Iran

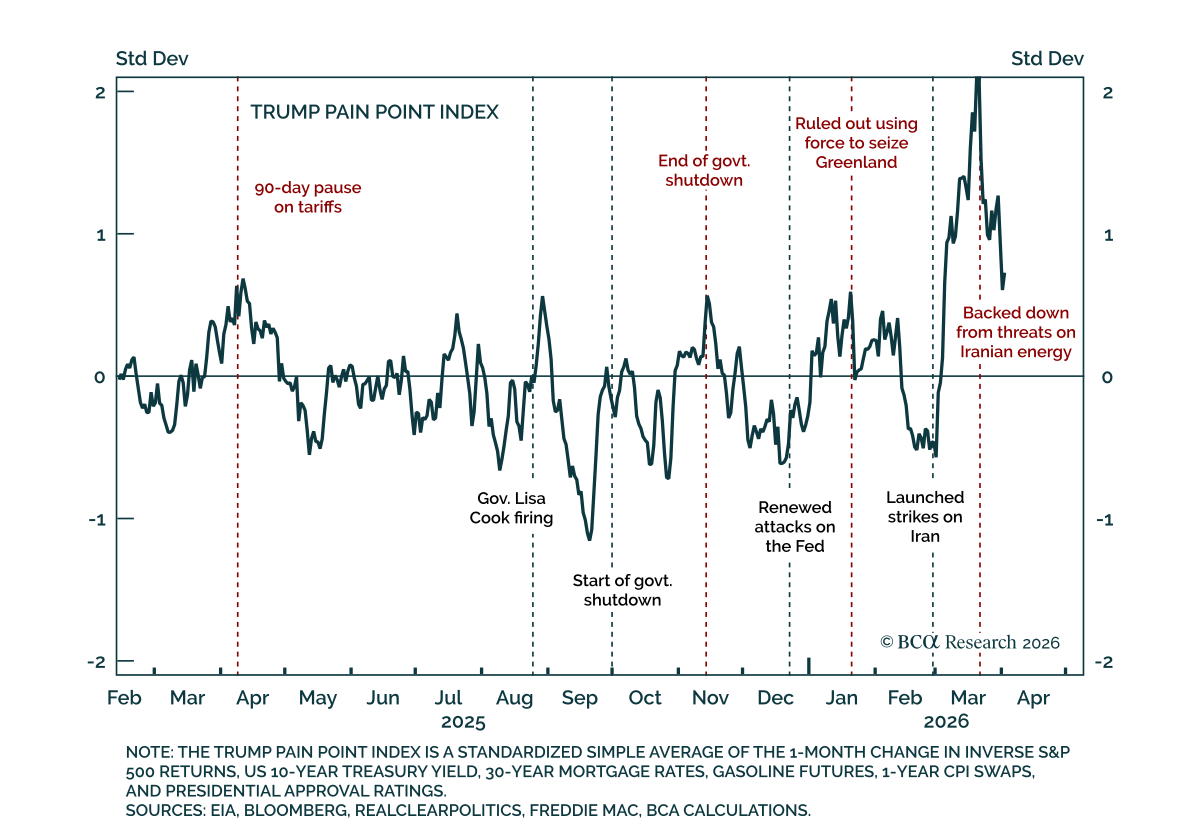

When the ceasefire between Iran and the US was announced on April 8, several clients told us that their geopolitical consultants were pitching a bearish narrative. The US had set up the two-week ceasefire to surge more material and troops to the region, so as to set up the next phase of the conflict. One such advisory firm also pointed out that it was unlikely that the US would hold back on further conflict since it had “already amassed ground troops to the region.”

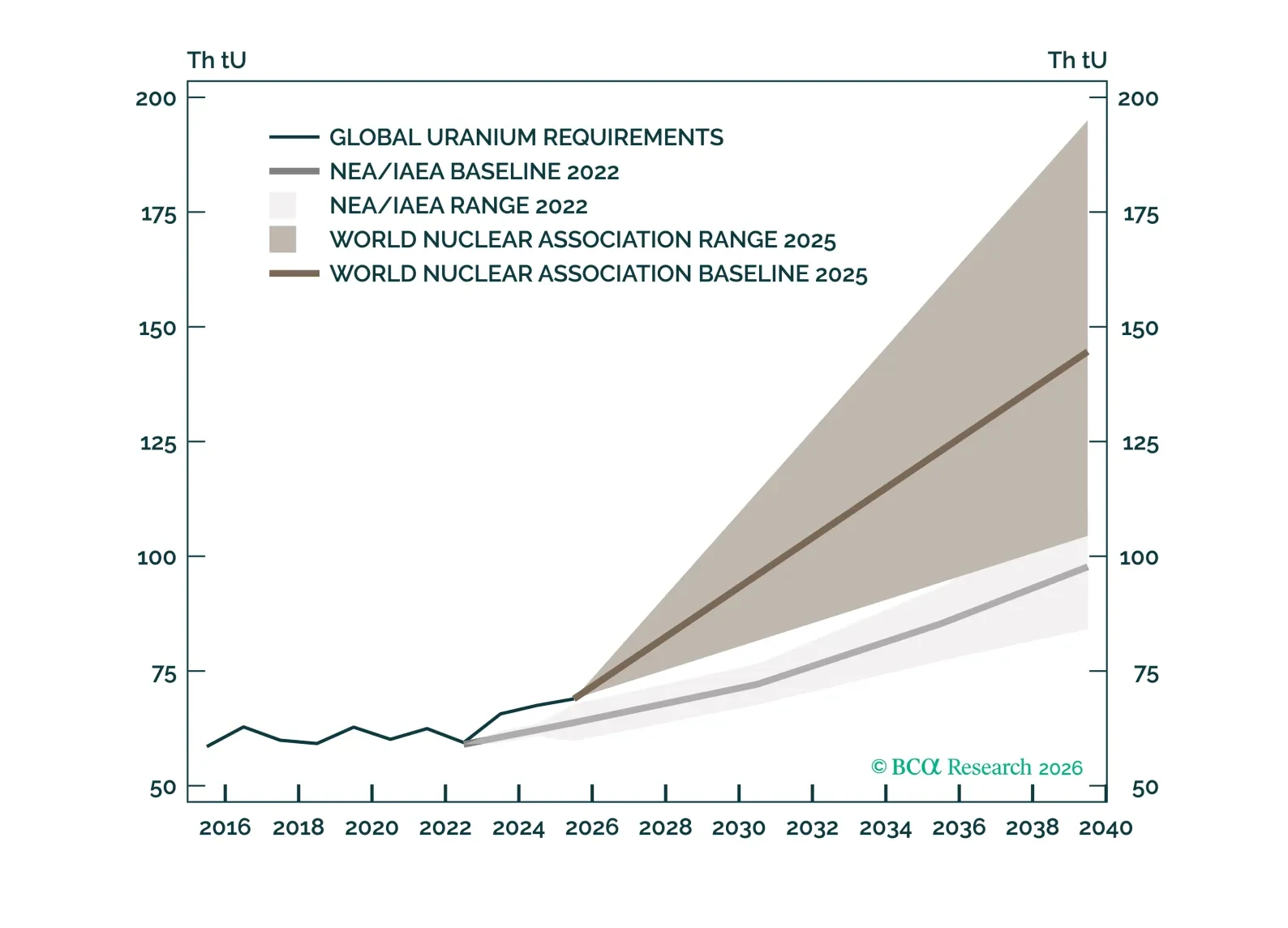

Uranium’s bull market remains intact, supported by structural supply deficits, rising nuclear demand, and tightening fuel-cycle constraints. The Iran war reinforces energy security concerns while disrupting key inputs like sulfur, exacerbating supply risks. With contracting strengthening and policy support accelerating, uranium is re-emerging as a strategic commodity with durable upside.

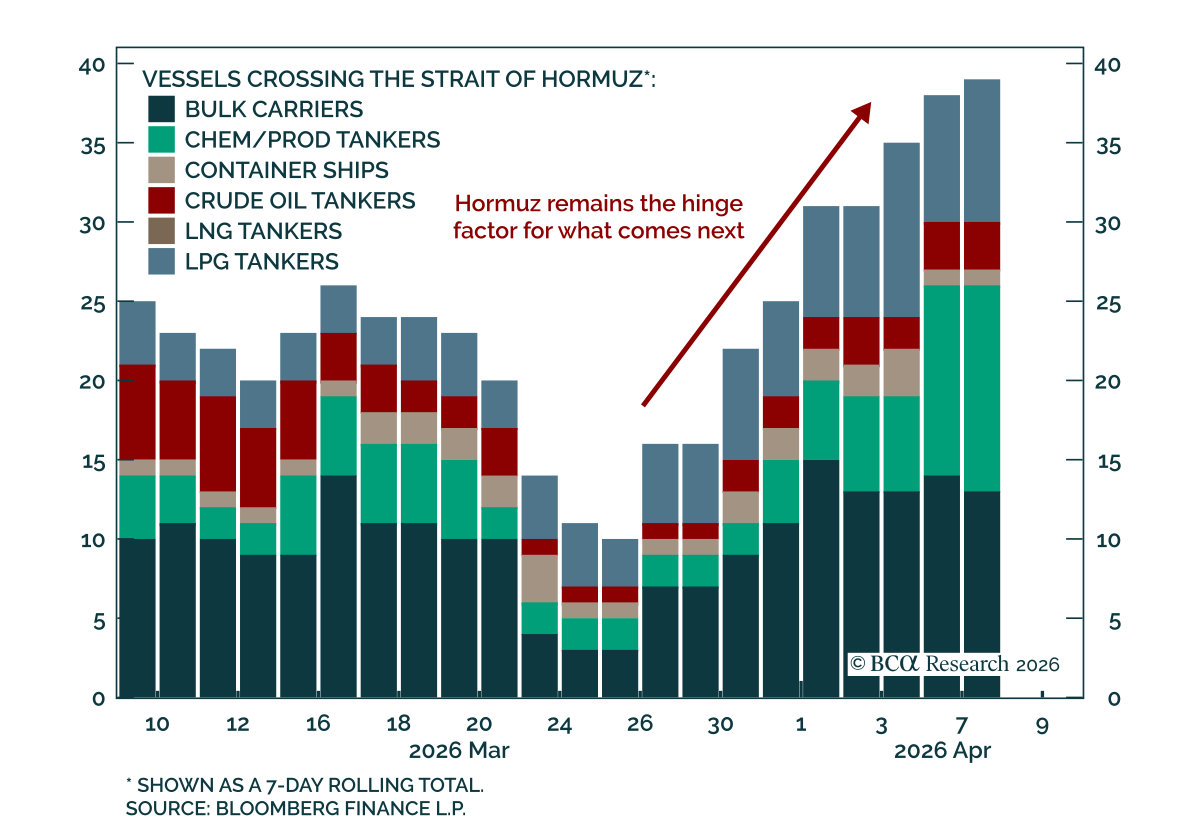

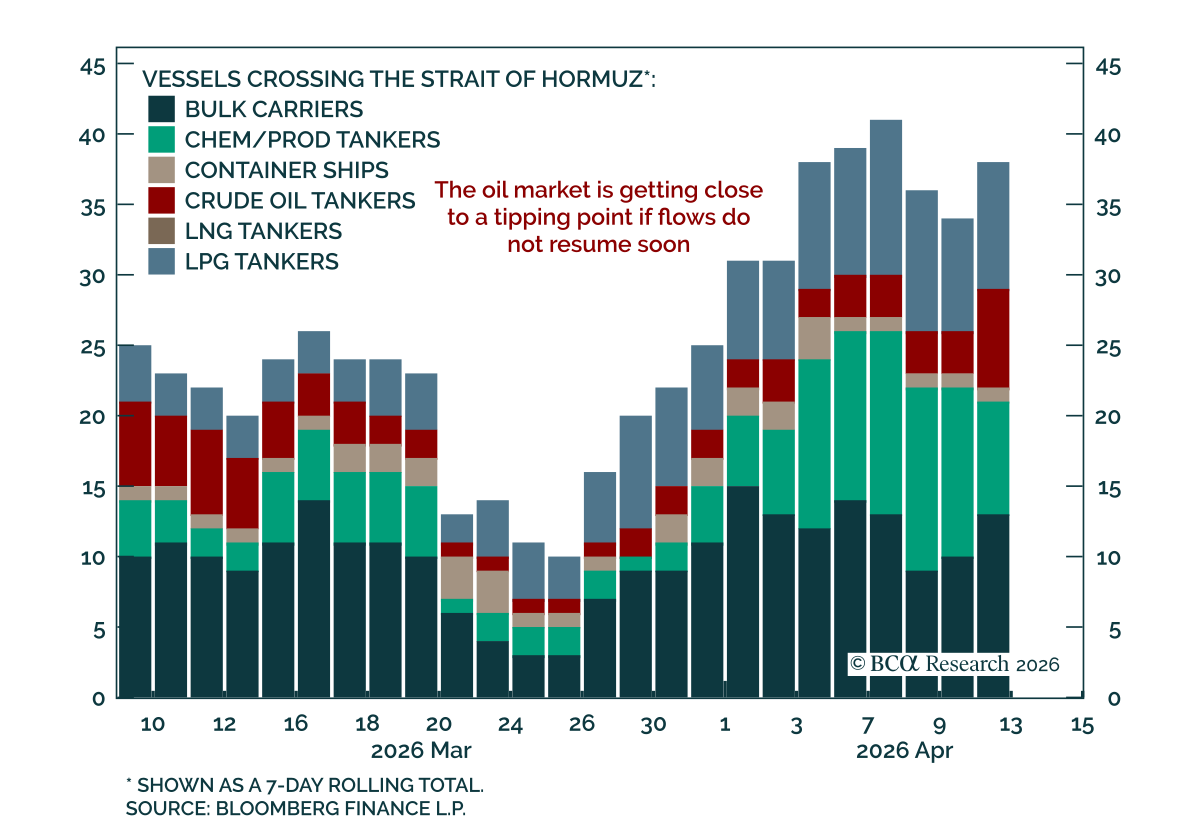

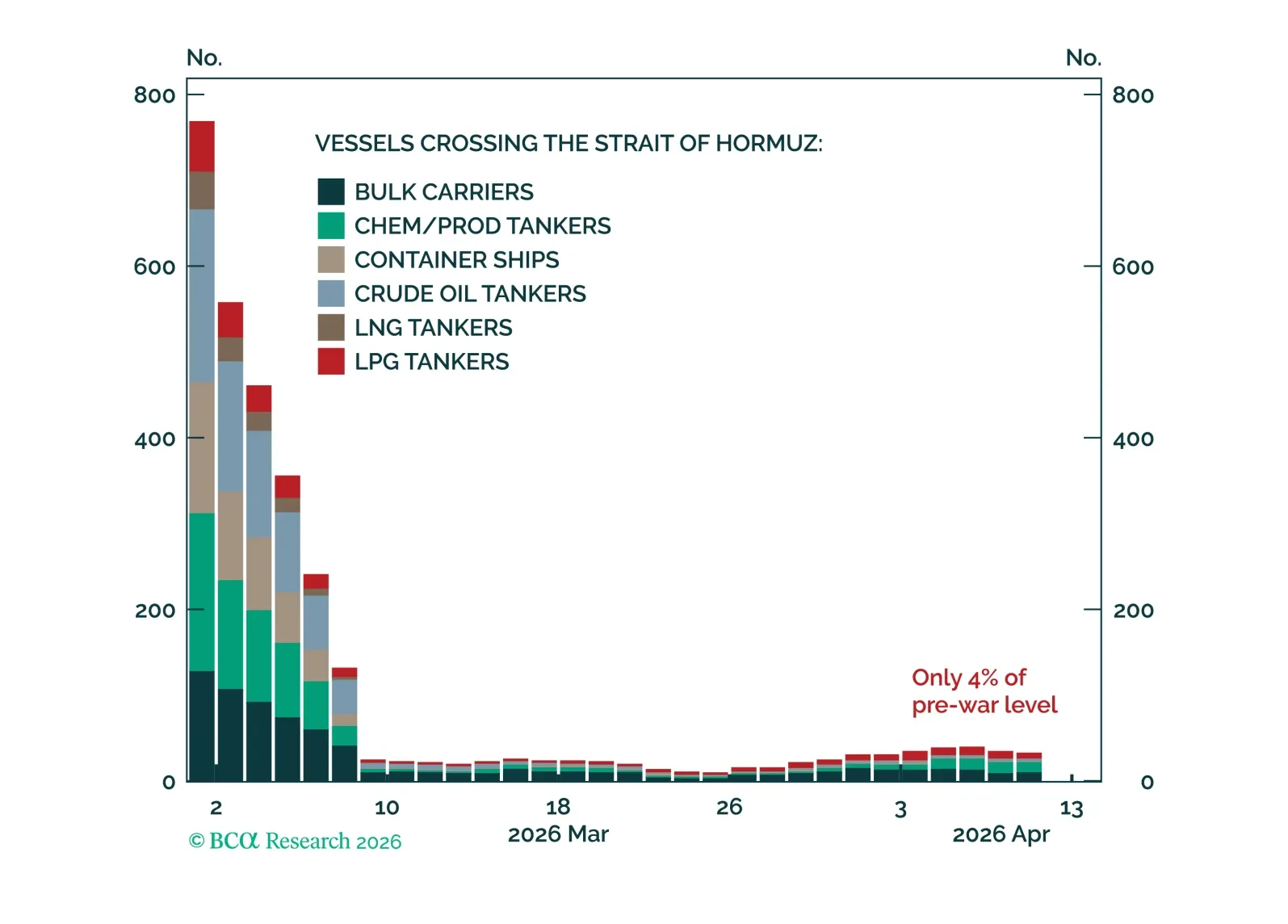

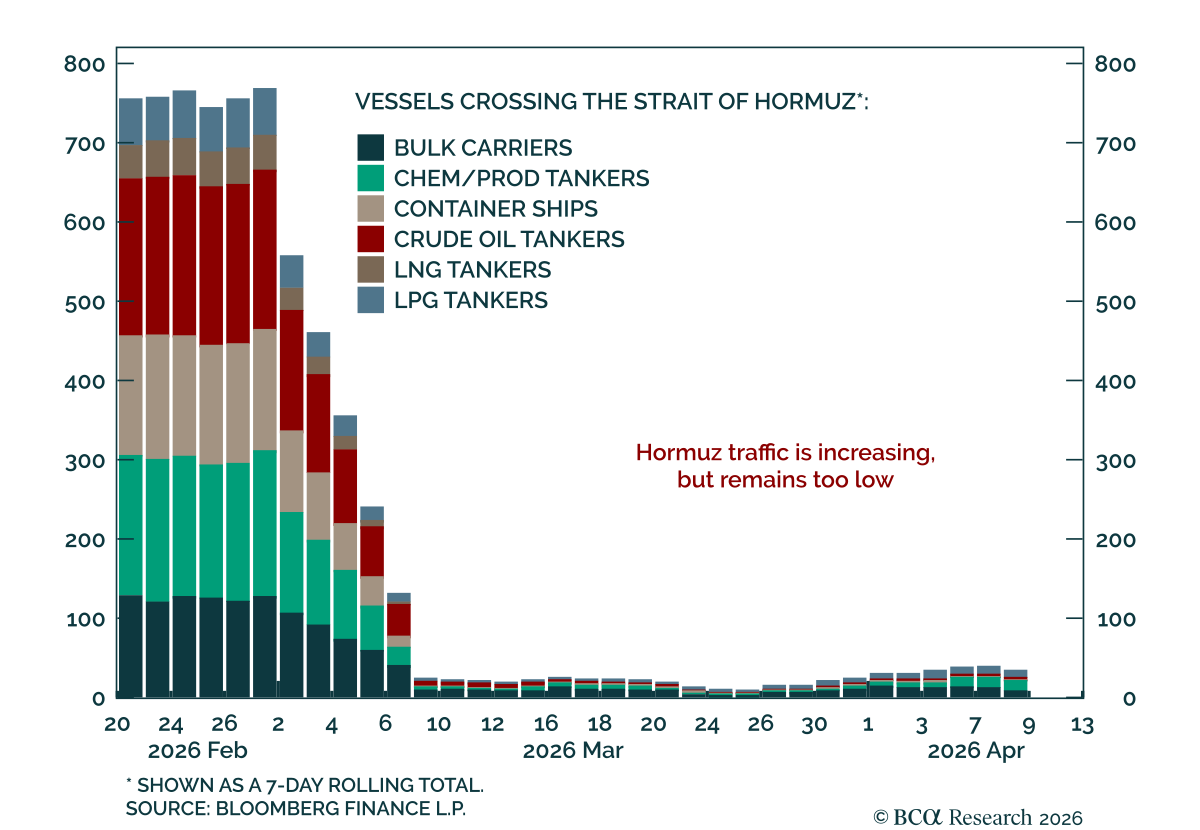

President Trump has announced that the US would impose a blockade on the Strait of Hormuz, in effect exacerbating the partial blockade that has already been in place due to Iran’s threats against shipping in the Persian Gulf. The threat comes after the direct negotiations between Iran and the US in Islamabad failed to make a breakthrough. Oil is up on the news and stock futures are down. How should investors read the situation?

In this report, we deviate from our base case and instead assume that there is an immediate improvement in Hormuz traffic. This exercise allows us to explore how the global oil supply shortfall could eventually be offset if the right conditions are in place.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

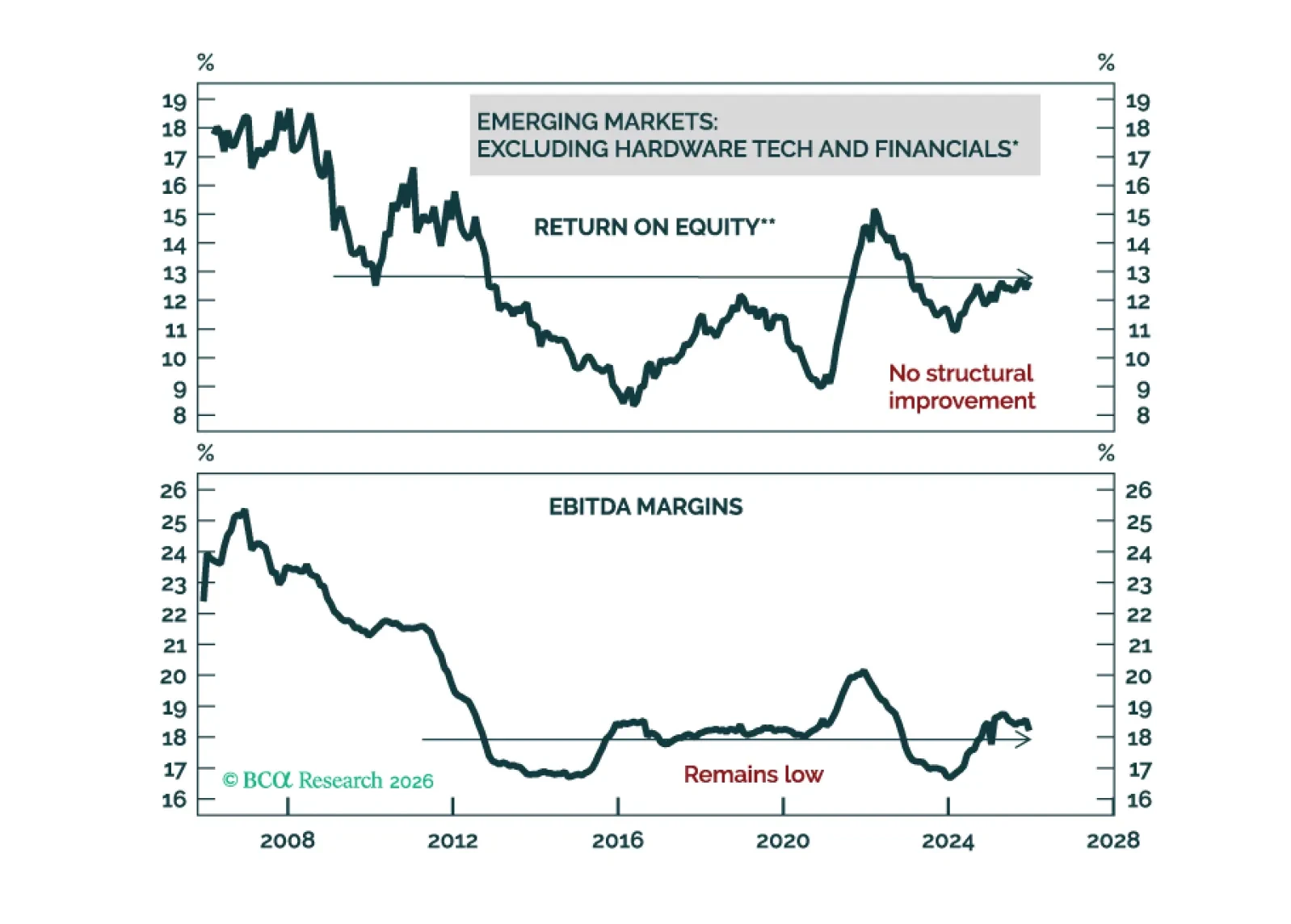

Outside Asian semiconductor producers, EM corporate earnings and profitability have seen little improvement. Despite the ceasefire in the Middle East, the medium-term outlook for EM stocks is still unattractive.