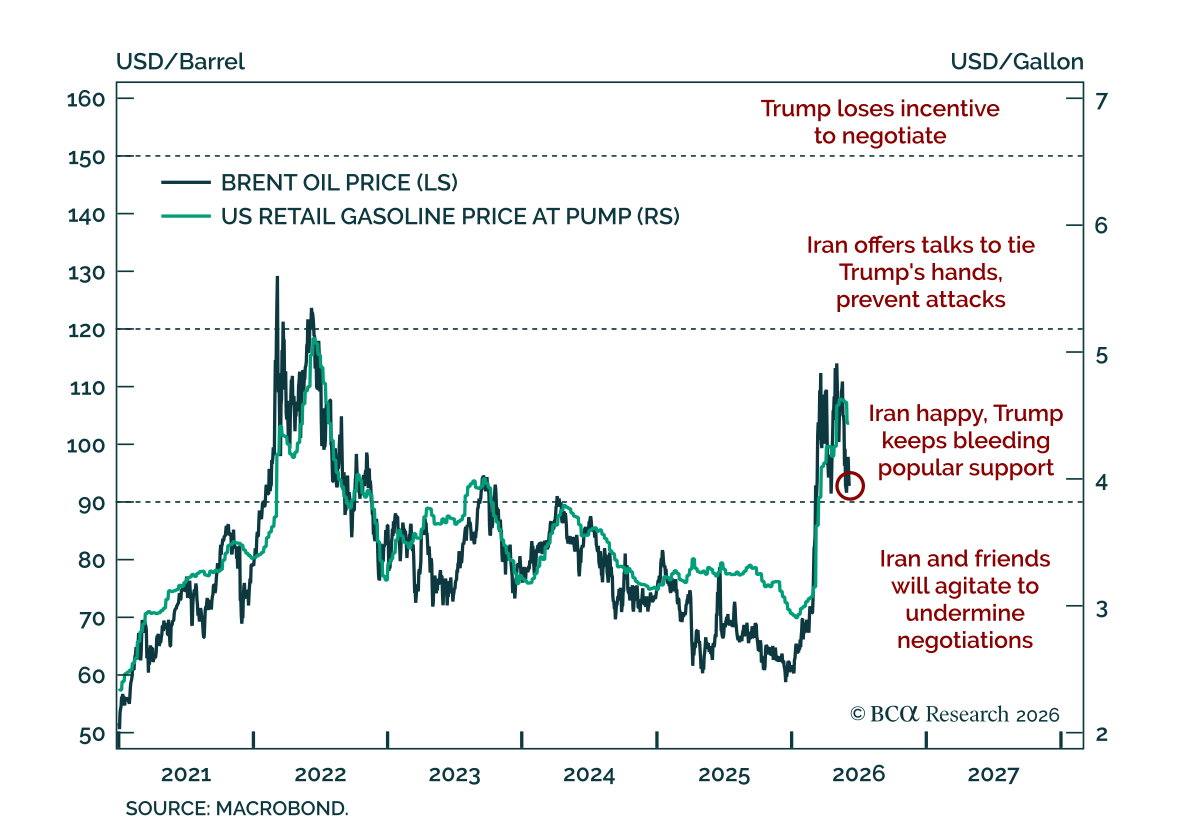

Iran

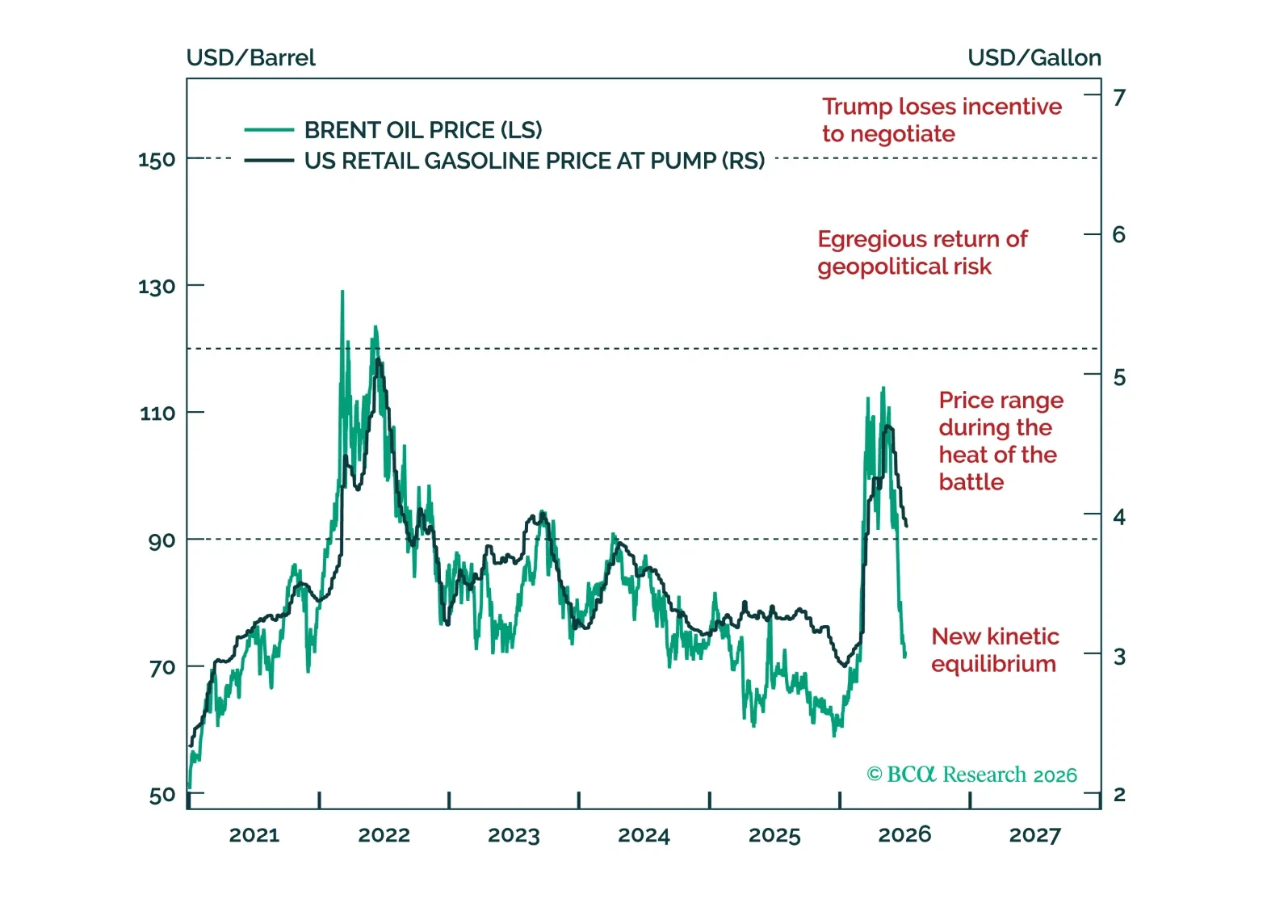

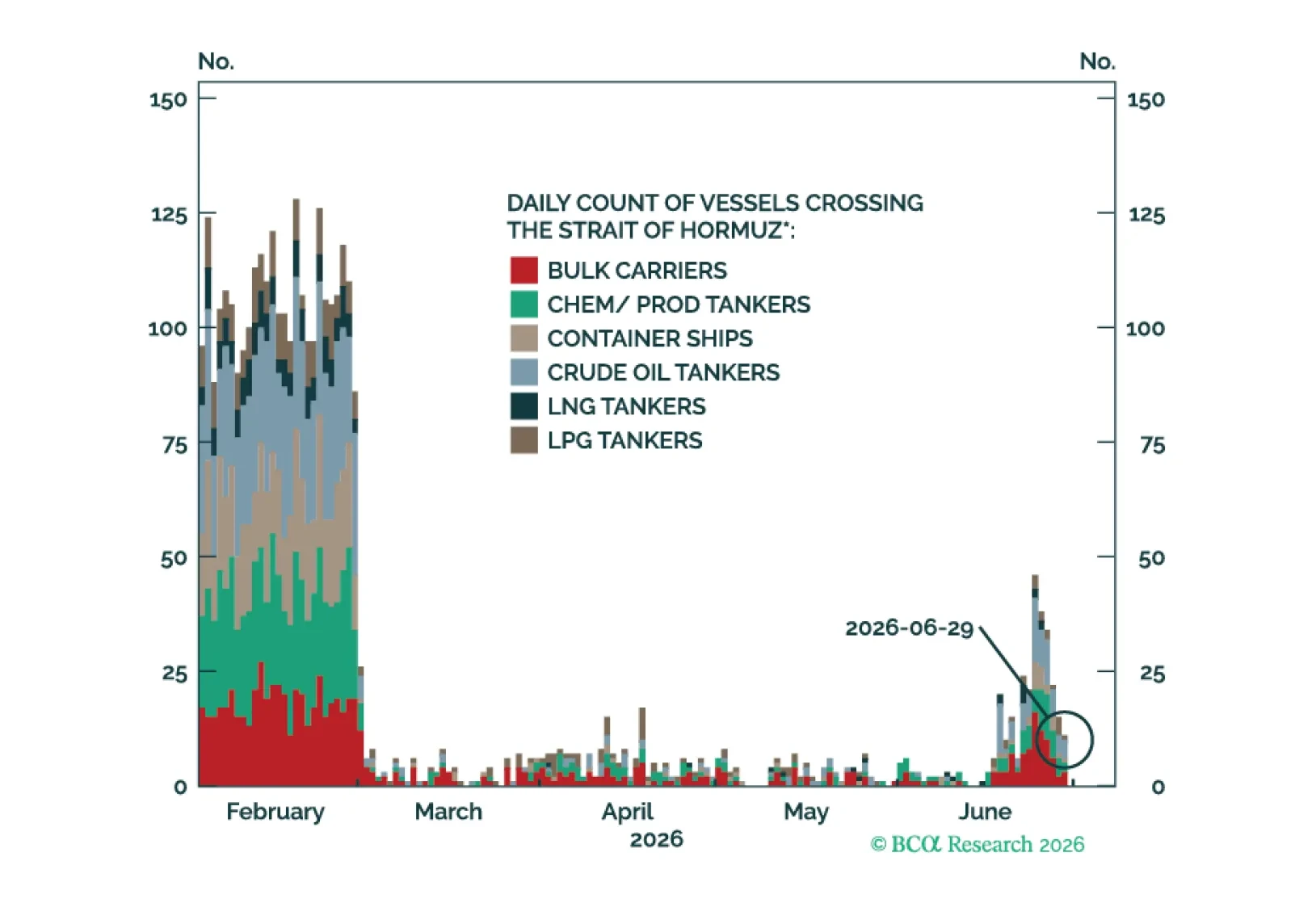

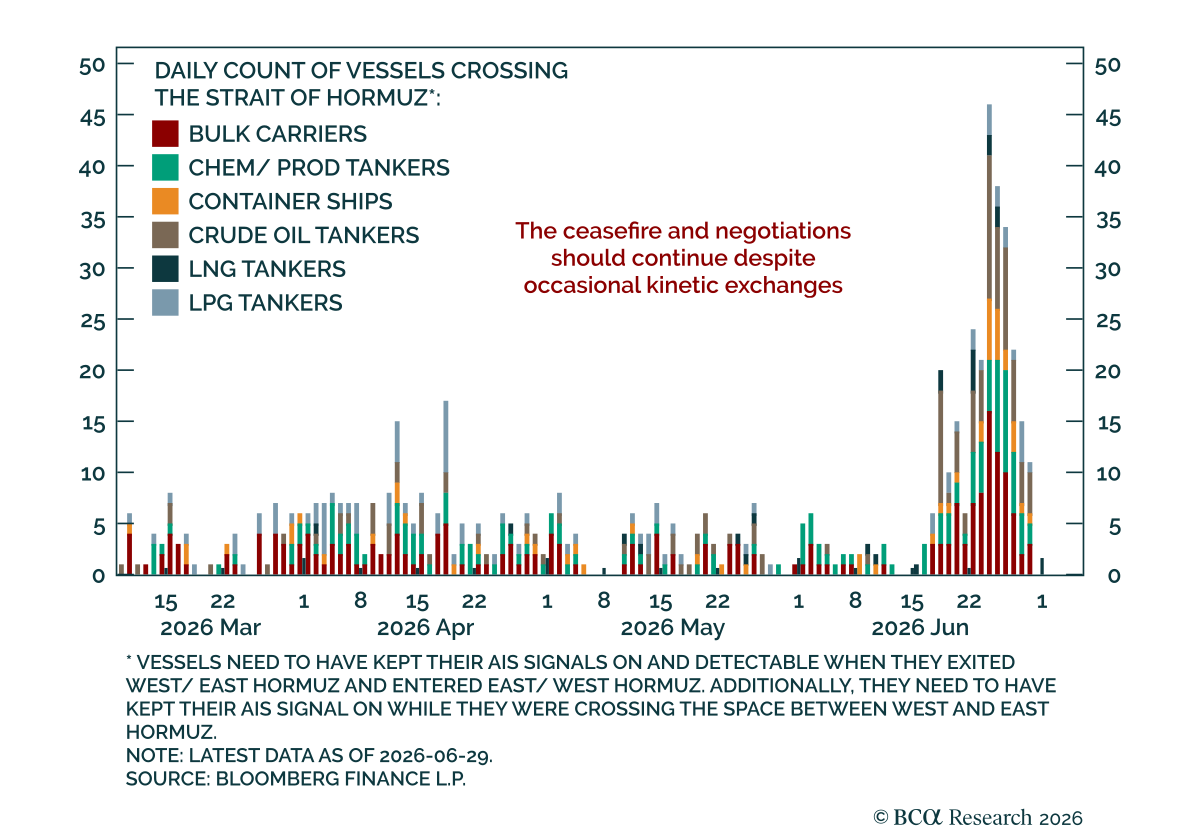

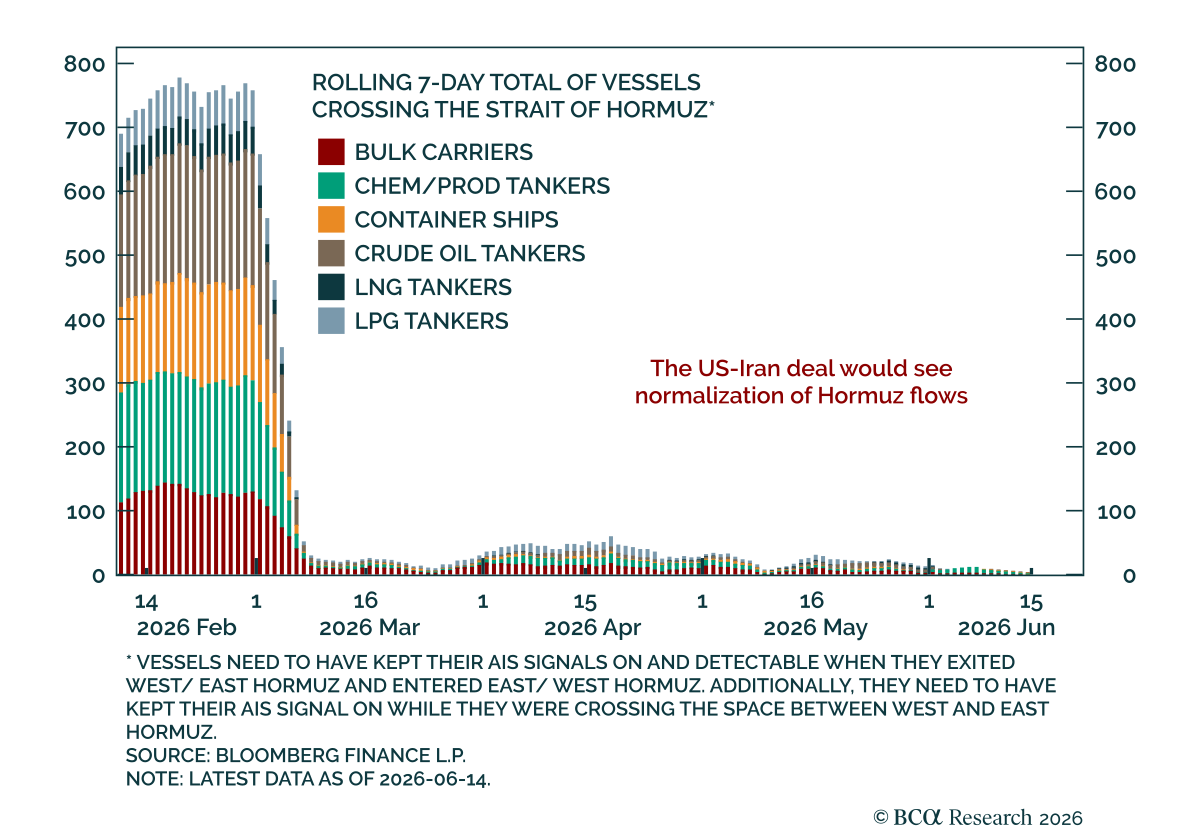

Just as we declared that geopolitical risk has peaked for the year – in yesterday’s Alpha report – President Trump has declared the ceasefire with Iran over after repeated violations via strikes against three tankers in the Strait of Hormuz. That is the life of an investment strategist. But the underlying dynamics continue to play out as we’ve described.

We remain bullish on risk assets given that the Hormuz war has resolved itself and oil prices have declined by even more than we expected. In addition, the macro fundamentals are not flashing any red signs. That said, we remain skeptical that the AI revolution will continue without any hiccups. In fact, a price war may ensue once all the players realize they’re in the commodity – not tech – space.

Geopolitical risk may rotate to Russia/Ukraine in Q3, while the Middle East could reignite in Q4.

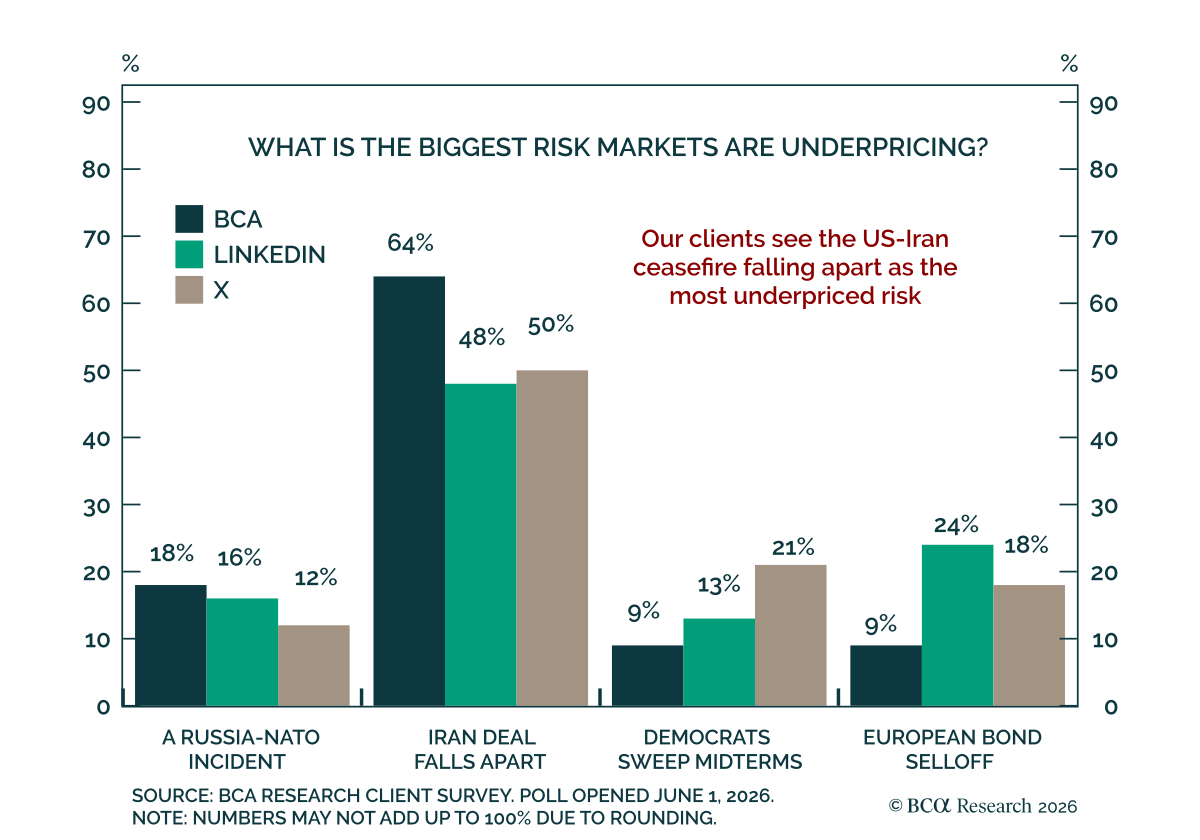

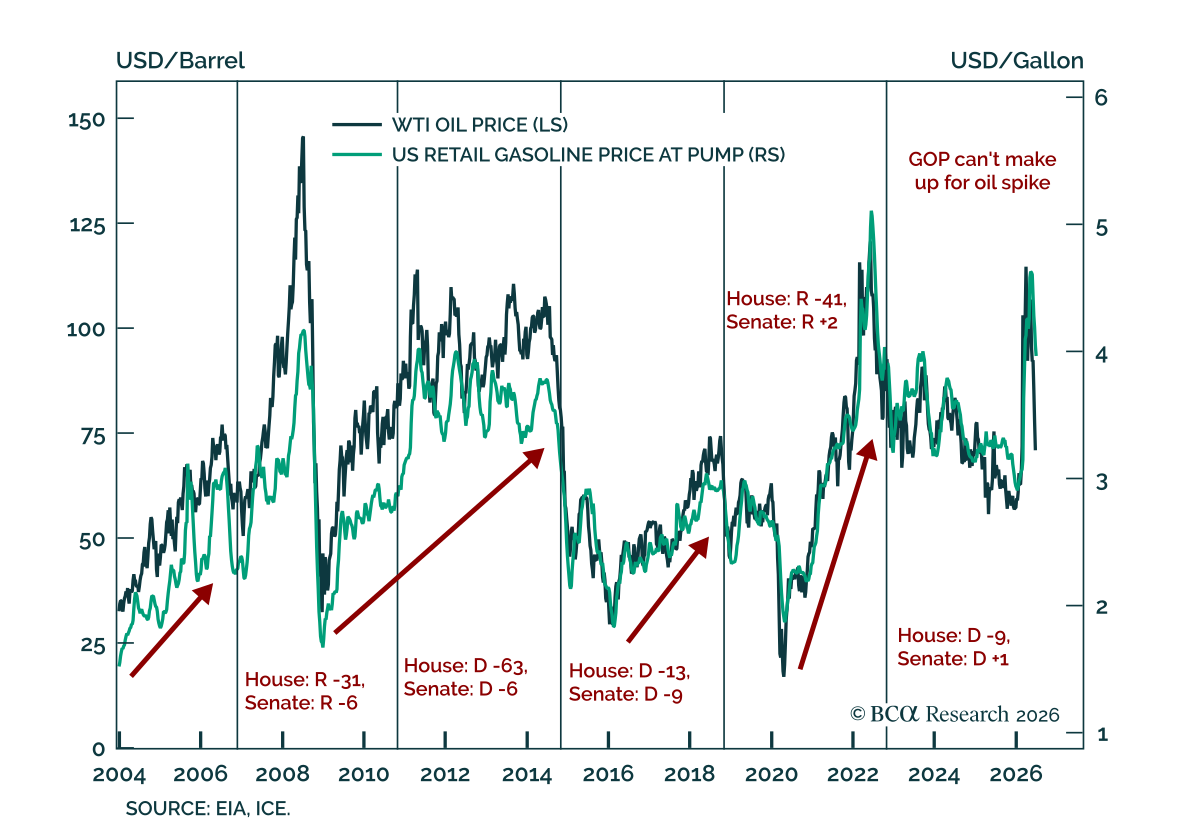

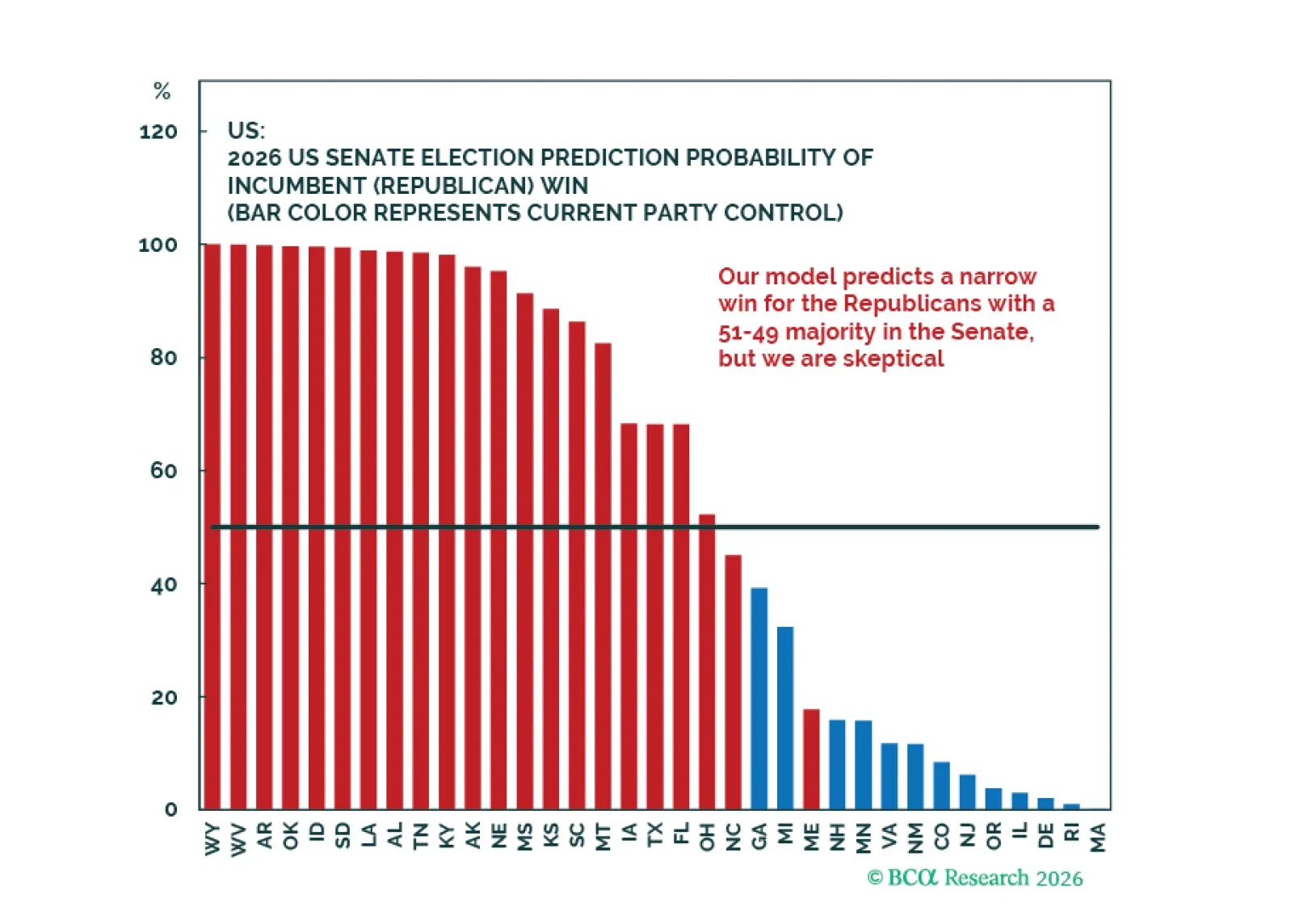

Midterms matter but geopolitics are the main risk this year. Markets will eventually refocus on geopolitical and inflation risks, raising Fed rate hike odds and supporting US dollar and stocks over global counterparts this year.