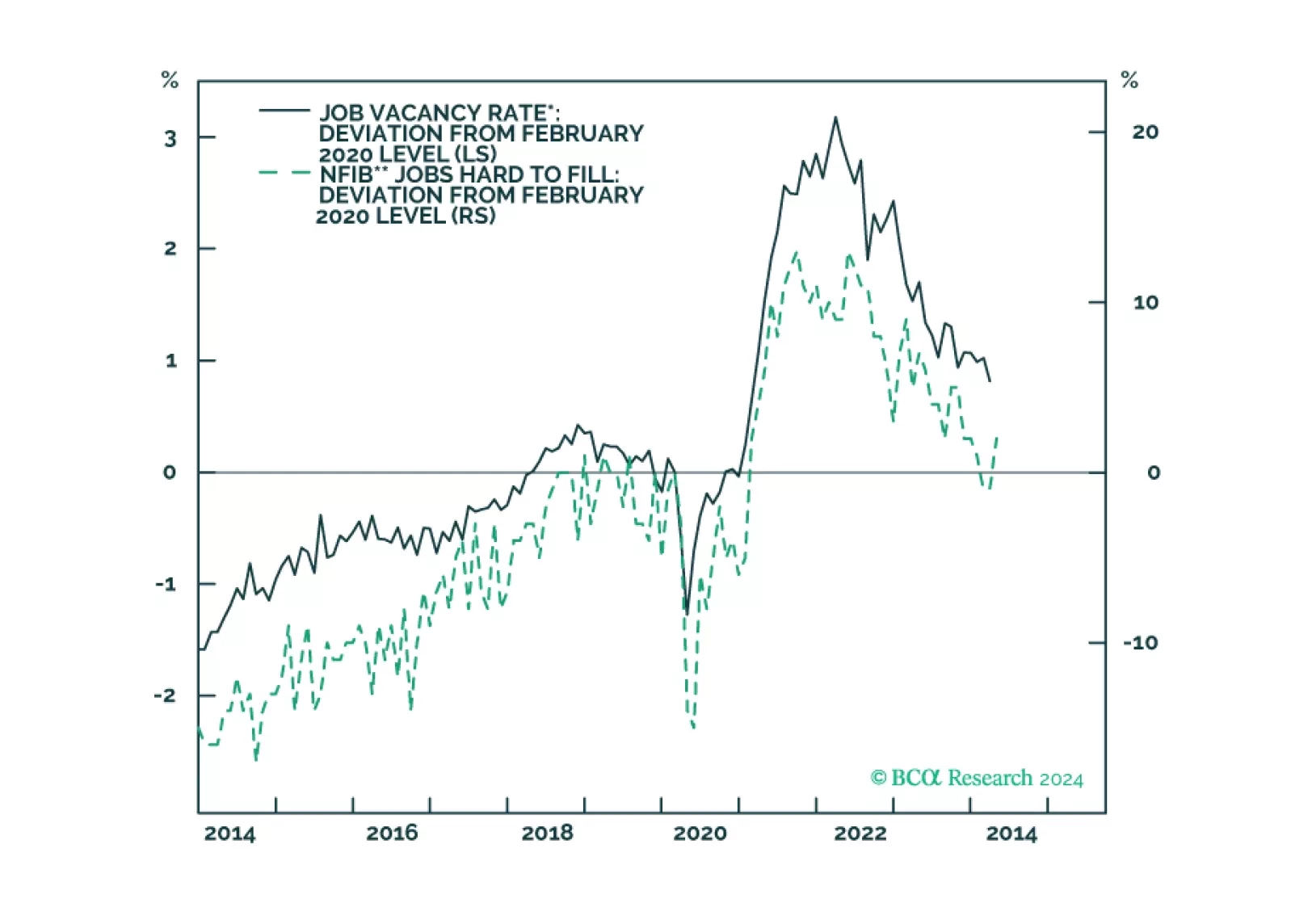

Labor Market

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.

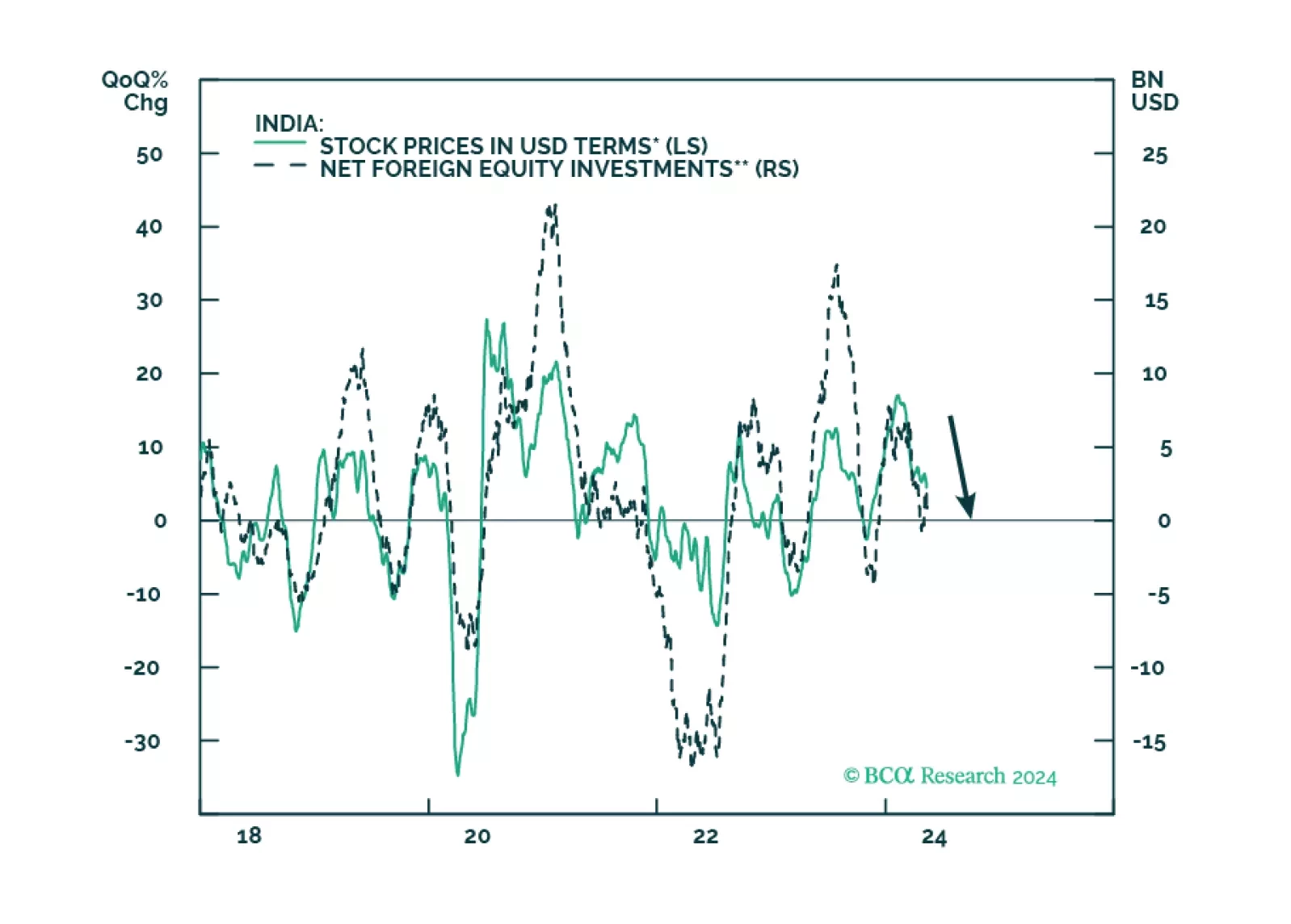

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.

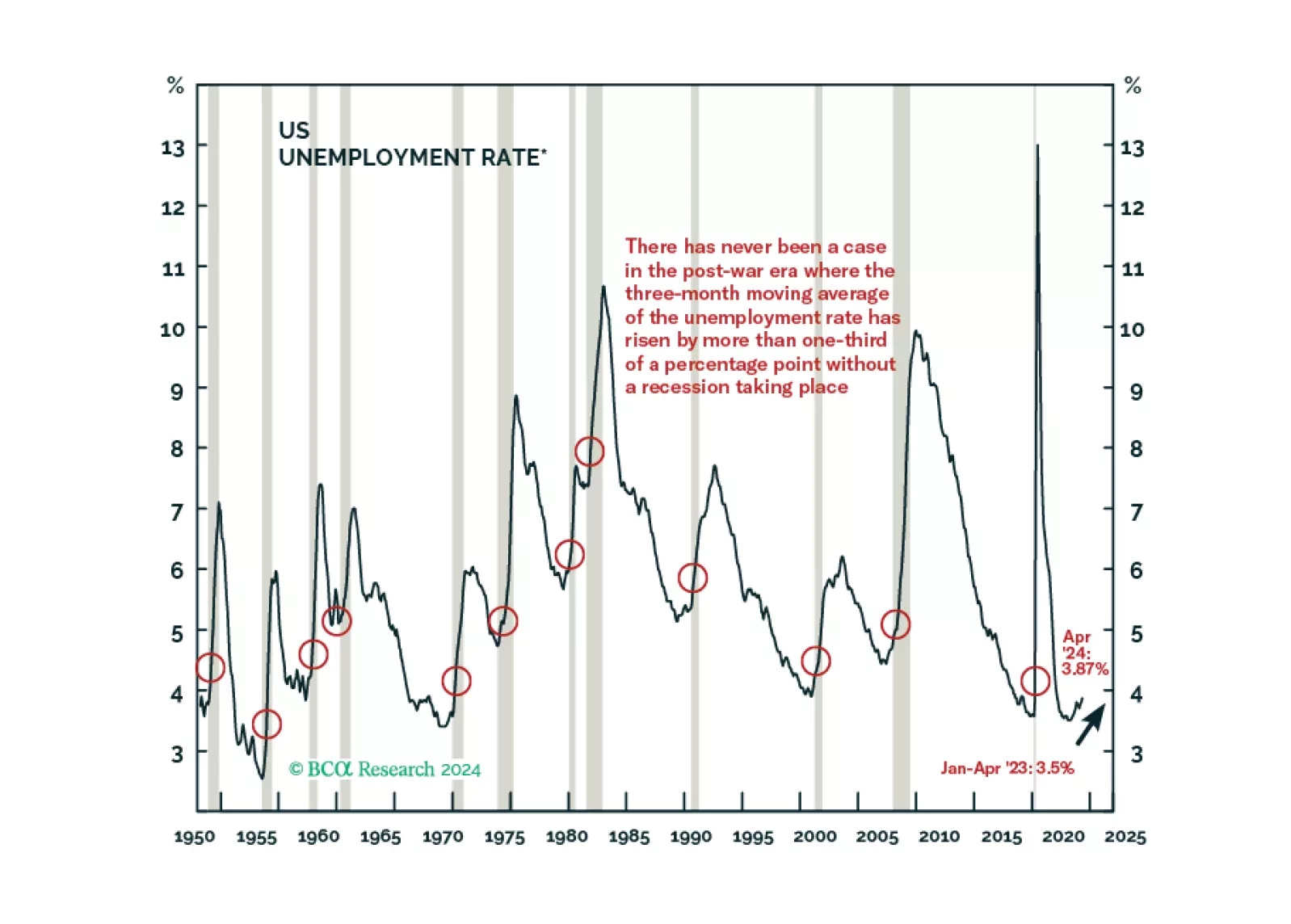

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.

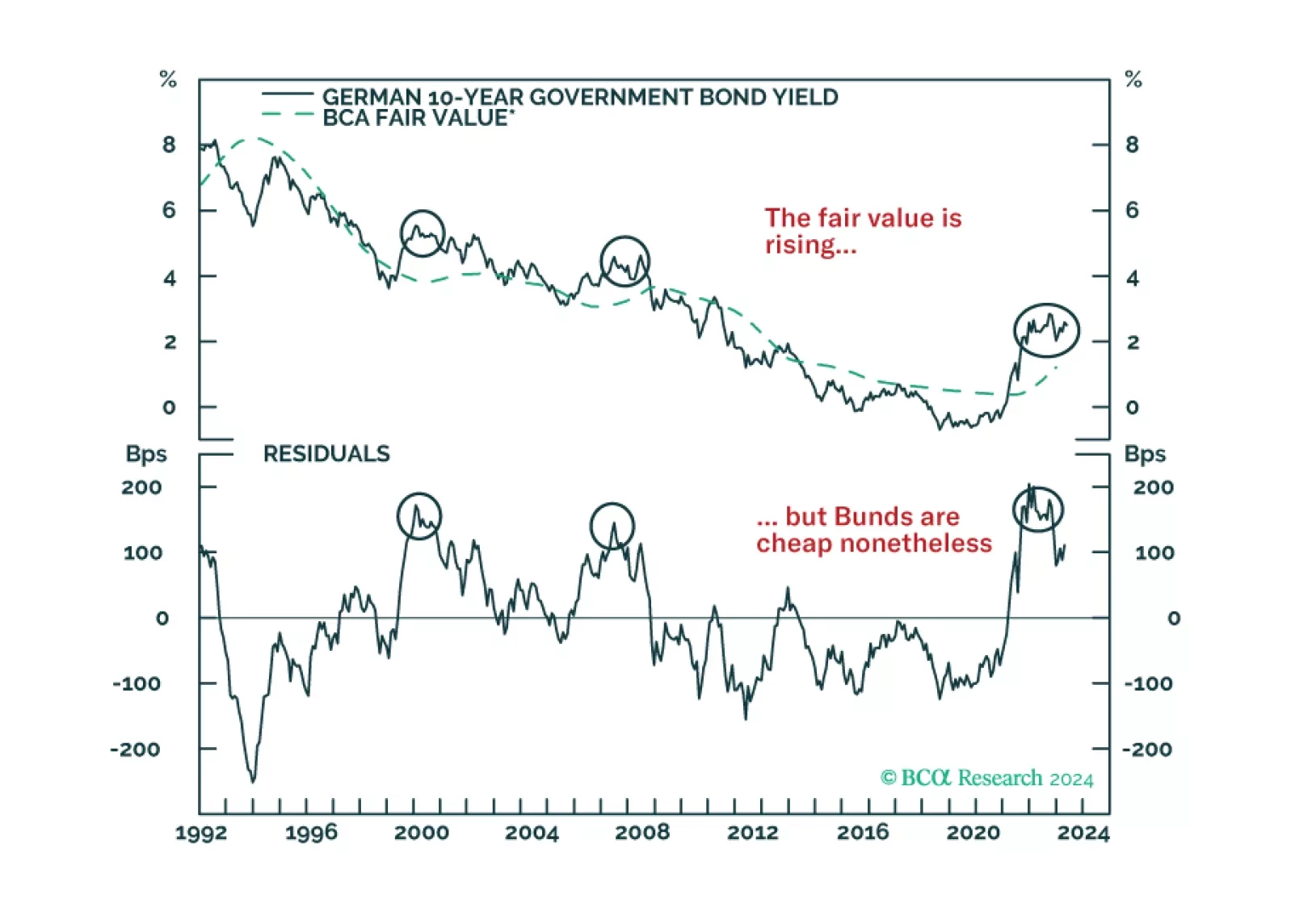

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

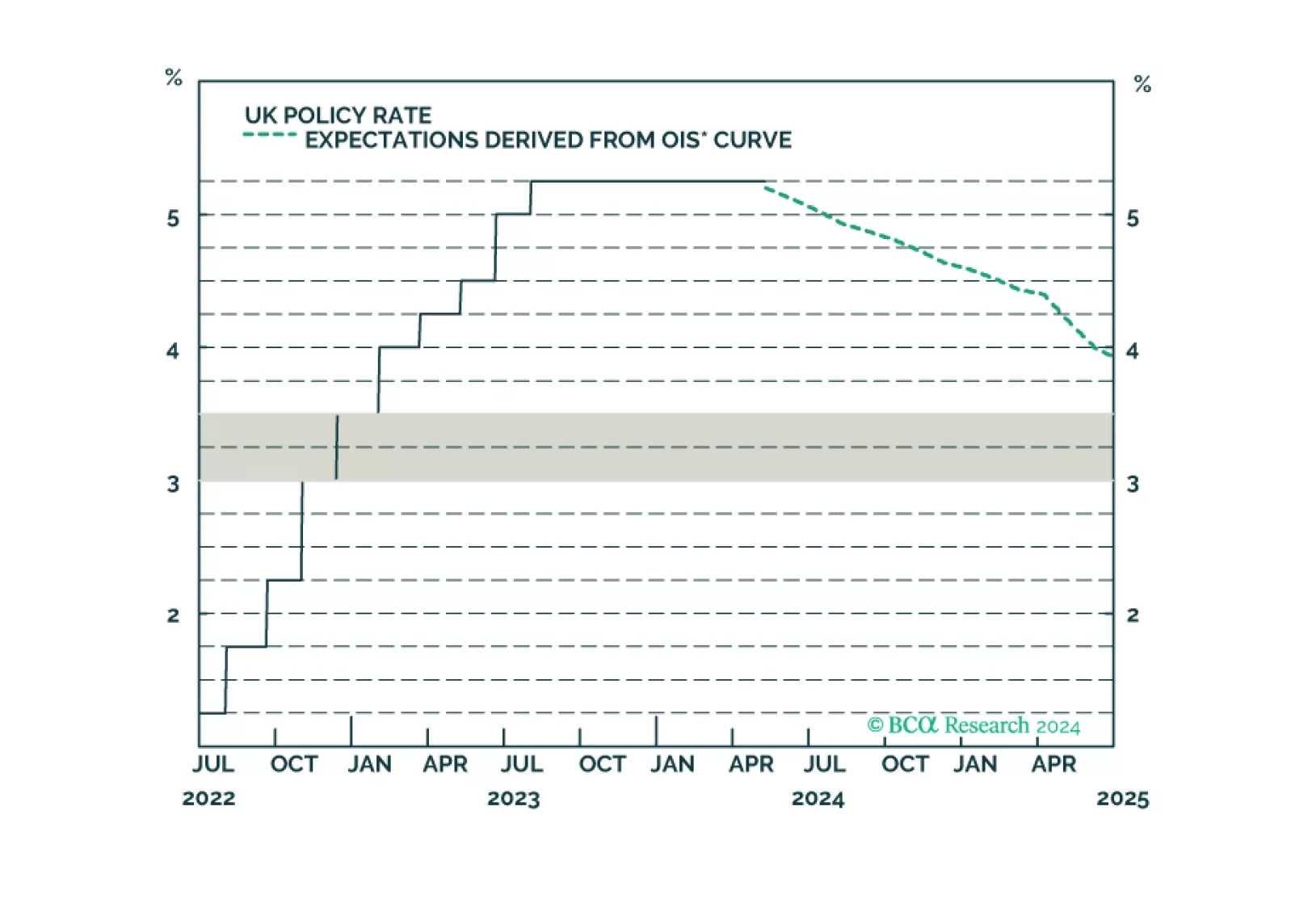

An update to our views on UK rates and currency following today’s Bank of England meeting.

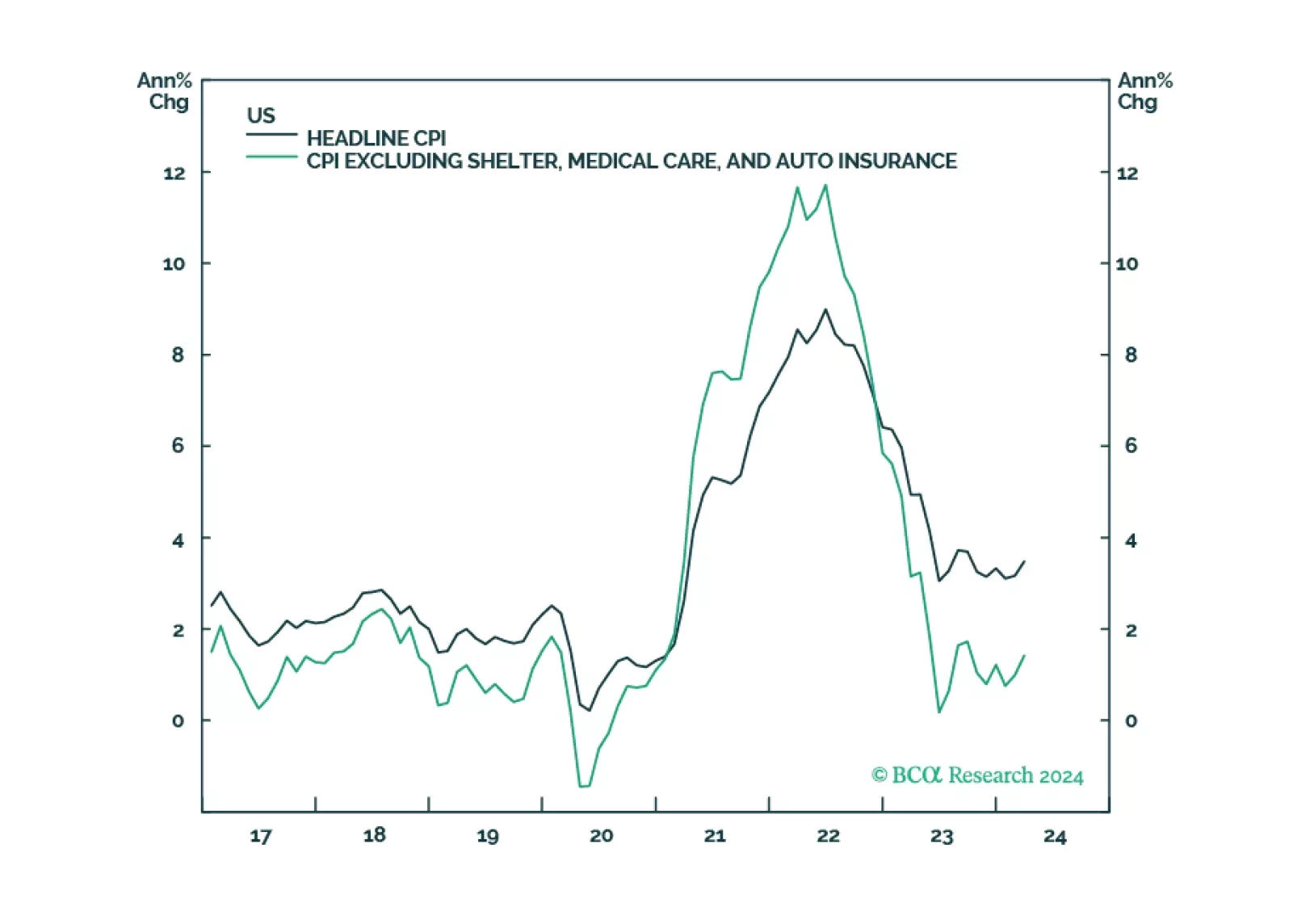

In this week’s report, we defend four out-of-consensus claims. Claim #1: Underlying inflation in the US is not reaccelerating. Claim #2: The US labor market is set to weaken abruptly. Claim #3: The S&P 500 will drop to 3700 in 2025. Claim #4: Japan is not in danger of a currency crisis.