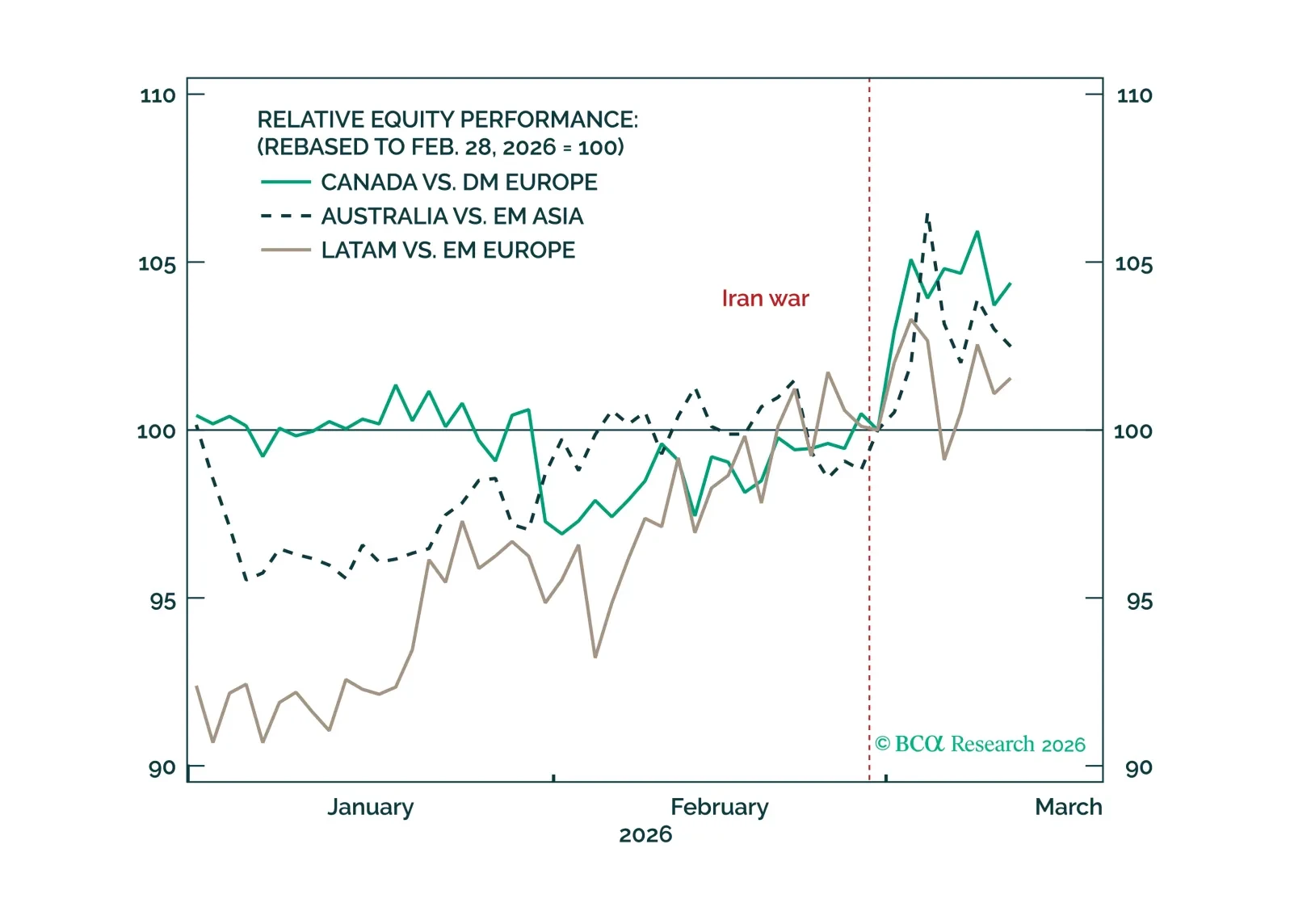

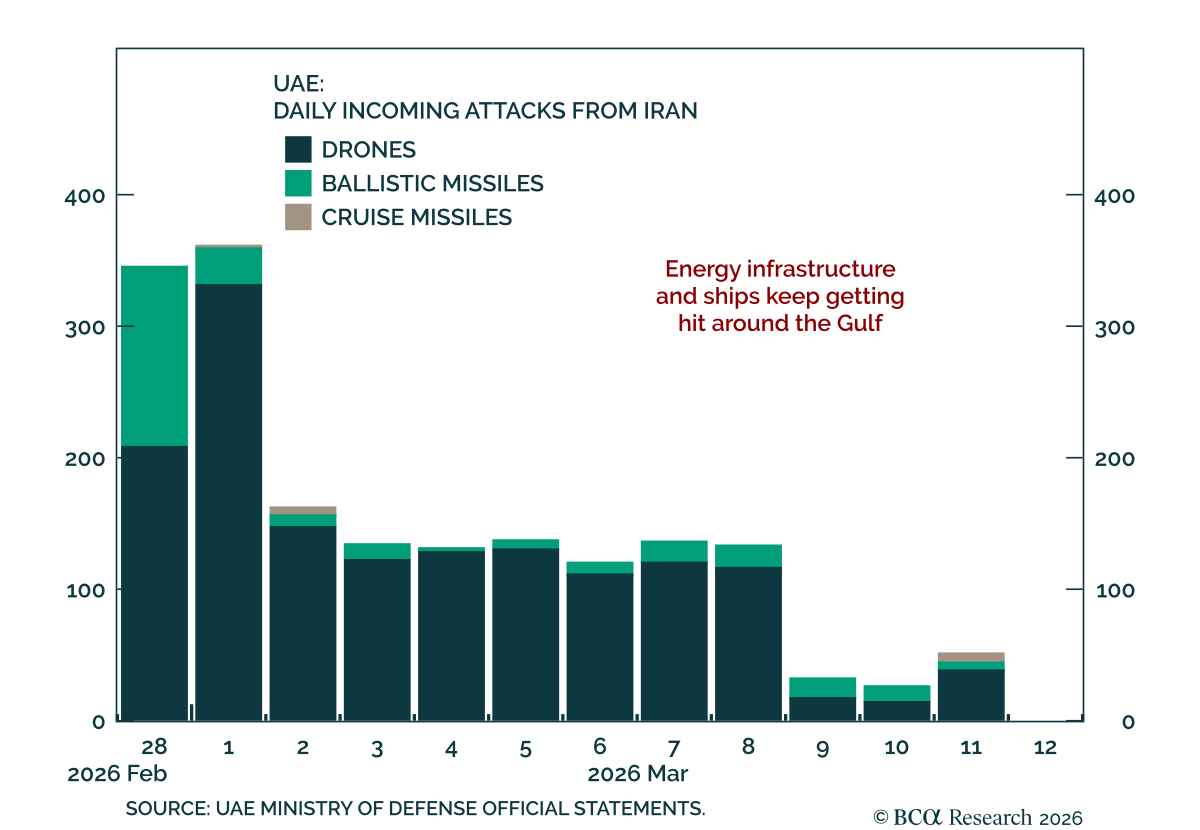

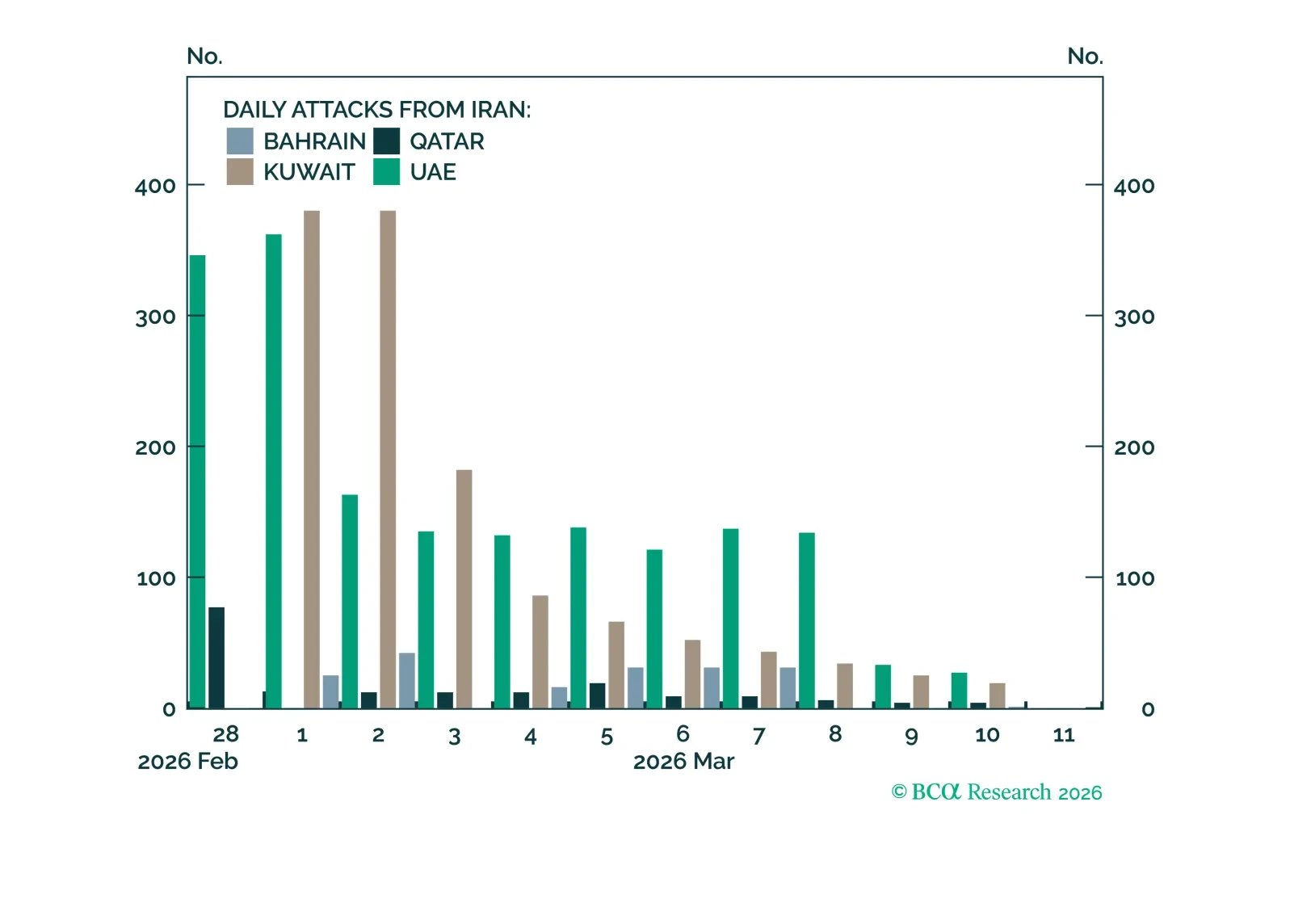

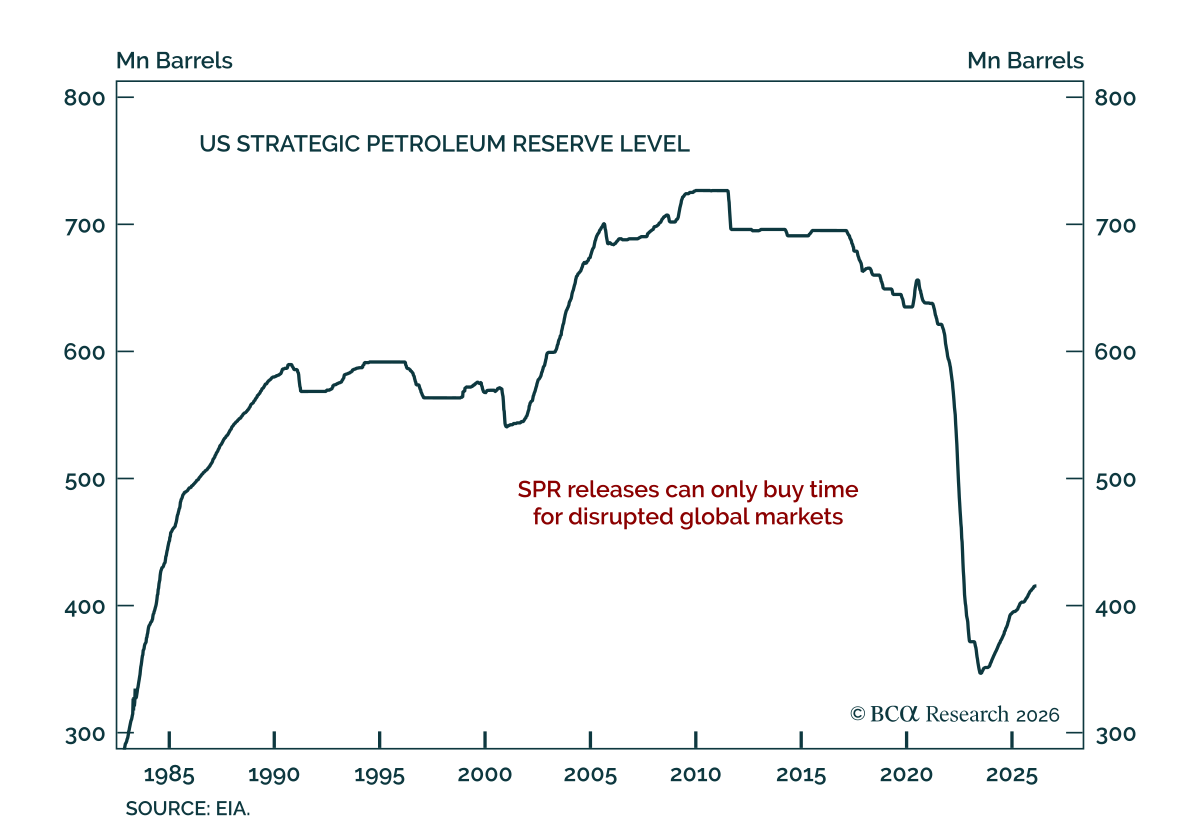

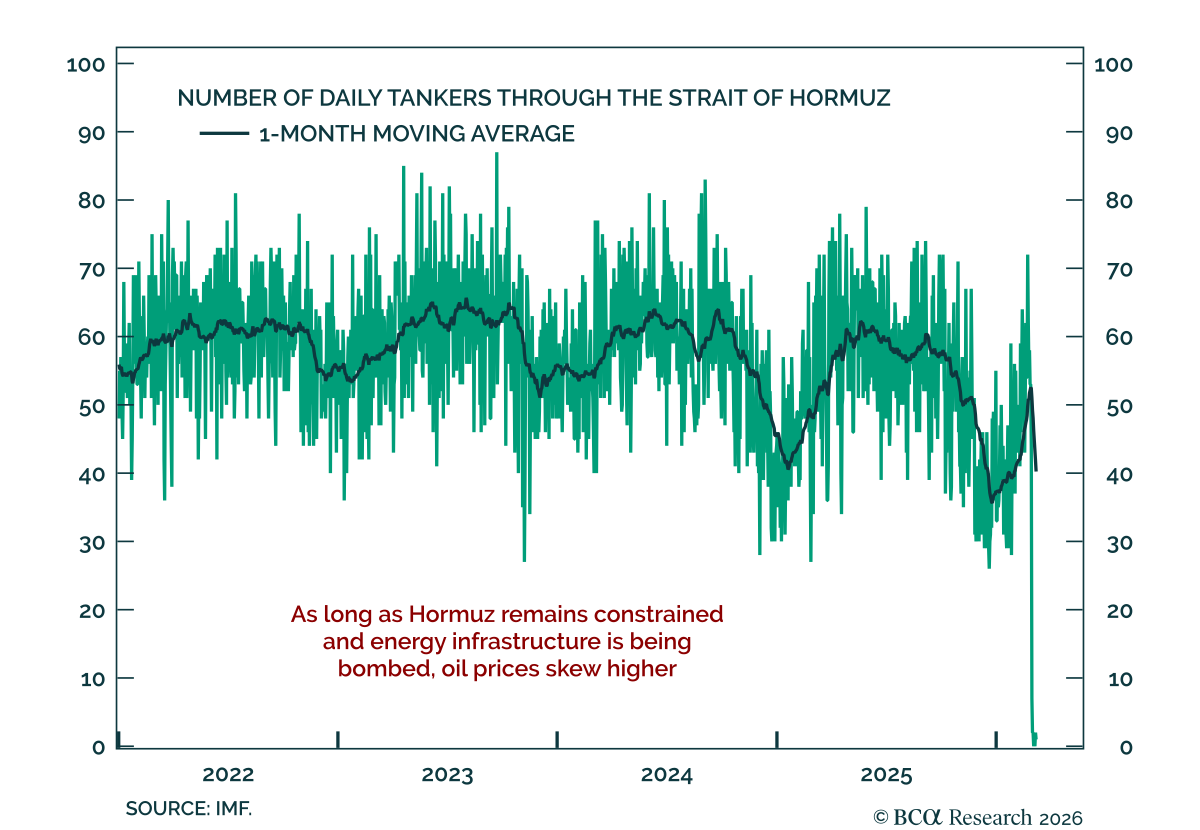

Iran

Regional geopolitical risk is rising for Europe, EM Asia, and South Asia. We adjust our regional risk matrix accordingly.

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

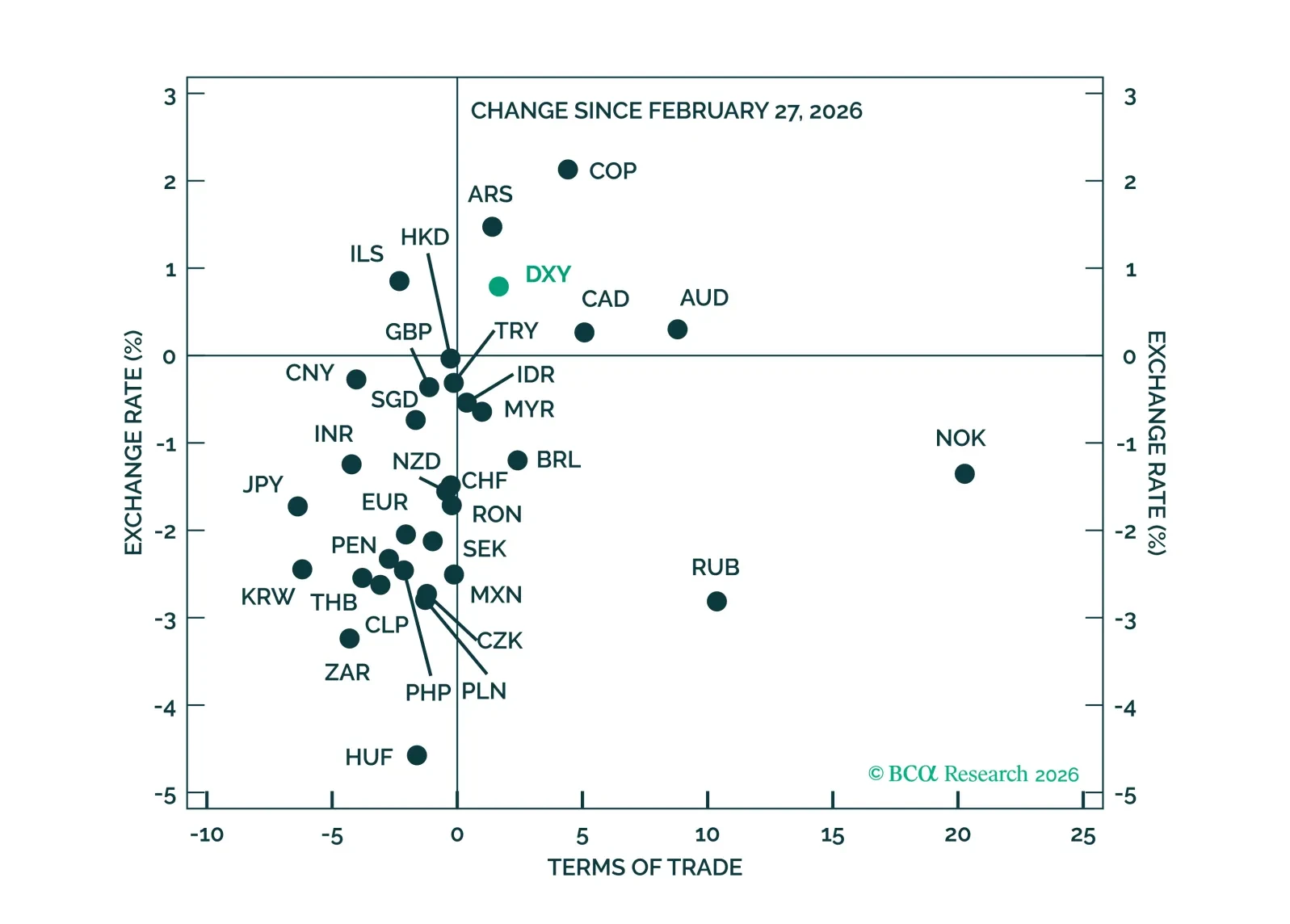

The Iran war remains a terms-of-trade shock rather than a classic flight to safety – for now. As oil risks skew higher, policy repricing and growth differentials should continue to favor a tactical rebound in the USD.

Oil prices will likely rise in the near term, irrespective of developments in the Strait of Hormuz. Given that global share prices have become correlated with crude prices, global stocks will continue selling off. Go short the EM equity index and take profits on our open trades that have benefited from the global risk-on environment.

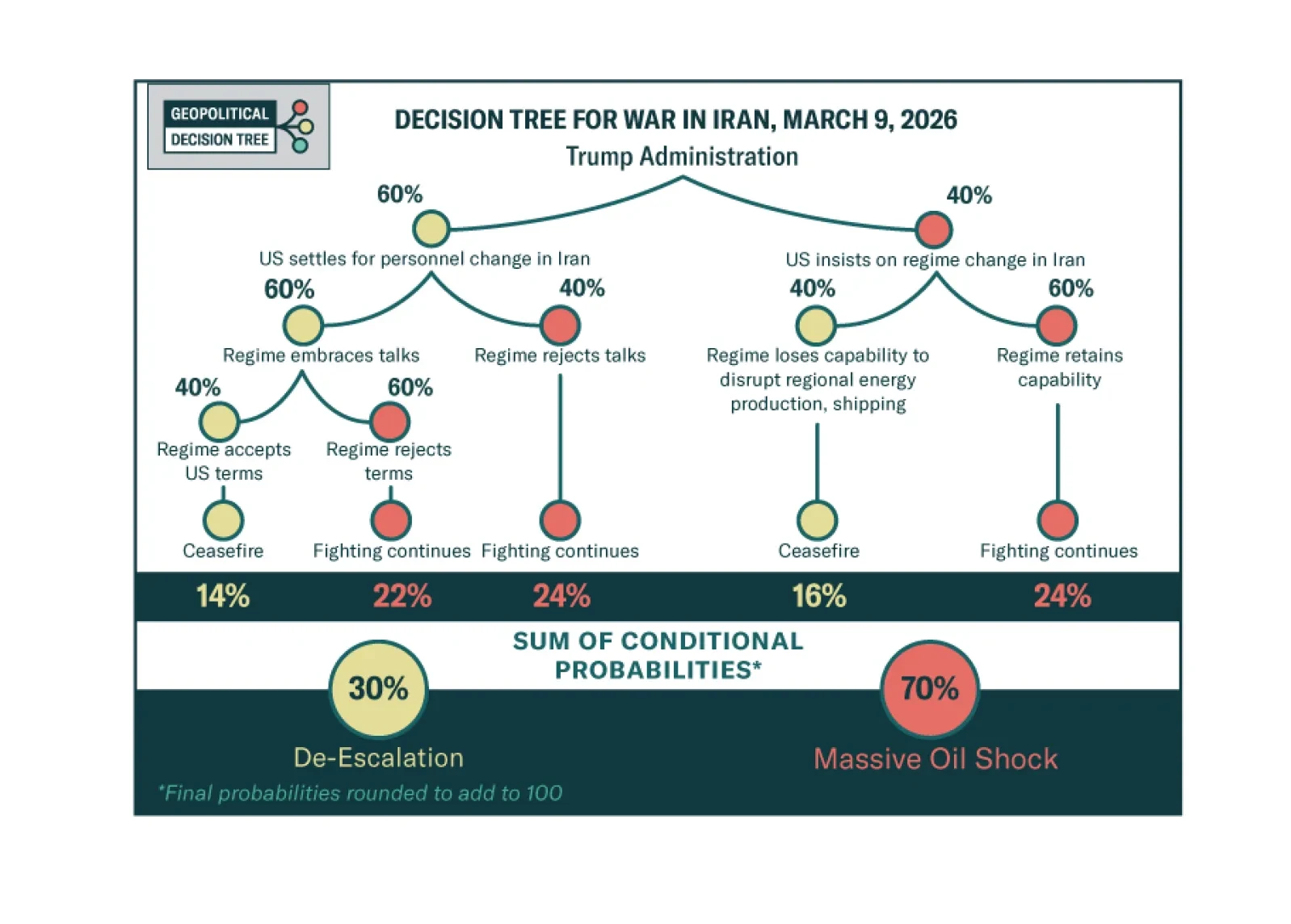

With all eyes on the Strait of Hormuz, BCA Research has created a dashboard of data for your convenience.

Close oil trades tactically, but beware lingering economic costs of the Iran war this year.

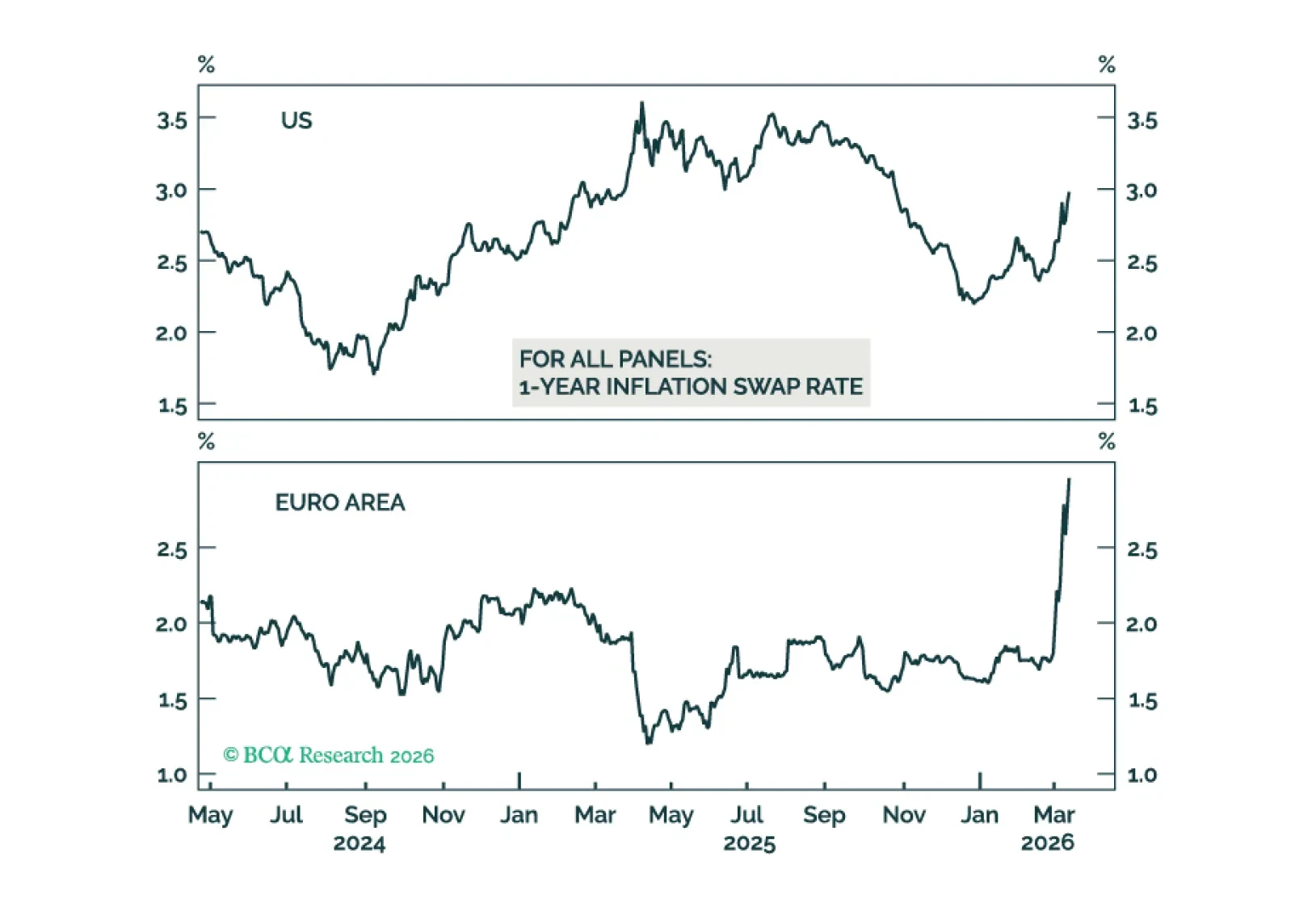

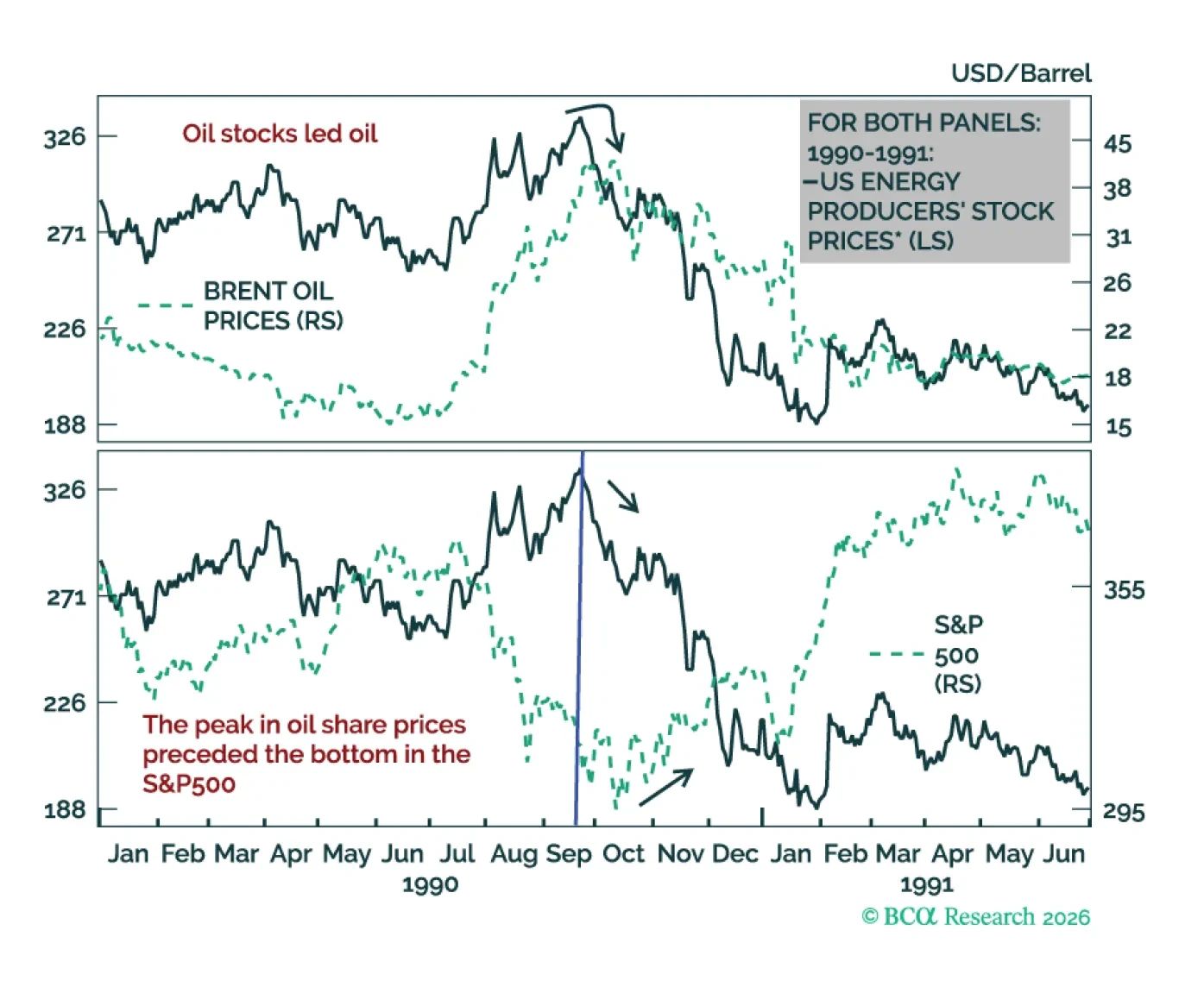

If the 2022 roadmap is any guide, equity markets and cyclical currencies will trough only after confirming that the peak in energy prices is in the rearview mirror. In the very near term, investors should focus on P&L preservation. Reduce exposure to equities, and seek refuge in gold, and inflation-linked bonds (ILBs). Amid a very different demand side than in 2022, today’s supply shock is unlikely to generate lasting inflation, and investors should fade rate-hike odds.